CA - Enbridge: My Top Income Idea After Its 29th Annual Dividend Increase Of 3.1%

2023-12-12 09:00:00 ET

Summary

- Enbridge has announced its 29th consecutive annual dividend increase, providing shareholders with additional income for the holidays.

- Enbridge is considered a top income pick for 2024 due to its stable dividend, high yield, and projected earnings growth.

- The changing macroeconomic environment, with declining risk-free rates, could make Enbridge an attractive investment for income-seeking investors.

I love dividends, and Enbridge (ENB) just gave its shareholders a wonderful holiday present of more income. Part of my portfolio is dedicated to generating income which is continuously being reinvested. There are several income investments that I consider cornerstones, as their high yield is complemented by decades of annual increases. Enbridge just announced its 29th consecutive annual dividend increase after 69 years of paying dividends to its shareholders. I have been bullish on shares of Enbridge despite the market not reacting well to their announced acquisition of Dominion's (D) utility companies. It looks as though shares of Enbridge may have established a bottom, and the recent dividend increase could help generate some additional excitement as yields on the 2- and 10-year continue to retrace. I think we're likely to see shares of ENB return to the $40 level sometime in 2024, as its high yield and dividend growth will be very attractive to incoming capital from the sidelines looking to recreate the risk-free rate of return they were accustomed to as rates decline.

{kind=link}

Following up on my previous article about Enbridge

On September 6th, I wrote an article covering Enbridge's acquisition of 3 utility assets from Dominion ( can be read here ). I had discussed why I liked the deal, what it could mean for earnings, and how it could lead to stronger core earnings. Now that Q3 earnings are out, and Enbridge has just increased the dividend, I wanted to follow up on my previous article as discuss why Enbridge is my top income pick for 2024.

Enbridge keeps the tradition alive as they give shareholders additional income for the holidays

I am infatuated with dividends and have capital allocated toward many different income investments, from MLPs to BDCs and everything in between. I have investments in covered call ETFs, REITs, Closed-End Funds that specialize in corporate debt, and traditional equities. I am a fan of diversification and generating income from many different segments of the market. I had to think about what my top income idea for 2024 would be for some times as there are many candidates. While I could have gone with a fund or equity that had double-digit yields or a Dividend King that had at least 5 decades of dividend increases, I chose to select Enbridge. To come out and say that a specific investment is my top income idea for 2024, I wanted to select an investment that I felt would provide a combination of income and appreciation while having an income profile that was of the highest quality. I went back and forth with several ideas, and at the end of the day, Enbridge was at the top of my list.

