MSFT - Electronic Arts: Holding Out Strong With A Solid Quarter

Summary

- As the cards remain largely stacked against it, Electronic Arts came out swinging for its Q2 '23 earnings, once more, beating both top and bottom line analysts' expectations for the quarter.

- With companies downgrading guidance and missing earnings across the board, the industry veteran is still beating the market and performing better than some defensive stocks.

- EA stock is currently being traded at a relatively attractive 10.77x NTM EV/EBITDA, 16.30x NTM P/E, and at NTM 15.33x P/FCF.

- The company struck a lucrative deal with Disney in order to develop a trio of games based on beloved Marvel superhero characters such as Iron Man.

- Still, the best path toward value creation for EA's shareholders in our view remains an acquisition, similar to the Activision Blizzard deal that was announced back in January.

Electronic Arts ( EA ) was not the sort of company we initially expected is going to outperform during this challenging environment, let alone prove itself as a great defensive-oriented stock during the time. However, circumstances as of late have changed our mind in that regard. First, there's a high level of confidence among investors that the company is able to weather the ongoing difficulties and come out on the other end as an all-around more attractive value proposition. And the second interesting thing is that there seems to be more than one investor largely uninterested in the ongoing day-to-day results of Electronic Arts, most likely looking forward to a potential buyout by one of the major players in the space similar to the one involving Microsoft ( MSFT ) and Activision Blizzard ( ATVI ) earlier in the year.

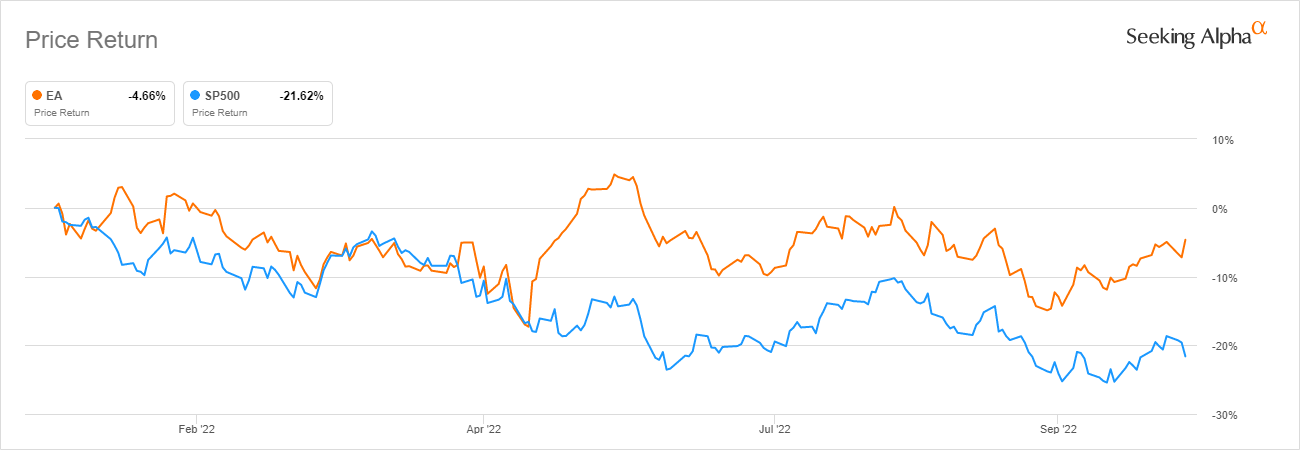

We initially outlined our position on the Redwood City-based entertainment giant earlier in January, but as we have stated in our latest coverage , the industry pioneer managed to carry itself extraordinarily well against the ongoing bear market sentiment and the recession-headed economy, much to our amazement. This trend has ensued well into the third quarter of the year, given that the company just reported its latest earnings that were well received by investors and analysts alike. As a result, even if facing a single-digit negative return for the period, the industry pioneer managed to generate extraordinary year-to-date and year-over-year results outperforming the S&P 500 ( SPY ).

