PBR - Ecopetrol: Too Risky Don't Focus On The Dividend Yield

2023-06-21 00:25:27 ET

Summary

- Ecopetrol is a South American energy company with operations in oil and gas exploration, production, refining, and distribution, as well as electric power transmission services.

- EC's future strategy includes way more renewables, hydrogen, CO2 storage and so on.

- The dividend looks high on paper, but is likely to be significantly lower next year.

Investment Thesis

Ecopetrol ( EC ) is popular among high-dividend investors. But the dividend is based on last year's earnings and is paid out in three steps. Given the lower oil prices and, thus, falling EPS, the dividend should be significantly lower next year. Furthermore, the company seems to be taking a different course overall. The investor presentation is largely about CO2, hydrogen, and other woke issues. The company itself says that it plans to significantly reduce its revenue percentage from hydrocarbons by 2040. A significant portion of the company's capital expenditures is expected to be directed to these areas, increasing the risk of declining earnings and dividends.

Company Overview

I became aware of the company because I'm invested in Petrobras ( PBR ). In the comments, someone mentioned Ecopetrol. The two companies have several things in common: based in South America, cheap valuations and high dividend yields, politically rather left-wing country, high government shareholding , and uncertainty about the future course of the companies due to the political leadership. The big questions are if the companies will pull back more and more from their cash flow generating oil and gas investments and instead focus on renewables, hydrogen, and similar areas.

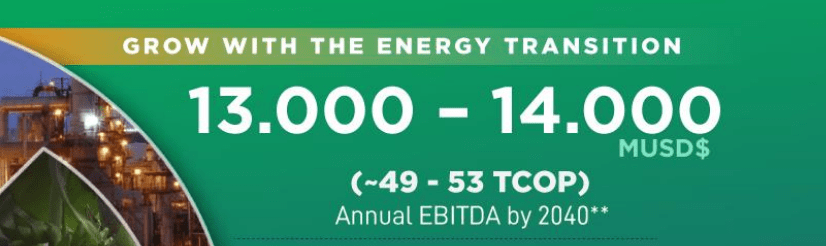

2040 corporate strategy

Some of the goals ( page 4 ) for this period include:

- 49 - 53 trillion COP annual EBITDA by 2040 (about $12B in the current exchange rate)

- 30% - 50% share of low-emission business in EBITDA

- 8% - 10% return on capital

- < 2.5x Debt/EBITDA

Unless I entirely misunderstand something, the annual EBITDA target 2040 would be lower than the current revenues because the first quarter results extrapolated would be about COP 72 trillion (about $17.2B).

During the first quarter, we recorded revenues totaling COP 38.9 trillion, net income of COP 5.7 trillion, EBITDA of COP 17.8 trillion, and an EBITDA margin of 46%.

This seems very strange. Who has ever heard that a company aims to make less revenue 17 years later? Please correct me if I am wrong here, but I can't see that I made a mistake. Above is an original quote from the Q1 report, and below is an excerpt from the investor presentation.