{kind=link}

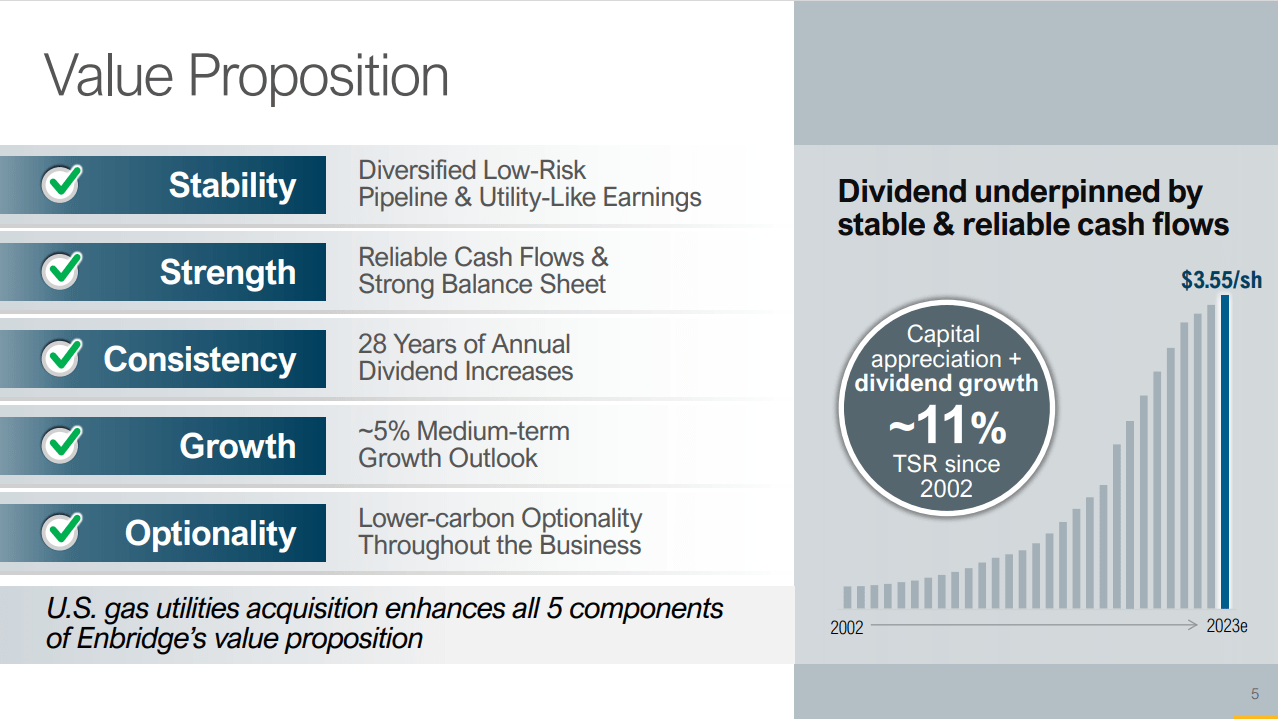

Everything about Enbridge's income profile screams quality, and there are no red flags. To be my top income idea, I need to believe that the dividend will remain intact beyond a shadow of a doubt. This just doesn't mean that the income profile is strong, but rather that the underlying business is so important that society wouldn't be able to function without it. I would speculate that some readers would have guessed that my top income idea would have been Altria Group (MO) as it has a larger dividend yield, over 5-decades of dividend growth, and projected annual increases in the mid-single digit range over the next several years. I am very bullish on Altria, but there is increasing pressure on their business from government regulations to a society that is moving beyond smoking, and for those reasons, I can't place it in my top spot. Enbridge is the only triple threat in the energy infrastructure space that I know of, as it operates one of the largest pipeline networks, will have the largest gas utility segment in North America, and has a multi-billion asset renewable portfolio. Society can't function without energy or fossil fuels, and Enbridge is at the center of these markets, which protects their dividend.

