CA - Enbridge: We're Backing Up The Sleigh

2023-11-28 07:00:00 ET

Summary

- Demand for infrastructure investments is at a record high, with global assets in listed infrastructure products reaching $111 billion.

- Enbridge Inc., a multinational pipeline and energy company, is viewed as a solid buy-and-hold investment with a 7-8% dividend yield.

- The company is well-positioned for growth in the renewables sector and has a conservative leverage target and strong profitability.

This article was coproduced with Wolf Report.

Demand for infrastructure investments is at the highest level on record, and assets in listed infrastructure products has reached $111 billion globally.

The appetite for infrastructure's attractive historical investment attributes include the opportunity for strong total returns, reduced volatility, and inflation protection.

We rarely discuss energy companies - midstream, upstream, or downstream.

Very recently, when Enbridge Inc. (ENB) dipped below $32 USD for the NYSE ticker, we started adding to this company, and have been adding since.

We invest in companies like Enbridge in two ways - either we go for the common shares, if we view them as appealing enough (or if that's the only option), or we're also open to investing in the debt/preferred shares ("prefs").

In this article, we'll show you why that is, and why we view Enbridge as a very solid buy-and-hold investment - or at least until the company hits more than $50/share, all things currently being equal.

Enbridge has a solid 7-8% dividend yield

Fundamentals for Enbridge speak for themselves.

The company has a market cap of over $72B with a credit rating of BBB+.

As a business, it's a multinational pipeline and energy company.

Its primary M.O. is the operation of pipelines through Canada and the U.S., transporting a variety of inputs and commodities, including but not limited to natgas, crude oil, and natgas liquid. It also has renewable income operations.

For the longest time, we weren't all that interested in Enbridge's common shares.

The prefs offered a far more compelling income upside.

That's one of our main reasons for investing in Enbridge - income.

The upside potential goes well beyond income, of course, but it's a very good "baseline."

The company's first name during incorporation was Interprovincial Pipe Line Company, by Imperial Oil in 1949 - and since that time, it has only been growing.

It was one of the first midstreams to invest in renewables, purchasing wind farms back in 2002, and has been consistently pushing to remain one of Canada's leading renewables.

Enbridge today is a very impressive operation. The company, generally speaking, is a play on a growing global energy demand , and we believe that demand is well-recorded and justified.

Enbridge IR

Not just that, but also growing exports of LNG, liquids, and overall renewable capacities both to Europe and Asia.

Also, following the Spectra merger, very few companies managed to come even close to this company's encompassing coverage in terms of its business mix and cash flow resilience as well as geographical diversification.

Enbridge IR

A higher amount of renewables, upwards of 8-10%, could be argued to be more desirable in this and the forward climate, but we believe this is something we'll see materializing over time.

The company is already establishing itself as a first choice in the renewables sector, with positioning in Europe through key assets.

The company is, therefore:

- The best liquids pipeline franchise in NA.

- One of the best gas transmission networks.

- N.A's largest natgas utility

- A significant and large renewable platform with...

- ....ongoing opportunities in carbon capture/lower carbon.

The company is predicting billion-dollar revenues, as well as ongoing growth from every single part of its business, with ongoing new upside from new energies of over $1B per year.

Its goals remain focused on conservative leverage - under 5x and around 4.5x, with a 60-70% payout range, currently delivered, with ongoing share buybacks when necessary.

Q3 2023 , which is the latest quarterly results we have access to, confirms these upsides and targets.

For the quarter, the company's YTD performance is on track with overall reaffirmed guidance.

The company has managed to put into place over $14B of funding for U.S. gas utility M&A, and the overall picture for Enbridge is a delivery of its commitments and an expected growth rate for the Dominion assets of 8% CAGR.

While we do not expect the same dividend growth rate as we've seen historically, we do expect dividend safety from this investment.

Enbridge IR

The company is positioned to see significant growth not only in legacy gas/liquids and utilities, but also in renewables in Europe. Several of the company's assets are already in operation, and several are under construction.

The company expects significant growth from its renewable portfolio in 2024E.

Enbridge is already acquiring more as we speak, with 7 operating landfill-to-RNG facilities across NA, which enhance the company's lower carbon characteristics and generate immediately accretive DCF (discounted cash flow).

The current headwinds for Enbridge are no secret - because they're essentially the headwinds that most other companies here see.

It's financing costs, it's tool revisions and similar headwinds - but so far, the company is maintaining guidance despite these increased costs and lower mainline tolls.

Current estimates are as follows.

Enbridge IR

And this estimate, at this price, is good enough.

To be clear with you, if the company was $5/share more expensive, we would still be investing in the preferential stocks instead - but as we're down to sub-$35/share levels, and even sub-$32/share when we bought the first stake, the common shares are now undeniably attractive.

If you want to play your cards even closer to your chest, you could sell put options during a down day, which could lock in strikes of closer or even sub-$30/share at not-uninteresting annualized RoR.

But, we're locking in steady yields and what we view as attractive returns here.