EA and S&P500 YTD Results (Seeking Alpha)

{kind=link}

Electronic Arts Q2 FY23 earnings report

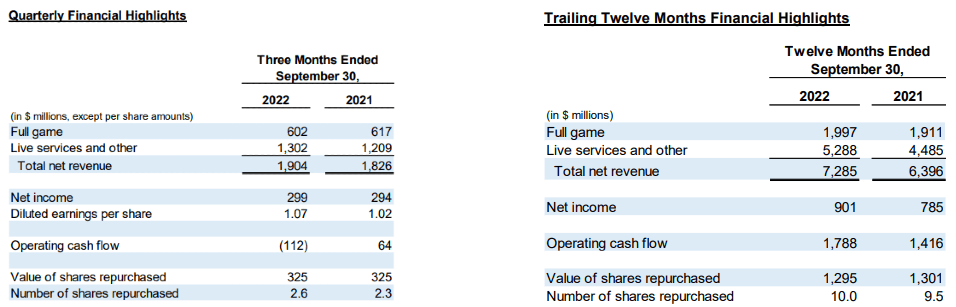

The video game giant posted what might be considered an unexpectedly good earnings release on Tuesday. In a challenging time when major players across the board are missing expectations and downgrading guidance, Electronic Arts managed to beat both top and bottom-line analyst expectations in its Q2 2023 earnings results published on the 1st of November, further solidifying its position.

In the said quarter, Electronic Arts posted revenues of around $1.9 billion, slightly higher than what analysts anticipated at $1.8 billion. Meanwhile, EPS ended up at $1.07 per share, which also is higher than what Analysts expected at $0.92 per share. The company reported net income of $299 million for the three months that ended Sept. 30, compared to net income of $294 million for the same period last year. It also has posted earnings of $1.07 per share, compared to the $1.02 per share it earned in the same period last year.

In terms of the trailing twelve-month figures, EA generated revenues of $7.28 billion for the 12 months that ended Sept. 30, a 13.92% increase when compared to revenues of $6.39 billion for the same period last year. The company reported a net income of $901 million for the same period, which is a 14.77% increase compared to the net income of $785 million for the same period last year. This strong performance is mainly led by a sharp increase in live service segment revenues.

{kind=link}

Another interesting highlight from the earnings release is the newly announced collaboration between Electronic Arts and Disney ( DIS ). The two companies will work together to bring three games in total to the market in the upcoming years based on the Marvel IP, beginning with creating an Iron Man game. They already have worked together previously on a similar system where they jointly tackled bringing Star Wars-based games like the "Star Wars Battlefront" series in the previous years.

In Q2, we also announced an exciting long-term, multi-game collaboration with Marvel, joining forces with a culture-defining powerhouse to expand our entertainment offerings. From our EA SPORTS league partners to Disney's Star Wars and Marvel universes and more, we're partnering to grow our global communities, build value together, and co-create the future of entertainment.

Andrew Wilson, CEO - Q2 2023 Earnings Call

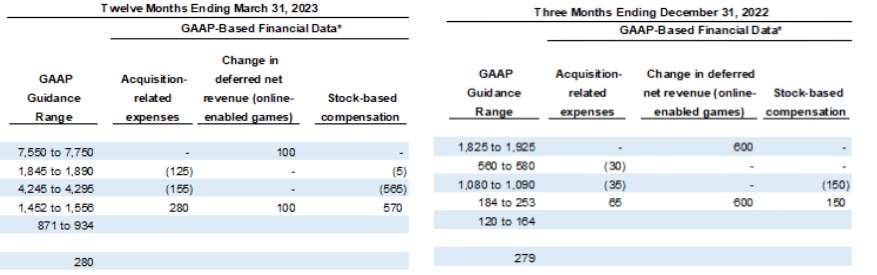

With most other companies both in the same space and overall in the market downgrading guidance and missing earnings across the board, Electronic Arts came out solid and held its quarterly and fiscal-year guidance, only slightly revising adjustments mostly related to FX impact.

