CA - Endeavour Silver: An Inferior Way To Buy The Dip

Summary

- Endeavour Silver continues to be one of the worst-performing silver miners, down ~60% from its 2021 highs and 5% year-to-date.

- This underperformance can be partially attributed to Endeavour being highly leveraged to silver due to its relatively high cost profile, meaning that its margins get pinched as silver declines.

- While this could change once the company's Terronera Project comes online, this continues to look like a Q3-2025 opportunity earliest with no financing package in place yet.

- So, with relatively low margins, short reserve lives, and no immediate improvement to margins (2+ years for Terronera to move into commercial production), I continue to see EXK as an inferior buy-the-dip candidate.

Just over two months ago, I wrote on Endeavour Silver ( EXK ), noting that while the company was tracking ahead of annual guidance, I didn't see any margin of safety in the stock at a share price of US$3.45. This was because the stock was trading at roughly 1.20x P/NAV and more than 12x forward cash flow despite being a small-scale producer with razor-thin margins in Mexico. Since then, the stock has continued its decline despite blowout Q4 results with production coming in above its already upward revised FY2022 guidance. I attribute the weak response to Endeavour's high leverage to silver prices due to its cost profile, with silver now negative year-to-date.

Fortunately, Endeavour Silver's ("Endeavour") 2023 outlook came in better than I expected, and production is set to increase yet again this year with another year of robust grades from Guanacevi. This should contribute to lower costs, benefiting from the higher sales volumes. That said, Endeavour's costs are still well above the industry average, and although it may benefit from ~650 gram per tonne silver-equivalent grades at Guanacevi, the reserve life remains short relative to other silver assets sector-wide. So, with short mine lives at both its assets, industry-lagging margins, and no path to material margin expansion until H2 2025 (Terronera), I continue to see EXK as an inferior buy-the-dip candidate.

