CA - Enbridge: Running With The Bulls (Maintaining A Buy)

2024-01-08 07:20:22 ET

Summary

- Enbridge has raised its dividend by 3% and expects future increases in EBITDA and distributable cash flow, potentially increasing the yield on shares.

- Analysts have increased expectations for the stock, with price targets ranging from $43 to $61, representing a potential 67% upside.

- Enbridge has made recent deals in the renewables space and is building a solar farm in Ohio, expanding its exposure to renewable energy.

- We think ENB will meet or exceed targets for the coming quarters and are maintaining a buy at current levels.

Introduction

It's been several months since the last update on Enbridge, (ENB), and normally they wouldn't be due for another so soon. But, there are some new developments that merit a fresh look into the investability of the company.

{kind=link}

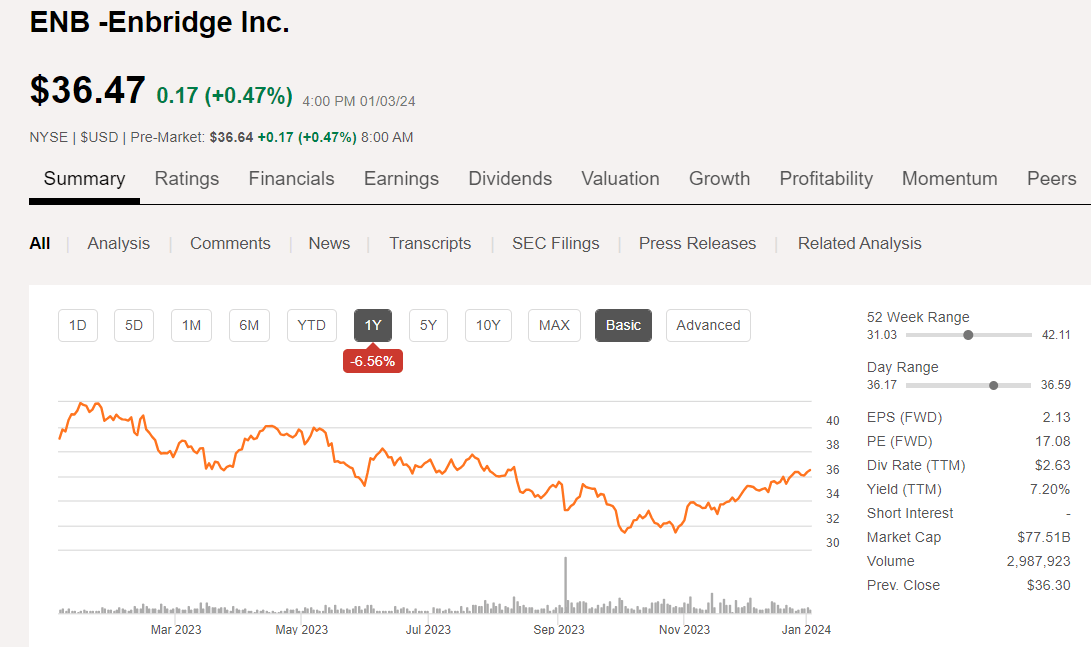

We last covered the company with a bullish article in late October. In it, we highlighted the company's move to shift the focus of their portfolio toward the distribution side of the business with the purchase of Dominion's, ( D ) distribution assets. It's been a decent call from a capital growth aspect, as the company is now trading above $36 and delivering an 8.1% yield on shares purchased at the time of publication.

The question now before us is - do we continue to add shares at the current level? The yield is down to 7.2%, and you will remember that I pitched ENB as a retirement income vehicle. I like growth as much as anyone, but I also like income. My real retirement income plan is predicated on having ~8% returns, and ENB fits right into that category. There are no guarantees these days - were there ever? That said, I find the chart below encouraging and have recently increased my position in ENB in my IRA and taxable accounts. ENB is now my third largest holding.