{kind=link}

For full-year 2023, the company provided revenue guidance in the range between $7.55 billion and $7.75 billion, with net income expectations of $871 million to $934 million. That leaves earnings per share in the expected range of $3.11 to $3.34 a share. As for the quarter ending in December, the company provided revenue guidance in the range between $1.82 billion and $1.92 billion, with net income expectations of $120 million to $164 million. That leaves earnings per share in the expected range of $0.43 to $0.59 a share.

Just over half of our sales are generated outside of the US, and the US dollar has strengthened between 7% and 15% vs. our largest foreign currencies when compared to rates at the time of our initial FY23 guidance. As a result, we now expect an FX impact of approximately $200 million vs. our initial full-year net bookings guide, as the impact will grow in our second half, and into FY24, at current exchange rates. Beyond FX, our business fundamentals remain healthy, with strong player engagement trends across our platforms and franchises. We expect strength from our console and PC game franchises to offset most of the impact of the current mobile market softness. In particular, we expect to see the momentum of the FIFA 23 launch carry into the second half, aided by the excitement surrounding the World Cup.

Chris Suh, CFO - Q2 2023 Earnings Call

Rise of the live-service model

The industry veteran has been almost always at the forefront of pursuing new, innovative, and often controversial revenue streams. The industry itself has been evolving throughout the last decade and the pace over the past couple of years has been slowly accelerating. There's a significant pivot from the old business model when companies almost solely relied on brick-and-mortar game sales in order to keep the business afloat.

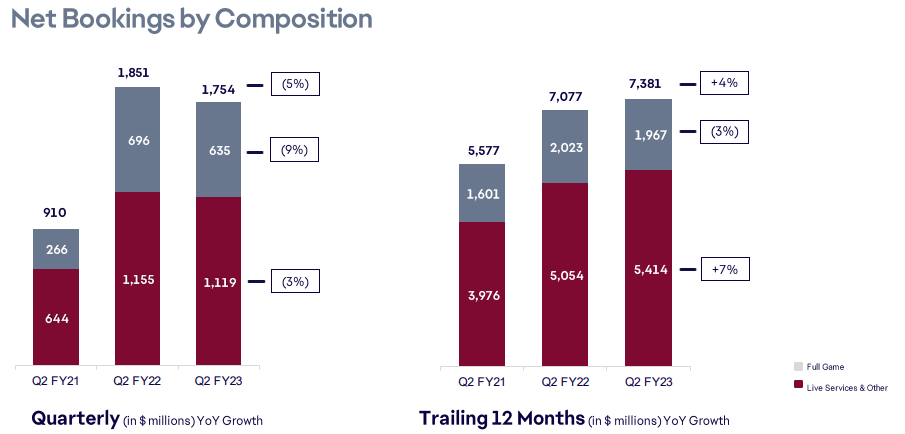

A major component of the company's current success trajectory is the strong performance of its live-service games. As best examples of such successfully implemented models, we could consider triple-A titles such as FIFA Ultimate Team, Apex Legends, or Battlefield 2042. On the other end, the company also is making a sensible pivot to mobile, which is naturally closer to this approach and has been one of the major growth potentials for EA.

We delivered solid performance across our business in Q2, driven by our EA SPORTS portfolio and our multi-platform live services business. Our broad IP, exceptional talent, and growing player network of more than 600 million are the foundation of strength and stability in an uneven macro environment. During Q2, we launched premier sports games and provided over 120 content updates on 35 titles across our global catalog. Our teams are deeply committed to delivering amazing games and entertainment that inspire fans to play, create, watch and forge enduring social connections. Our broad IP portfolio is unrivaled in the gaming industry. Foundational to our leadership is EA SPORTS, with breadth and depth of partnerships that allow us to continue delivering deeply immersive experiences to fuel long-term growth.

