CA - Enbridge: 7.58% Yield For A Rich Retirement

2024-01-20 06:07:56 ET

Summary

- Enbridge Inc. is a top investment for retirement, offering high yield, safety, and sustainable dividends.

- The company has become the largest midstream company in North America, focusing on pipelines, gas storage, and renewable energy.

- Enbridge is currently trading at a potential 25% discount to its fair value, with the possibility of achieving annual returns exceeding 14% over the next 3 years.

- The 7.58% dividend yield is well-covered with a 1.5x distribution coverage, and it is expected to grow at a rate of 3% annually.

If you are already enjoying your retirement or perhaps nearing it, the investment priorities naturally shift towards high yield over total returns. You prioritize the safety of your investments and the sustainability of dividends to continuously fund your lifestyle without having to worry.

In today's investment landscape when reasonable valuations are scarce, it might be challenging to find the combination of all three characteristics; however, Enbridge Inc. (ENB) is one of the top investments that comes to mind when thinking of a rich retirement.

Enbridge is the largest midstream company in North America with a $76 billion market cap, headquartered in Canada. With today's distribution yield of 7.58% and 1.5x distribution coverage, expected to grow the dividend at a rate of 3% CAGR over the next years, this investment becomes a no-brainer for income hungry investors.

The company is trading today at 7.9x its P/OCF, well below its historical valuation, implying a potential discount of 25% to its fair value alongside margin of safety and the potential for 14%+ annual returns over the next 3 years.

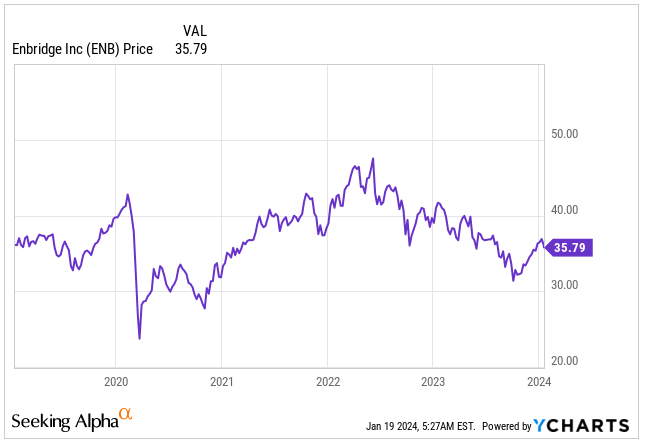

Price Development (Seeking Alpha)

{kind=link}

Energy Demand Is Not Going To Fade...

When I talk about investment opportunities in the energy sector, like Enbridge, people often ask why anyone would invest in a business centered around fossil fuels.

This question arises, especially considering the strong push from both the government and society toward more sustainable energy sources such as hydropower, wind, or solar, with the anticipation that fossil fuels will eventually be phased out .

The key here is to question whether the phase-out of fossil fuels is indeed imminent, since data suggests otherwise.

While I fully support the transition to net-zero and the adoption of alternative, more sustainable energy sources, we need to recognize that between 2010 and 2050, the demand for energy is projected to surge.

Although the gap is expected to be mainly filled by the growth of renewables, it's crucial to note that natural gas, petroleum, and other liquid sources are also projected to expand, albeit at a slower pace.

Energy Mix Growth (EIA)

It's essential to acknowledge that fossil fuels won't vanish overnight; instead, they will coexist alongside other, perhaps more sustainable energy sources.

Enbridge benefits significantly from the increasing demand for energy, which serves as a major tailwind for the company. The reliance of our economies, built on fossil fuels, provides a protective layer for Enbridge's business.

While Enbridge is primarily known for its pipelines, specializing in the transportation of commodities like natural gas, crude oil, and other liquids - a characteristic of a midstream company - the whole picture is more nuanced.

Enbridge goes beyond traditional midstream operations, with its energy segment that actively extends its footprint into the renewable energy sector. The company not only invests in but also operates projects involving wind, solar, and hydropower.