Q4 & FY2022 Production

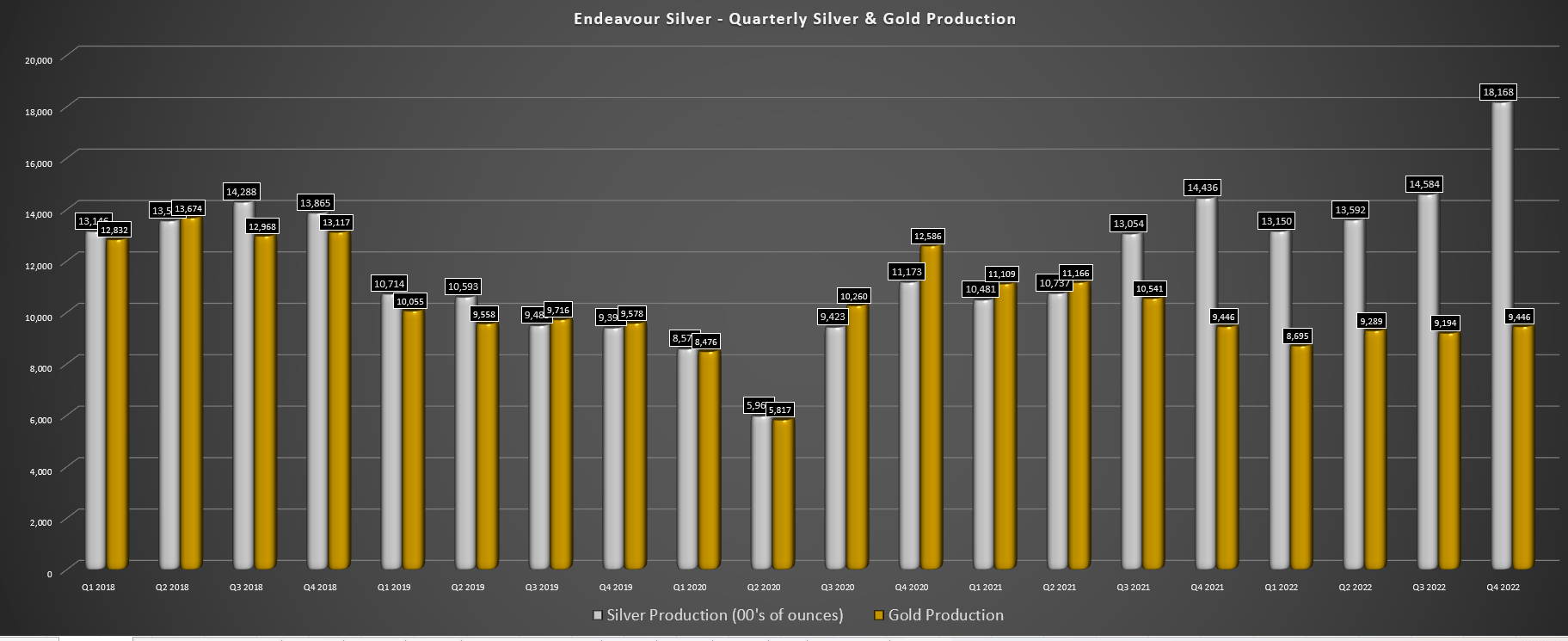

Endeavour Silver released its Q4 and FY2022 production results last month, reporting quarterly production of ~1.81 million ounces of silver and ~9,400 ounces of gold, the best quarter for silver production in years and its best quarter for gold production in 2022. These strong results were helped by another impressive quarter from Guanacevi, with silver-equivalent grades coming in at ~650 grams per tonne, and throughput up sharply year-over-year due to plant modifications and refurbishments. Guanacevi's solid performance helped offset weaker output from Bolanitos where gold grades declined from 1.83 grams per tonne in Q4 2021 to 1.72 grams per tonne in Q4 2022.

Endeavour Silver - Quarterly Silver & Gold Production (Company Filings, Author's Chart)

