CA - Enbridge: Safe 7.7% Dividend Yield Plus Stellar Growth History

2023-11-28 07:30:00 ET

Summary

- Enbridge's recent underperformance is attributed to investor caution about its aggressive endeavors to become North America's largest gas utility company.

- Despite missing revenue estimates, Enbridge showed profitability expansion and strong operating leverage in its latest quarterly earnings.

- The company's strategic moves to diversify its revenue mix towards cleaner energy are likely to build a resilient business model.

- My valuation analysis suggests ENB stock is significantly undervalued.

Investment thesis

My initial bullish thesis about Enbridge ( ENB ) did not age well, as the total return was -4.5% since mid-July when my first article went live. This is a notable underperformance compared to the broader U.S. stock market, which demonstrated about a one percent increase over the same period. Investors are very cautious about the company's recent aggressive endeavors to become North America's largest gas utility company. But this move looks sound to me as the world is moving toward cleaner energy sources and the demand for natural gas across North America is expected to increase secularly. The company continues delivering strong operating leverage and wide free cash flow margins. This means that Enbridge is likely to sustain its stellar dividend growth history. Moreover, my valuation analysis suggests the stock is substantially undervalued. All in all, I reiterate my "Strong Buy" rating for Enbridge.

Recent developments

The latest quarterly earnings were released on November 3, when the company significantly missed revenue and GAAP EPS consensus estimates. Revenue dropped notably on a YoY basis by 16%. However, the revenue decline decelerated compared to the previous two quarters. Another good news is that despite revenue softness, Enbridge delivered profitability expansion, indicating strong resilience and a good sign for investors. The gross margin improved YoY by more than eight percentage points, which allowed the operating margin to improve by almost three percentage points.

Seeking Alpha

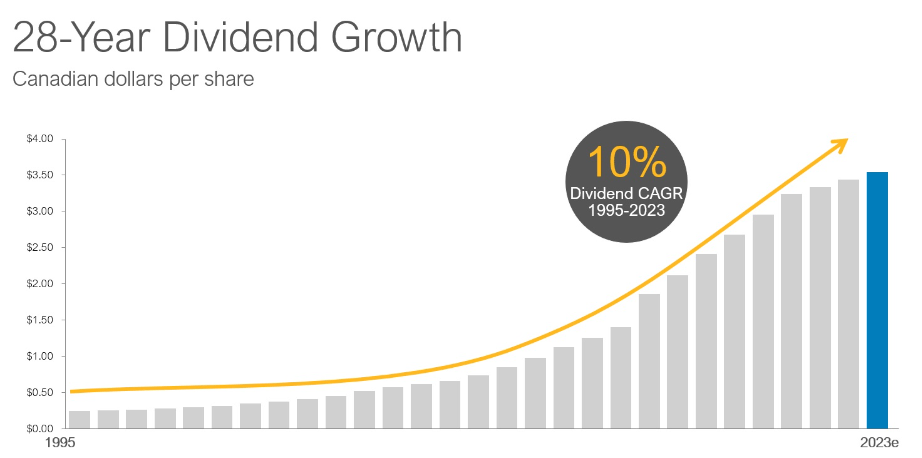

Strong operating leverage enabled ENB to improve its cash flow from operations by 46%. Strong operating cash flows mean the management will likely continue implementing its shareholder-friendly capital allocation approach of consistently increasing dividend payouts. Over the past 28 years , the dividend has grown at a 10% CAGR. The current dividend yield is around 7.7%, and the management strives to sustain the payout ratio within the 60% to 70% range .

{kind=link}

Enbridge's balance sheet is solid, with an above $2 billion outstanding cash position as of the latest reporting date. Liquidity metrics are also decent. The company is in a substantial net debt position, but the major part of the debt is long term, and a high level of debt has been inherent to the company over the last decade. That said, I do not consider substantial indebtedness as a significant risk for ENB.

Seeking Alpha

The earnings release for the upcoming quarter is scheduled for February 14, 2024. Consensus estimates forecast quarterly revenue at $9.73, which indicates a 3% YoY decline. Despite challenges for the top line, the adjusted EPS is expected to expand slightly from $0.47 to $0.50. It is crucial to underline that during the latest earnings call , the management reaffirmed its EBITDA and DCF per share guidance, demonstrating confidence in the financial outlook.

Seeking Alpha

Apart from the optimistic expectations regarding the company's near-term performance, I would also like to emphasize the management's strong strategic moves to build long-term shareholder value. Despite investors starting to sell off the stock after the company announced its acquisition of natural gas utilities from Dominion Energy ( D ), I think it was a sound move. The secular shift to decarbonization means that the demand for natural gas will grow as it is a much cleaner fossil fuel. The acquisition from Dominion made Enbridge the largest gas utilities company in North America, strategically positioning ENB to absorb the favorable secular trend of transition to clean energy. By expanding its presence in the U.S. utility sector, Enbridge secures a substantial volume of gas delivery and gains a strong foothold in critical regions.

