CA - Endeavour Mining: A Much Stronger H2 Ahead

2023-05-18 15:42:24 ET

Summary

- Endeavour Mining released its Q1 results earlier this month, reporting quarterly production of ~300,800 ounces of gold, a 13% decline from the year-ago period.

- The company's lower sales volumes combined with its revenue protection program unfortunately resulted in lower revenue and cash flow in the period, with revenue down 14% year-over-year.

- However, Q1 was expected to be a soft quarter and despite the impact of higher sustaining capital/lower sales, Endeavour still reported some of the lowest costs sector-wide.

- Given Endeavour's solid organic growth profile and industry-leading returns to shareholders (dividends/buybacks), I continue to see the stock as a top-5 gold producer and an attractive buy-the-dip candidate.

We're over halfway through the Q1 Earnings Season for the Gold Miners Index ( GDX ) and one of the first companies to report its results was Endeavour Mining (EDVMF). Overall, it was a much weaker quarter year-over-year with the impact of higher fuel/consumables prices and lower sales volumes impacting unit costs and production down 13% year-over-year with lower contributions from key assets. However, a soft Q1 was expected with production guided to be back-end weighted, and with the benefit of lower fuel prices, the company should have no issue delivering into its cost guidance of $940/oz to $995/oz for FY2023, maintaining its spot as one of the sector's highest-margin producers. Let's take a look at the Q1 results below:

