CA - Endeavour Mining: Solid Reserve Replacement Despite Rising Cost Environment

2023-06-27 15:14:38 ET

Summary

- Endeavour Mining's gold reserves declined by 6% in FY2022, but the company maintains a strong reserve base with multiple long-life core assets.

- Plus, the company has focused on quality ounces over quantity, divesting lower-margin assets and upgrading its portfolio, leading to headwinds to reserve growth due to consistent divestments.

- I continue to see Endeavour as a top-10 gold producer and a solid investment opportunity if bought on weakness, with a very reasonable valuation at less than 9x forward EV/FCF.

Investors in the precious metals sector have had to endure a rollercoaster ride in 2023, with the index starting the year off with a double-digit gain only to find itself back near flat year-to-date and massively underperforming the major market averages. We can attribute the poor performance for most miners to declining margins year-over-year and flat production/sales and what have been underwhelming year-end FY2022 Reserve/Resource statements on balance, with less than one-third of large producers successfully replacing reserves. And given the steadily rising share counts for many producers, this means that investors hoping for leverage to metals prices by owning producers have been getting the opposite, given that share counts have been climbing at a quicker pace than gold reserves. The result? An investor in most of these names needs to buy more shares to get the same amount of gold production and gold reserves as they did several years ago.

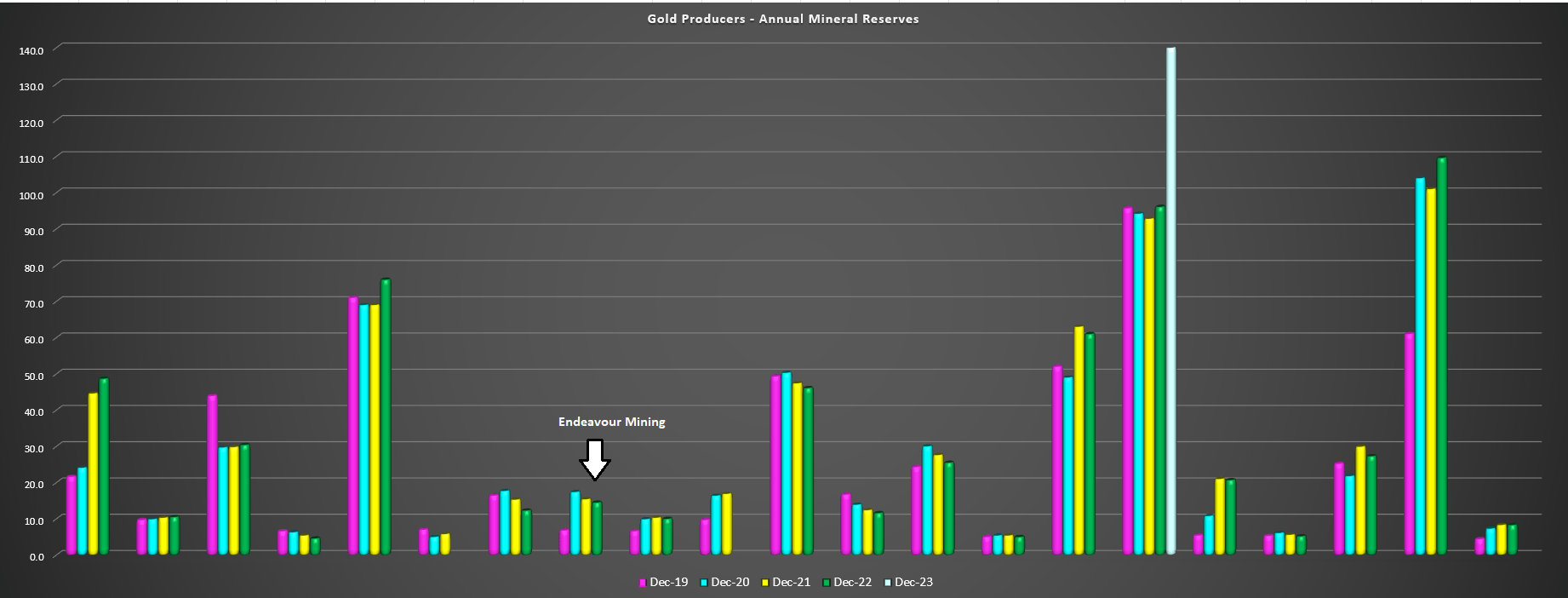

Large Gold Producers - Annual Gold Reserves (Company Filings, Author's Chart)