{kind=link}

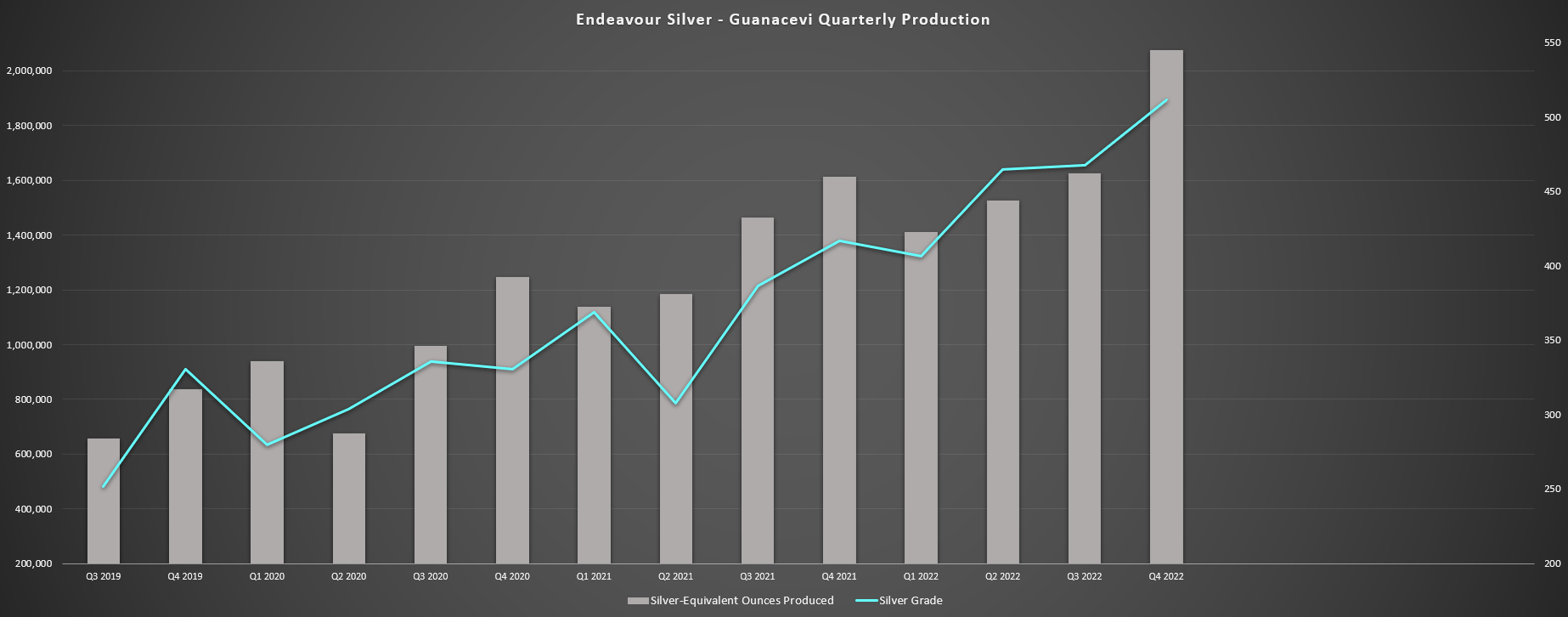

Digging into the operations a little closer, we can see that Guanacevi had a monster year and an impressive finish to 2022, producing ~1.68 million ounces of silver and ~4,900 ounces of gold in Q4, and ~5.34 million ounces of silver and ~15,700 ounces of gold for the year. This represented a significant increase from ~4.33 million ounces of silver and ~13,300 ounces of gold in FY2021, driven by much higher grades as shown in the below chart. The good news is that this should continue into 2023 despite difficult year-over-year comps. with Endeavour forecasting production of ~5.45 million ounces of silver and ~16,000 ounces of gold, translating to 7.0 million silver-equivalent ounces [SEOs] at the top end of guidance.

Endeavour Silver - Guanacevi Silver-Equivalent Production (Company Filings, Author's Chart)

{kind=link}

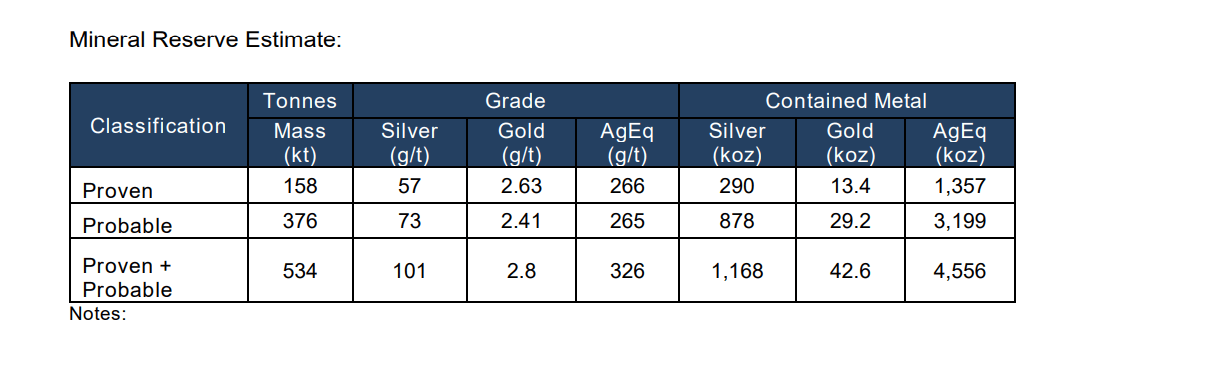

Looking at Bolanitos, this asset won't be as fortunate to maintain 2022 production levels, with output down in FY2022 due in part to declining gold grades, and silver production set to decline this year based on company guidance. The lower production is despite an expectation for slightly higher throughput (averaging 1,200 tonnes per day), with feed sourced from the Plateros La Luz, Lucero-Karina and Bolanitos-San Miguel vein systems. The bigger issue for Bolanitos, though, is that while production may be more or less stagnant year-over-year, reserves continue to dwindle, declining to just ~534,000 tonnes which is based on metals prices near spot levels ($1,735/oz and $21.80/oz).

