CA - Enbridge Has It All

2023-05-14 07:00:39 ET

Summary

- Enbridge has an incredibly strong core business, generating massive EBITDA and cash flow at the cost of substantial debt.

- The company has a dividend yield of 6.5% it can comfortably afford, but it's committed to hefty capital investments.

- The company has rapidly focused on diversification, opening up a new segment of stable long-term earnings.

- Overall, the company might not be as cheap as some of its peers, but it has the valuation to drive significant returns.

Enbridge (ENB) is a multinational company headquartered in Canada. The company has strong renewable assets, a strong portfolio of midstream assets, diversification, and incredibly strong cash flow generation. As we'll see throughout this article, Enbridge's diversification and assets makes it a valuable long-term investment.

Enbridge 1Q Results

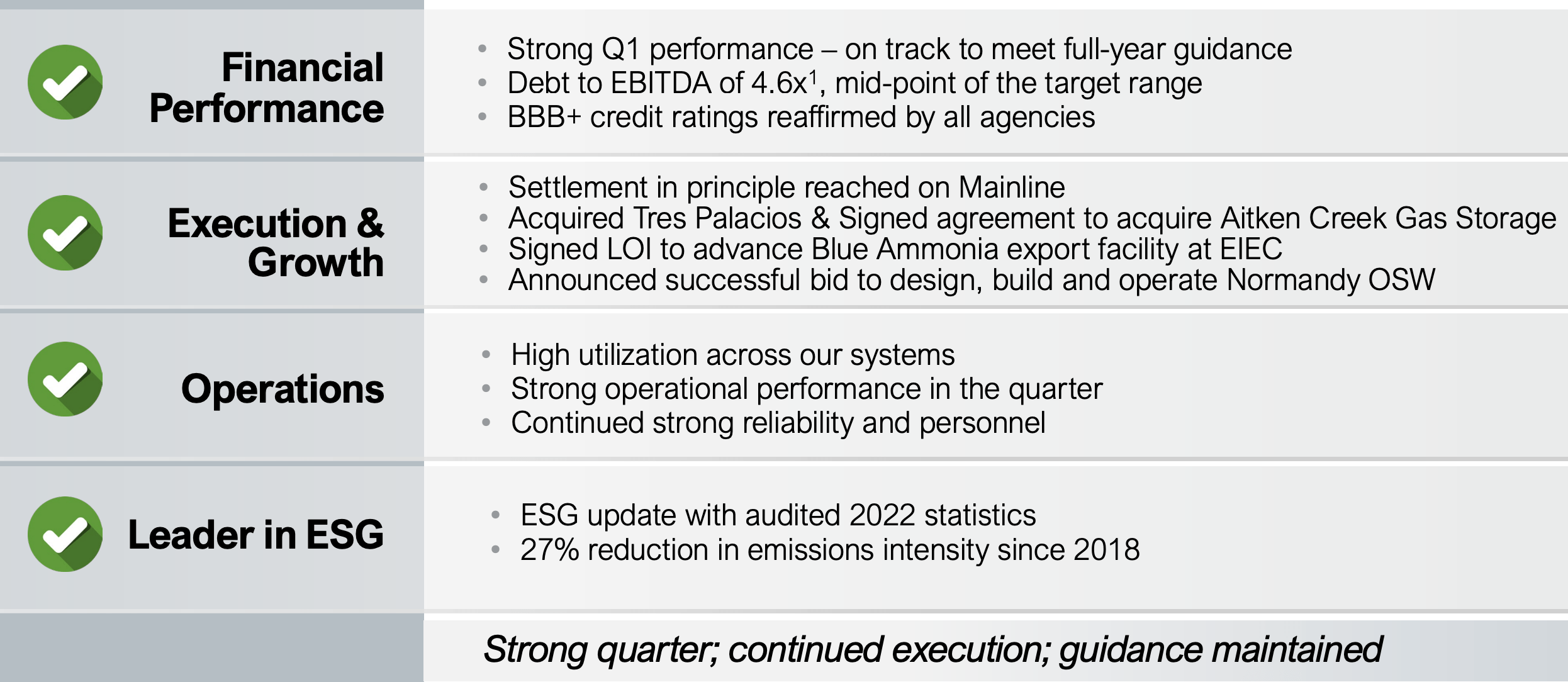

Enbridge generated strong 1Q results, highlighting its financial strength.