Q1 Production & Sales

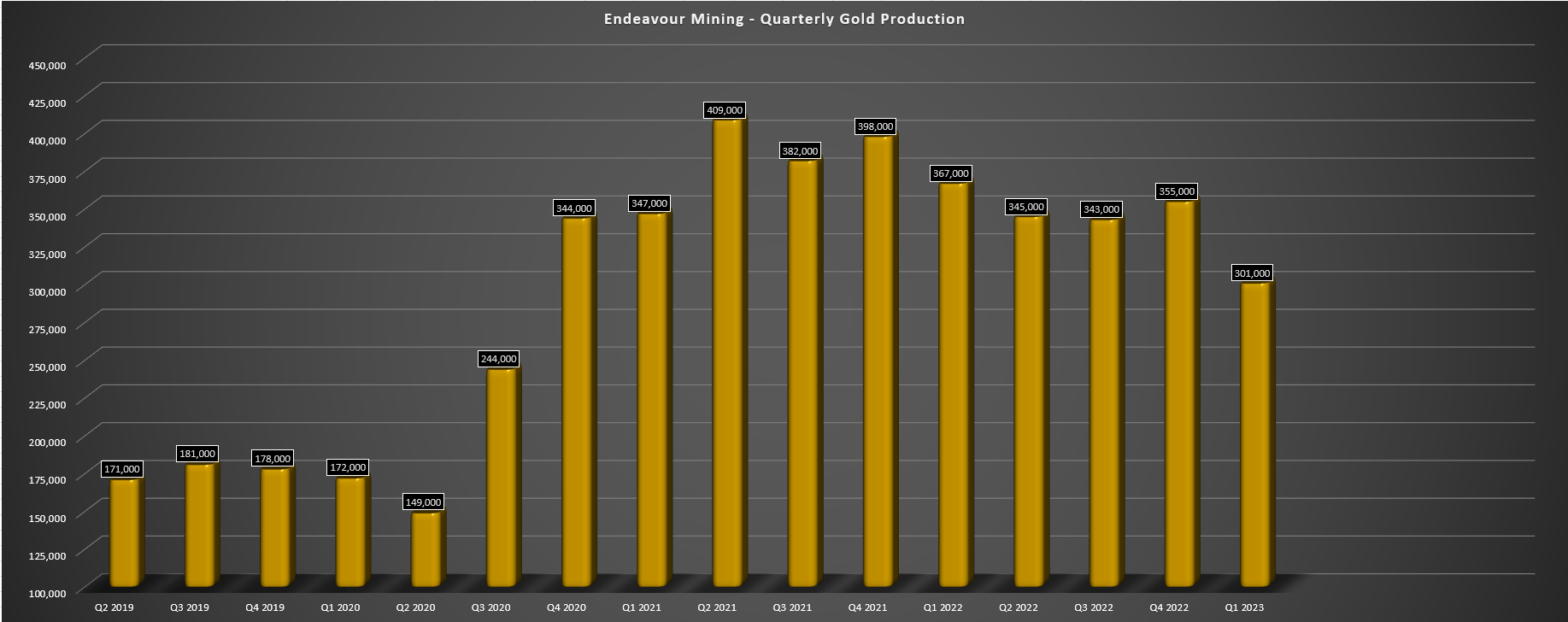

Endeavour Mining released its Q1 results earlier this month, reporting quarterly production of ~300,800 ounces of gold, translating to a 13% decline from the year-ago period (Q1 2022: ~357,100 ounces of gold production). And while this meaningful drop-off from Q4 levels and lower production year-over-year might alarm some investors with it tracking at just ~21.9% of annual guidance, it's important to note that Q1 has consistently been a weaker quarter for Endeavour, and Q1 2023 was no different, with the company focused on accelerating stripping activities during the dry season in the first half of the year.

Endeavour Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

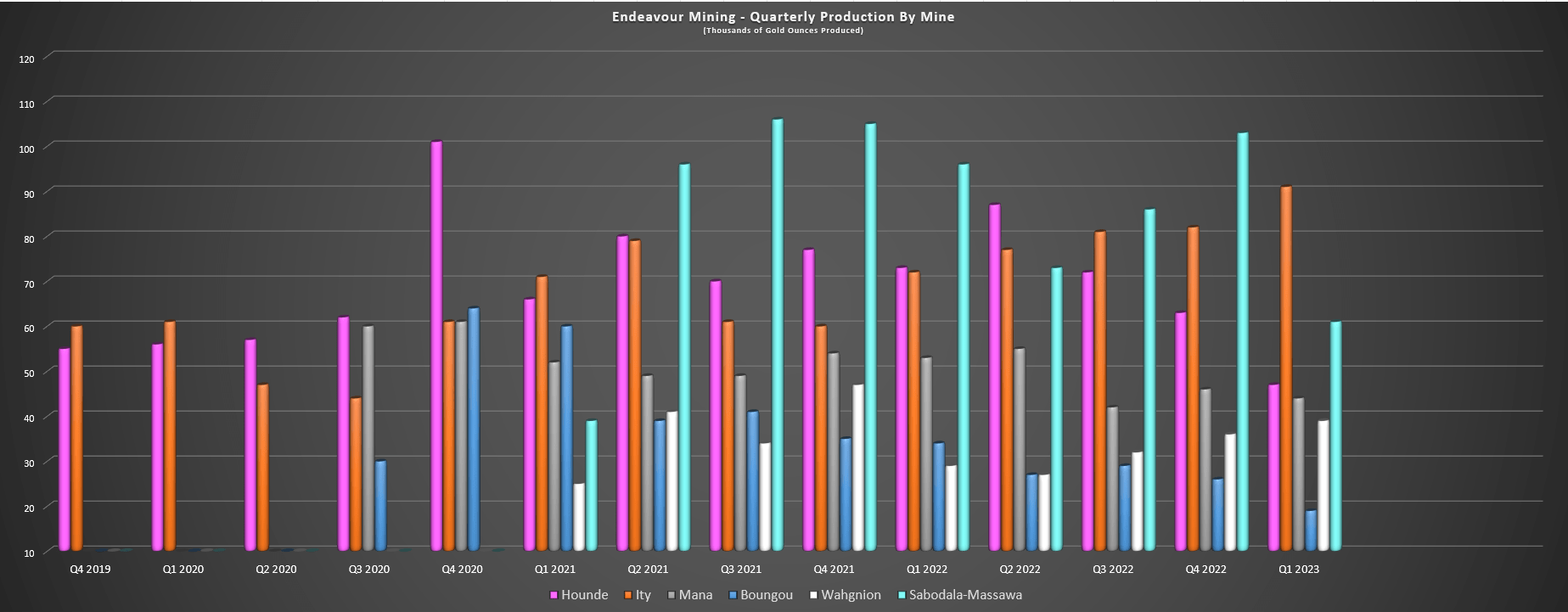

Digging into the quarterly results a little closer, the primary reason for the lower production was the company's largest Sabodala-Massawa Mine, which produced just ~61,500 ounces in Q1 at $787/oz vs. ~96,300 ounces at $578/oz in the year-ago period. Lower production in Q1 2023 was related to the mining sequence, with lower grades processed as work is ongoing to develop the Massawa North Satellite Pit. That said, output will improve meaningfully as the year progresses, with higher-grade ore coming from the Delay Pit in H2, and higher grades from Sofia North/Massawa CZ. During the quarter 1.12 million tonnes were processed at 2.04 grams per tonne of gold, down from 1.15 million tonnes at 3.16 grams per tonne of gold in Q1 2022.