{kind=link}

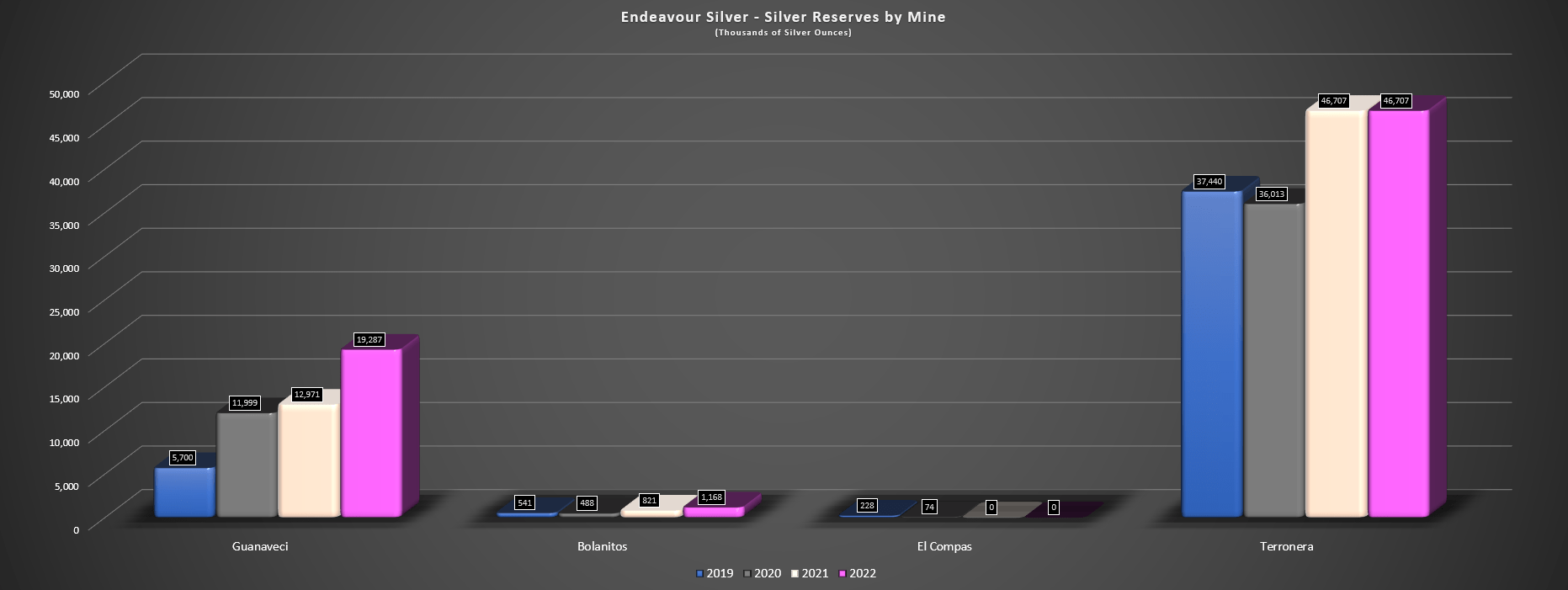

Assuming a throughput rate of 400,000 tonnes, this translates to a sub 2-year mine life for Bolanitos and there's minimal wiggle room to increase metals price assumptions given that the company is not using conservative figures. To date, the company has successfully replaced reserves and continues to run the mine despite a relatively short mine life given that it isn't an enormous task to replace just at least 0.50 million tonnes per annum of material. However, this is a risk to the Endeavour Silver thesis.

Endeavour Silver - Silver Reserves by Mine (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Given that inflationary pressures are stickier than expected, it's tough to be overly optimistic about this mine over the long run unless we see much higher gold and silver prices which would create a lower hurdle for replacing reserves above the current cut-off grade of ~150 grams per tonne silver-equivalent. So, although Terronera should add 7.0+ million silver-equivalent ounces [SEOs] to Endeavour's production profile post-2025, we could see this partially offset by ~2.0 million less SEOs from Bolanitos depending on whether it remains in operation. In summary, this may not lead to the production growth per share that some are expecting, especially with Endeavour already diluting heavily over the past several years.