That said, the recent announcement about acquiring U.S. renewable gas facilities also aligns with the company's strategic move to diversify its revenue mix towards cleaner energy. This move once again showcases the management's forward-looking approach to sustainable energy. These moves are set to diversify Enbridge's earnings mix, which is projected by the management to be 50% natural gas and renewables and 50% liquids. In my opinion, the more diversified mix enhances the overall resilience of the company's business model.

Enbridge's latest earnings presentation

I like the management's strong commitment to following a strategic plan to build a resilient, low-risk business model supported by the company's scale and diversification. The company's strong balance sheet, together with strong operating leverage, makes the company well-positioned to continue expanding its reach to become one of the leading North American companies to lead the decarbonization trend in the region.

Valuation update

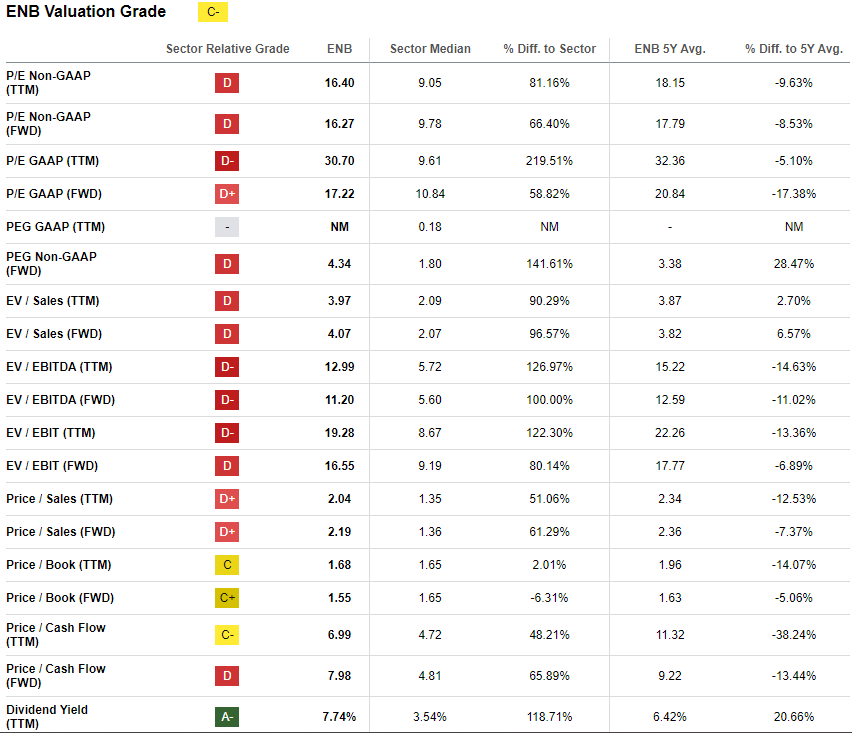

ENB declined by 12.3% year-to-date, significantly lagging behind the broader U.S. stock market and the energy sector ( XLE ). Seeking Alpha Quant assigns the stock a relatively low "C-" valuation grade, meaning the stock is overvalued. Indeed, ENB's valuation ratios are substantially higher than the sector median. On the other hand, many current valuation metrics are below the company's historical averages. That said, ratios analysis gives me a mixed picture, and it is difficult to conclude whether the stock is fairly valued or not.

{kind=link}

I want to proceed with the dividend discount model [DDM] simulation. I use the same 8% WACC as I did previously. Dividend consensus estimates forecast a $2.66 payout in FY 2024, which I also incorporate into my calculations together with a very conservative 2% dividend growth rate.

Author's calculations

According to my DDM simulation, the stock's fair price is around $45, which indicates a 30% upside potential. That said, I believe the stock is very attractively valued, especially given the forward dividend yield of 7.74%.

Risks update

ENB stock demonstrates relatively weak momentum , an apparent drawback for potential investors. The overall current market sentiment toward ENB is not favorable, and investors might need time to see the shift in the sentiment. The company will likely need to deliver a few quarters of beating quarterly earnings estimates for the sentiment to improve. That said, potential investors should know that it might take multiple quarters before the gap between the market stock price and the fair price will narrow.

While Enbridge's aggressive recent acquisitions opened new opportunities and improved the revenue mix for the company, integration risks are also significant. Operational integration poses potential challenges as merging diverse systems and corporate cultures demands exceptional execution to prevent disruptions. Enbridge's capacity to navigate these complexities will determine the ultimate success of its recent acquisitions and their contribution to shareholder value.

Bottom line

To conclude, ENB is still a "Strong Buy". The company demonstrates solid operating efficiency, which is converted into substantial positive cash flows. That increases the probability that Enbridge will sustain its shareholder-friendly capital allocation approach, and the 7.7% forward dividend rate and consistent growth are safe. My valuation analysis suggests the stock is substantially undervalued. Still, investors should be aware that it can take multiple quarters before the market stock price catches up with the fair price.

For further details see:

Enbridge: Safe 7.7% Dividend Yield Plus Stellar Growth History