{kind=link}

Unfortunately, Endeavour Mining ( EDVMF ) was one company that struggled to replace reserves in 2022, with reserve growth at two key assets (Hounde and Ity) being offset by moderate reserve declines at Sabodala-Massawa and Mana, and large percentage declines at what could become non-core assets, Boungou and Wahgnion. That said, the company's reserve base continues to be well above that of other large producers like Evolution Mining ( CAHPF ) and B2Gold ( BTG ) and only slightly behind that of Northern Star ( NESRF ), and much of its reserve declines over the years have been tied to divestments (Agbaou, Karma, Nzema, and Tabakoto), while M&A has added high-margin and long-life assets to the portfolio like Sabodala-Massawa. Hence, if the company was focused on an absolute production ounce figure and extending lower-quality assets like some miners, its reserves would be higher. Let's look at the FY2022 Reserve/Resource statement below.

{kind=link}

All figures are in United States Dollars unless otherwise noted.

2022 Reserves

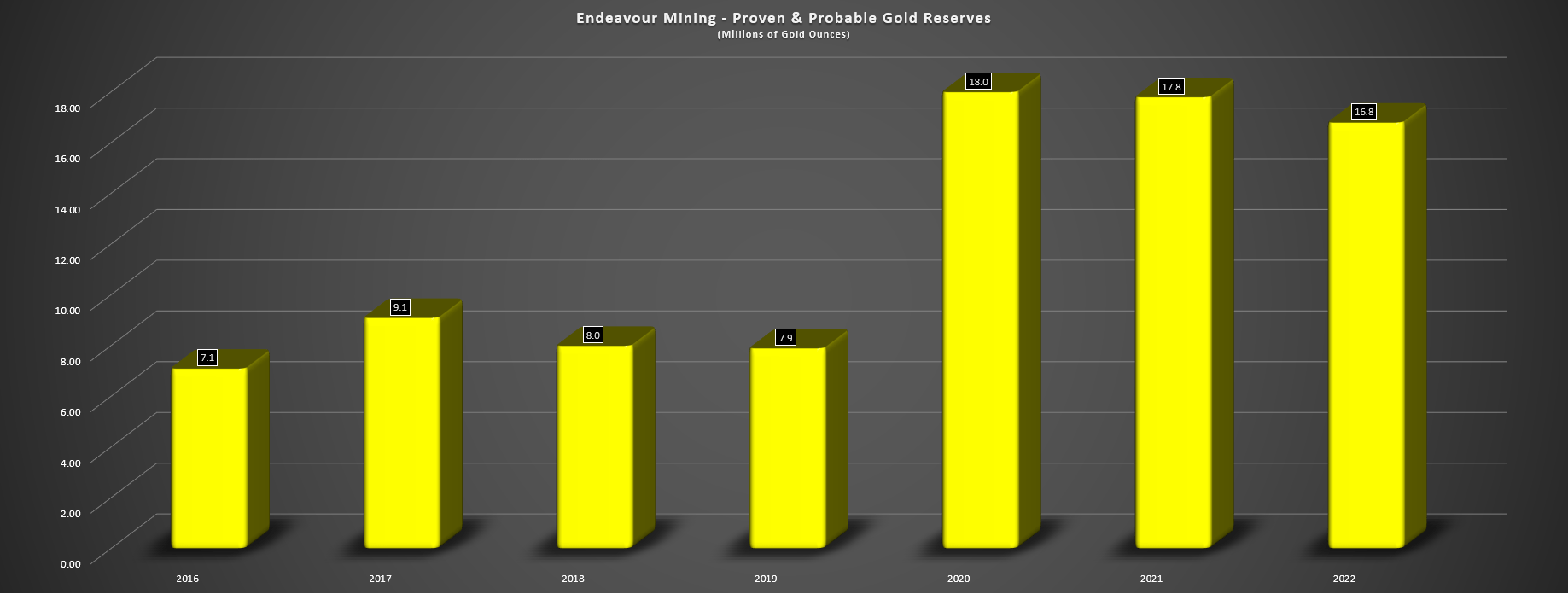

Endeavour Mining released its FY2022 Reserve/Resource statement earlier this year, reporting proven and probable gold reserves of ~16.8 million ounces of gold, a 6% decline from ~17.8 million ounces of gold in the year-ago period. The moderate decline in gold reserves for a second consecutive year was related to the divestment of its Karma Mine, higher input costs, and an updated geological interpretation at its smaller Boungou Mine, with the reserve declines at Boungou, Mana, Sabodala-Massawa, and