{kind=link}

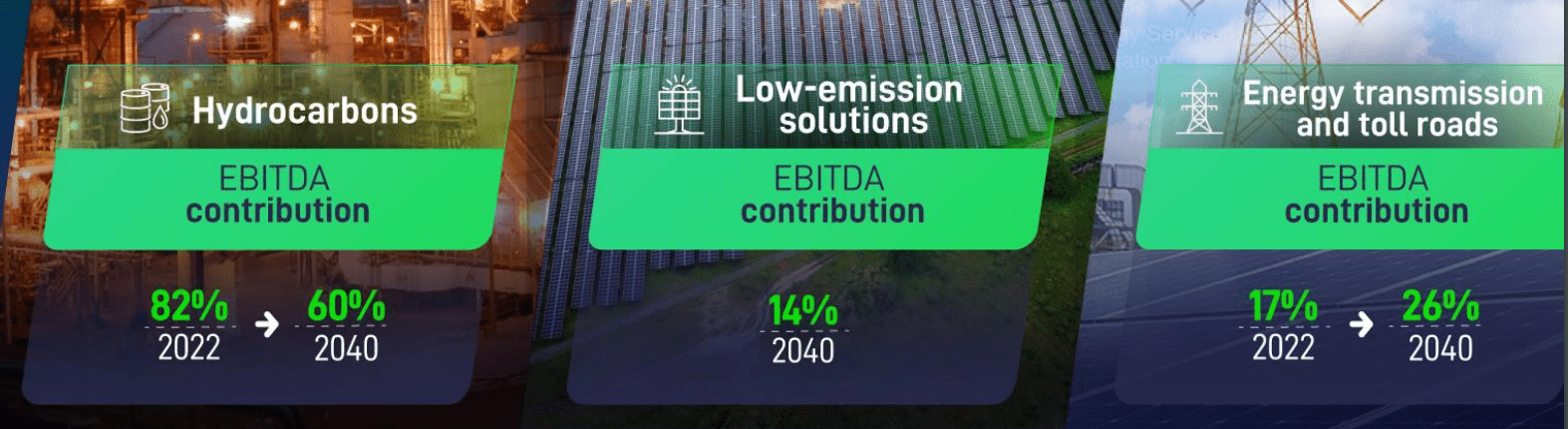

Overall, the company seems to be very serious about shifting the share of its EBITDA away from hydrocarbons and towards renewables. For investors, it is essential to know that operating wind and solar farms can generate significant cash; I am also invested in Brookfield Renewable Partners ( BEP ), but only after years of investment.

{kind=link}

Financial Progress & Trends

First, a short overview over a longer period for revenues, expenses, and net income. Like all companies in the sector, Ecopetrol has experienced a boom year in 2022.

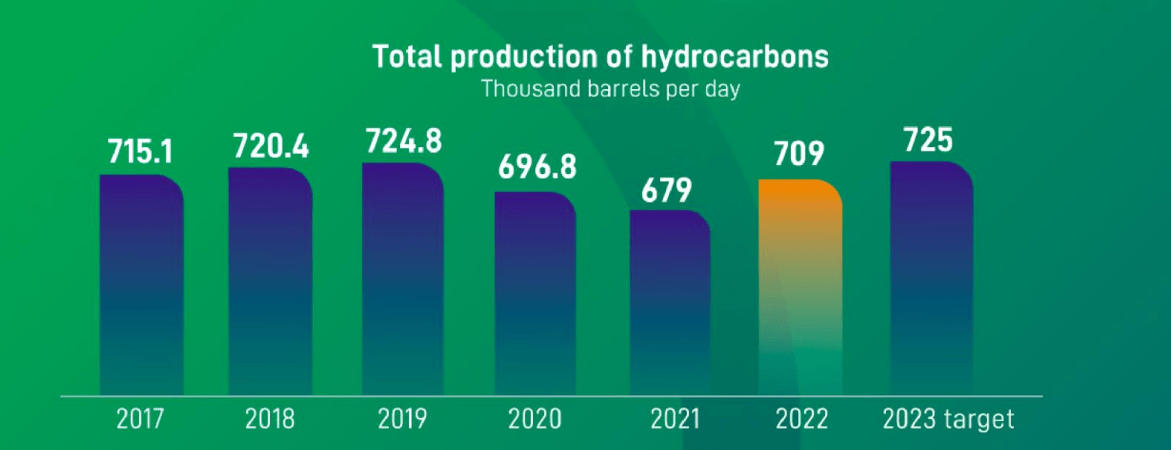

Also, the company has managed to significantly ramp up production in 2022, and this is expected to be even higher in 2023.

