TLT - Emerging Market Risks And U.S. Economic Landings

Summary

- Are markets re-rating EM here? Has the "sudden stop" of capital flowing into emerging markets started?

- A steadfast tightening Federal Reserve will play into and heighten these EM risks through various channels.

- The outlook for the US economy remains generally-positive as shown by recent jobs and retail-sales-data. The article will also explain three potential scenarios for the US and the effects on risk-assets.

- The ECB is not only lagging the Fed on tightening - the ECB is also more prone to reverse course than the Federal Reserve amongst more bearish global conditions, lower inflation and a likely recessionary environment in Europe. I would expect downward pressure on EUR/USD.

- Risk-assets generally stand to see declines in my view as the Fed reverses the "wealth-effect" on US spending and aggregate demand as asset price inflation has now shown to translate into consumer-price-inflation. Emerging markets, metals, energy, and the commodity sector stand out as vulnerable in a continued strong USD environment.

IMF

The above chart is the "holy grail" of the problems facing Emerging Market economies. To briefly explain - the feedback loop is catalyzed by a tightening in US financial conditions such as a strong USD and higher US real Treasury yields thereby enticing global capital movement out of emerging market economies and currencies and into the USD in search of currency appreciation, higher relative yields and less political risk.

Emerging market central banks are then forced to raise rates to fend off capital flight and inversion of yield differentials which weaken carry trades into EM currencies. As yields rise in EM economies, not only do their economies slow, also, their banks experience mark to market losses on sovereign or government bonds held by emerging market private sector banks, which is a higher percentage than government bonds held by domestic banks in developed market economies (shown below, IMF). This means greater mark to market losses on their bond portfolio for EM banks due to higher yields than banks in advanced economies facing higher yields. This also tightens lending into a given EM economy - weakening the corporate sector and overall economic strength of a country resulting in lower tax revenues for the government, forcing a greater supply of EM sovereign bond issuance and again even further higher yields in the loop shown above.

IMF

Natalia Gurushina

As shown above 5Y yield premium of emerging market sovereign bonds are narrowing with EM Asia leading the breakaway move lower. This means US Treasury yields are closing in on the higher yields generally offered in emerging market economies. This is one catalyst for the mechanism described in the paragraphs above. Another issue of EM is the large amount of USD denominated debt where an appreciating USD or acute dollar shortage results in higher debt burdens, forced selling of UST Treasuries to acquire US dollars, higher relative US yields as a result of the en-masse selling of US Treasury bonds held internationally (sold for much needed USDs), and a worsening of the starting USD shortage in a cycle.

According to the Bank of International Settlements , foreign credit in US dollars stood at $13.1T while foreign euro and yen credit are at $4T and $0.3T respectively.

Next, I will cover three potential economic outcomes for the domestic US economy. First, I will mention the weak H1 2022 real-GDP growth.

The US experienced negative H1 2022 real GDP growth during an expansion which is quite rare . The NBER did not announce an official recession and most forecasters at the time were not expecting a continuance of negative real GDP growth. This has proved correct.

Inflation has come down with nominal growth and aggregate demand remaining strong. I said previously the negative real GDP in the US was temporary and shouldn’t be construed as a nominal growth recession reflective of a weak economy and high unemployment. The negative real growth was due to prices rising vastly above trend and factors outside of the health of us economy’s aggregate demand and underlying nominal growth trend, including a strong dollar weighing on exports which boosts the trade deficit and subtracts from NX (net exports) contribution to growth and also inventory adjustments weighed on nominal growth early in 2022.