The company is at the lower end of its leverage target , at the conservative midpoint of payout, and is moving to low-risk growth strategies, such as utilities. Every single aspect of this company seems to move in one direction - safety and stability.

I applaud this.

From a business model perspective, Enbridge is one of the better businesses in the sector in terms of gross and operating as well as free cash flow ("FCF") margins.

It has a solid record of profitability, and its yield is one of the better ones in the entire sector. By the better ones, we mean in the 60-70th percentile in the sector.

While the company is no longer as cheap as it was during the sub-$32/share, as we were writing this article, it's still a very solid and not-expensive business.

Not given the stability that the company's business model offers.

Enbridge Business Model (GuruFocus)

Several fellow analysts apparently have been buying this stock "on the way down."

We aren't one of them.

Our target for Enbridge, like it was for any energy player, was a cheap one.

We have been buying the preferential stocks for some time, locking in high yields and a very nice reset when those yields reset in a few years (provided they don't appreciate, then we'll sell). However, now the time has come to take advantage of a very undervalued Enbridge as the company dropped below $35/share. The further below $35/share, the better.

{kind=link}

Let's value Enbridge and see what the upside is at this excellent price.

An income investment with a good upside

One of the main reasons we invest in Enbridge is for the attractive income.

We've locked in a yield of almost 8% on the common shares, and that is absolutely superb.

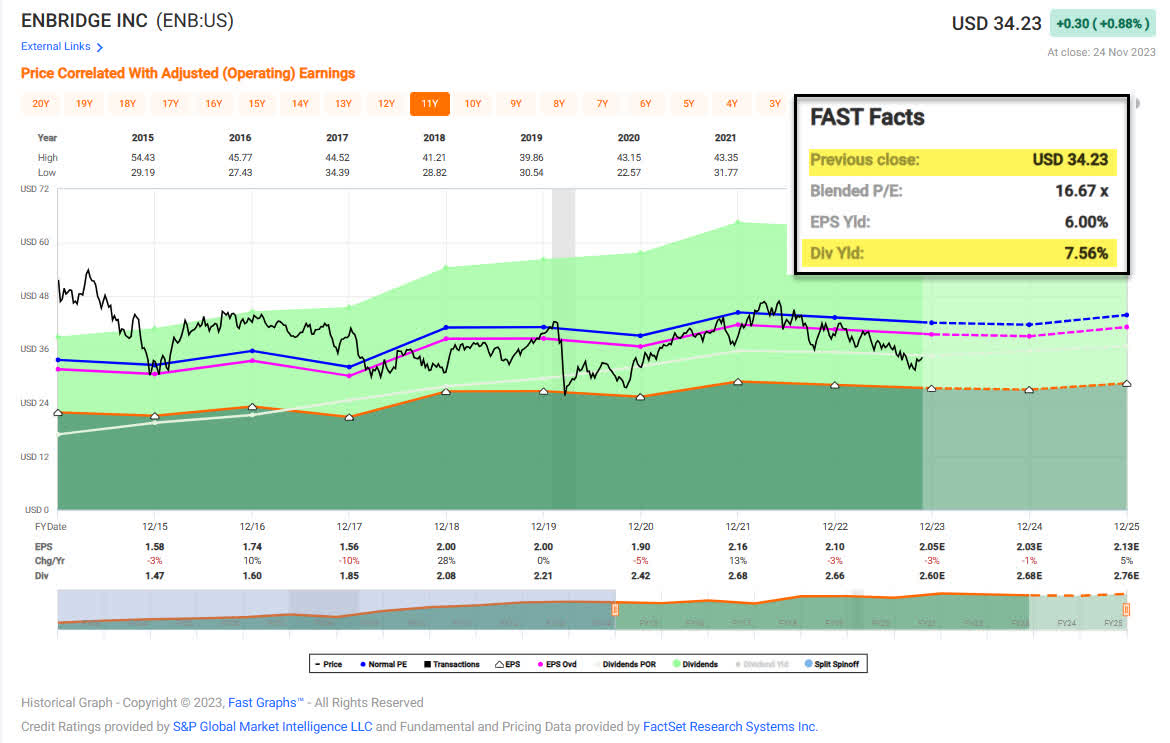

As we're writing this article, Enbridge is a BBB+ rated stock with a well-covered 7.6%+ yield trading at a P/OCF/FFO of 7.7x.

That's compared to a typical historical multiple of around 9-10x, which still is discounted, meaning the company is materially undervalued here, as we see it.

FAST Graphs

Growth is the reason the company is being valued like this.

Enbridge is expected to grow, just not much - and in this year, OCF is expected to decline 3.5%, and another 4% next year before recovering as some of the company's new assets and strategies start bearing fruit (+8% in 2025).