{kind=link}

The company remains on track to maintain its full-year guidance with strong earnings for the quarter. Its debt to EBITDA of 4.6x is lofty, with the company's net debt approaching $75 billion ($55 billion USD). The company does have a reasonable credit rating though and part of its debt is continued financial improvements. The company is maintaining high utilization.

Enbridge Mainline Tolling Agreement

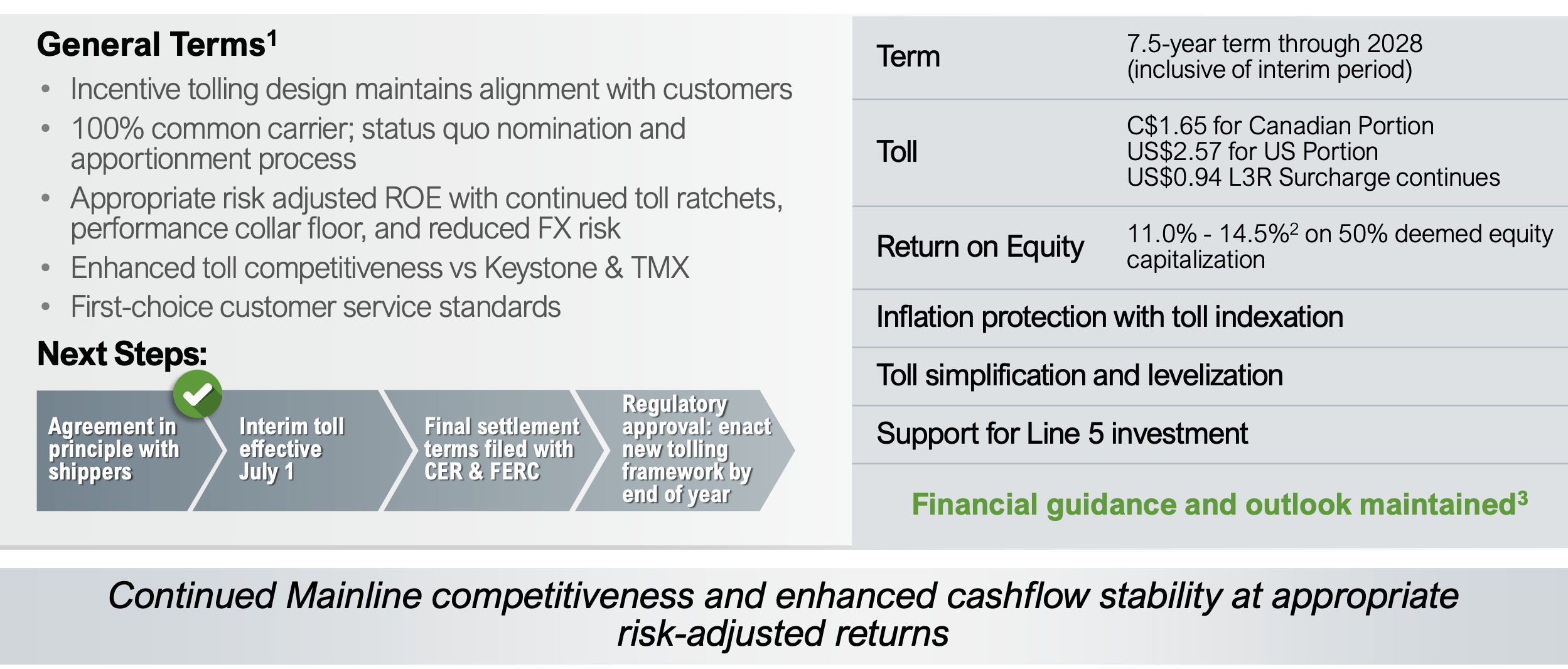

Among the most important of the company's assets is the mainline, which has a new tolling agreement.

{kind=link}

The new agreement will support Line 5 investment as the company struggles with a potential re-route or safety issue in the great lakes. The new agreement comes with higher tolls, double-digit returns on equity, and inflation protection. The new agreement has been agreed upon and will enable strong cash flow for the company with minimal risk.

This will continue to support strong cash flow for the company.

