CA - Dundee Precious Metals: Another Record Quarter

2023-08-03 13:11:42 ET

Summary

- Gold miners have generally underperformed compared to the price of gold due to tightening monetary policies and inflationary pressures.

- Dundee Precious Metals stands out as an exception with a 35% rise in shares and strong Q2 results.

- Dundee has managed to control costs and report lower all-in sustaining costs, leading to record profitability and free cash flow.

- The company has a pristine balance sheet, is committed to increased capital returns, and offers leverage to future gold prices via an exciting growth pipeline.

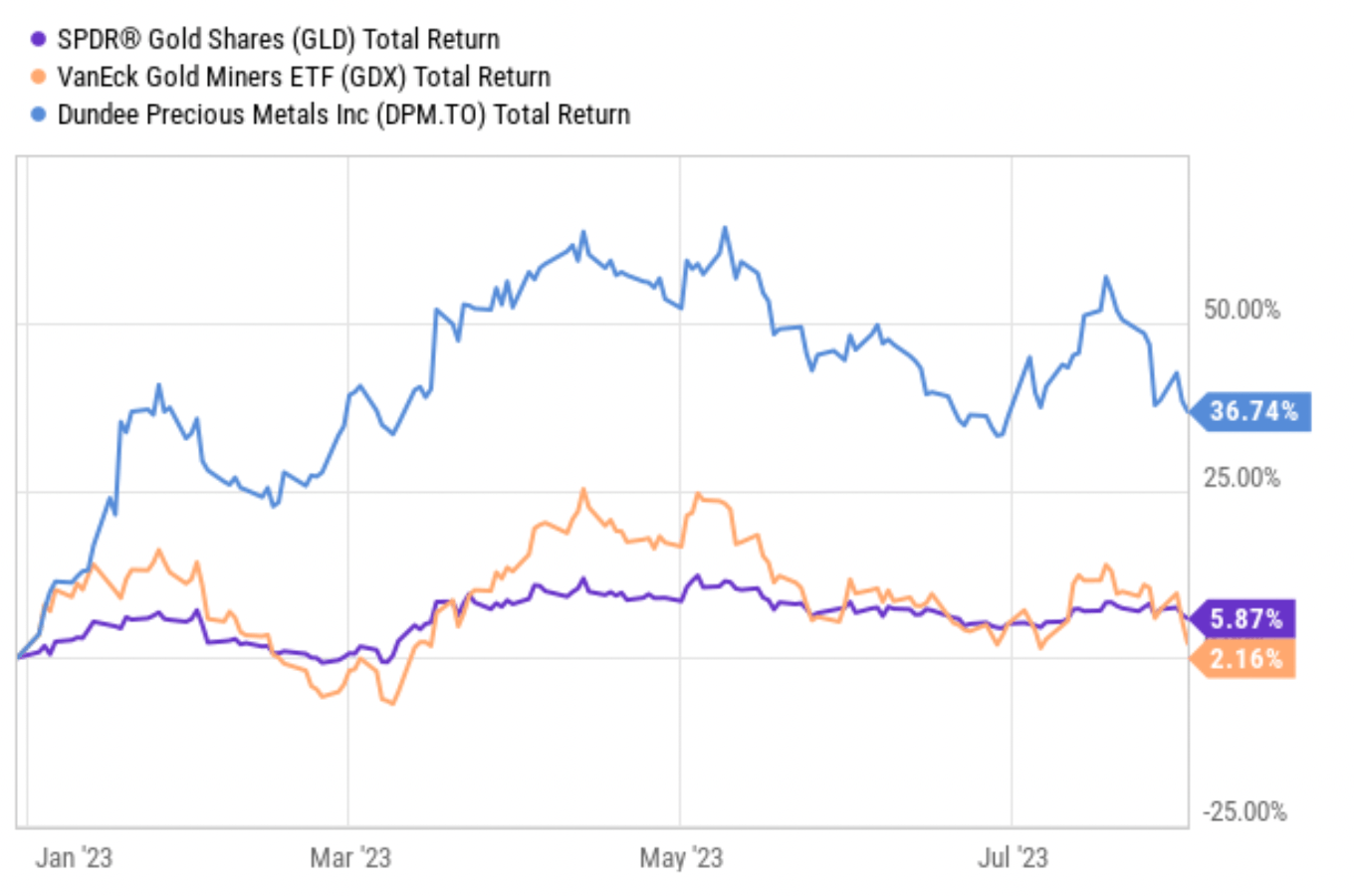

Gold miners have had a disappointing performance since the beginning of the year, despite the strong gold prices. Year-to-date, gold miners have generally underperformed compared to the price of gold itself. This can be attributed to the constraints on the price of gold due to tightening monetary policies worldwide, while inflationary pressures have hit miners hard, especially considering the capital-intensive nature of their business. As a result, profit margins have significantly contracted, to the extent that some miners are now producing little or no free cash flows at current gold prices.