Costs & Margins

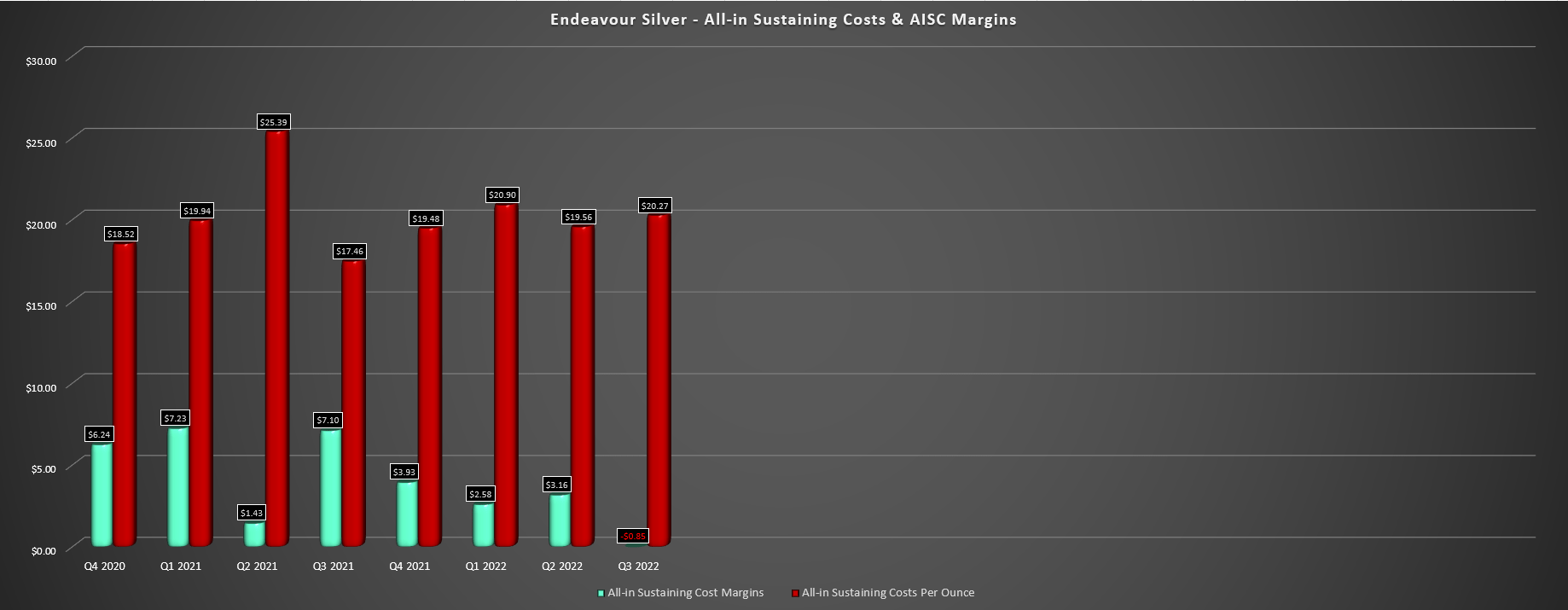

Moving over to costs and margins, Endeavour reported negative AISC margins in Q3 2022, with its all-in-sustaining costs coming in at $20.27/oz, over 4% above its average realized silver price of $19.24/oz. Fortunately, the silver price rebounded in Q4 and has spent most of Q1 above $22.50/oz, suggesting that we should see better margin performance when combined with an outlook of $19.50/oz (guidance mid-point with gold by-product credits) for FY2023. That said, these are still very weak margins and further weakness in the silver price would be very detrimental to the company's profitability. In fact, all-in costs are likely to come in above $23.00/oz this year, and this is very modest exploration spending at its two operating mines this year (~$2.0 million combined).

Endeavour Silver - AISC & AISC Margins (Company Filings, Author's Chart) Terronera Cost Profile vs. Peer Group (Company Presentation)