Enbridge Business Overview

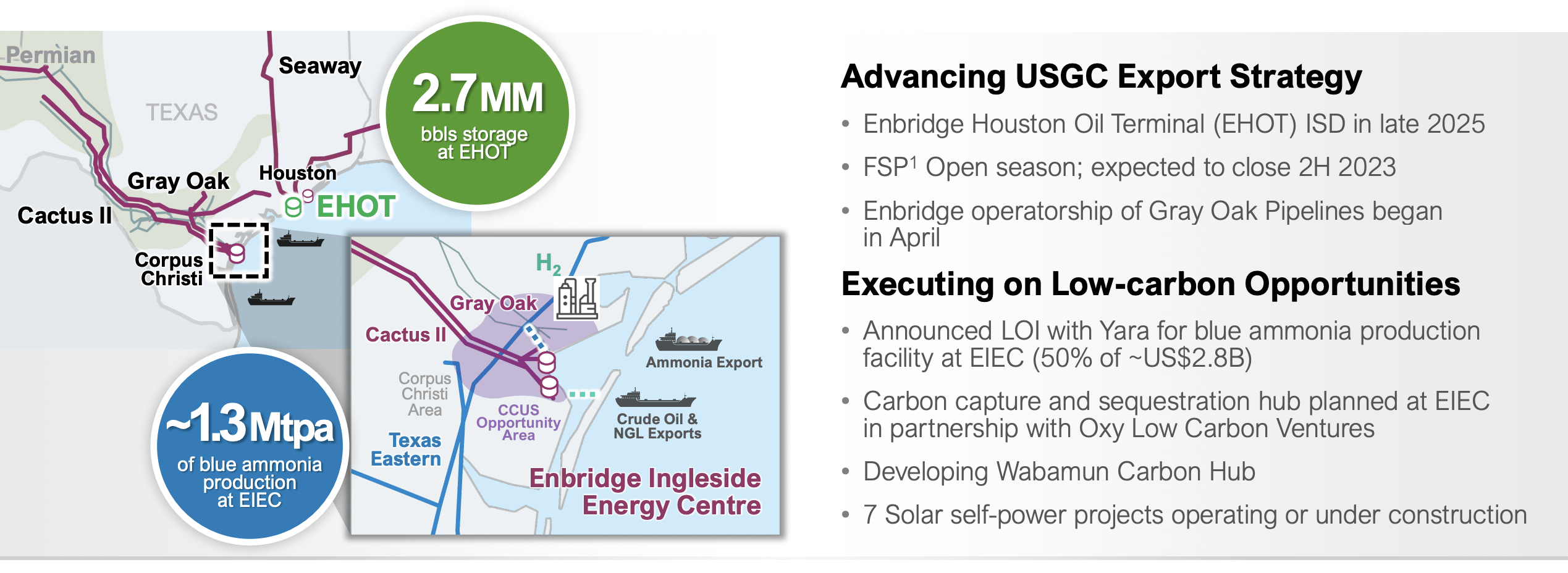

Overall, the company operates a diversified portfolio of business that it has continued to build on.

{kind=link}

The company has continued to build out its liquids business with new storage and blue ammonia production. The company is continuing to invest heavily in low-carbon facilities, and the Houston area remains the largest area of oil and gas infrastructure in the company. It also remains a hotbed of low carbon development, such as carbon capture & sequestration.