Against this trend, Dundee Precious Metals (TSX: DPM:CA ) ( DPMLF ), a Canadian intermediate gold miner with operations in Bulgaria (Chelopech and Ada Tepe), a smelter operation in Namibia (Tsumeb), and undeveloped projects in Serbia (Timok) and Ecuador (Loma Larga), stands out as a clear exception. Despite a recent 20% sell-off, the company's shares have risen around 35% year-to-date.

Returns year-to-day of gold, the VanEck Gold Miners ETF (GDX), and Dundee Precious Metals (YChart)

{kind=link}

In the midst of the Q2 2023 earnings season, while many miners are disappointing due to rising production costs, Dundee, on the contrary, has recently released exceptionally strong results for the quarter. The key differentiators lie in its superior ability to control costs and its overall low-cost, high-margin assets.

While all-in sustaining costs (AISC) are increasing for many other companies in the sector, Dundee has managed to report a lower quarter-on-quarter AISC, down 16% from $872 in Q1 2023 to $733 per ounce. As a result, the average AISC during H1 2023 was around $802 per ounce, well below the sector's average of around $1200-1300 per ounce. Remarkably, AISC has also decreased on a year-to-year basis, down 7.5% from $792 in Q2 2022.

Several factors have contributed to this achievement. Increased volumes of gold sold were driven by improved mine sequencing and operational optimizations. Furthermore, a reduction in treatment and freight charges at Chelopech was achieved by diverting a higher fraction of concentrates away from Tsumeb and towards lower-cost third-party smelters, a trend expected to continue throughout the rest of the year. These cost reductions were partially offset by higher labor costs and lower byproduct credits due to lower volumes and realized prices of copper.

One other crucial element to consider is energy costs. In 2023, energy prices have come down, leading to decreased power costs for Dundee. Although the company no longer qualifies for state subsidies, the cost per megawatt hour is still below what it was last year when the subsidy was in place. Diesel and cement costs have also eased and are expected to continue on a declining trajectory. Overall, management has expressed confidence in achieving its annual guidance for AISC of $700-$860 per ounce for the full year.

The ability to control costs has translated into record profitability. While gold prices are still below their all-time highs, they have averaged record prices in the last two quarters. However, this hasn't been reflected in the financial results of most miners. Conversely, Dundee's strong cost performance is allowing the company to fully capitalize on the current robust pricing environment. Additionally, strong production figures have boosted its bottom line, making Q2 a record quarter for the company from multiple angles.

Gold production for the quarter amounted to 76,000 ounces, up 4% compared to the same period last year, and it is on track with guidance for 270 to 315 thousand ounces for the full year. The average realized gold price was $1,961, a record for the company. Revenues reached $168 million, up 25% year-on-year, driven by higher production figures and the higher realized gold price. Cost of sales amounted to $83 million, unchanged compared to the same quarter last year.

Consequently, the company achieved a record free cash flow of $71 million for the quarter. Even with capital expenditures weighted towards the second half of the year, Dundee can generate around $250 million of free cash flow for the full year at current gold prices. With a market capitalization of around $1.25 billion and a cash position of $542 million, the company is trading at an attractive EV/FCF multiple of around 3x.

The company's substantial cash position was recently increased with the proceeds from the divestment of B2Gold shares following its acquisition of Sabina. The question now is how this cash will be used. Certainly, it is needed to advance the company's various growth initiatives, both greenfield and organic. Additionally, shareholders can expect increased returns going forward. It's worth noting that while Dundee's main Bulgarian assets are high margin, they have relatively short mine lives.