{kind=link}

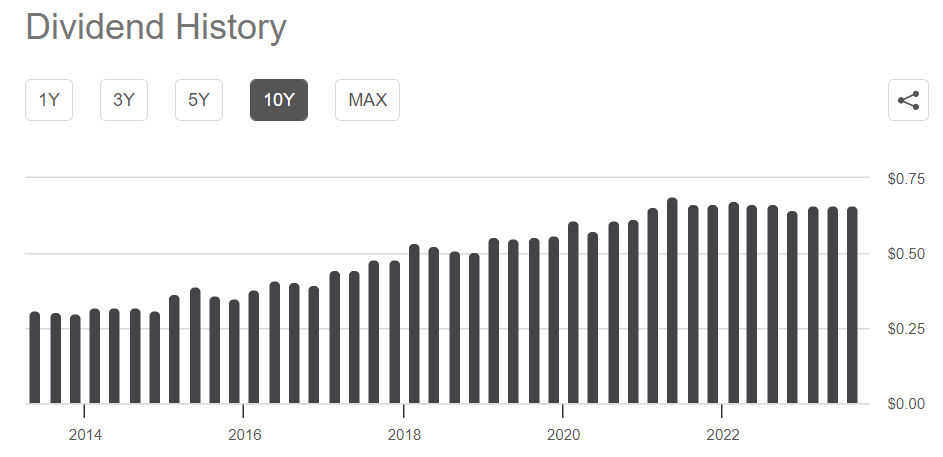

The current yield doesn't quite fit my 8% target, although 7.2% is nothing to sneeze at, but there is good news on that subject. ENB just raised the dividend 3% for an effective annual payout of $2.73 per share. And, noted in a release announcing the dividend increase , that they expect a 4% increase in EBITDA, ex-Dominion which doesn't close until sometime in 2024, and for distributable cash flow-DCF, to increase by 3%. That seems to pave the way for future increases that could increase the yield on shares bought at current levels.

The analyst cadre has increased expectations for the stock while maintaining an Overweight rating. Price targets range from $43.00 on the low side, to an outlier of $61.00. The median is $53.00, putting a solid 67% upside to today's pricing. That works for me. We may have a little fun with numbers to see what it might take to get to the median of the analyst's projections, as we close out the article.

The thesis for ENB

As a provider of various energy-related midstream services, the company operates through five segments: Liquids Pipelines, Gas Transmission and Midstream, Gas Distribution and Storage, Renewable Power Generation, and Energy Services. As noted, the recent Dominion acquisition was targeted to increase the proportion that comes from their distribution business. As we noted in the last article, most of this infrastructure lies in states that have not been adversely targeting the gas industry, making for a more favorable operating environment. As a critical provider of energy-related midstream services, the company is poised to participate in the robust production of shale-based resources.

Post earnings deals

Recent deals have been in the renewables space to fill out the Renewable Power Generation segment's portfolio.

The company has been increasing its exposure in the Renewable Gas-RNG, space with its acquisition of seven landfill sites in Texas and Arkansas to take produced gas and upgrade it to pipeline-quality methane. Once this happens, it can be blended with other methane sources, and is of course a Carbon-Neutral fuel. This avails it of tax credits that are accretive to RNG.

Farther afield, ENB bought back a ~25% interest in some German Offshore Wind Farms that it sold to the Canada Pension Plan Investment Board-CPP, in 2018. The CAD$374 mm price looks like a slam dunk for ENB, as CPP paid them CAD$1.75 bn in 2018 . For what it's worth, Germans pay the highest electricity prices in the modern world, bless them.

ENB is also building a 150 MW solar farm in Ohio. This has a pretty rapid turnaround, as the company notes. Fox Squirrel will be constructed in three phases and is designed to ultimately deliver up to 577 MW of renewable energy to the utility grid by the end of 2024. A 20-year take-off contract is also in place for the power.

It's hard to throw stones at any of these deals on a cash flow basis. It will be interesting to see how the company paid for them. New debt or shareholder dilution appears to be the likely outcome here.

Line-5 updates

This saga has taken a turn in ENB's favor as the Michigan Public Service Commission approved its permit to build a tunnel to upgrade this ~70-year-old line. The commission noted in its approval:

The PSC said there is both a public need for the energy products Line 5 carries and a need to replace the underwater section to protect Great Lakes waters, and the company's plan offers the most prudent option.

You might think that ENB is out of the woods, so to speak with this permit in hand, but there are further gates to go through as this RBN blog post notes in its summary paragraph.

The tunnel and replacement project still needs essential permits from the Army Corps pertaining to the tunnel that will encapsulate the new single pipe. In March, the agency delayed issuing the needed approvals. It also held back the release of its draft Environmental Impact Statement ((EIS)) to the spring of 2025 from an earlier target of late 2023; a final EIS will be released in 2026. Enbridge expects it will take 3-4 years to build the project after the Army Corps' approvals, pushing the completion of the project back to at least 2029 .

So stay tuned on this one. One might wonder if the good people of Michigan know how tenuous their supply is of the 545K BOPD of crude and NGLs that are piped though it, might be? Probably not. Hopefully, that 70-year-old line-soon to be 77-year-old line will keep on, keeping on in the interim.