{kind=link}

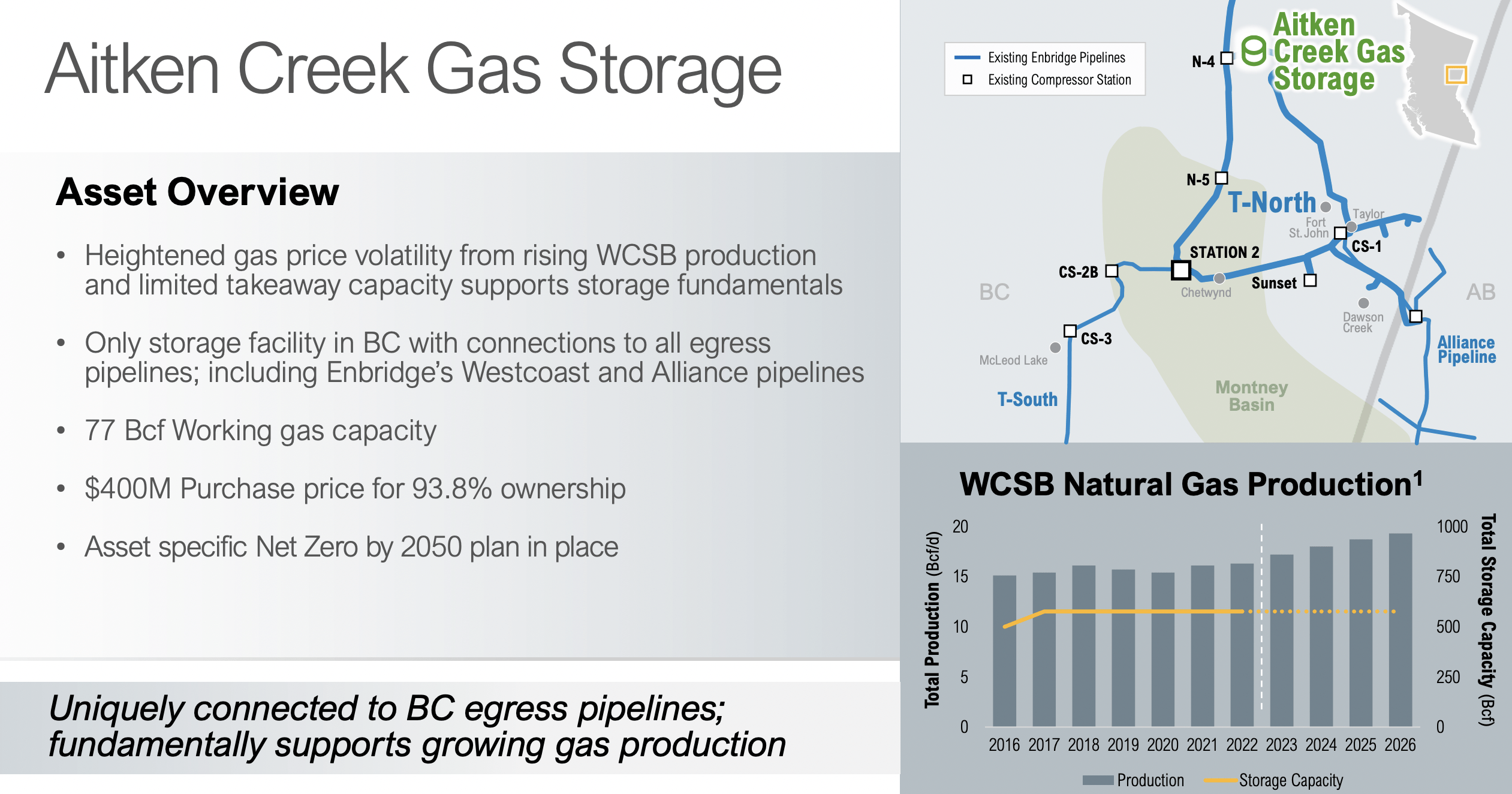

Another example of the company's growth is its acquisition of the Aitken Creek Gas Storage facility. The facility connects well to the company's assets and was purchased for a $400 million plan for just under 94% ownership. The asset takes advantage of limited storage capacity in a region where production is increasing, and its 77 Bcf working gas capacity is significant.

The company's integrated assets enable it to increase profits at every step.