Wahgnion offsetting solid reserve growth at its legacy Hounde and Ity mines which added ~0.30 million ounces combined. This ability to continue to grow reserves at Hounde and Ity is quite impressive, with the combined reserve base of ~5.8 million ounces at these two mines being nearly 40% higher than the combined ~4.2 million ounces in 2016 despite over 2.0 million ounces of depletion in the period.

Endeavour Mining - Proven & Probable Gold Reserves (Company Filings, Author's Chart)

{kind=link}

Given that these are two of Endeavour's lowest-cost assets with sub $920/oz FY2023 all-in sustaining costs (blended basis using guidance midpoint), it's encouraging to see the continued reserve growth here with their mine lives extending into the 2030s. Endeavour noted that reserve growth at Hounde was related to the addition of the Mambo and Kari South deposits and a change in block size at Kari Centre to better align with the mining block size. Meanwhile, at Ity, reserve growth from ~2.98 million ounces at 1.47 grams per tonne of gold to ~3.02 million ounces at ~1.62 grams per tonne of gold was attributed to including new discoveries and the re-optimization of pit shell design, plus maiden reserves at Verse Est, Bakatouo Northwest, and Yopleau. And as for 2023, the company plans to test underground resource potential at Vindaloo Deeps + Kari West plus look at extending Vindaloo Southeast along strike (Hounde), while it will spend $14.0 million testing mineralization around existing deposits at Ity, and test recent regional discoveries like Ggampleu.