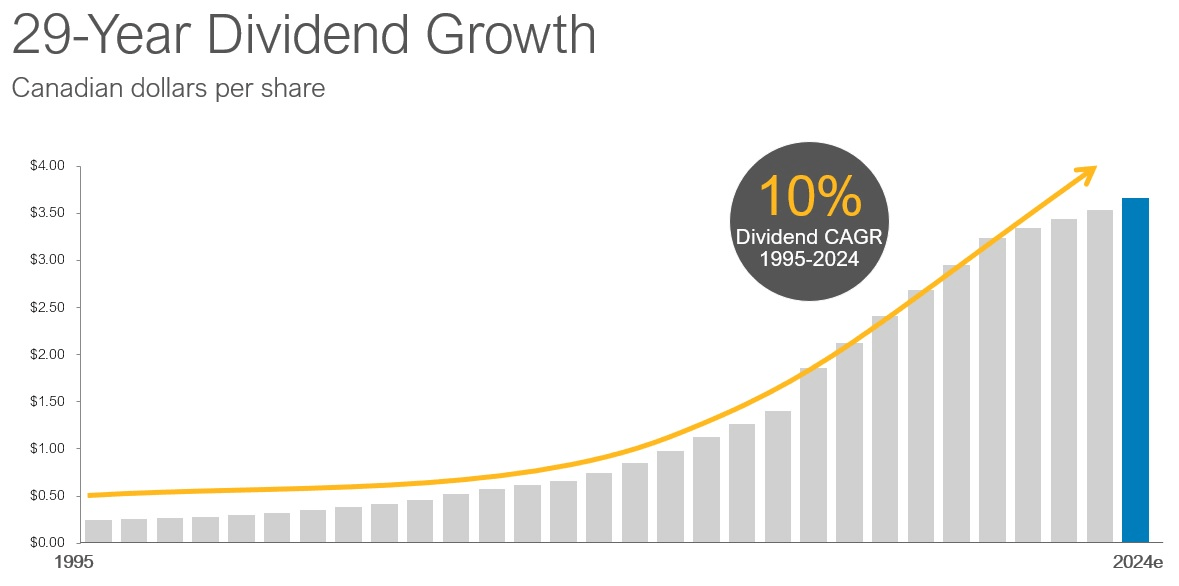

Enbridge has paid dividends for over 69 years and just recently announced its 29 consecutive annual dividend increase. Between these two metrics, the stability of Enbridge's dividend, especially after another dividend increase, is of the highest quality in my opinion. From a growth perspective, Enbridge's dividend has grown at a compound annual growth rate ((CAGR)) of 10% since 1995, as they just took the quarterly dividend from $0.8875 CAD to $0.915 CAD. On an annualized basis, shares of Enbridge are now paying $3.66 per share instead of $3.55 per share CAD. Since this is a Canadian company, the quarterly amount paid to investors in the U.S. could fluctuate due to currency exchange rates, but based on the current CAD to USD rates , the U.S. annual dividend payment would be $2.70, which is a 7.72% yield on Enbridge's current share price of $34.99.