{kind=link}

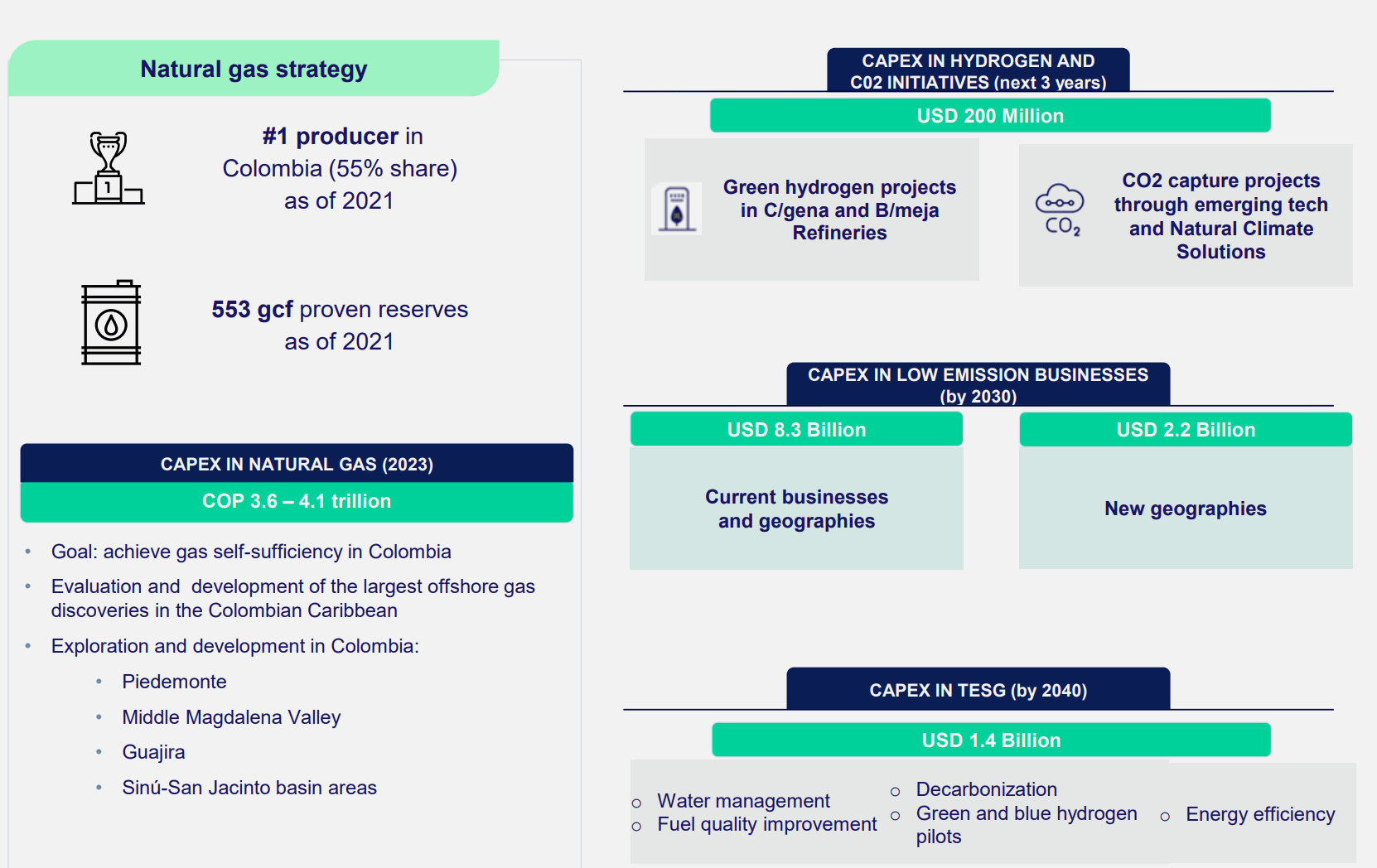

In the distribution of CAPEX, however, we see in which direction the company is heading. It is bizarre that in the investor presentation, CAPEX has a page dedicated to it, but oil is not even mentioned.

{kind=link}

Valuation & Outlook

The company is currently valued at an enterprise value of $52B. The market cap is $21.68B, and the total debt is about $25B.

Compared with Petrobras, both are currently valued almost equally.

Regarding the dividend, the plan is to pay out 60% of net income as a dividend. This year's dividend is based on 2022 earnings and will be distributed in three equal payments, so we can already see the future distribution on Seeking Alpha. Probably these figures are not quite correct as the dividend was originally declared in Colombian pesos, and the 11,860 COP would currently correspond to even $2.84, more than stated here.

{kind=link}

On the current share price, this corresponds to a yield of about 28%, and those who buy the shares now could still receive two dividends this year. Next year's dividend will be based on 2023 results and is likely to be significantly lower, if only due to the much lower oil prices this year.

Risks

One current development in several South American countries is the left political orientation and the higher state influence that goes along with it. An excellent article on Seeking Alpha describes this company's political situation and dangers well.