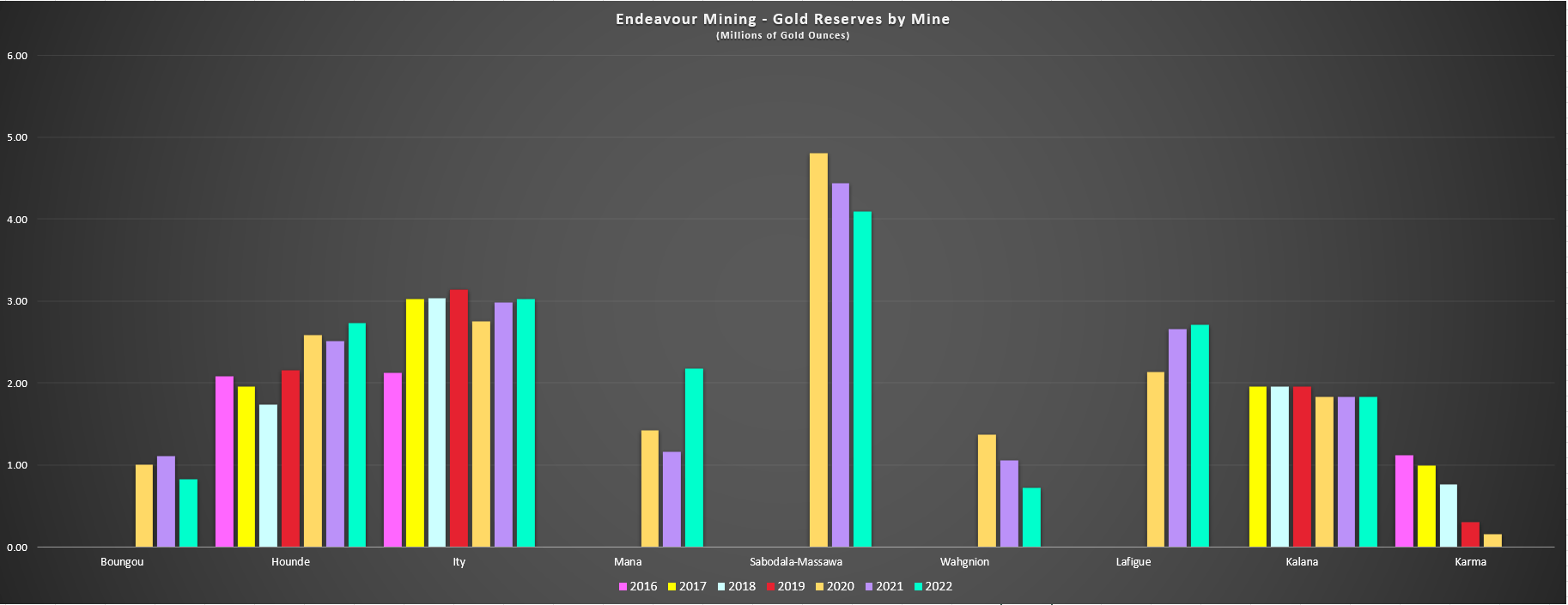

Endeavour Mining - Gold Reserves by Mine (Company Filings, Author's Chart)

{kind=link}

Moving over to assets where we saw declines in reserves, Boungou's reserve life declined to barely seven years based on ~833,000 ounces in gold reserves (FY2022: 1.11 million ounces), assuming a similar production rate to FY2022 levels. This was related to higher input costs that affected cut-off grades and updated geological interpretations. Elsewhere, at Wahgnion, reserves declined to ~720,000 ounces at 1.59 grams per tonne of gold, down from ~1.06 million ounces at 1.52 grams per tonne of gold previously. This was attributed to mining depletion and remodeling at the Nogbele and Fourkoura pits with more conservative dilution factors and higher cost assumptions. Lastly, at Sabodala-Massawa and Mana, reserves declined because of mining depletion and higher cut-off grades related to higher operating costs (Sabodala-Massawa), and updates to the underground mine model (changes in mining method at Wona and Siou underground).