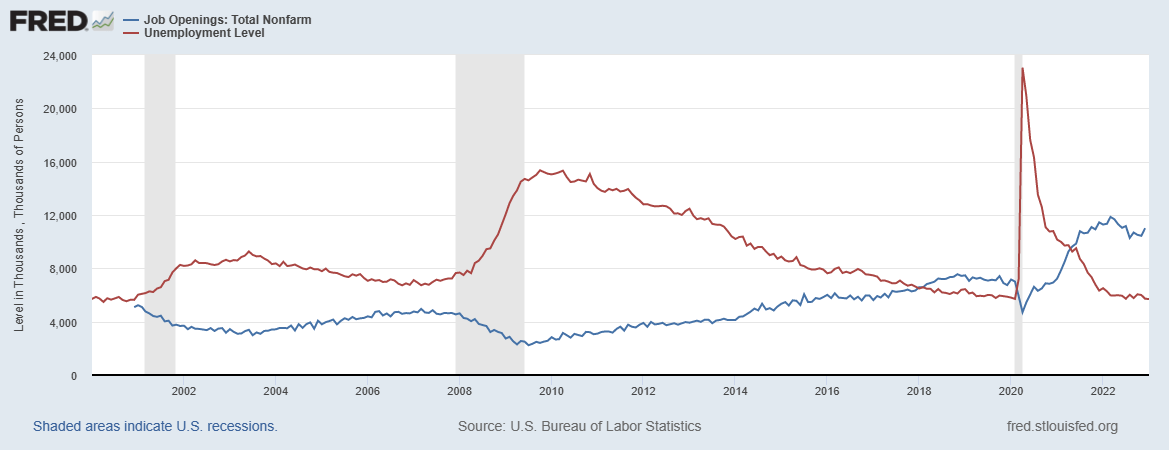

The US labor market remains very tight as shown by job openings exceeding unemployed people shown below.

Job openings versus Unemployed persons (St. Louis Federal Reserve)

{kind=link}

The three scenarios I mentioned above are a soft-landing, a nominal growth recession and lastly stagflation or a negative-real growth environment due to persistently high inflation.

I am in the camp of a soft-landing for the United States and interestingly this is not the bullish scenario for equity longs, as it allows the Fed to tighten continuously and hold at a restrictive Fed Funds Rate level with the CPI coming down and creates an environment very detrimental to emerging markets economies and currencies, which the market has shown sensitivity to in the past.

The ideal scenario for risk-on equity longs is actually stagflation. This would be characterized by a weak USD, continued high inflation rates, a Fed deemed somewhat irrelevant or too passive in their tightening cycle, and strong aggregate demand domestically and globally particularly in emerging market economies.

The other outcome would be a nominal growth recession in the US where unemployment vastly rises, and nominal growth craters.

The key to understanding these outcomes is knowing the difference between nominal GDP and real GDP. The latter is adjusted for inflation. If real GDP is negative due to an above trend CPI, it could be construed as bullish for risk and equity markets. If nominal growth is negative, it means the economy has fallen off a cliff and would be bearish. In the soft landing scenario nominal GDP remains resilient, while the CPI comes down allowing positive real growth, though the spillback effects of a tighter Fed policy onto emerging markets would likely bring down historically elevated risk-asset values (such as stocks) as well as commodity markets.

The soft-landing is gaining traction recently with the strong jobs report and good retail sales print. Various Fed officials have come out in favor of returning to a 50bp hike next meeting. The last CPI report which came in higher than expected also reinforces this.

A point I want to make and have made before on the size of the next rate hike: I've continuously been in the go big camp and exceed market expectations (which the Fed hasn't done although has still raised very aggressively) and I say go 50bp next meeting as the potential recessionary effects are greater by climbing slower to a higher terminal rate than faster to a lower terminal rate in my view.

This is because overshooting market-based expectations for the FFR causes an immediate market reaction and tightening of financial market conditions (such as higher yields real and nominal, wider credit spreads, lower equities, stronger USD) so the downward effect on inflation happens sooner and quicker.

This means the Fed could potentially stop at 5% FFR instead of having to go to 7% for example while also lowering inflation sooner and more effectively boosting real GDP growth. A higher terminal rate will eventually stymie business investment and the growth of the supply side of the economy, so I think getting to a lower terminal rate quicker is more optimal than the other strategy of climbing higher slowly.

Before the latest CPI data I pointed out - the nature of inflation data isn't typically perfectly linear. Even if the trend is lower, we could print high one month very easily especially given the loosening in financial market conditions recently and sure enough we did.