Sabodala Massawa Operations (Company Presentation)

{kind=link}

Moving to the company's Ity Mine, it had a phenomenal quarter, producing ~91,300 ounces of gold vs. ~73,100 ounces in the year-ago period. Increased production was related to higher throughput and recoveries offset by marginally lower grades, with higher mill availability and recoveries from an increased proportion of softer oxide ore processed in the period, and the benefit of the commissioning of the pre-leach tank. Given the significant increase in sales volumes, Ity's all-in sustaining costs [AISC] came in at an industry-leading $732/oz (Q1 2022: $728/oz) despite inflationary pressures experienced since last year and despite slightly higher sustaining capital.

As for its to Burkina Faso operations, Hounde saw significantly lower production (~46,600 ounces vs. ~73,100 ounces) because of the reliance on lower-grade ore from Kari West with pre-stripping underway at the Stage 3 pushback at Kari Pump, slightly offset by higher throughput. All-in sustaining costs rose from $1,154/oz vs. $771/oz because of the lower sales volumes and higher sustaining capital. Meanwhile, at Boungou, production came in at ~19,000 ounces (Q1 2022: ~33,800 ounces) at all-in sustaining costs of $1,252/oz (Q1 2022: $901/oz), with lower throughput, lower grades, and lower recovery rates. Endeavour noted tonnes mined were affected by supply chain delays that impacted the ability to get fuel and consumables to the site.

Endeavour Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

Finally, at Mana, production came in at ~44,100 ounces at $1,130/oz AISC vs. ~52,600 ounces at AISC of $1,000/oz. Lower Q1 gold output was related to Endeavour focusing on underground mine development at Wona where the company is constructing a third portal, with stope production deferred until later in the year. Meanwhile, throughput was marginally lower as well, with ~614,000 tonnes processed. And while Wahgnion picked up some of the slack from other mines in the quarter with a better year-over-year performance (higher grades and tonnes processed), this is one of Endeavour's smaller mines so it made little difference to the total ounce figure despite the year-over-year increase of ~7,300 ounces.

As for the company's gold sales and operating cash flow, Endeavour sold ~308,900 ounces in the period at $1,886/oz, comparing unfavorably to ~359,100 ounces sold in the year-ago period at $1,891/oz. The lower average realized price was impacted by its revenue protection program during its higher-capex growth period, with revenue declining from $688.9 million to $590.6 million. Meanwhile, operating cash flow came in at $242.2 million before working capital changes ($205.6 million when adjusted for working capital), down from $367.7 million before working capital changes in Q1 2022. This was due to lower sales volumes and margins, higher taxes, and increased exploration costs.