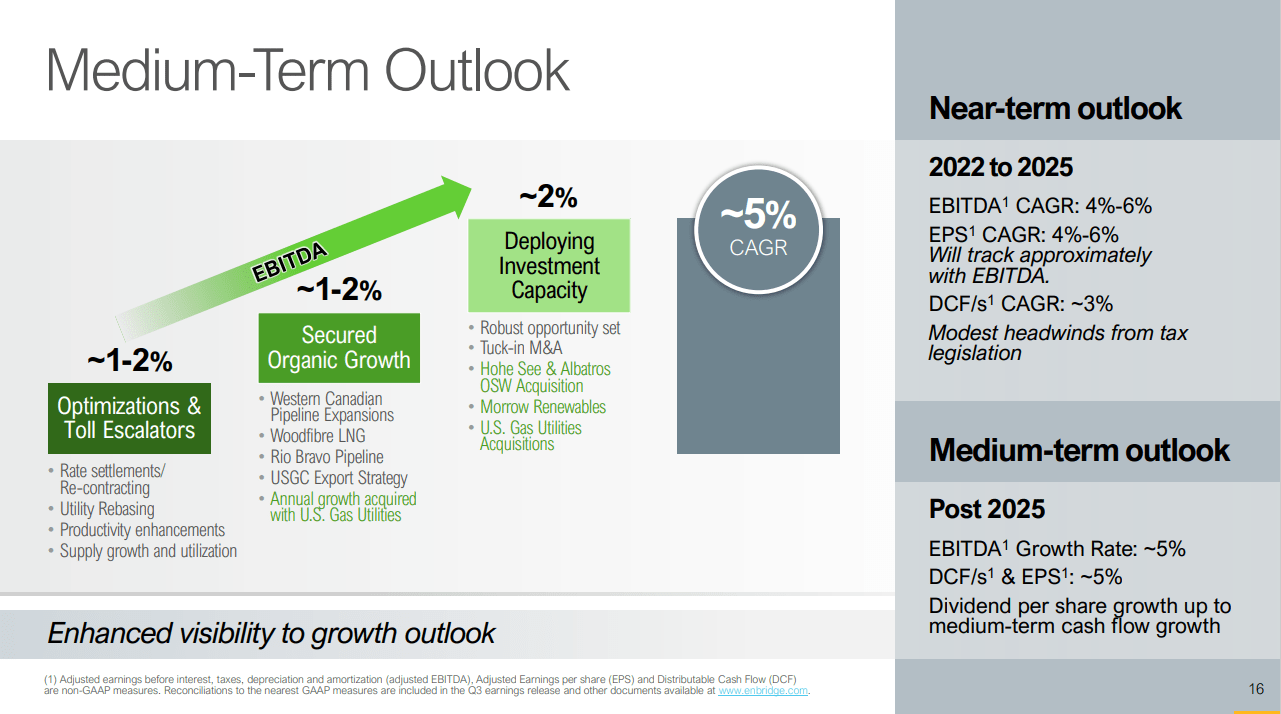

In Enbridge's Q3 earnings presentation , they projected that there would be 4-6% CAGR with EPS growth from 2022 through 2025. On November 29th when Enbridge increased the dividend, they also indicated that they would see higher core earnings in 2024 than what they had expected. Enbridge guided its EBITDA to come in at $16.6B - $17.2B CAD, which was more than 4% higher than the midpoint of its 2023 guidance. Enbridge also sees its distributable cash flow ((DCF)) coming in at $5.40 - $5.80 CAD per share, which is well above the newly established dividend of $3.66. This is the other reason why Enbridge is my top dividend idea. Enbridge's dividend has an impressive trailing history of dividend payments and annualized increases, but its forward outlook is also strong as the future dividend increases are expected to replicate the DCF growth on a percentage basis. Overall, Enbridge is my top income idea as its dividend has the longevity, high yield, and future earnings growth to support ongoing dividend increases in a macroeconomic environment where treasury yields are falling, and the Fed is expected to pivot in 2024.

{kind=link}

Enbridge could be extremely attractive to investors looking to recreate yields from risk free assets in 2024

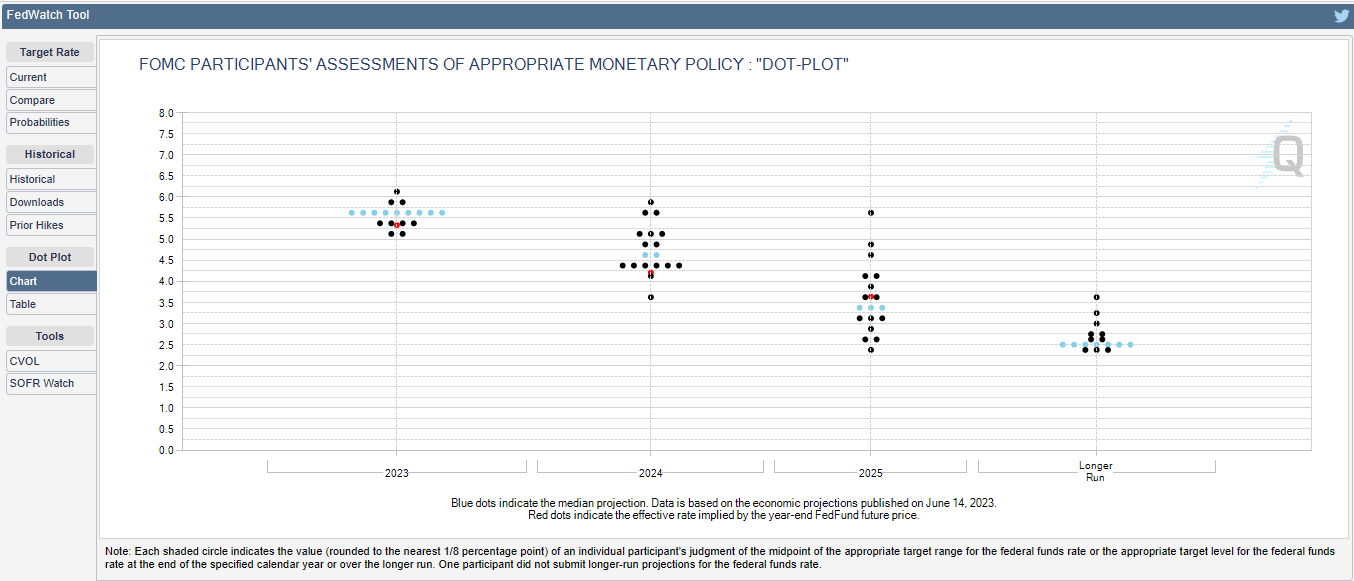

Over the past several months, the 2-year has gone from yielding 5.49% to 4.72% while the 10-year has declined from 5% to 4.24%. Nobody knows what Jerome Powell will say this Wednesday or what rates will do, but after the latest unemployment number, I am expecting him to remain hawkish rather than starting a victory lap. The CME Group is projecting that there is a 98.4% chance that rates will remain where they are and a 1.6% chance that the Fed will surprise us with a 25 bps increase. Whether the Fed pauses or shocks the market with a hike on Wednesday, the overall sentiment is that we are at the end of a tightening cycle and will rapidly approach a Fed pivot. Based on the Fed Dot Plot, we could see rates in the low 4s in 2024 and somewhere between 300 - 400 bps in 2025.