A quick point on FOMC and UST yields that I think is under looked is markets had, until recently, been pricing in cuts starting in September and there's still a camp that feels the Fed will be forced to cut.

Doesn’t the double downshift from 75 to 50 basis point hikes and then 50 to 25 basis point hikes serve to lower the chance of a US recession and the need for any cuts this year at all? Therefore, the slowing in Fed tightening may mean higher yields than if the FOMC did continue to go +75bp or +50bp as the result of the downshift is decreased risk of a nominal growth recession resulting in rate cuts. We've seen this a bit as the rate cuts this year have been being priced-out of Fed Fund Futures though not entirely.

Inflation is coming down and we don’t have a threat of a severe recession, and therefore the 'bear market is over' is a common argument from equity longs. This argument doesn’t hold weight in my opinion because stocks have yet to pass the test of higher UST yields.

I agree with the no recession call, especially looking at the last jobs report though again, stocks have to stand on their own and show resilience with a 10Y yield going above 4% in my view. The CPI is still above 6.00%. And the Fed isn’t done so yields are going to move higher either on the Fed pushing harder, and if the Fed is too passive then the CPI will remain elevated and higher inflation expectations (break evens) will push nominal yields up in that way. Expecting unrealistically low yields to subsidize equities is the old paradigm that many may not realize has changed.

If you take a look at this chart I made, it does look as if market downturns tend to occur when the Fed Funds Rate rises above nominal 10Y yields. I have no real statistics on it, though it does make sense given a FFR above a nominal 10 UST yield implies an inverted yield curve which is associated with falling inflation and recessions; which tend to occur with stock price declines intuitively on weak aggregate demand in the economy and low pricing power by corporates and weak profits, and less accommodative monetary policy.

St. Louis Federal Reserve

While I have covered the USD versus emerging market FX, the most weighted currency against the USD in most indexes is in fact the euro. I will now explain why the ECB is more dovish than the Fed and the outlook for EUR/USD is bearish.

First markets are pricing a lower terminal or ending central bank policy rate of 3.75% in Europe versus over 5% in the United States.

The ECB has recently announced a plan to roll-off the bonds on its balance sheet bought during some of its QE or quantitative easing programs. A fact often overlooked is the ECB has two QE programs - the Asset Purchase Program or APP and the Pandemic Emergency Purchase Program or PEPP.

The APP unwind will be significantly slower than the Fed's balance sheet drawdown as well as the PEPP remaining untouched. According to the ECB's latest monetary policy statement :

The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP until the end of February 2023. Subsequently, the APP portfolio will decline at a measured and predictable pace, as the Eurosystem will not reinvest all of the principal payments from maturing securities. The decline will amount to €15 billion per month on average until the end of June 2023 and its subsequent pace will be determined over time.

As concerns the PEPP, the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

For comparison the Fed is rolling bonds off its balance sheet at a pace of $95B per month versus 15 billion euros per month for the ECB respectively. Total assets held by the ECB relative of the size of the economy is also larger in Europe than assets held by the Fed as a percent of US GDP meaning not only is the ECB moving slower in reducing liquidity, the ECB also has more ground to cover.

I also feel Europe's economy is generally weaker than the United States and a return to lower rates is much more likely in Europe than in the US if there is a downturn in the global economy and a significant deceleration in global inflation rates. One reason is Europe and particularly Germany are very export-dependent economies with large reliance on demand for emerging markets, so Europe is more susceptible to a drop off in Chinese demand for imports for example than the US is.

Much of the inflation in Europe is cost-push driven by high natural gas prices due to the war in Ukraine, rather than domestic demand-pull driven inflation. This can be seen in a higher core CPI in the US with a higher headline CPI in Europe. This means aggregate demand or total spending in an economy overwhelming production capacity in Europe is much less of an issue than in the US and could allow the ECB to return to a more dovish monetary policy stance before the Fed especially if recessionary risks are more heightened in Europe.