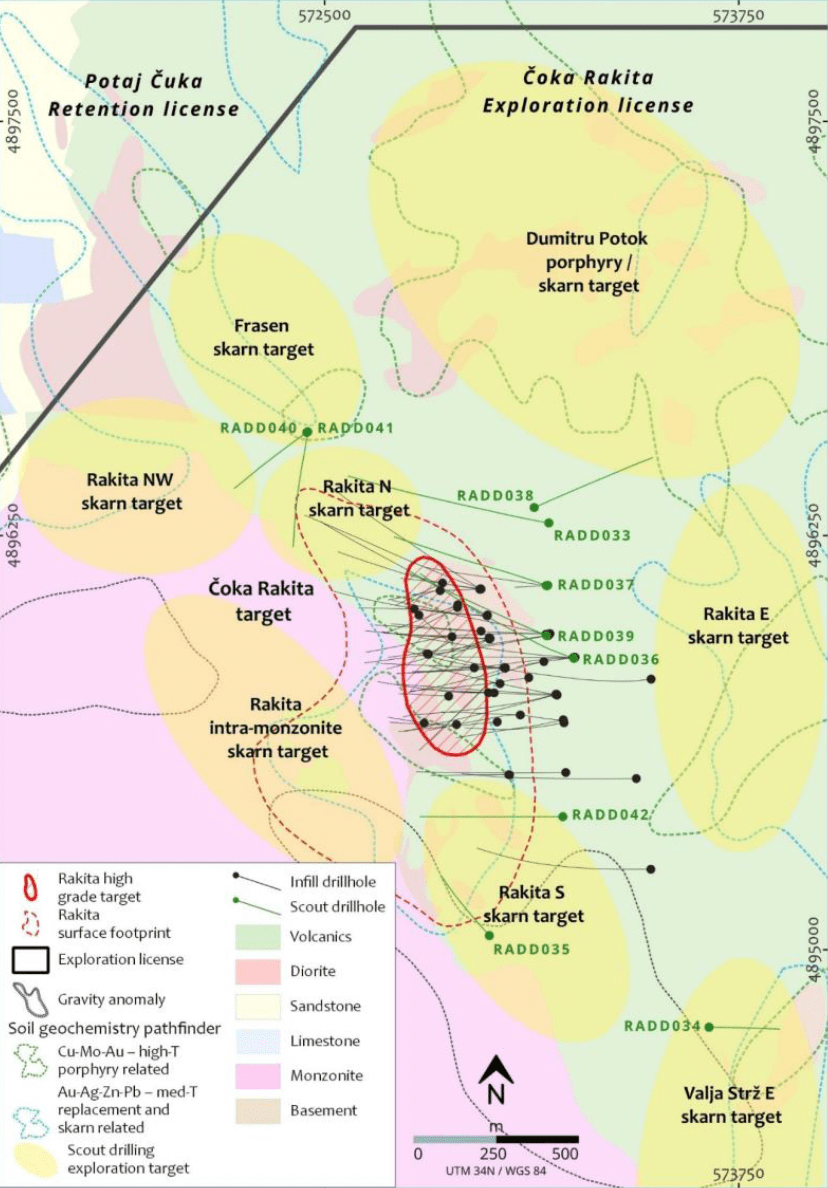

Dundee boasts an exciting pipeline of exploration prospects. Recent exploration success at ?oka Rakita indicates that the project could be developed as a standalone asset with robust economics. In mid-July, the company released additional assay results confirming and extending the core high-grade zone to the south. The 40,000-meter infill program, involving drilling at a spacing of 60x60 meters, is mostly complete. A 30,000-meter infill drilling program with a tighter spacing of 30x30 meters has also begun. Dundee aims to complete a maiden mineral resource estimate by the end of the year. Geotechnical drilling and metallurgical test work are being conducted in parallel. Due to these positive outcomes and increased activity, the company has raised its exploration spending guidance for the year 2023.