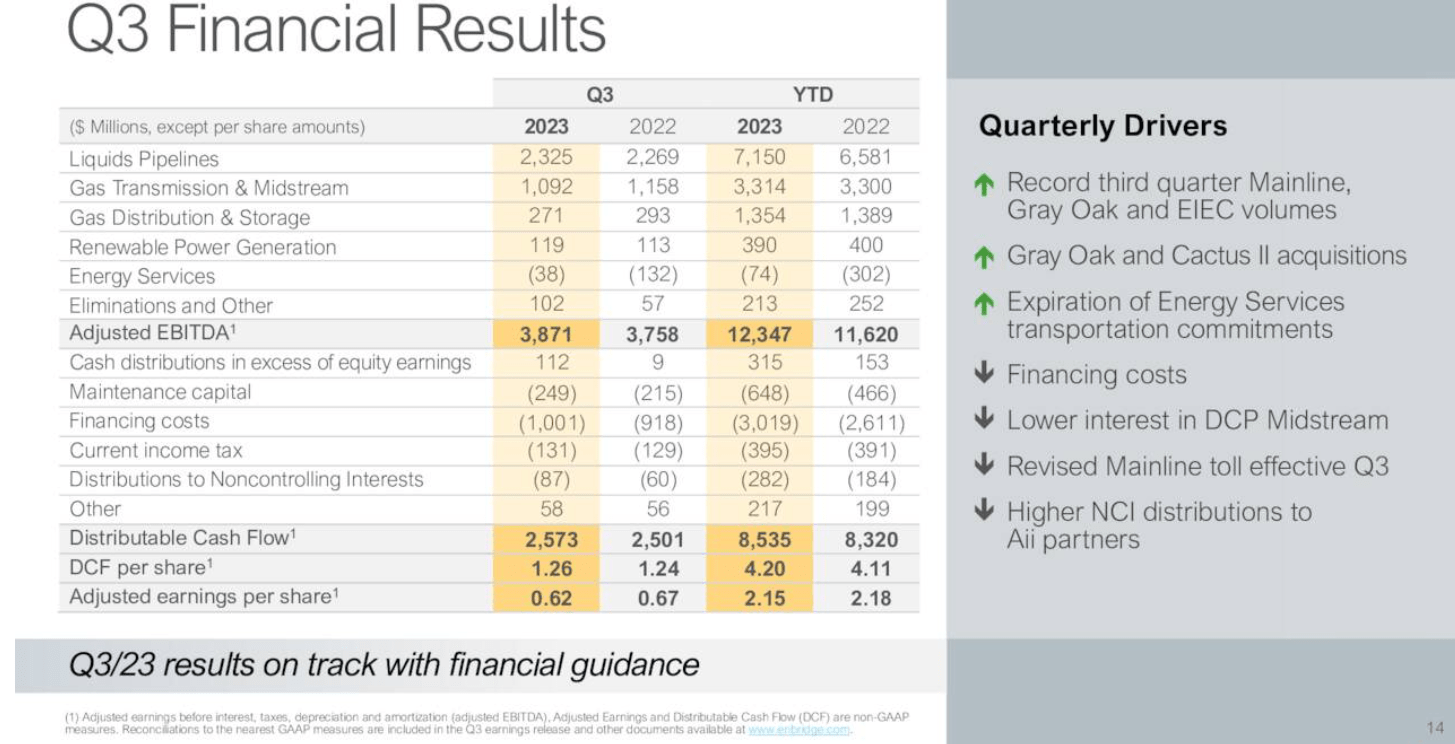

Q-3 and Guidance

ENB beat on the bottom line but missed on the top line, with lower tolls on the Mainline cited in the call. Revenues were $7,247 for Q-3, down from $7,848 in Q-2. What matters more to investors is that even with lower revenues, EBITDA and Distributable Cash Flow are increasing. A sign that profitability is building in the business.

