CA - Dundee Precious Metals: A Safer Way To Get Gold Equity Exposure

2023-05-17 12:03:38 ET

Summary

- Dundee Precious Metals reported another strong quarter, generating FCF of US$65M on the back of rising gold prices.

- The company is swimming in liquidity with over US$530M of cash, following the disposition of its stake in Sabina Gold and Silver Corp.

- The current environment of rising gold prices and rising interest rates creates the perfect storm for Dundee to leverage its liquidity in new acquisitions at attractive prices.

- The company is among the safest equity bets on gold, due to its considerable net cash position, low cost profile, and relatively low political risk of the operating assets.

- Despite the recent bull-run, Dundee remains attractive, with an annualized FCF yield of 17.8% and forward EV/EBITDA much lower than its peers.

Back in November 2022, I wrote an article about the gold producer Dundee Precious Metals (DPMLF)(DPM:CA), highlighting it as a very attractive opportunity in light of geopolitical tensions and economic uncertainty. Since then, the shares have soared about 60%, and it's worth taking another closer look at the company. The recent performance of the company showcases its ability to generate strong cash flows in a rising gold price environment, while the restructuring at Tsumeb has yielded fruit and the smelting facility is now contributing to earnings, instead of being a drag. Dundee has a considerable cash position of US$530M following the disposition of its stake in Sabina Gold and Silver Corp. This puts Dundee in a perfect position to make attractive acquisitions given the rise in the cost of and access to capital in the economy and the sector. The low AISC profile and pretty safe jurisdiction of the operating assets make Dundee one of the lower-risk plays in the gold space. The only downside is that a high AISC producer would theoretically have more torque to rising gold prices, but at the expense of higher risk. In terms of valuation, despite the recent bull-run, Dundee remains attractive as it trades around an annualized FCF yield of 17.8% and Forward EV/EBITDA much lower than its peers.

Operational overview

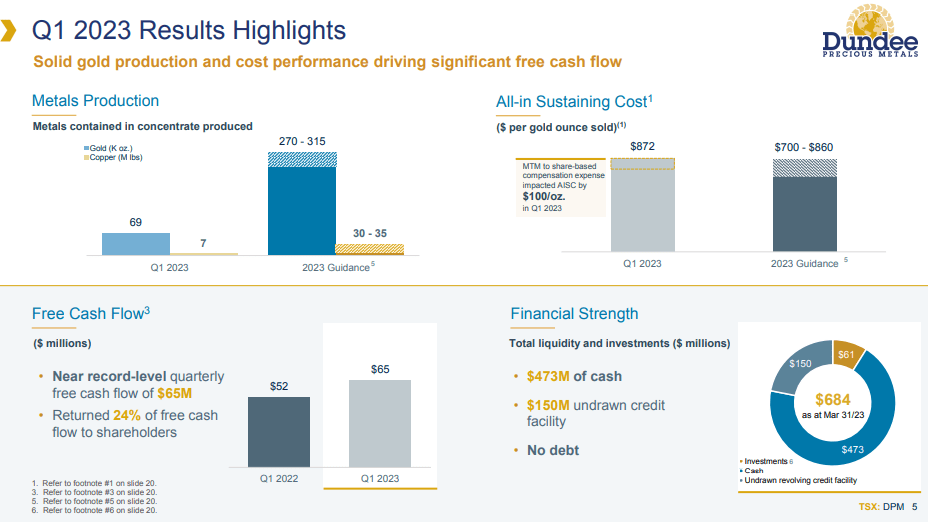

Dundee reported solid Q1'23 figures, with a 9.0% jump in gold production to 68.6koz on the back of higher grades in the Ada Tepe mine (6.31 g/tonne, compared to 3.72g/tonne in Q1'22). The average realized price of Au was US$1,918 (+2.2% YoY). On the other hand, copper production was down 6.7% YoY to 7.1Mlbs due to lower recoveries (78.8%, compared to 85.3% in Q1'22). Realized prices for the metal were lower at US$4.06/lbs (-11.4% YoY). Revenue was slightly up to US$155.8M (+1.3% YoY) while AISC came at US$872/oz (+27.5% YoY) with the increase being mainly due to mark-to-market on share-based compensation, which added around US$100/oz and lower by-product credits.