Endeavour Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

Costs & Margins

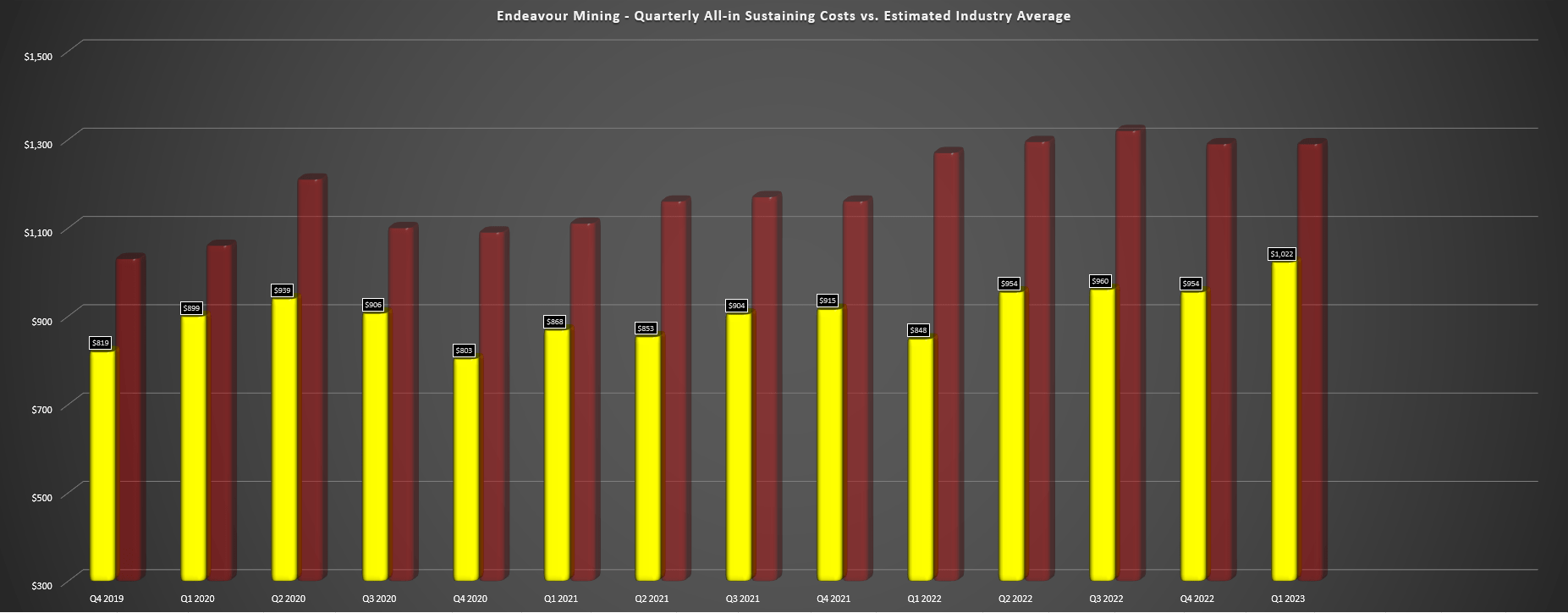

Moving over to costs and margins, Endeavour reported cash costs of $871/oz in Q1 and all-in sustaining costs of $1,022/oz. These compared unfavorably to $745/oz and $848/oz in the year-ago period, with all-in sustaining costs on a year-over-year basis impacted by higher fuel and consumables costs, an 8% increase in sustaining capital, and the impact of much lower sales volumes. That said, costs were only slightly above the FY2023 guidance range ($940/oz - $995/oz) in the worst quarter of the year, and with fuel prices cooling off a little, I am confident that Endeavour can deliver within its guidance range for the full year. Plus, as shown below, even with the increase in costs, its costs remain below the industry average.

Endeavour Mining - Quarterly AISC vs. Estimated Industry Average AISC (Company Filings, Author's Chart)

{kind=link}

As for margins, Endeavour's AISC margins dipped to $864/oz vs. $1,063/oz in Q1 2022, with the impact of a lower average realized gold price and higher costs. That said, the company is on track to report AISC margins of $935/oz for the year assuming all-in sustaining costs of $985/oz and an average realized gold price of $1,920/oz, which would be an 8% improvement from $864/oz in FY2022. And despite the limited free cash flow generation in Q1 2023 due to lower production and the ~$330 million convertible notes reimbursed in cash, Endeavour's balance sheet remains solid with $800+ million in cash and just $50 million in net debt at the end of the quarter.