I’m not arguing that this is a bad investment, I am arguing that this is one that you should skip over if you are not looking to play roulette with your money. Ecopetrol is a company that is now in the hands of allies of a former communist rebel and at the mercy of his political whims. While it’s certainly possible that Petro could wake up tomorrow and decide that he wants to do a complete 180 on his energy policies, I think that this is highly unlikely. For those looking to invest in oil, I would suggest you forget the dividend here and look for a company with actual growth potential as there are many out there.

Ecopetrol Now At The Mercy Of New Left-Wing Government, And Exploration Restrictions

More info is also available in this article.

How radical is Petro’s plan on oil exploration? For critics, Petro’s oil policy amounts to “economic suicide.” Many warn his plan to boost agriculture and tourism won’t be enough to make up for lost oil export earnings, potentially leaving a big hole in public finances. Analysts have predicted a significant devaluation of the peso against the dollar as a result of falling investor confidence in Colombia.

No Oil Producer Wants to Be the First to Give Up the Fuel. Except Gustavo Petro’s Colombia

The President does not want to issue new licenses to explore new oil wells, but the processing of already issued licenses remains allowed. However, Ecopetrol needs new wells and further exploration because the existing oil reserves only have a lifetime of 8 more years. There may be some additional future production from licenses that have already been issued. But the thing about oil is that the production rate decreases towards the end of the well's life. For Ecopetrol, this would mean that less and less oil is produced each year. However, this development could still be a few years away. At least in 2023, the production rate should be slightly higher than in 2022, as shown above.

The market had similar concerns in the case of Petrobras, but nothing concrete has materialized (at least so far). With every day that passes, the chances are higher that, in the end, it was all political talk, but the Brazilian government of President Lula will change much less than one might have feared. The Brazilian government has a significant share in the company and earns tens of billions annually in dividends and taxes (the same is true for Ecopetrol and Colombia). I am still invested in Petrobras and do not intend to change anything here. See here my latest article on the company. By the way, Lula even commented on his Colombian counterparty and his plans.

As part of his campaign, Petro vowed to immediately stop issuing new permits for oil exploration—a big deal in a country where oil makes up 40% of exports and 12% of government income . Petro also called on Lula, who could become his most important regional ally, to join him . So, would he?“Look, Petro has the right to propose whatever he wants,” Lula said, smiling and shaking his head as if we were discussing an eccentric old friend. “But, in the case of Brazil, this is not for real. In the case of the world, it’s not for real.

No Oil Producer Wants to Be the First to Give Up the Fuel. Except Gustavo Petro’s Colombia

There is also currency risk, as the company declares its income and dividends in Colombian Pesos, which are later converted into Dollars. Currency fluctuations are always a risk and also an opportunity at the same time.

Another risk for shareholders looking for high dividends is that the company reduces distributable income by investing in renewable energies. I have nothing against renewable energies, but they need years to return the invested money. The same applies to hydrogen, or it is even worse: hydrogen has not even proven itself on a large scale, unlike solar.

Investor presentation

Conclusion: So many risks

Some things about this company seem inconsistent. For example, the production volumes in 2023 are expected to be even higher than in 2022. As is often the case with politicians, we don't know exactly what of the original election promises will be kept or what will remain just rhetoric. From everything I have read, however, the Colombian president seems more extreme in his views than most others.

But even if not, the dividend next year should be significantly lower, and the forward P/E ratio of 4.5 is low, but there are still better candidates to invest in. At the peak of its political risk, Petrobras was priced even lower than that. In the Investor's presentation, much more is written about CO2 and net-zero than oil. For a company that earns its money with oil, I don't like to see that.

Overall, it is not a good sign that my risk section is so lengthy. Towards the beginning of the article, I also wrote about how strange it seems that the company wants to generate less EBITDA in 2040 than today. Furthermore, there is a risk that the hydrogen plan might be just money-burning. I am not yet convinced of hydrogen's benefits and economic feasibility.

Therefore, I think there are too many risks, and investment doesn't seem attractive to me at this point. I think Petrobras operates in a similar sector but is a much better investment.

For further details see:

Ecopetrol: Too Risky, Don't Focus On The Dividend Yield