{kind=link}

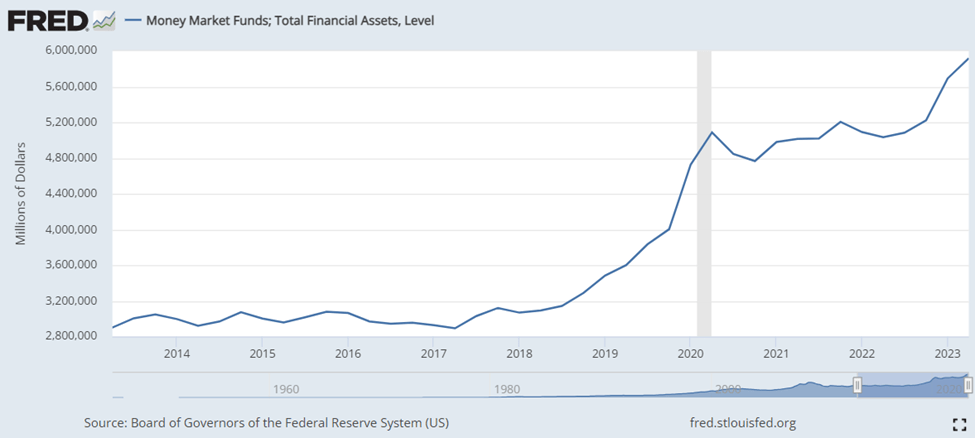

There is nearly $6 trillion in capital sitting idle in money market accounts due to the risk-free rate of return, but as we have seen with treasuries, it's starting to decline. I think that when the Fed does its first rate cut, the floodgates will open, and we will see a significant portion of capital flow into the capital markets from the sidelines. This doesn't include the possibility of additional capital finding its way into the markets from CDs and treasuries that are maturing from investors who established ladders from their cash. The capital sitting in money market accounts can be moved instantly, and I feel that investors who are using money market accounts as a proxy to generate income will look to get ahead of the curve and deploy capital to income-producing assets.

{kind=link}

I think Enbridge will benefit from a changing macroeconomic environment as they will be coming off a down year, and the risk-free rate will be declining. I think that companies with hard assets that produce large amounts of cash will come back into favor, and Enbridge will look very compelling. Enbridge is expecting to generate 4-6% growth in EBITDA and EPS annually through 2025 then in a post-2025 environment, its growth rate is expected to be around 5% for EBITDA, EPS, and DCF. This is due to $3 billion of capital programs coming online in 2023, $4 billion of projects in 2024, and another $17 billion from 2025 to 2027. Enbridge will be there to facilitate the demand and generate additional profitability, which will support the growing dividend as the demand for energy increases. I think the combination of the dividend yield providing a safety of margin for investors coming out of a risk-free environment combined with future earnings growth will be more than enough to attract income investors repositioning themselves in 2024.

{kind=link}

Conclusion

The holidays came early for Enbridge shareholders. Enbridge's dividend was increased for the 29th consecutive year, and investors got a 3.1% raise. There are many attractive income-producing companies out there, but Enbridge is my top income idea for 2024. I think that the strategic investments that Enbridge has made will allow them to provide annual dividend increases for the foreseeable future, and investors will be able to compound their way into significantly more dividend income. Capital will be looking for a home as the cutting cycle begins, and the combination of high yield, increasing profits, and a dividend CAGR of 10% over the past 29 years will be compelling reasons for capital to flow into Enbridge. I plan on adding to my position over the next several months until Enbridge reaches $40.

For further details see:

Enbridge: My Top Income Idea After Its 29th Annual Dividend Increase Of 3.1%