AAIC - Ellington Financial: Lack Of Dividend Coverage Makes Me Hesitant

2023-09-25 13:27:00 ET

Summary

- Ellington Financial Inc. offers an attractive dividend yield of around 13.96%.

- The mREIT's share price has been affected by mark-to-market losses in certain segments of its portfolio, such as agency-backed MBS.

- The acquisition of a large portfolio of mortgage servicing rights (MSRs) could provide a more stable source of revenue for the mREIT in the future.

- Several quarters of a non-covered dividend leads to some concern over the sustainability of the dividend.

Ellington Financial Inc ( EFC ) is a mortgage real estate investment trust (mREIT) offering a dividend yield of around 13.96%. Like most mREITs its share price has not performed particularly well in a rising rate environment given the increase in mark-to-market losses in certain segments of its portfolio such as agency-backed mortgage-backed securities (MBS). Uncertainty over the direction of the rate environment could continue to weigh on the mREIT’s share price in months ahead. However, the acquisition of a large portfolio of mortgage servicing rights (MSRs) could add a more stable source of revenue for the mREIT going forward.

The portfolio

The bulk of Ellington Financial’s portfolio is invested in residential mortgages, with around 72% of its portfolio being invested in residential mortgages. Around 22% of its portfolio is then made up of commercial mortgages, of which 11% is made up of mortgages in the office sector. The effect thereof is that the mREIT has quite limited exposure to the office market, which has been an underperforming market amidst rising office vacancies.

Investments in agency-backed MBS amounts to just under $1 billion, or around 24% of the overall portfolio. This part of the portfolio saw realized losses of just under $15 million in the second quarter of 2023. Management noted that this part of the portfolio experienced substantial losses in the first part of the quarter as volatility arose amidst the rise of MBS on the market as the FDIC sought to offload MBS from failed regional banks. These losses were largely erased as the market stabilized later in the second quarter. Management also used the time period during which the price of agency MBS was depressed to add to its agency MBS portfolio, leading to the total value of its agency MBS portfolio increasing by around 7.7% quarter-over-quarter in the second quarter of 2023.

The future earnings of the agency-backed MBS portfolio seem largely dependent on the future direction of interest rates. To be clear, income from agency MBS has largely been stable, but a rise in interest rates would result in further mark-to-market losses. Futures are pricing in a roughly 50% chance of another 25-basis point rate hike by year-end, while economists widely expect that the Fed has reached the end of the rate hike cycle for now. The Fed itself has indicated the possibility of another rate hike this year should inflation remain elevated.

Nevertheless, inflation in several core areas has slowed down substantially in recent months. However, inflation in core consumer goods such as food has remained stubbornly elevated and has not slowed down meaningfully as of yet. Food inflation for foods consumed at home has remained at around 3.6% while inflation on food consumed away from home has reached 7.1%. These specific areas of stubbornly high inflation make it harder to foresee what the Fed will do in terms of rates. Investors interested in investing in mREITs would accordingly need to monitor inflation and indications from the Fed closely, as the risk of further mark-to-market losses will make mREITs a less attractive investment in the short term.

The proposed acquisition of Arlington Asset Investment Corp ( AAIC ) could substantially diversify EFC’s investment portfolio. This would be EFC’s first significant foray into the area of mortgage servicing rights ((MSR)). These MSRs over a more stable source of income in a rising rate environment, as they are not affected by the negative mark-to-market write-downs faced by most MBS securities in a rising rate environment. Rising interest rates also reduces the risk of early repayment on mortgages, which is accretive to MSR investments. While the current rate hike cycle might well be nearing its end, the addition of a relatively stable source of revenue would, in my view, be highly beneficial for EFC in the long term.

The majority of AAIC’s portfolio consists of MSRs. Its portfolio is made up of around $300 million worth of investable capital, of which around 62% has been deployed in MSRs. A further 26% of its portfolio consists of agency MBS, which would mean that the acquisition is also likely to increase the percentage of EFC’s portfolio made up of MBS. Should there be further interest rate hikes, this aspect of the portfolio might well be negatively impacted again. Nevertheless, on the whole, I believe the acquisition of AAIC is a positive long term addition to EFC in light of the MSR exposure.

Management also expects to generate attractive returns on MSRs, even though it is unlikely to constitute a substantial portion of the portfolio in the near term. Management observed that –

As long as, frankly, financing is there, continues to be there at attractive levels to be able to finance the MSRs, that's going to be key. But the yields that they're trading at given the risk profile and given the financing costs that are available currently, make it an attractive strategy. It's not a trading strategy, right? So I think, just consistent with what I was saying before, it's not going to be, I don't think a huge part of our portfolio anytime soon. But it's something that I think continues to – that we'll continue to add to and diversify returns and can achieve well into mid-teens returns, or not higher on a leverage basis.”

Returns in the mid-teens would certainly be attractive and, while MSRs percentage of the overall portfolio would be limited, would nevertheless be positive to earnings overall.