{kind=link}

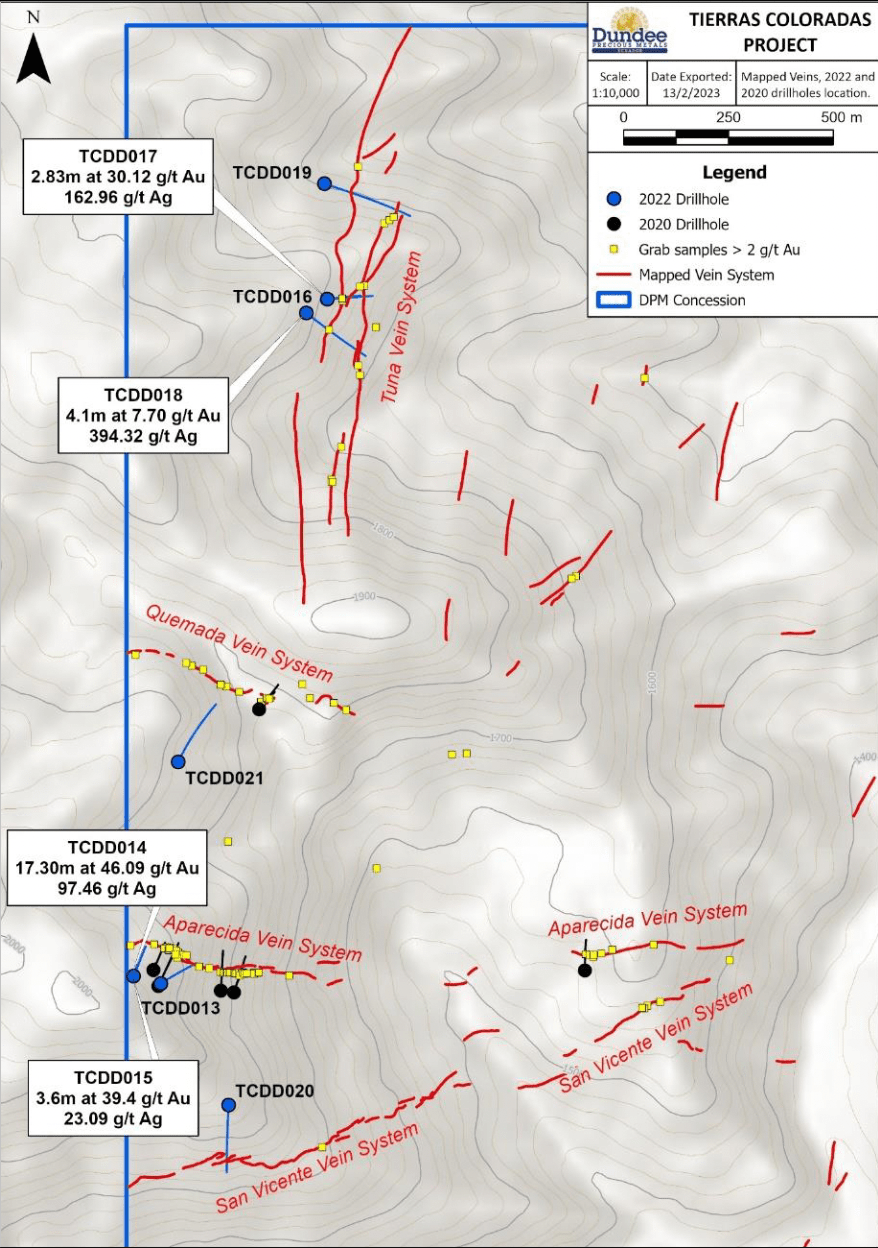

In addition to ?oka Rakita, ongoing exploration efforts are taking place at the Tierras Coloradas concession, located 200 kilometers south of Loma Larga in Ecuador. The company plans to initiate a 10,000-meter drilling program this month. This program aims to build upon the positive results reported at the end of February, which confirmed the presence of two high-grade vein systems that have potential for further expansion in multiple directions. The main objectives of this program are to further assess the extension and shape of these two vein systems and to investigate recently identified high-grade vein and soil anomalies.

Tierras Coloradas concession (Company's Q2 2023 Presentation)

{kind=link}

Finally, but of crucial importance, there is the Loma Larga project. It is more advanced than the other two mentioned earlier, but it is currently facing legal challenges that have been extensively discussed in previous articles. There is no significant update in this regard, except that Dundee is progressing with an updated feasibility study, incorporating optimization work based on the expertise gained from the Chelopech project in Bulgaria. The study is expected to be completed in the second half of 2023, while drilling activities at Loma Larga remain paused.