It's natural that, as an energy company, Enbridge will experience some degree of volatility driven by the general dynamics of the energy sector, but also in relation to its ESG risks.

Yet, the company holds a BBB+ rating, with 98% of EBITDA generated from cost-of-service or contracted assets, reducing overall risk.

More than 95% of Enbridge's customers are investment grade, with 80% of EBITDA having inflation protection, ensuring that revenue does not fall behind in today's challenging environment.

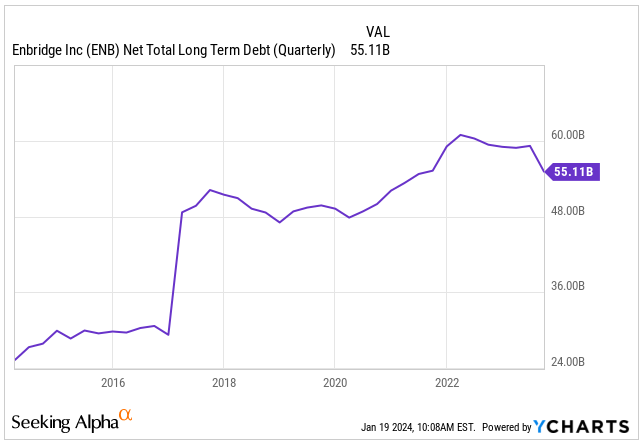

Furthermore, only roughly 10% of the 2024 interest expense is exposed to the floating rate, so higher rates are not a concern despite the elevated $55 billion net long-term debt.

Net Long Term Debt (Seeking Alpha)

{kind=link}

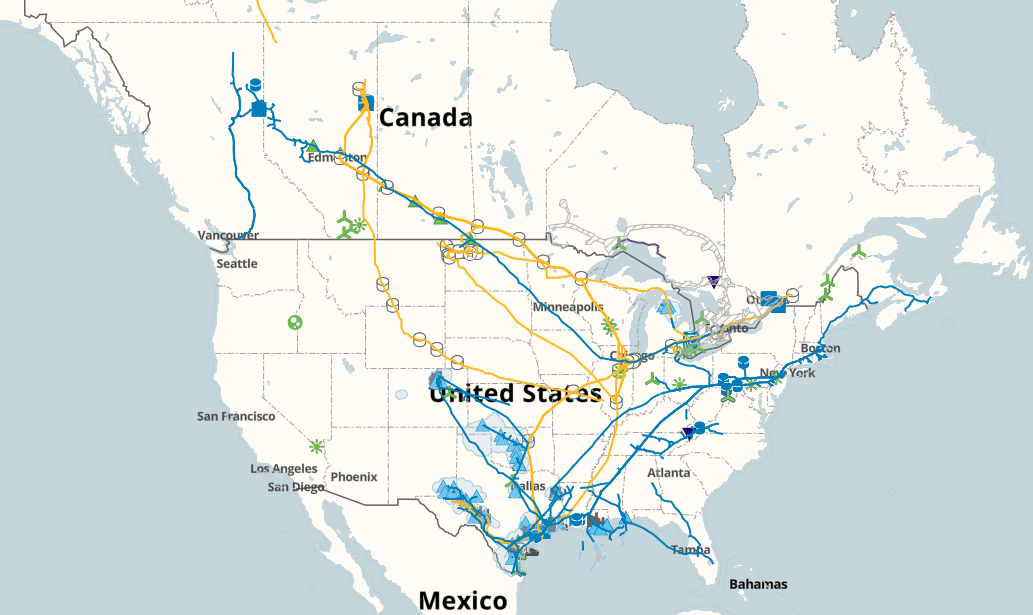

Back in 2017, Enbridge has merged with Spectra Energy, a step which has led to creation of the largest energy infrastructure company in North America spanning from North of Canada down to the key Gulf of Mexico.

