BKR - Energy Income Weekly: The Energy Sector Starts To Outperform

2023-09-12 15:36:33 ET

Summary

- Energy was the best-performing S&P 500 sector, notably outperforming technology shares.

- The fundamental setup for oil and oil-related equities remains bullish.

- Energy stocks are likely to continue to outperform as higher oil prices raise concerns about inflation and higher interest rates.

Energy Income Performance

It was another week of outperformance for the energy sector. Increasing oil prices raised the prospect of higher inflation, which, in turn, pushed up Treasury yields and pushed down the S&P 500 (SP500). The 10-year Treasury yield (US10Y) rose 2.0%, and the S&P 500 traded 1.3% lower.

{kind=link}

The energy sector ( XLE ) was the top-performing sector in the S&P 500, gaining 1.4%, largely in response to WTI’s 2.3% gain. E&Ps ( XOP ) underperformed the oil price, rising only 0.6% on the week, and oilfield services ( OIH ) performed slightly better, trading up 1.0%.

Midstream underperformed for yet another week, which is to be expected due to the segment’s relatively low direct exposure to oil prices. The Alerian MLP Index declined 1.8% on the week.

Positive inventory data supported oil prices. U.S. crude oil inventories declined by 6.3 million barrels this week, significantly more than the market’s expectations for the third week in a row. Refining margins remain strong, and backwardation ticked higher, indicating a tight supply/demand balance.

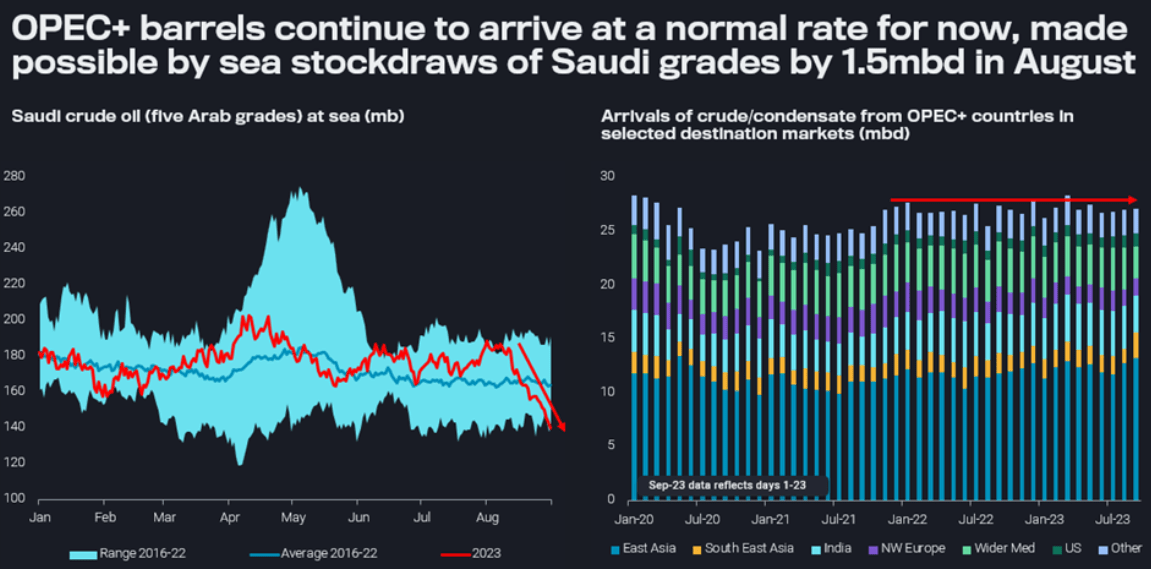

The oil market’s fundamental outlook is set to gain additional support from Saudi Arabia’s export reduction. The chart below, courtesy of Vortexa, shows that Saudi exports began to fall in August instead of July, when its production cut began. The timing of its export reduction will translate to falling onshore inventories in October and beyond as shipments arrive at their destinations.

{kind=link}

Source: Vortexa , Sept. 7, 2023.

Major consultancies see supply deficits even greater than our own forecasts. Rystad, for instance, is forecasting a massive 2.7 million barrel per day supply deficit in the fourth quarter. As the supply deficit hits onshore inventories, it is likely to push crude prices higher. We expect it to push WTI into the $90s per barrel.

The main obstacle to higher prices will come from the release of China's reserves accumulated over recent quarters at low prices. Reserve releases are even more likely after Saudi Aramco's announcement this week that it was increasing prices to its Chinese customers.

While China's reserve releases are likely to prevent an oil price spike and could reduce crude's near-term upside, we don't expect them to be large enough to overwhelm the supply deficit, which we expect to remove roughly 200 million barrels from global inventories from September through year-end. Given where global inventories stand, further draws are likely to exert upward pressure on prices. And once China's reserve releases have run their course, that pressure will intensify.