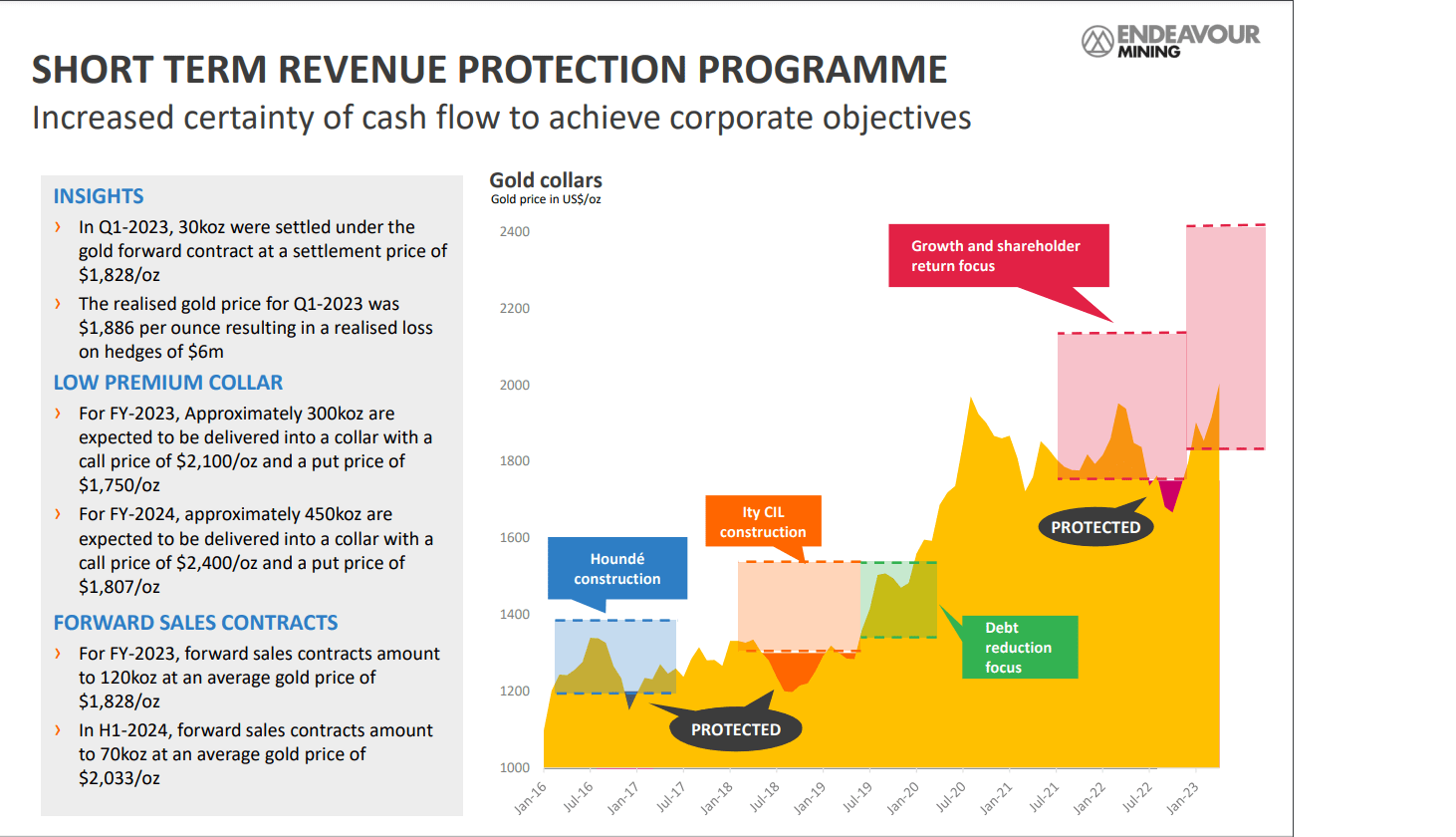

Endeavour - Short-Term Revenue Protection Program (Company Website)

{kind=link}

Recent Developments

Finally, moving over to recent developments, Endeavour repurchased ~71,000 shares after quarter-end at an average price of US$25.91, and continues to have significant availability in its buyback program to opportunistically reduce its share count and be active in the market. As for operations, the company noted that Wahgnion and Boungou are becoming non-core assets, which may worry some investors regarding Endeavour's production taking another step down post-2024 if it looks to divest one or both assets.

However, it's important to note that the Lafigue Project and the Sabodala-Massawa Expansion are on track and schedule (first gold production from BIOX plant due in Q2 2024) and would offset lost production from these two assets at much higher margins. Given that the market appreciates quality ounces over quantity, I don't see any reason to be worried about the possibility of divesting these assets at some point, especially when higher-margin ounces will replace them and the jurisdictional profile would get a minor upgrade with Burkina Faso production seeing a higher discount because of security concerns than some other African jurisdictions.