Andrew Wilson, CEO - Q2 2023 Earnings Call

{kind=link}

To explain things in layman's terms, game developers and publishers across the globe suffered for decades from the same sort of issues movie studios still have to endure even today. They would engage in expensive and risky projects with no guarantee of success or knowledge of pay off until the final product would hit the theatres in the opening week.

This business approach turns the tables around, as it significantly lowers the risk the company is facing but also increases the longevity and durability of the product itself. It would be similar if a three-act blockbuster movie would hit theatres with only the first act ready to go, for half the cost. EA in this situation simply has to throw things at the wall and see what sticks. Keep the winners and throw away the losers.

Live services, as the next evolutionary step in EA's business, currently take up the majority of total net bookings for Electronic Arts. The impact of the model on financials has been steadily on the rise for years. When taking the quarter into consideration, live services made up 63.79% of total bookings, while the number increases to almost 73.35% on a trailing twelve-month basis. This is a huge step in the direction of creating shareholder value.

{kind=link}

EA stock's price tag

At face value, some might deduce that the developer and publisher is trading at a relatively steep valuation when compared to some other perhaps more enticing opportunities in the market. In other words, the company does not seem to have a "bear market" discount applied, unlike some of the other competitors operating in the same space. While the S&P 500 endured a loss of almost a quarter of its market value as it was erased from existence since the beginning of the year, EA's rivals had to endure being discounted by as much as 50% in the same time period.

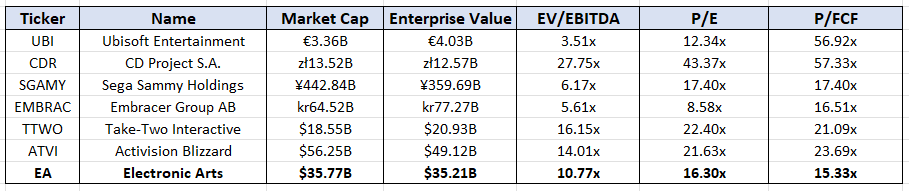

On the other end, EA is holding out strong and is currently traded on the open market at $127.64 per share. The market is valuing Electronic Arts at 10.77x NTM EV/EBITDA, 16.30x NTM P/E, and at NTM 15.33x P/FCF. With improved operational results and a slight one-digit pullback the company faced since the onset of the year, Electronic Arts is now an even more attractive value proposition in our view. However, we can see the rest of the industry peers are slowly catching up, mostly due to the fact that their market capitalization was cut almost in half during the same time frame.

Industry Peers (Author Spreadsheet IQ Capital Data)

{kind=link}

Closing thoughts

Earlier in August, there had been a rumor that Electronic Arts was being sold off to Amazon ( AMZN ) which was reportedly looking to expand its reach within the entertainment industry. GLHF, a Swedish media group, published an article on USA Today saying that Amazon was about to buy EA, quite literally by the end of that day. That report was obviously proven false, but the important takeaway from the situation is that everyone suspects that EA would be open to a deal at the right price, and there are many predators in the space akin to Microsoft, Disney, or Sony ( SONY ) who have been actively expanding their entertainment empires throughout the years.

As you already know we have already written on a couple of occasions that we believe the best path toward value creation for EA's shareholders would be an acquisition similar to the Activision Blizzard that was discussed earlier in the article. EA has obviously been at the center point of such discussions given both the depth and the quality of the IP the company commands. With virtually no debt, good operating results, and a resistant business model, we do not see a 30%-50% premium out of the range of possibilities, which would land the price at $163.8 to $189.93 per share. We still stand behind our belief that it is highly unlikely that the game industry veteran will enter the next decade as an independent company. Given the summary of our thoughts explained within the article, we maintain a bullish outlook on EA.

For further details see:

Electronic Arts: Holding Out Strong With A Solid Quarter