This key investment has reduced the overall risk for Enbridge as the company diversified its geographical exposure and the business now offers a more balanced mix of 49% liquids, 47% gas and a smaller 4% renewable energy business, but this is the fastest growing area.

Enbridge's Network (ENB Website)

{kind=link}

Operating the largest pipeline network in an industry where size matters is key to unlocking value for shareholders. The stable cash flow from the liquid pipelines and gas midstream is providing the company with tons of EBITDA, which can be further redeployed into key growth areas, such as the renewable and carbon capture portfolio.

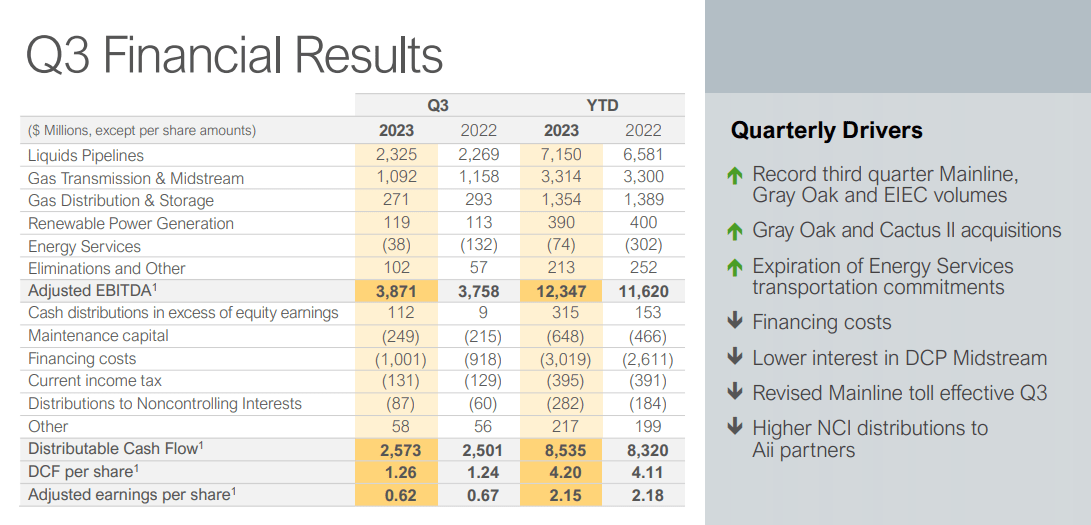

As of Q3 , Liquid pipelines accounted for 60% of the adjusted EBITDA, with gas transmission & midstream coming in second at 28%. Renewable power generation contributed 3% to the overall mix.

The good news is that for the quarter, the adjusted EBITDA grew YoY by 3%, and Enbridge has generated a significant amount of distributable cash flow, or 'DCF,' reaching CA$2.57 billion, marking a 2.8% increase YoY.

{kind=link}

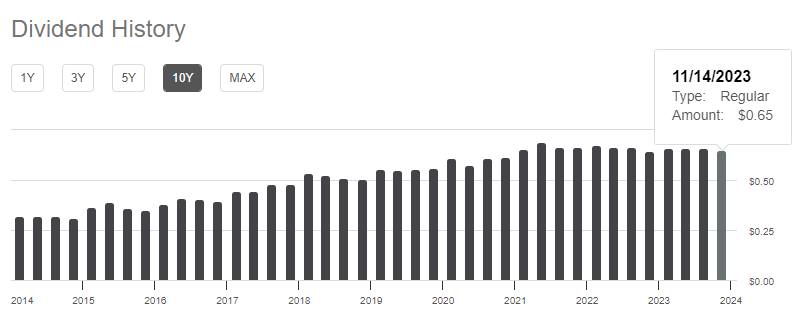

During this time, Enbridge also raised its dividend by 3%, with today's yield now being 7.58%, or $0.65 per share, placing it roughly in the middle when it comes to distribution compared to peers:

- Kinder Morgan ( KMI ) with dividend yield of 6.53%

- Enterprise Products Partners ( EPD ) 7.71%

- Energy Transfer ( ET ) 9.11%

With DCF per share being CA$1.26 in Q3 and assuming 1.35 USD/CAD FX, that would imply a distribution coverage of 1.43x, indicating significant stability and safety for the continuously growing dividend.