Endeavour Mining Q1 Conference Call (Seeking Alpha Transcripts)

{kind=link}

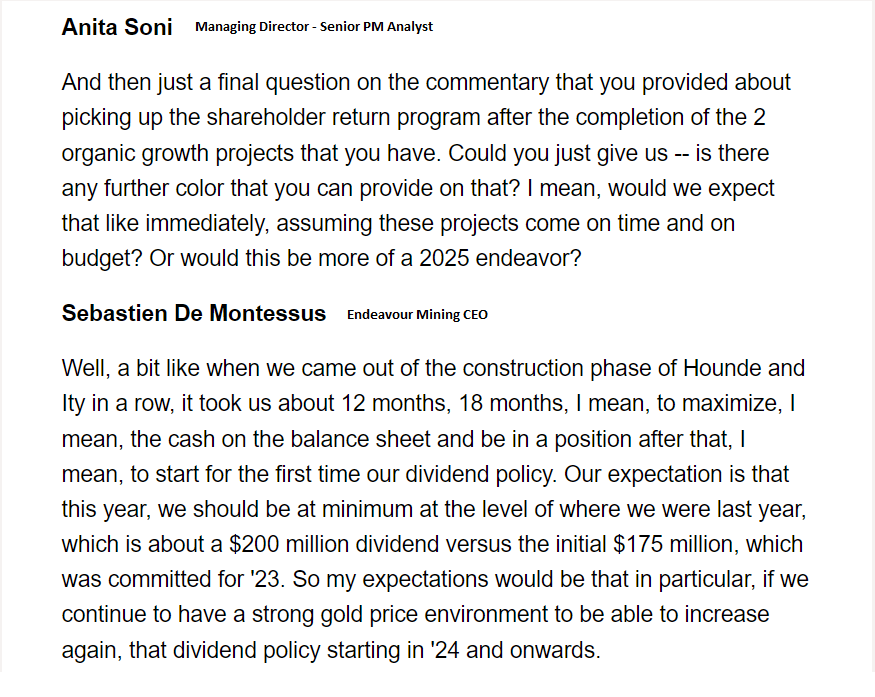

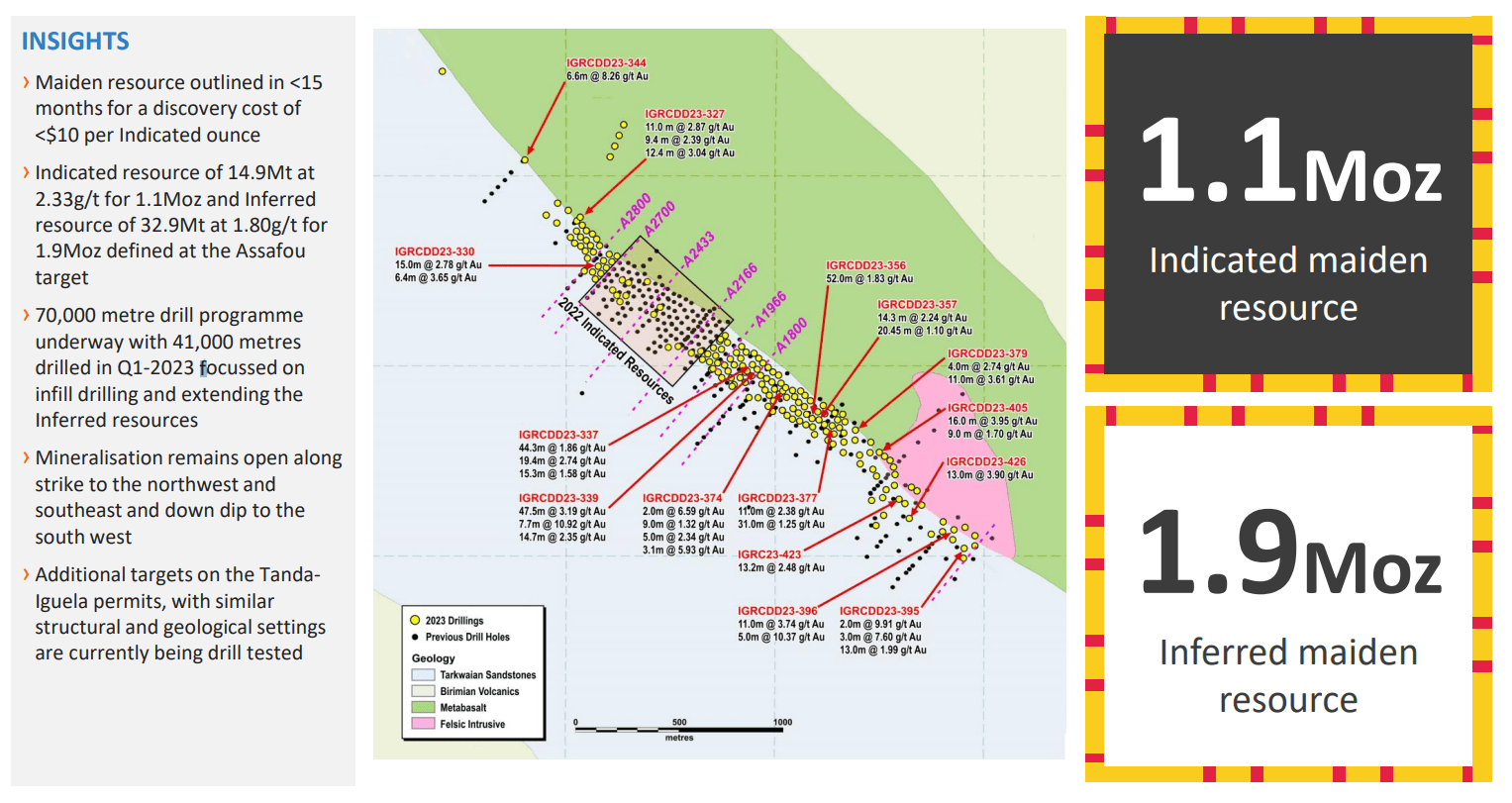

Plus, as discussed by the company, investors can likely look forward to increased shareholder returns once Endeavour is out of this capital-intensive phase with two growth projects ongoing, and any proceeds from the sale of one or both assets could go towards future growth, like Tanda-Iguela. In fact, Endeavour appears to be very optimistic about this asset, with the company stating that it has the potential to be a Tier 1 asset in the region based on ongoing drill results. Based on Endeavour's definition, this would imply ~400,000 ounce per annum potential, and an open-pit mine at these grades and scale would make it a very high-margin operation.

Tanda-Iguela - 5 Million Ounce Resource Potential (Company Website)

{kind=link}

Obviously, its early days and production isn't likely until H2-2027, but if Endeavour ends up being correct, this would certainly improve the investment thesis with the potential for another Sabodala-Massawa like operation in the portfolio from a profitability standpoint (380,000+ ounces per annum at sub $850/oz AISC). Plus, with a cost of discovery of just $10/oz on indicated to date, the return on capital here is incredible vs. some companies like Kinross ( KGC ) that are paying ~$170/oz for ounces that haven't even made it into a NI 43-101 resource statement at the time of acquisition (Great Bear), even assuming it proves up 8.5 million M&I ounces in Red Lake.

Valuation

Based on ~247 million shares and a share price of US$25.00, Endeavour Mining trades at a market cap of $6.18 billion and an enterprise value of US$6.23 billion. This remains one of the cheapest valuations sector-wide for 1.0+ million-ounce miners, and it has a path to ~1.60 million ounces of gold production in 2025 at industry-leading costs once the Sabodala-Massawa Expansion and Lafigue Project are online. Looking at Endeavour from a cash flow standpoint, it also trades at one of the most attractive valuations sector-wide despite its strong rally, trading at just ~5.4x cash flow, a very attractive valuation for a miner that continues to focus on quality ounces over quantity and has grown in a disciplined manner.

Using what I believe to be a conservative multiple of 7.50x cash flow, which balances its capital discipline and strong margins with its non-Tier 1 jurisdictional profile, I see a fair value for Endeavour Mining of US$34.50 per share, pointing to a 38% upside from current levels. On a total return basis and when including dividends, this translates to closer to a 40% return with the company on track to return upwards of $300 million to shareholders this year from dividends and buybacks. Hence, I continue to see the stock as attractively valued despite its outperformance.