A Mixed Week for Energy Income

One of the most interesting developments during the week was the energy sector’s 3.4% outperformance of the technology-heavy Nasdaq. If oil prices continue to increase, as we expect, the same dynamics that sent energy shares higher and tech shares lower this week are likely to continue, as higher energy prices translate to higher interest rates. Higher interest rates suppress technology and other growth stock valuations because they make it easy for investors to obtain a high return at no risk today instead of having to wait for uncertain growth to provide a competitive return in the distant future. They thereby incentivize the flow of capital away from technology and other growth stocks and toward sectors that offer immediate cash flow and inflation resistance, with the energy sector being the most obvious beneficiary. Investors should position accordingly before energy’s outperformance grows more pronounced.

The biggest energy income news during the week was Enbridge’s ( ENB ) acquisition of natural gas utility assets from Dominion Energy ( D ). ENB stock ended the week down 5.6%, reflecting the market’s concerns about the company’s strategic direction and its lofty leverage metrics.

Despite the market’s negative reaction, the deal came at an attractive price and will diversify ENB’s operations away from low-growth liquids. We like the deal. ENB is following TC Energy ( TRP ) in favoring its natural gas assets while reducing its liquids exposure. At the moment, TRP stock is more undervalued than ENB, even after ENB’s selloff during the week. We continue to prefer TRP to ENB for a multi-year holding period.

Midstream weakness was concentrated in natural gas-weighted names, as gas prices declined 5.8%. Williams ( WMB ), Kinder Morgan ( KMI ), Oneok ( OKE ), and Antero Midstream ( AM ) all traded at least 2.0% lower.

But even liquids-weighted names struggled, despite the rise in oil prices. Plains All American ( PAA , PAGP ) was among the biggest losers, down 4.7%, on no news other than Citi’s downgrade of the equity from Buy to Neutral. We recently sold our PAA units, though we believe the company’s outlook remains constructive due to the Permian’s bullish long-term production outlook.

Western Midstream Partners ( WES ), another name with a heavy liquids weighting, traded lower after announcing its acquisition of privately-held Meritage Midstream, which operates gathering and processing infrastructure in the Powder River Basin. While shareholders panned the deal, WES management is one of the few we trust when it comes to capital allocation. The company is betting that Powder River Basin production prospects are good, and we wouldn’t bet against it.

WES’s deal was made at an attractive 5.5-times estimated 2024 Adjusted EBITDA. It will also yield synergy opportunities. Importantly, it will diversify WES operations away from their heavy concentration in Occidental Petroleum ( OXY ). We also recently sold our WES units, but we believe the units are attractively priced after the week’s recent selloff.

Delek Logistics Partners ( DKL ), another midstreamer with liquids exposure, also traded lower. DKL traded down 4.9% after its sponsor and owner of its general partner, Delek US Holdings ( DK ) disclosed in an SEC filing that it would sell 13.6 million DKL units. The unit sale will decrease Delek US Holdings’ stake in DKL from 78.7% to 47.6%. Not surprisingly, public unitholders were concerned about the size of the sale and sold DKL units.

Among the week’s gainers, we were pleased to see four of our portfolio holdings listed among the top ten.

{kind=link}

Outside of our holdings, Tellurian ( TELL ) shares gained after the company announced a deal on Tuesday with Baker Hughes ( BKR ) for eight gas turbines for TELL’s Driftwood LNG project. TELL said that it is on schedule to complete certain parts of Driftwood by early next year.

Then on Friday, TELL dropped the requirement that Driftwood’s LNG be sold exclusively to Driftwood equity holders. The shares fell in response to the announcement, as it appeared to signal desperation on the part of TELL in its efforts to sign sale and purchase agreements aimed at supporting the project and obtaining financing. TELL shares remain highly speculative, and we recommend avoiding them.

Holly Energy Partners ( HEP ) hit a 52-week high, ending the week up 6.0% for the week after the shares of its sponsor, HF Sinclair Corp (DINO) rose along with the rest of the refining sector, which is benefitting from strong refining margins. HF Sinclair is in the process of buying HEP in a deal where it is offering 0.315 HF Sinclair shares and $4.00 of cash in exchange for each HEP unit. The terms make HEP’s stock price closely tied to that of HF Sinclair’s.

Weekly HFI Research Energy Income Portfolio Recap

Our portfolio outperformed its benchmark, the Alerian MLP Index, by 2.5% during the week.

{kind=link}

After our portfolio underperformed its benchmark in the first half of the year as we allocated funds to equities exposed to oil prices—which at the time had been out of favor—it is now handily outperforming its benchmark for the third year running.

Calumet Specialty Products Partners ( CLMT ) continued its hot streak, gaining 5.6% on no company-specific news. The move suggests there is a wider recognition of Montana Renewables’ prospects for CLMT. Also, the company is likely to benefit from the high refining margins that have prevailed throughout the third quarter. CLMT remains an attractive long-term holding, and we maintain our $30 price target.