{kind=link}

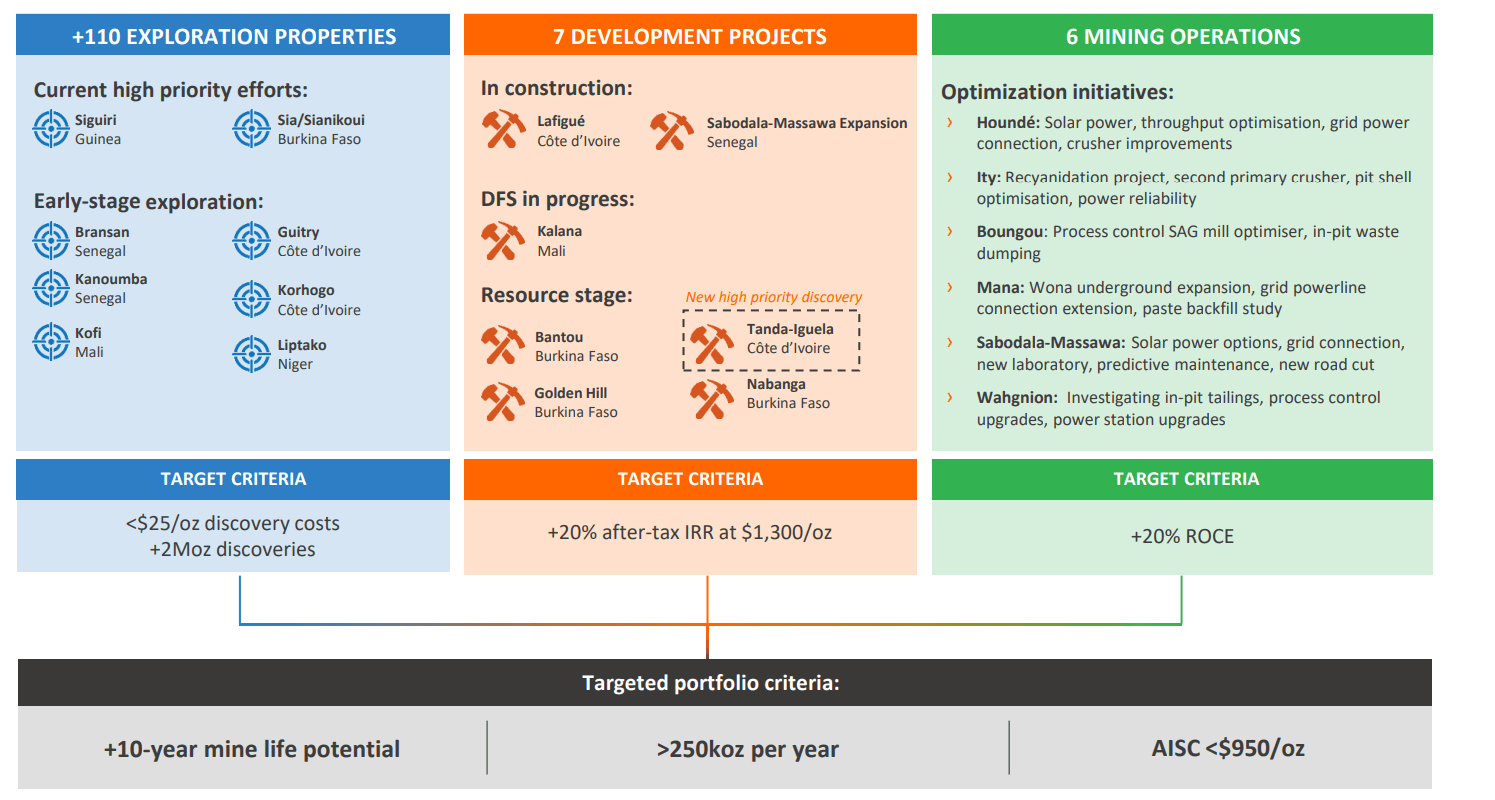

Looking at the above chart, it's clear that the declines in reserves at its smaller three assets plus a moderate decline at Sabodala-Massawa (flagship operation) overshadowed the minor gains at Lafigue and Ity, and the solid increase in reserve ounces at Hounde. That said, Endeavour is planning to spend another $22 million on greenfields exploration this year as part of a larger $70 million exploration budget, and the $21.5 million spent last year as part of the greenfields budget certainly paid off with meaningful ounces delineated Assafou (part of Tanda-Iguela Property) where the company has defined a mid-grade (2.0 gram per tonne open-pittable resource) of 3.0 million ounces at a discovery cost of less than $10/oz on indicated resources in less than 18 months. So, given that it's in the right jurisdiction to discover low-cost ounces with continued delivery on its resource targets, I am quite optimistic regarding reserve growth near-mine and on new projects like Assafou.