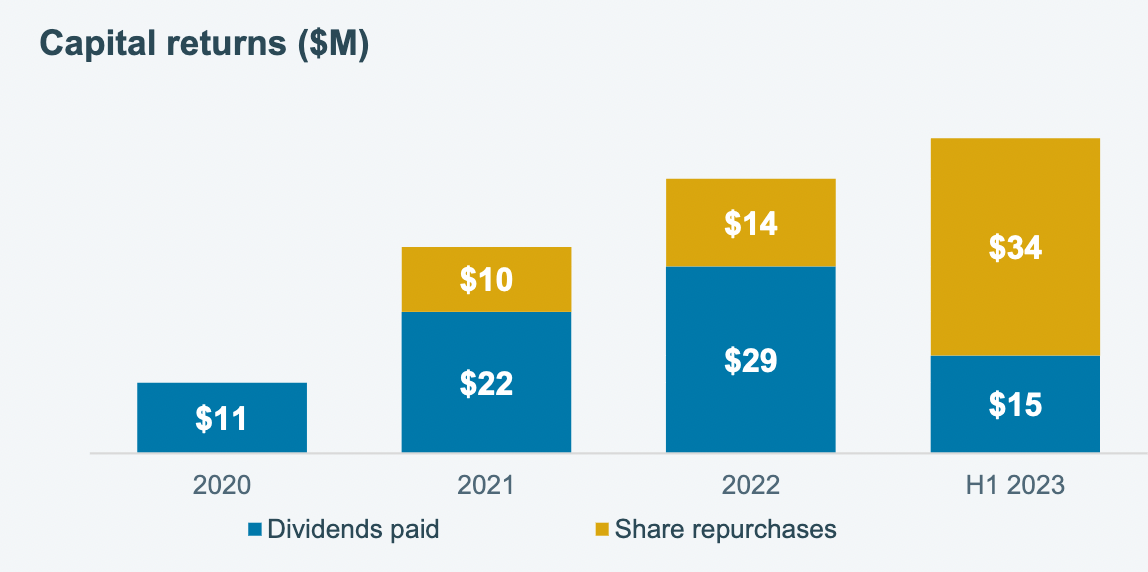

Apart from investing in growth initiatives, Dundee also has the potential to enhance shareholder returns in the near future. During the first half of 2023, the company returned 36% of free cash flow to shareholders through a combination of quarterly dividend payments and a share buyback program. The buyback program, initiated in March 2023, allows the company to repurchase up to $100 million of its shares over a 12-month period. Up to July, Dundee has already bought back approximately six million shares for around $42 million. This is a significant increase from the previous quarter when I was lamenting the fact that only 1.3 million shares were repurchased, indicating the company's commitment to taking advantage of recent price weaknesses.

The following visualization illustrates how capital returns have increased in parallel with the company's operational and financial success over the past four years. 2023 is expected to be a record year for capital returns, especially considering that there is still $58 million available for further buybacks. This is anticipated to provide support to the share price, even if the overall sector experiences some downward movement over the coming months.

{kind=link}

To conclude this article, while my outlook on Dundee remains optimistic, it is essential to consider potential sources of risk. Primarily, this means talking about Loma Larga. There is still uncertainty about the eventual development of Loma Larga. Ecuador is heading towards a new election in August, but it is likely that the final results will be available only in October. The outcome of these elections will clarify whether Dundee will be able to count on the necessary political support to finally get the project fully permitted. The risk is that Loma Larga could remain in limbo for an extended period, consuming resources without clear progress. The company has just increased capital expenditures at Loma Larga for 2023 to between $18 million and $22 million (up from the previous guidance range of $10 million to $14 million). So, at least it seems that the management believes there is still a significant probability of getting the project permitted. Other sources of risk include a significant decline in gold prices (which, however, does not seem likely now close to the end of a tightening cycle), and a resurgence of inflation in Europe, especially through a renewed energy crisis.

Despite the complexities surrounding Loma Larga, I continue to see Dundee as a top pick among gold miners. I am taking advantage of the recent price correction over the past two weeks to rotate funds from other precious metal producers. Dundee is one of the lowest-cost producers in the sector, and yet it trades at a compelling valuation, thus offering a significant margin of safety. To top it off, it has a pristine balance sheet, is committed to increased capital returns, and offers leverage to future gold prices via its exciting growth pipeline.

For further details see:

Dundee Precious Metals: Another Record Quarter