{kind=link}

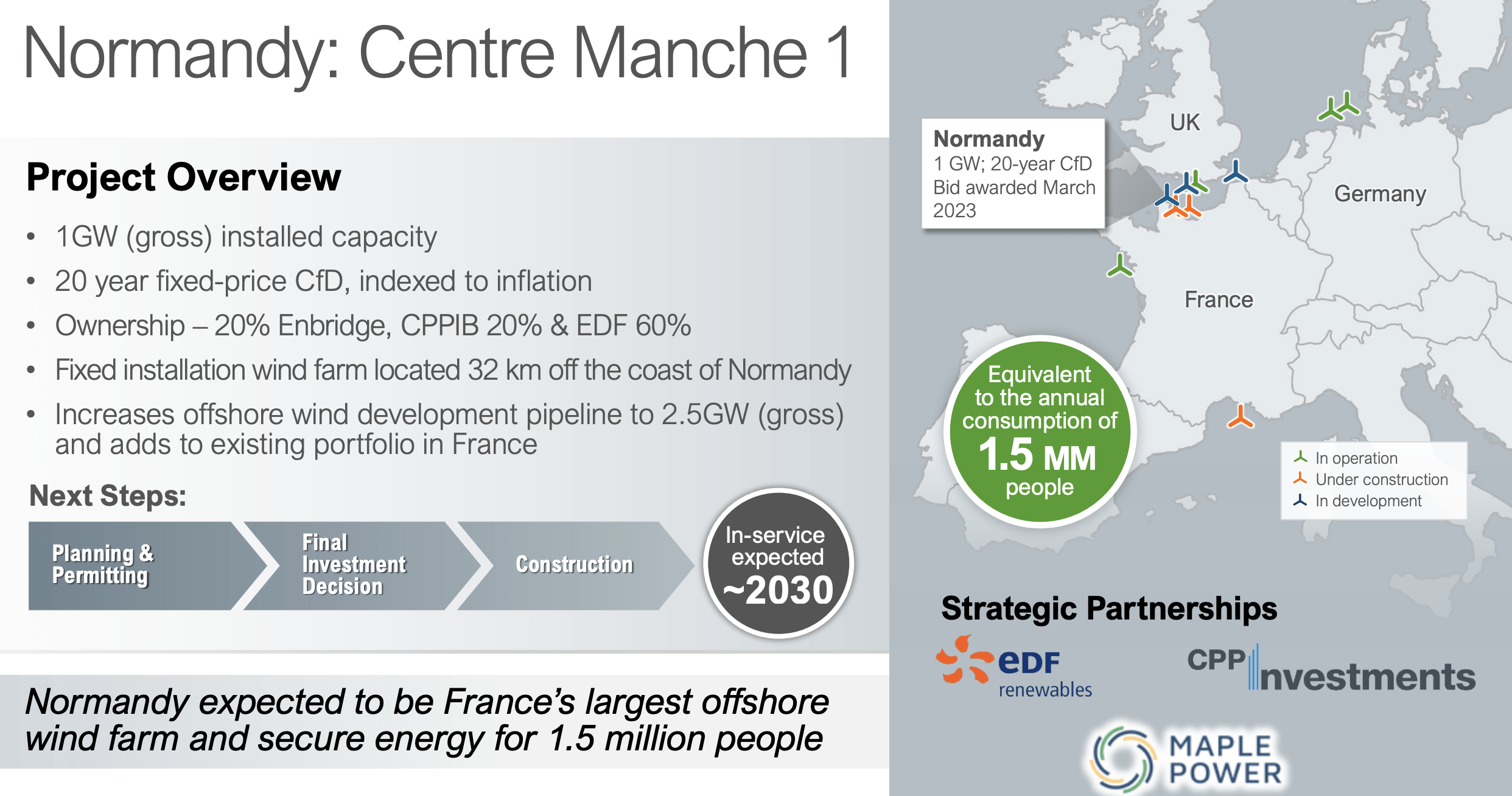

The last asset we want to discuss is the company's impressive renewable energy assets. The company has worked hard to diversify its business, while building a renewables business that generates incredibly strong long-term cash flow. The Normandy wind farm will provide electricity for 2% of France's population.

The company is installing 1 GW in gross capacity. Enbridge will have 20% ownership and 20% fixed earnings. Offshore wind is a massive area of growth and the company is working to expand its assets here substantially.