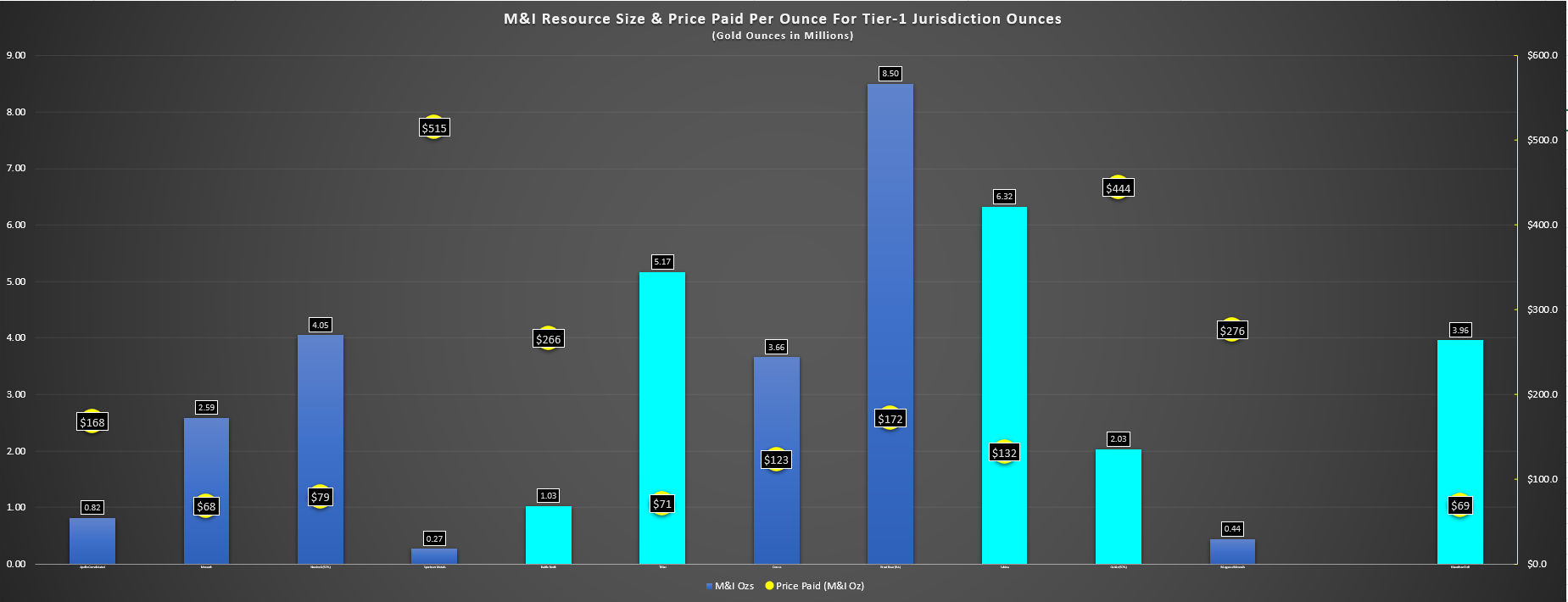

It's also worth noting that the average price paid for M&I ounces across all jurisdictions in M&A transactions (developers) has been above $90/oz, while the Tier-1 jurisdiction (Australia, Canada, and United States) average price paid has been well over $200/oz (2020 to current). So, if Endeavour can consistently delineate ounces and move them into reserves at a discovery cost of less than $40/oz, it has a path to growth in reserves per share without the need to bloat its share count to add resource/reserve ounces as we've seen from heavily dilutive transactions elsewhere in the sector like Equinox Minerals, Red Back Mining, and other major deals. And given the strong pipeline that Endeavour has with two assets (Assafou, Kalana) that could eventually become mines besides Lafigue which is in construction (2024 production), the company should be able to maintain its positive production growth per share trend as well even if it continues to divest non-core assets.

M&I Resource Size & Price Paid For Tier-1 Jurisdiction Ounces (Company Filings, Author's Chart)

{kind=link}

Reserves Per Share

As I've noted in past updates, reserve growth is important, but far more important is reserve growth per share, which isn't discussed enough. This is because reserve growth that comes at the expense of significant share dilution means that investors are getting exposure to fewer ounces per share held, which makes owning an ounce of gold more attractive, given that an investor is getting negative leverage to gold if reserves per share and or production per share is declining. Obviously, this is not ideal, since it makes no sense to own a more volatile and riskier gold producer (relative to the gold price) if it is not offering the leverage that one should get for taking on this added risk. Some examples of companies that have failed miserably to deliver reserve growth per share are Coeur Mining ( CDE ), Americas Gold and Silver ( USAS ), and McEwen Mining ( MUX ), which is why I continue to see these names as names to avoid.