This coverage ratio guarantees that Enbridge has the financial capability to comfortably increase its dividend in FY24 while still having sufficient cash to invest in its business and potentially pursue additional acquisitions this year.

Dividend History (Seeking Alpha)

{kind=link}

Keep in mind that Enbridge common shares traded on the New York Stock Exchange (NYSE) and the Toronto Stock Exchange (TSX) will pay dividends in Canadian dollars . However, Enbridge provides payment to US holders of Enbridge common shares in US dollars, adjusted according to foreign exchange rates, implying potential volatility.

Dividends paid to US shareholders are subject to a 15% withholding tax; however, some US shareholders may have experienced up to a 53% withholding tax on their dividend payment if all the required tax forms were not completed. To avoid any withholdings on your dividend, one must complete the NR301 and W9 tax forms.

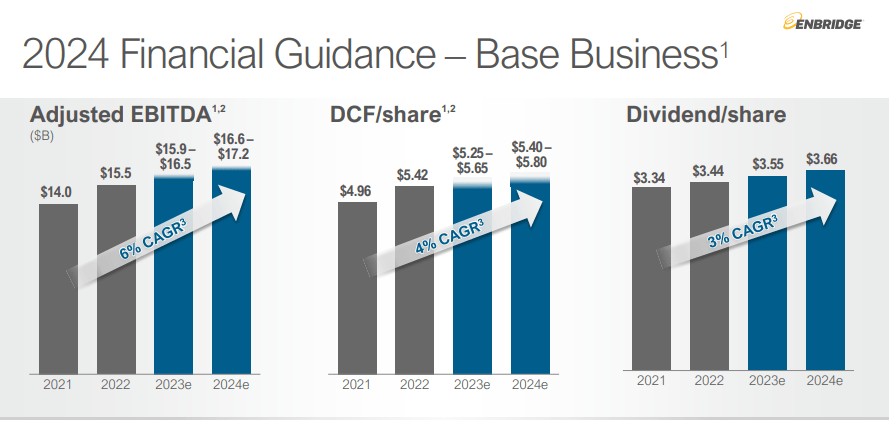

In September 2023, Dominion Energy ( D ) announced an agreement to sell three gas distribution companies to Enbridge. This $14 billion deal , comprising an all-cash consideration of $9.4 billion plus debt, which is highly credit accretive, anticipates utilizing 100% of after-tax proceeds to retire debt. The transaction is expected to close by the end of 2024, pending regulatory approvals.

While the acquisition is not projected to have a significant impact in 2024, the company is still expected to experience substantial growth. Management forecasts a growth of approximately 4.4% in adjusted EBITDA, a 2.9% increase in DCF per share, and a 3.1% growth in dividend.

{kind=link}

Valuation

As the interest rate cycle peaks and investors shift towards cash markets to minimize risk, high-yield companies, including Enbridge, have faced repercussions despite the business's quality.

The stock hit a low of $31 in October 2023 but has since rebounded, currently trading at around $35 to $36.

It's crucial to recognize that elevated interest rates are unlikely to persist indefinitely, especially with the FED signaling a pivot in 2024.

This shift will likely lure income-seeking investors back to equity markets, driving up the stock prices of high-yield companies.

Remaining in cash for an extended period may result in missed opportunities to invest in excellent businesses like Enbridge at discounted prices.