Robin Brooks, IIF Robin Brooks, IIF

The euro currency being "weak" is a common misconception as shown below. The euro is only moderately weak against the USD (which is considerably strong above 100 on the DXY even with the recent downtrend which I think has bottomed). In a basket including other currencies, the EUR actually stands around 1.50 which is very strong. This means Euro area net exports versus Japan, and EM exporters are losing competitiveness (euro area is) as a strong currency makes exports more expensive for foreign purchasers. How can Europe close the new current account deficit (after long being a current account surplus region) with such a strong euro undermining exports?

Robin Brooks, IIF

Lastly, I will look to China where mega-bullish sentiment and optimism on the Covid-zero policy reopening led to a rise in commodity prices and Chinese share prices. I remain bearish on the world's second largest economy.

Robin Brooks, IIF

China has a much lower CPI than the United States, so in nominal terms the US is actually outgrowing the Chinese economy. GDP is often adjusted for inflation to discount the impact of higher prices as that is not reflective of new economic output though nominal growth can be used as a read on resilience and strength of aggregate demand in an economy as firms cannot raise prices in an economy that is experiencing weak aggregate demand. In essence, it is easier to achieve positive real growth when facing an inflation rate that is fairly/comparatively low assuming no steep drop-off in aggregate demand. See the divergence between the CPI and producer price index for more on pricing power and a read on underlying demand in an economy.

For example, since the 2020 lows, China's producer price index climbed to almost 15% yet the CPI barely budged above 2% y/y growth over the same period. Compare that to the US where the PPI rose to almost 12% yet the CPI tracked closely peaking above 9% meaning input costs couldn't be passed onto consumers as effectively in China.

So, I think China is sort of "threading the needle" avoiding negative real growth these last few GDP prints in the sense - the Chinese CPI is quite low and nominal growth/aggregate demand is weak though not recessionary yet.

The 5% growth target was abandoned in 2022 instead aiming for "best possible results" Last time the growth target was put to the side was 2015 which was a concerning year for China, the yuan and the commodity sector.

China retail sales continuing to under pace industrial production and fixed-asset-investment signals reliance on the state-controlled supply side of the economy and pours cold water on the idea of a "beautiful" consumer rebalancing over the near-intermediate term.

I think weak Chinese economic data will lead the move lower in PBOC rates because the authorities in China want to rebalance and restructure the economy without igniting speculative activity particularly in stocks and housing markets so lower rates in China will occur after or while their economic downturn unfolds, rather than preempt it.

Moving PBOC policy accommodative too soon would risk "blowing further bubbles" rather than the ideal scenario where the need for adjustments in the growth model are acknowledged (not saying there won't be adjustment costs to Chinese growth and asset prices) though the roadblock to future growth, such as an overleveraged banking system, too high of PBOC rates, an inefficient construction-driven growth model, declining export competitiveness, overvalued real estate markets, among others will be cleared and China's monetary policy would be positioned accordingly to navigate the downturn, rebalance and grow again over the intermediate and long term at that point.

In conclusion, I am particularly bearish on inflation hedge assets such gold, energy and commodities. I think negative real GDP growth due to a persistently high CPI (stagflation) and a too dovish Fed is unlikely even if I think the Fed could be a little more aggressive.

I think real yields (inflation-expectation-adjusted) rise. The Fed has raised very fast and I think the slowing down in pace recently (with potential to ramp back up to 50bp hikes) is a vote of confidence their policy will work and also a warning on global recessionary and disinflationary impulses.

Getting to 2% CPI will require higher inflation expectation adjusted real yields, lower asset prices, a commodity (input) price downturn, and a monetary policy by the Federal Reserve built for the US - not to procrastinate a downturn and adjustment in China, EM economies and EM currencies. I think US growth will be resilient in real and nominal terms, rather than the scenario of continued inflation eroding nominal growth to a negative real figure. I believe US aggregate demand will be okay allowing the Fed to stay the course back to 2% CPI with the Fed Funds Rate being held above 5% while the emerging market downturn and adjustment happens in the background.

For further details see:

Emerging Market Risks And U.S. Economic Landings