Enbridge 2023 Guidance

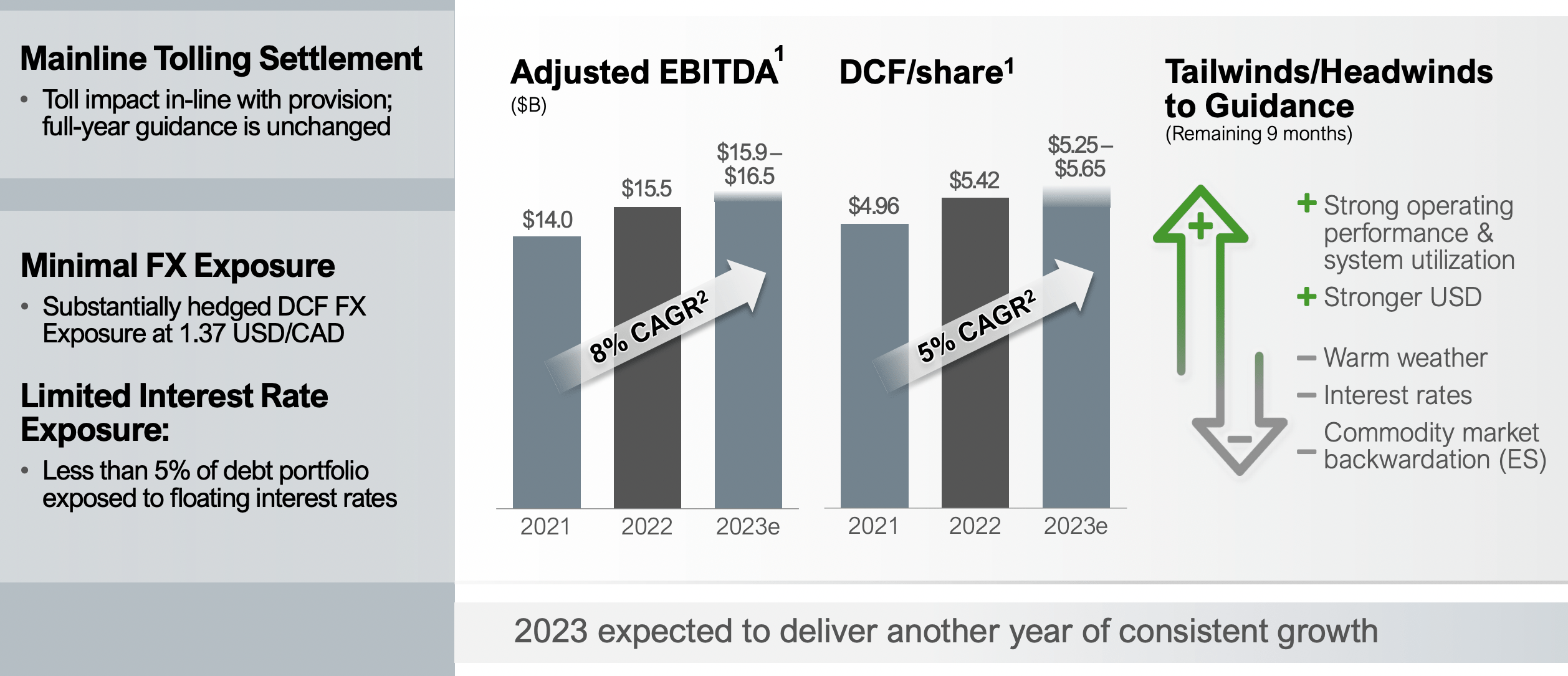

The company's 2023 guidance shows its continued cash flow strength and ability to drive returns.

{kind=link}

The company expects adjusted EBITDA to grow towards a midpoint of roughly $16.2 billion ($11.8 billion USD). The company expects DCF / share to hit $5.45 / share ($4 USD), versus a share price of just under $40 USD, indicating a 10% DCF yield. The company has been impacted some by warm weather (natural gas prices) but is continuing to perform well with its business.

The company's strong guidance will enable continued shareholder returns.