{kind=link}

{kind=link}

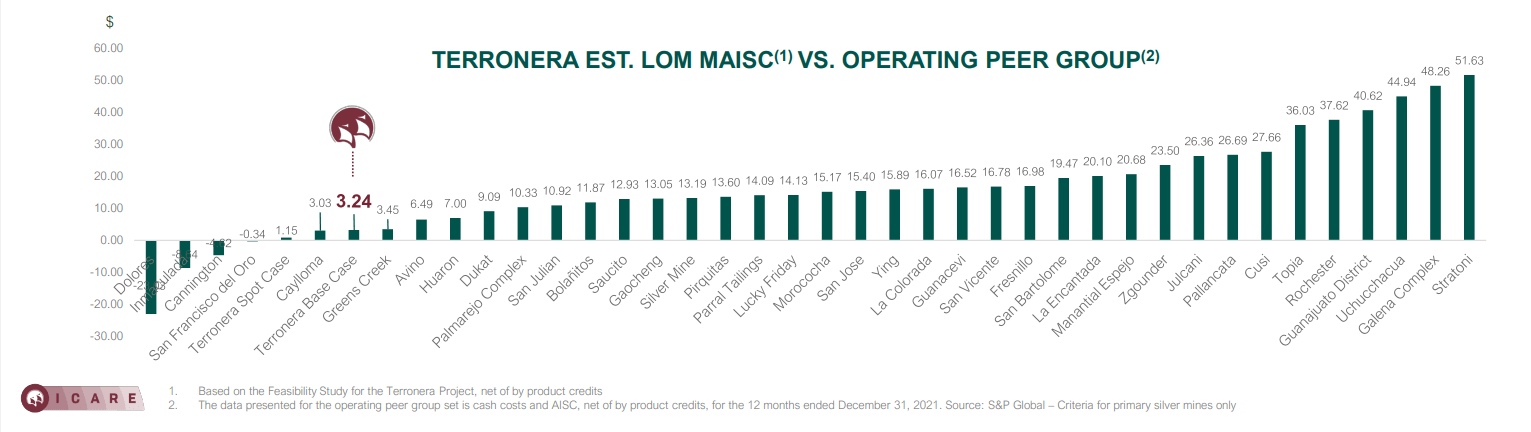

As discussed in previous updates, the antidote to improve margins is the company's development-stage project in Mexico, Terronera. Endeavour noted that it expects to make a development decision on Terronera "soon", and assuming a H2-2023 development decision, we should see commercial production at the asset by Q1 2026. Assuming the asset performs as expected (sub $5.00/oz AISC), this would be a game-changer for Endeavour, pushing silver-equivalent production to north of 13.0 million ounces per annum and pulling consolidated AISC well below $14.00/oz.

That said, this still looks to be at least 30 months away with the project yet to be green-lighted, and it's possible we could see further share dilution if the project comes in above capex estimates. So, although I see this as a positive long-term, it doesn't help EXK today or next year, with its peers continuing to be far more attractive and insulated from lower silver prices. Some examples include SilverCrest ( SILV ) which should enjoy AISC below $10.00/oz even after incorporating inflationary pressures, and MAG Silver ( MAG ), which continues to be one of the highest margin producers sector-wide.

Valuation & Technical Picture

Based on ~196 million fully diluted shares and a share price of US$3.20, Endeavour Silver trades at a market cap ~$625 million. This continues to leave the company trading at a premium to its estimated net asset value of $580 million despite its sharp correction, with Endeavour trading near 1.10x P/NAV. Although this figure is certainly cheap when compared to names like First Majestic ( AG ) at above 2.0x P/NAV, every stock in the sector looks attractively valued compared to First Majestic, so I don't see this as a valid barometer of attractiveness from a valuation standpoint. Plus, if we look at what's available elsewhere, Endeavour Silver is trading at premium vs. much better companies like Endeavour Mining ( OTCQX:EDVMF ), a West African 1.50 million-ounce gold producer, and Osisko Gold Royalties ( OR ), a high-margin royalty company.

Some investors might argue that a silver producer like EXK should trade at a premium to gold producers due to silver's leverage and the fact that primary silver deposits are becoming harder to find each year. Although a fair point, I think this rule should apply only to high-quality silver producers with long reserves lives and Tier-1 operations, such as Hecla ( HL ), not producers in less favorable jurisdictions (Mexico) with short mine lives and all-in sustaining costs above $19.00/oz. So, using a more conservative multiple of 1.15x P/NAV for Endeavour Silver (below its peer group of silver producers), I see a fair value for the stock of US$3.20, pointing to limited upside from current levels.