The dividend and its safety

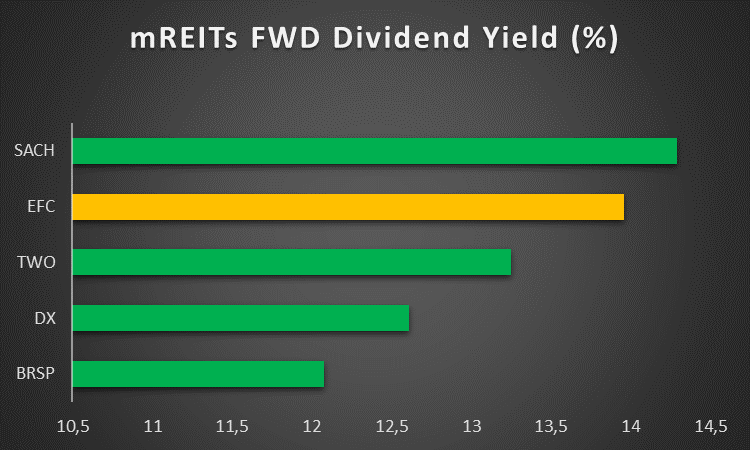

Ellington Financial currently offers a forward dividend yield of around 13.96% which is the second highest of the mREITs considered in the peer comp chart below. This dividend is made up of a $0.15 dividend per share paid monthly. In its most recent quarter this dividend was not fully covered by adjusted distributable earnings, which was $0.38 for the second quarter of 2023 giving a dividend coverage ratio of just under 85%.

{kind=link}

mREITs FWD Dividend Yield (%) (Author created based on data from SA)

Importantly, a single quarter of the dividend coverage ratio being below 100% does not necessarily signal a dividend cut. However, EFC has reported several recent quarters in which the dividend was not fully covered by adjusted distributable earnings. While the dividend was fully covered in the first quarter of 2023, it was also not fully covered in the third or fourth quarters of 2022. EFC’s one-year average dividend coverage ratio amounts to around 94%.

The dividend not being fully covered by adjusted distributable earnings again does not necessarily mean that the dividend will be reduced. However, it does in my opinion substantially increase the likelihood of a dividend cut and makes me more hesitant to conclude that the dividend is safe. Investors in EFC would need to monitor the dividend coverage ratio and signals from management on the future direction of the dividend closely in the quarters ahead.

Valuation

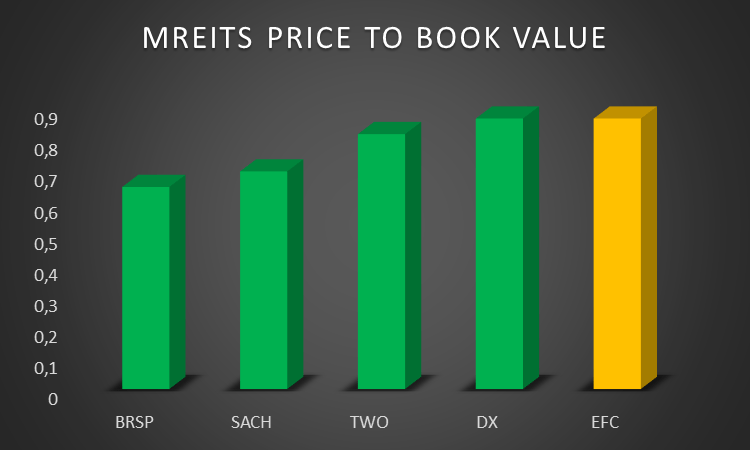

EFC is currently trading at around 0.89 times book value, which is the highest of the mREITs considered in the peer comp charts below. Importantly, the figure on most quote pages would be 0.87, but the 0.89 was calculated based on the update provided by the company after the payment of the dividend. Excluding the impact of the dividend and the update, the price to book value would still be the highest of the mREITs considered in the peer comp charts below.

{kind=link}

mREITs Price to Book Value (Author created based on data from SA)

The discount to book value does not seem inappropriate given the uncertainty in the interest rate environment at the moment. Uncertainty over the sustainability of the dividend also justifies a certain discount to book value at the moment. Therefore, I am of the view that EFC stock is trading near fair value at the moment.

Conclusion

Like many mREITs, Ellington Financial faces challenges in a rising rate environment, particularly in segments of its portfolio, such as agency-backed MBS. This uncertainty may continue to negatively impact on its share price in the coming months. Nonetheless, the acquisition of a substantial portfolio of MSRs represents a positive development, offering a more stable source of revenue. This move could potentially bolster EFC's long-term financial outlook.

Despite these positive developments, I do not consider the stock a buy at the moment. While the dividend yield is attractive, the dividend coverage ratio has frequently been below 100% in recent quarters, indicating some level of caution. This situation doesn't necessarily signal an impending dividend cut, but it does warrant close monitoring and makes me more hesitant to rate the stock a buy. I also believe that the stock is trading around fair value for current market conditions, despite the discount to book value.

For further details see:

Ellington Financial: Lack Of Dividend Coverage Makes Me Hesitant