Enbridge Shareholder Return Potential

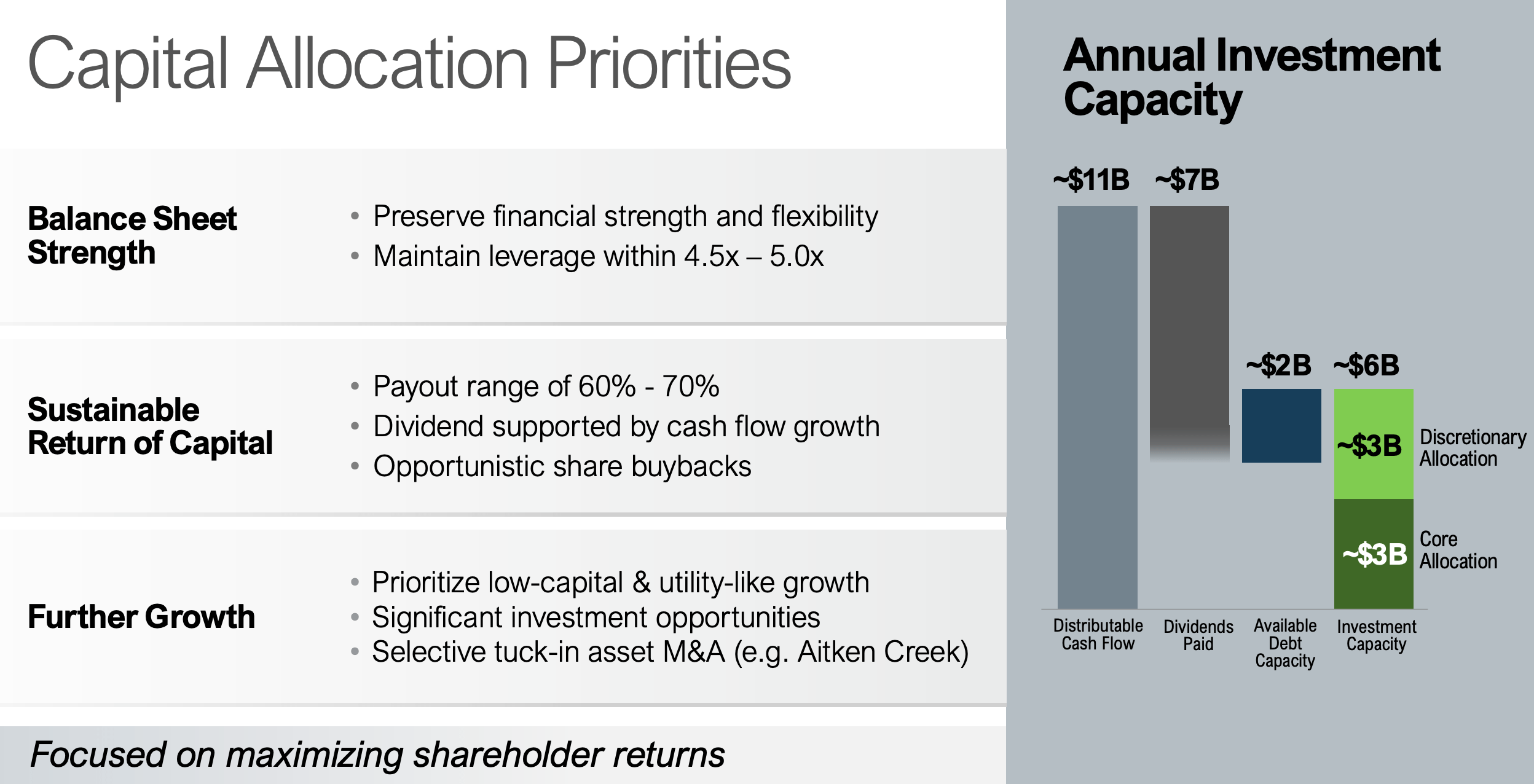

The company is continuing to invest in its business, and it has the ability to drive substantial shareholder returns.

{kind=link}

The company's annual DCF is $11 billion ($8 billion USD). The company pays out roughly 60-70% of that to shareholders, resulting in its dividend yield of almost 7%. The company plans to use $2 billion ($1.5 billion USD) in additional debt capacity as its EBITDA increases, resulting in roughly $6 billion ($4.5 billion USD) in annual investment capacity.

That's substantial capital investments. The company's secured capital program is $12.4 billion USD currently with ~$2.2 billion USD in the next two years, enabling the company to continue its growth with additional debt utilization. Most of this capital is expected to be natural gas, with renewable spending being more than oil spending.

Thesis Risk

The largest risk to our thesis is the company's lofty debt load. The company's debt load is especially risky in a rising interest rate environment, with potential Fx risk if the USD value stops going up because of a smaller interest rate differential with Canada. We'd like to see the company tone down its debt to <4x EBITDA to better prepare itself for a downturn.

Conclusion

Enbridge has it all. The company has an incredibly strong and valuable portfolio of midstream assets. However, it additionally has a new portfolio of renewable assets that it is building up as well. In many areas, the company delivers directly to the consumer, generating reliable long-term cash flows for the company.

Going forward, the company offers shareholders an almost 7% dividend yield along with continued investments in its business. We'd like to see the company manage its debt load a bit more versus continuously expanding. Regardless, however, of how the company spends its cash flow, it has the cash flow generation to generate substantial long-term shareholder returns.

For further details see:

Enbridge Has It All