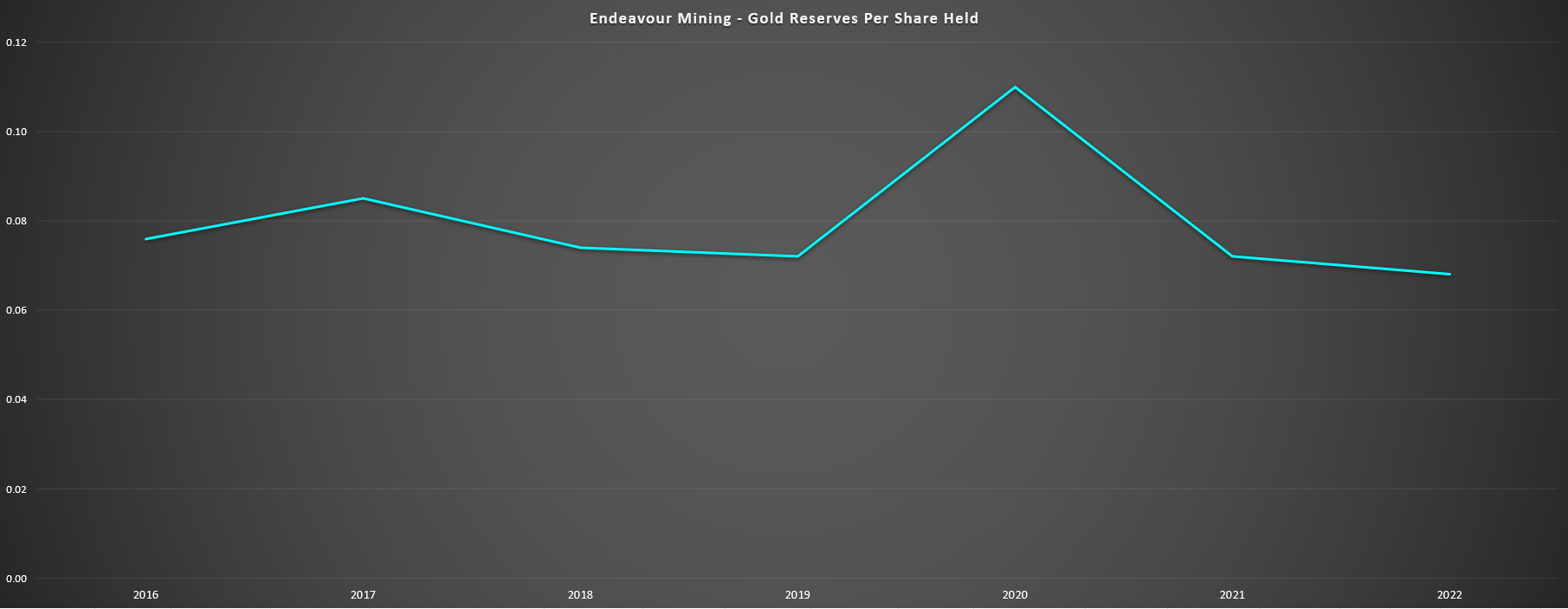

Endeavour Mining - Gold Reserves Per Share (Company Filings, Author's Chart)

{kind=link}

Looking at Endeavour Mining since 2016, we can see that it has struggled to grow reserves per share, but it has roughly held the line on gold reserves per share held, which I consider an achievement relative to the industry average. Plus, while the trend has been down slightly, this has been related to a complete transformation of Endeavour's portfolio since current CEO Sebastien de Montessus took over, with a focus on longer-life and higher-margin assets and not being shy about letting go of lower-margin and tired assets. This is clear from the below image, highlighting that it has longer-life and lower-cost assets, with four exceptional assets in Hounde, Lafigue, Sabodala-Massawa, and Ity. Therefore, while this trend in reserves per share may be down due to M&A to upgrade the portfolio with a near Tier-1 asset in Sabodala-Massawa (Teranga deal), the reserves per share trend don't tell the whole story given that the quality of reserves in 2016 was much lower.