Martin Midstream Partners ( MMLP ) marched 2.6% higher for another week on big volume. We still don’t know the reason for the bulk of the unit buying and can only point to the fact that the units had fallen to absurdly cheap levels before this spate of buying. However, we were gratified to see the company’s Chairman, Ruben Martin, participate in the buying to the tune of 71,120 units, which he bought at an average price of $2.97. We expect to see progress on MMLP’s deleveraging over the coming quarters, which should result in a higher unit price over time.

Genesis Energy ( GEL ) was our portfolio’s third-best performer, gaining 2.1%. The recent increase in GEL shares could be attributable to the surging soda ash price, which is shown below.

{kind=link}

Source: Trading Economics .

GEL’s management reduced its full-year guidance based on the expectation that the lower soda ash prices that prevailed during its second-quarter earnings call on August 3 would continue in the second half. The price surge over recent weeks could see the company outperform management’s—and the market’s—expectations.

Frankly, we’re sufficiently confident in GEL’s long-term return prospects that we actually liked having the units trade under $10 so we could buy more. If they fall back, we’ll most likely continue our purchases. For investors who don’t already own GEL, it remains one of the most attractively-priced midstream equities, even after its recent run-up.

Our biggest underperformers were tied to natural gas, which slumped during the week. Targa Resources ( TRGP ) generates a meaningful amount of EBITDA from the fractionation spread, and its exposure isn’t fully hedged, so its third-quarter results will reflect lower NGL prices. However, natural gas production in the Permian is booming, which we expect to offset the impact of lower NGL prices.

Cheniere Energy ( LNG ) shares fell 2.8% on no news despite a recent increase in European natural gas prices. There has been no change in our long-term thesis for Cheniere. We believe the shares remain attractively priced. We maintain our Buy rating and $180.00 price target.

Equitrans Midstream ( ETRN ) shares were the worst performer, falling 3.5%, presumably in response to lower natural gas prices. However, the stomach-churningly egregious exit deal for outgoing CEO Thomas Karam could have had a role in the poor weekly performance. We were so disgusted by the deal that we momentarily considered selling our shares.

Karam’s transition from CEO to Executive Chairman involves shareholders paying him a $625,000 annual salary, $625,000 in short-term incentives, and $3.25 million in long-term incentives. Nice work if you can get it for simply showing up at the office. Or not—we don’t even know if he is required to show up to be entitled to his compensation.

The deal also involves this gem: a $7.5 million bonus for Karam for having simply done his job.

{kind=link}

So how did ETRN shares perform under Karam’s tenure as CEO? See the chart below:

{kind=link}

Over the period that ETRN lost shareholders 60.3% of their investment, the Alerian Midstream Energy Index gained 58.3%, making ETRN’s underperformance under Karam a disaster for shareholders in both absolute and relative terms.

We have no problem with companies awarding outsized compensation for outperformance, but this is ridiculous.

The $7.5 million bonus referenced Karam’s role in getting the MVP approved, when in reality, the project was the ultimate debacle. The project’s cost escalated from management’s initial tally of $3.5 billion in February 2018, when construction began, to $6.6 billion upon completion, likely late this year or early next year. ETRN shareholders footed the bill for slightly less than half of the project’s cost overruns. Moreover, the MVP’s ultimate returns to ETRN shareholders are likely to end up far below management’s initial projections.

We'd hazard a guess that the amount of influence Tom Karam had on getting the Mountain Valley Pipeline ((MVP)) approved was close to nil. The project was stuck in legal limbo with almost no hope of survival until it was rescued from the scrap heap by a compromise deal between Senator Joe Manchin, Nancy Pelosi, and Chuck Schumer. The deal was made in order to secure Manchin’s support for various government spending measures. It rammed the MVP project through to completion by an act of Congress. The compromise Manchin struck to get the project approved was more likely motivated by his desire to support West Virginia jobs and economy, as well as his party’s political priorities and electoral prospects than Tom Karam’s desire or lobbying efforts to see the project through. Perhaps campaign contributions to Manchin facilitated by Karam—and paid for by ETRN shareholders—played a role, we don’t know.

In any event, Karam would have walked away from ETRN as a wealthy man regardless of whether the MVP was completed or not. So in the twisted logic of public company executive compensation, Karam enjoyed a “heads I win big, tails I don’t lose” arrangement where ETRN shareholders lose either way. They shouldered all ETRN's risks and costs after having collectively lost billions of dollars in market capitalization. This is a dangerous way for a board of directors to incentivize the individuals managing shareholders’ capital.

We’ll hold our nose and continue to hold ETRN stock, though our appraisal of its board of directors and corporate governance has dimmed considerably.

Capital Markets Activity

Enbridge announced a $4.0 billion bought-deal financing in connection with its Dominion Energy asset acquisition. The deal’s underwriters, including the major Canadian banks, have agreed to purchase 87,490,00 common shares at an offering price of $44.73. The price was 7.1% below the previous day’s closing price of ENB’s Canadian-listed shares.

{kind=link}

For further details see:

Energy Income Weekly: The Energy Sector Starts To Outperform