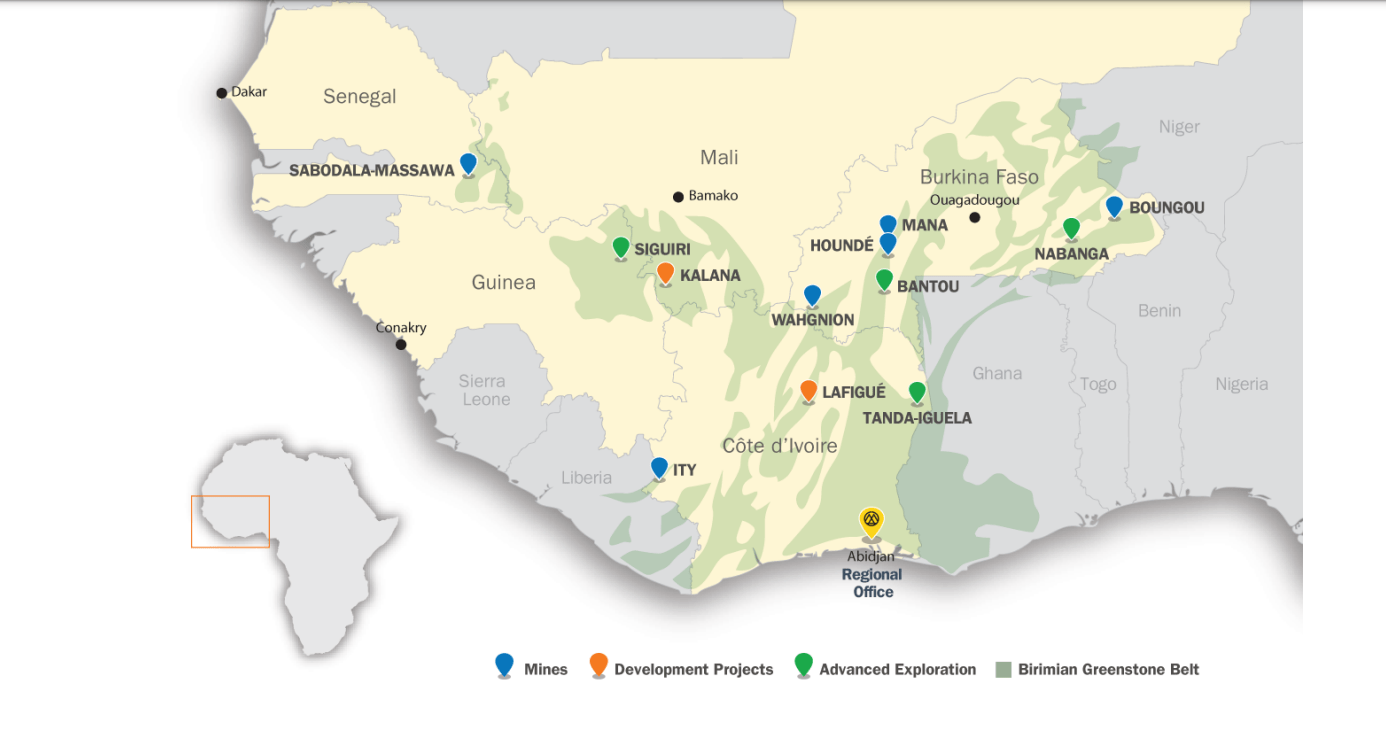

Endeavour Mining Portfolio (Company Presentation)

{kind=link}

All that being said, I prefer to only start new positions if I have a minimum 35% discount to fair value for non-Tier 1 jurisdiction producers to ensure I'm baking in an adequate margin of safety. And after applying this discount to Endeavour Mining's estimated fair value of US$34.50, the stock's ideal buy zone comes in below US$22.45. This doesn't mean that the stock has to drop to these levels, and its outperformance has certainly been justified given its strong execution, but while I am long the stock from US$18.40, I have no plans to add to my position here unless we see a deeper pullback.

Summary

Endeavour Mining had a softer Q1 from a headline standpoint, with production down sharply and costs higher, with lower production year-over-year at most of its largest contributors (Sabodala-Massawa, Hounde, Mana). However, this was expected given the back-end weighted guidance and while costs were up sharply, cash costs and AISC of $871/oz and $1,022/oz, respectively, remain well below the industry average. So, with a stronger H2 ahead, meaningful growth on deck and continued exploration success at industry-leading costs, I see Endeavour as one of the best-run producers sector-wide, and I would use any pullbacks below US$21.60 as buying opportunities.

For further details see:

Endeavour Mining: A Much Stronger H2 Ahead