Q1'23 highlights (Dundee Precious Metals)

Adjusted EBITDA was slightly down to US$68.4M (-1.5% YoY) while free cash flow amounted to US$65M (+24.1% YoY), with the difference being mainly due to US$4.5M reduction in working capital, compared to US$14.3M expansion in Q1'22. Management reported that it's on track to meet its 2023 guidance.

Strong balance sheet, supportive of future expansion

Dundee is one of the very few debt-free companies in the metals and mining space. Instead, it has a large cash pile of US$473.0M and about US$61.0M of investments as of the end of Q1'23. However, the majority of these investments were a 6.5% stake in Sabina Gold and Silver Corp., which was acquired by B2Gold (BTG). As a result of the transaction, Dundee received shares of BTG, which were later sold for cash proceeds of US$56.5M, which should've brought the cash position close to US$530M. On top of that, Dundee has available undrawn credit facility of US$150M, making the company's liquidity position even more impressive.

{kind=link}

The current macro environment of increasing cost of capital makes Dundee's financial position even more valuable. Management could look for attractive projects, which lack financing, and acquire them at attractive terms. However, I think that in the meantime investing the large cash pile into money-market securities, which could potentially add US$20-25M to the bottom line on an annual basis, makes sense.

Projects updates

Since the beginning of the year, there have been a number of positive developments related to Dundee's projects:

- Chelopech - Mine life was extended by one year to 2031 and replace about half of 2022 production by adding 1.1M tonnes to reserves.

- Ada Tepe - The company managed to increase the recoverable reserves by about 66koz, translating into approximately 16.5koz of the annual increase in production to 2026. Also, an updated Technical report was published, indicating after-tax NPV of US$343M, using a gold price of US$1,750/oz and total operating cost of US$515/oz.

- ?oka Rakita - Dundee released drilling results from the ?oka Rakita deposit, which is in a very close proximity of approximately 3 km to the Timok project. The results are promising, indicating interception of high-grade intercepts.

- Tsumeb - During Q1'23 Tsumeb become once again a contributor to the bottom line as net income of US$3.0M was reported, compared to a loss of US$15.1M, when restructuring costs were incurred.

Valuation discussion

Dundee's market cap is around US$1.4B at current prices. In the current gold price environment, I estimate that Dundee could generate FCF north of US$250M for the year. This indicates FCF yield of around 17.8%, which seems attractive. When accounting for the large net cash position, the unlevered FCF metric is around 28.4%.

In terms of forward EV/EBITDA, Dundee appears to be trading at a discount to peers, even after the recent surge in its share price. In theory, the discount could be attributable to the supposedly more risky profile of the company. However, I think, in reality it's the opposite - Dundee is much safer than its peers.

Superior risk profile

Besides the gold price risk, which is common for all miners in the sector, I like to highlight some company specific key risk areas.

Political risk

Many miners have operating assets in countries where the rule of law and property rights are eroded. In the case of Dundee, the two operating mines are located in Bulgaria - an EU member state, which is ranked 32nd in the economic freedom index of the Heritage Foundation - much higher than most countries in Africa and South America, where many mines are located. At the same time, it has to be noted that Dundee has a development project in Ecuador, which could be a source of high political risk. The project has already faced some problems with the permitting. It's unclear whether the project will be built at all. However, I doubt that the market assigns much value to it anyways.

Interest rates risk

While interest rates are increasing for the economy as a whole, the effects of that differ greatly from company to company. Companies with high levels of debt face an increase in interest costs and possible difficulties rolling its liabilities forward. In the case of Dundee, the company has no debt and large cash position, which could earn interest if invested in money-market securities or used for expansion.

Conclusion

Dundee Precious Metals are well positioned to continue to thrive in the current environment. The cash position and debt-free profile make the company more resilient to rising interest rates than peers, while the operating mines are located in a politically stable jurisdiction. Despite this relatively safer risk profile, the company trades at a considerable discount to its peers. In terms of FCF yield, Dundee trades at around 17.8% FCF yield on a levered and 28.4% on unlevered basis, which seems attractive.

For further details see:

Dundee Precious Metals: A Safer Way To Get Gold Equity Exposure