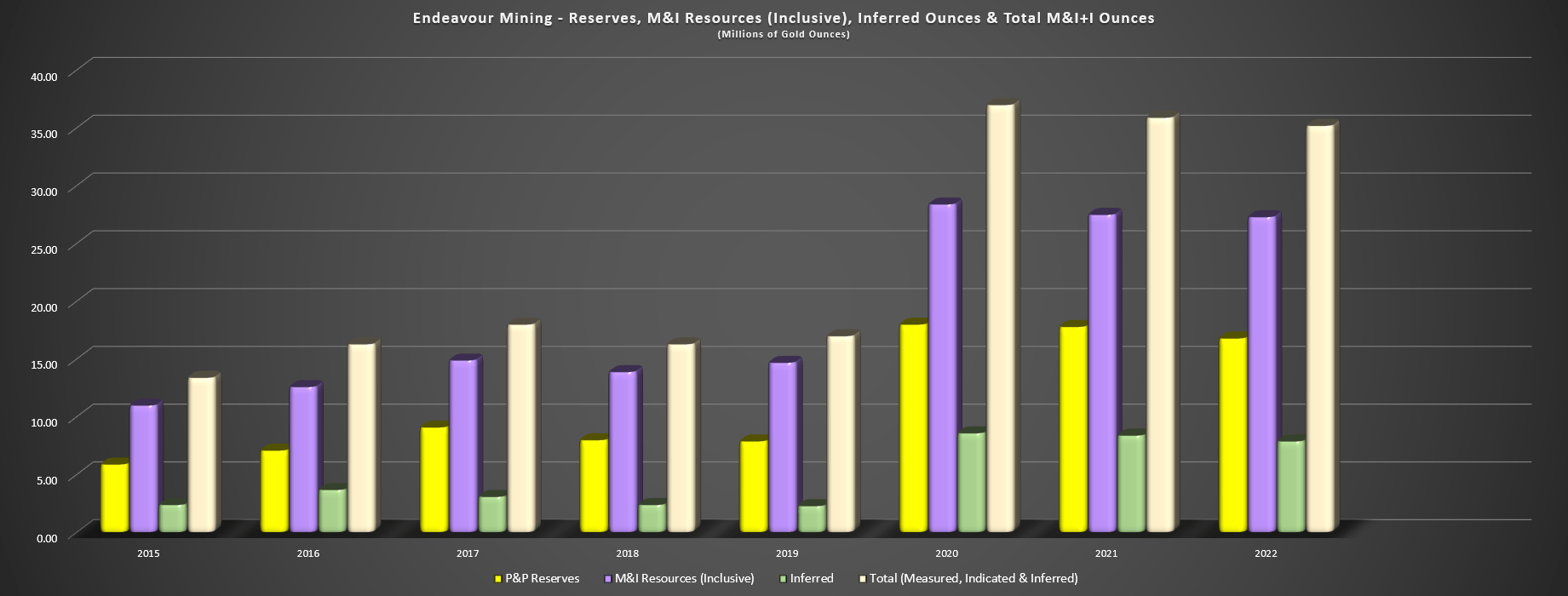

Endeavour Mining - Reserves, M&I Resources, Inferred Ounces & Total M&I Ounces (Company Filings, Author's Chart)

{kind=link}

In addition, it's also worth noting that Endeavour has a significant resource base backing up its reserves, with ~18.4 million ounces of measured, indicated, and inferred resources that are separate from its reserve base. And as highlighted earlier, the company looks to have a very special asset in Tanda-Iguela, with the company noting that this could be a Tier-1 asset based on ongoing drill results, implying ~400,000 ounce per annum potential which at this scale and with its grades (~2.0 grams per tonne of gold) would make it a very high-margin operation. To summarize, I think it's best to look past Endeavour's slight decline in reserve growth per share since 2016, and I would compare Endeavour's situation in 2016 to a General Manager of a sports team that had to transform its team with multiple deals and trades to be more competitive which obviously comes at a cost (salary cap hits or share dilution in this case), but is ultimately better for the long term.

Summary

While Endeavour Mining wasn't successful in replacing all of its mined depletion this year, the company has done an excellent job maintaining reserves per share relative to peers, with one of the better track records sector-wide. It's also worth noting that they have achieved this feat despite a strategy of being quick to divest aging and lower-margin assets, meaning that if it wasn't so focused on quality ounces over quantity with a re-vamped portfolio of much stronger assets vs. the 2016 Endeavour, it would have enjoyed reserve growth per share since 2016. And while reserves were down year-over-year, the Tanda-Iguela Property continues to be quite exciting and points to the opportunity to grow reserves further post-2025 without M&A while the company continues to reduce its share count through opportunistic buybacks, helping to maintain a leading reserve per share trend.

Given this rigid focus on quality ounces over quantity, which isn't employed by enough miners, and the company's industry-leading margins, low discovery cost per ounce, and ability to over-deliver on promises, I continue to see Endeavour Mining as a top-10 gold producer, and one of the best investment opportunities sector-wide. And with a very reasonable valuation of just ~8.8x EV/FCF using FY2024 free cash flow estimates, the stock continues to be one of the best values sector-wide, especially given its quality asset base. So, if we were to see further weakness in the stock and a dip below US$22.40, where it would trade at a 35% discount to my fair value estimate of US$34.50, I would view this as a buying opportunity.

For further details see:

Endeavour Mining: Solid Reserve Replacement Despite Rising Cost Environment