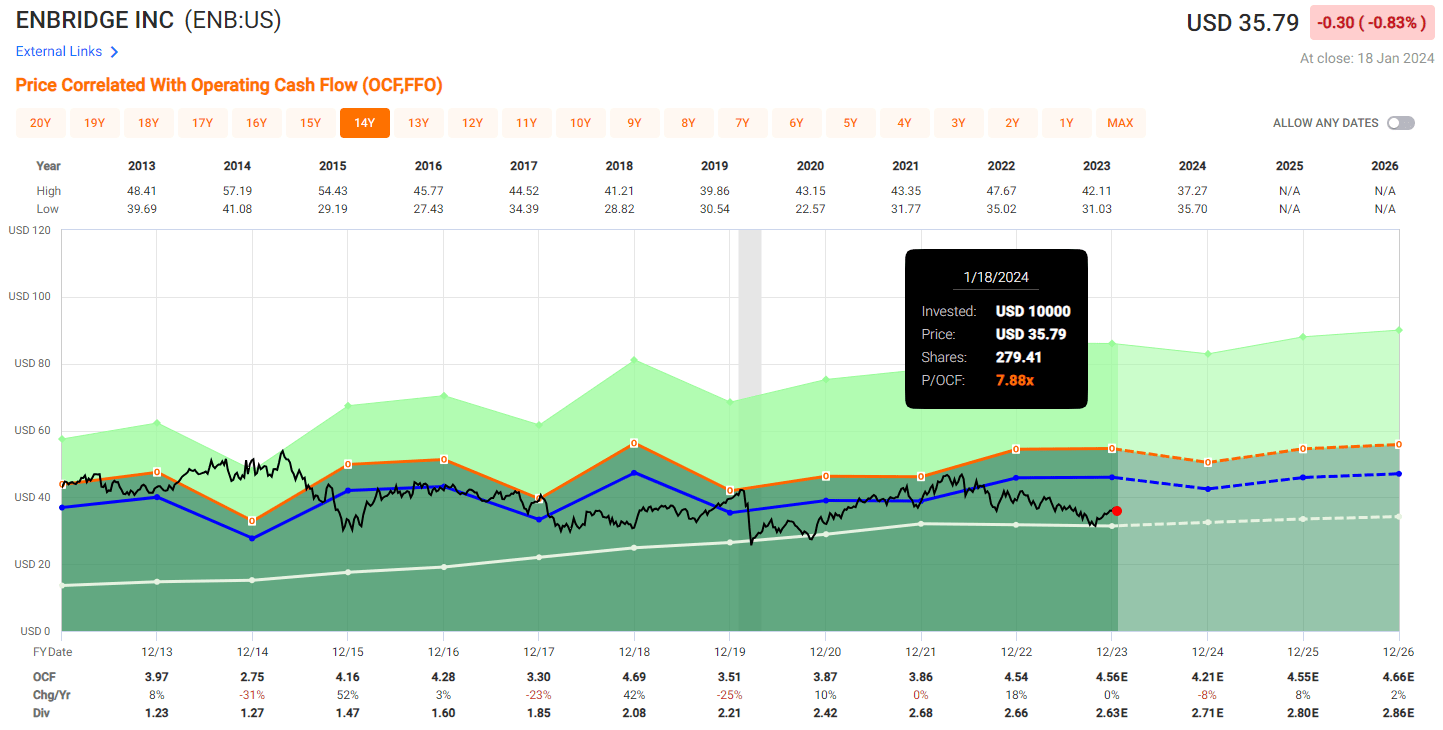

Currently, the stock on the NYSE is trading at 7.88x its blended P/OCF, notably below the average of 10.09x P/OCF since 2012.

During this period, OCF growth has averaged 1.74% annually.