FAST Graphs

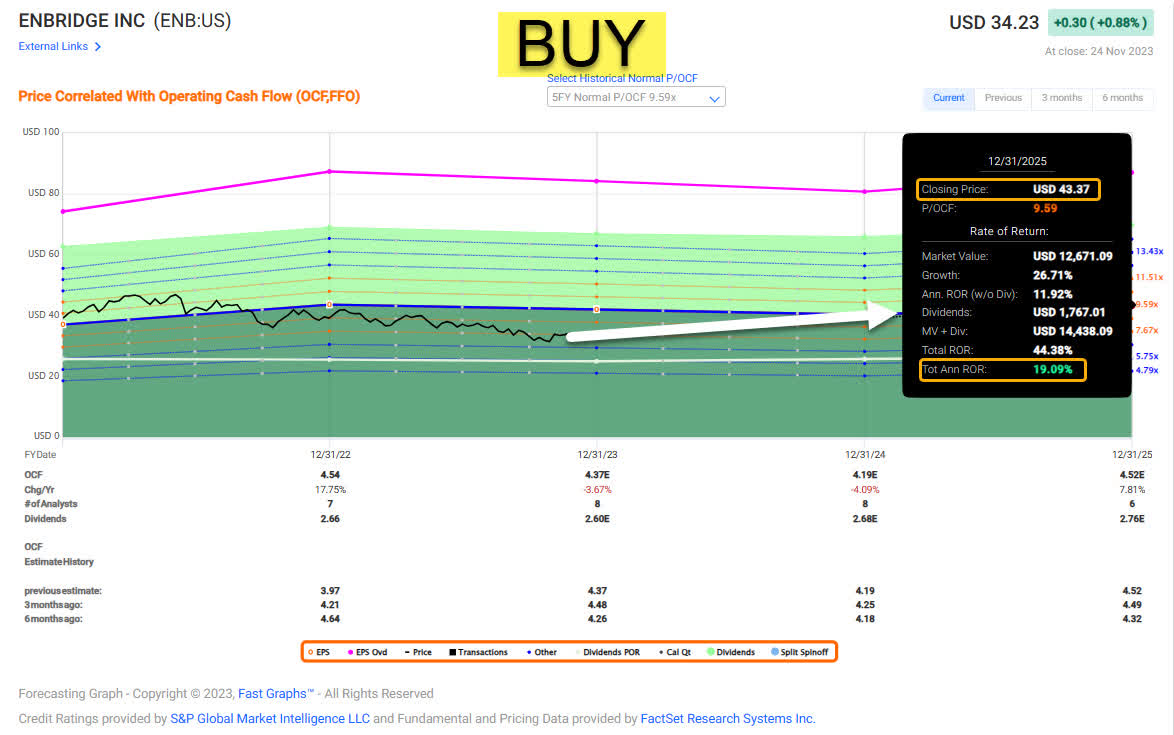

What can be said for the historical part of this thesis is the following.

Any time in the last 10+ years the company has traded at sub-8x P/OCF or FFO, this company has been a superb investment with a reversal potential of no less than triple digits to the upcycle target of around $45-$50/share.

At most, this company has reached those levels, before going back - and we don't see any reason why this time around should be any different, even if the rate environment might make the "top" somewhat lower.

We would look at Enbridge with dubious eyes starting at $45/share or above, and we would sell at $48-$50, depending on market opportunities.

But as long as the company doesn't go over $42, we'd consider our yield here well worth it under a wide range of FX scenarios, and the company at a rate of fundamental safety where the sheer income you get here makes the risk/reward worth it.

{kind=link}

You can choose the TSX or the NYSE ticker here.

For leverage/broker reasons, we go for the NYSE as opposed to the native ticker here.

In terms of other analysts , they consider Enbridge to most definitely be a "BUY" here, with a range starting at $33/share and going up to $60/share, with an average PT of $52 - that's for the Canadian, and those amounts are in Canadian dollars, but an overall upside of about 10% here.

We would agree with that upside.

If the company were to go up to around $37-$38/share, we'd probably look at other investments again, but as long as it skirts around this $35/share level, the company is a superb investment here.

The upside that this company offers here is even on only a 9.6x P/FFO, almost 20% per year, and this is based on essentially 1-2% growth.

With this being conservative, and what we consider very likely based on the current macro and where we're going the next 2-5 years, we say "BUY" here.

Thesis

- Enbridge is a class-leading investment in the energy sector, with a solid overall upside at the right price. The right price, as we see it, is below $35/share to really ensure that upside here. And as we're writing this article, the company is trading at this, or below this level.

- We believe Enbridge represents one of the safest income investments in the entire NA energy sector, based on how the company has been developing its portfolio for the past decade. However, given the slew of investment options including prefs, you want to be sure to pick the "right" avenue to enter this investment.

- At under $35/share, we believe the company represents a great value and an upside of 15% to 20% per year. Due to this, we say "BUY" here.

Remember, we're all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, we harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, we buy more as time allows.

- We reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

One More Sidenote:

Enbridge is a Canadian company.

In taxable brokerage accounts, there's a 15% Canadian withholding tax for US-based investors. Fortunately, owning the stock in retirement accounts can shield investors from the withholding tax (i.e., tax-free IRA, 401K, Roth IRA, etc.).

For further details see:

Enbridge: We're Backing Up The Sleigh