{kind=link}

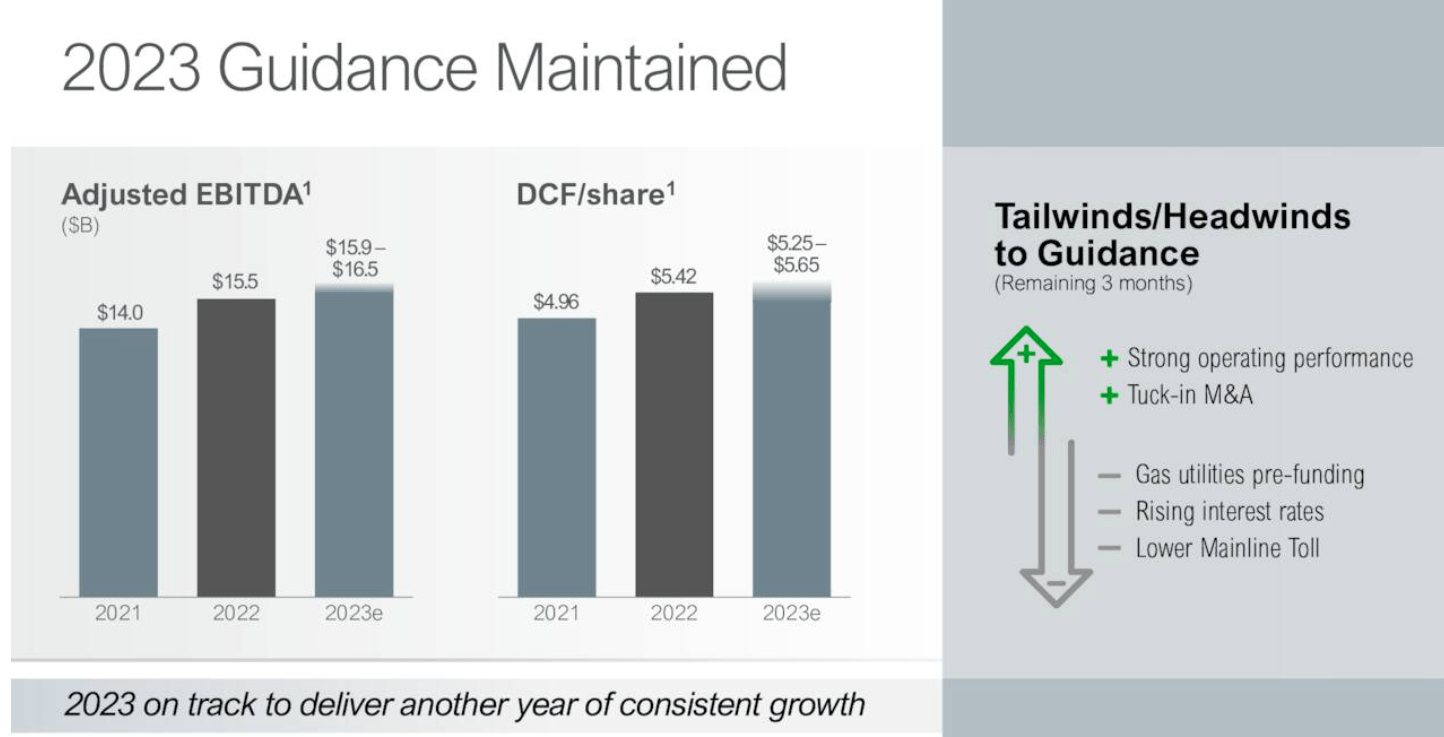

The slope on the EBITDA and DCF forward graphs below is also encouraging for those of us who would like our retirement income to increase.

{kind=link}

Your takeaway

On an EV/EBITDA basis, the company is trading at 7.56X on an NTM basis, which is probably what has the analysts rating the stock as Overweight. EPS projections have been increasing with Q-4, 2023 estimated at $0.69 per share, and Q-1, 2024 forecast at $0.79 per share. On a run rate basis, if they meet or beat these targets, shares could get a boost. For comparison competitors, Energy Transfer, ( ET ) is checking in at a 7.5X EV/EBITDA, and Energy Products Partners, ( EPD ) is at 10.2X.

Now for the part you read this far to read - FUN WITH NUMBERS ! ENB has forecast a 4% increase in 2024 EBITDA, which would land out at $16.8 bn using the midpoint of company guidance. If you apply that 7.5X multiple, you can deliver the upper end of analyst projections, ~$61 per share. Not too shabby from the present $36 or so.

Let's also remember that next year, EBITDA and DCF will get a boost from the new distribution assets hitting the balance sheet. ENB has forecast $18 bn of EBITDA for the full year, with the gas utilities consolidated to the balance sheet. Now remember, we are having FUN WITH NUMBERS ! In the scenario where that becomes a reality, that 7.5X multiple would take the share price to $67ish.

We remain bullish on ENB ahead of earnings. We are taking dividends as new shares and may add new money in this price range.

For further details see:

Enbridge: Running With The Bulls (Maintaining A Buy)