Analysts are projecting similar growth over the next three years:

- 2024 : OCF $4.21E, -8% YoY

- 2025 : OCF $4.55E, +8% YoY

- 2026 : OCF $4.66E, +2% YoY

Enbridge Valuation (Fast Graphs)

{kind=link}

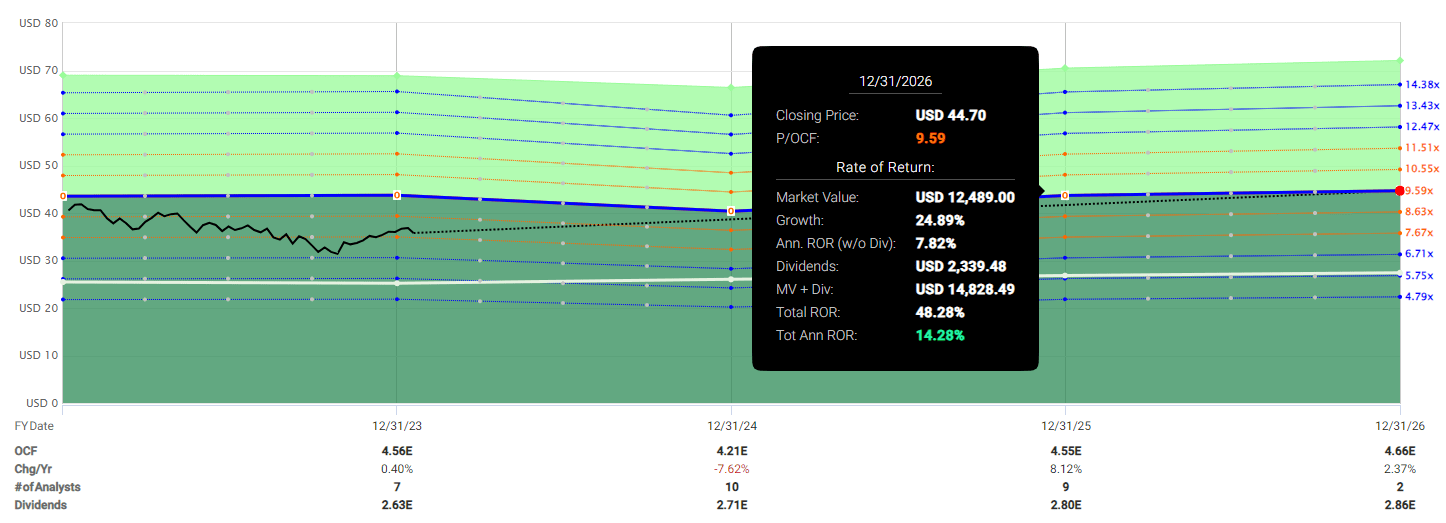

If this growth unfolds as anticipated and Enbridge reverts to trading at its average valuation, which I believe is likely, we could reasonably expect annual returns to hover around 14%.

Considering today's price of $35.8, I view the stock as a favorable buy for initiating a position.

However, if there is any additional decline toward $32, it would considerably enhance the potential return, prompting me to classify the stock as a strong buy.

On the other hand, if the stock price continues to rise, I would refrain from purchasing it above $37.

Potential Return (Fast Graphs)

{kind=link}

Takeaway

Enbridge stands as the largest midstream company in North America, boasting a substantial $76 billion market capitalization and headquartered in Canada.

As global energy consumption continues to rise and government initiatives to phase out fossil fuels appear unlikely, Enbridge emerges as a key beneficiary in this landscape.

The company is currently generating significant distributable cash flow through its expanding pipeline business, driven by strategic acquisitions.

Enbridge is actively diversifying into the renewable energy sector, further contributing to its growth trajectory.

Today, the stock is trading at a discount of 7.9x its P/OCF, a notable departure from its historical valuation. This deviation presents an opportunity for potential investors, with the prospect of achieving annual returns exceeding 14% over the next three years.

With a current distribution yield of 7.58% and a 1.5x distribution coverage, coupled with an anticipated 3% CAGR for dividends in the coming years, this investment stands out as an attractive option for income-seeking investors and retirees alike.

For further details see:

Enbridge: 7.58% Yield For A Rich Retirement