{kind=link}

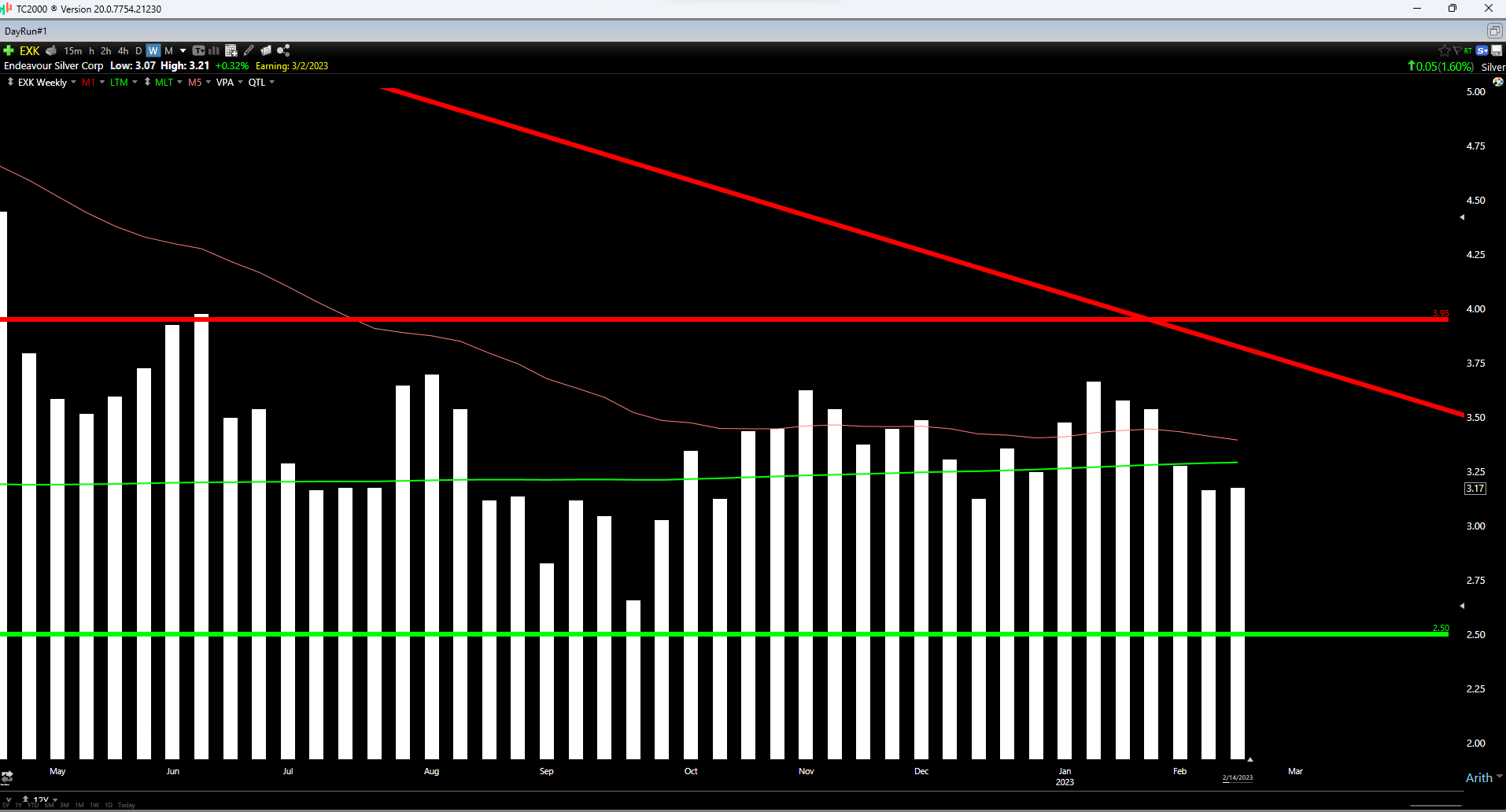

Finally, looking at the technical picture, Endeavour Silver may have pulled back sharply from its recent highs, but it's still trading near the mid-point of its expected trading range, with resistance at US$3.95 and no strong support until US$2.50. If we measure from a current share price of US$3.20, this translates to a reward/risk ratio of 1.07 to 1.0, well below the minimum 6.0/1.0 or higher reward/risk ratio I prefer to justify entering new positions in small-cap producers. Hence, from both a technical and fundamental standpoint, I do not see this as a low-risk buying opportunity, and the stock would need to decline below US$2.55 for me to get interested in the stock from a swing-trading standpoint.

Summary

Endeavour Silver had a solid year in 2022 and 2023 is shaping up to be a decent year as well, with AISC expected to come in lower than I had expected despite sticky inflationary pressures. However, this doesn't change the fact that Endeavour is not cheap, trading at ~11x FY2023 cash flow estimates ($0.29) and above 1.0x P/NAV despite being a small-scale miner in non-Tier-1 jurisdictions with relatively short mine lives. Hence, I don't see any reason to rush into the stock at current levels. For investors looking for precious metals exposure at a more attractive price, one of my favorite ideas continues to be Osisko Gold Royalties on sharp pullbacks, with 45% upside to fair value (US$18.30) and a low-risk business model.

For further details see:

Endeavour Silver: An Inferior Way To Buy The Dip