XOM - Energy Investors: Sell PEO Buy XLE

2023-03-06 06:38:50 ET

Summary

- PEO, the Adams Natural Resources Fund (formerly Petroleum & Resources), is a closed-end fund that currently sells at a 15.8% discount to NAV.

- The problem here is that PEO has historically always traded at a substantial discount.

- Meantime, the fund has a 0.56% expense ratio, a whopping 46 basis points higher than the SPDR Energy Select ETF.

- My advice: Sell PEO and Buy XLE.

The idea behind the Adams Natural Resources Fund ( PEO ) is strong, however the implementation is less than optimal for investors. I say that because decades ago, when it was called Petroleum & Resources, I was taken in by the large discount-to-NAV the fund was trading at. If memory serves, I bought it at an 8% discount, and I sold it many years later at, you guessed it, an 8% discount. Today, that discount to NAV is a whopping 15.8%, proving that it was a wise decision to eject this fund from my portfolio and invest more directly into my other energy holdings. During my many years of holding the fund, I tried multiple times to convince the management team to convert the fund to trade at NAV. Today, nothing has changed with the fund other than the name: PEO is still a very expensive way to get diversified exposure to the energy industry and one with a history of relatively unpredictable distributions. My advice: sell PEO and buy the much more cost-efficient Energy Select Sector SPDR ETF ( XLE ) instead.

Investment Thesis

If Putin's horrific war-on-Ukraine - which broke the global energy (and food) supply-chains and caused oil and gas inflation around the planet - taught investors anything last year, it is that they need to have exposure to the energy sector, specifically oil & gas. Investors, of course, have many options in which to accomplish that. They can invest in some of the individual leading oil & gas international integrated companies, focus on U.S. shale operators and/or refiners, or select one of the sector's many funds and ETFs (or a combination of all these). PEO is one of those funds, so let's take a closer look at how it has positioned investors for success going forward.

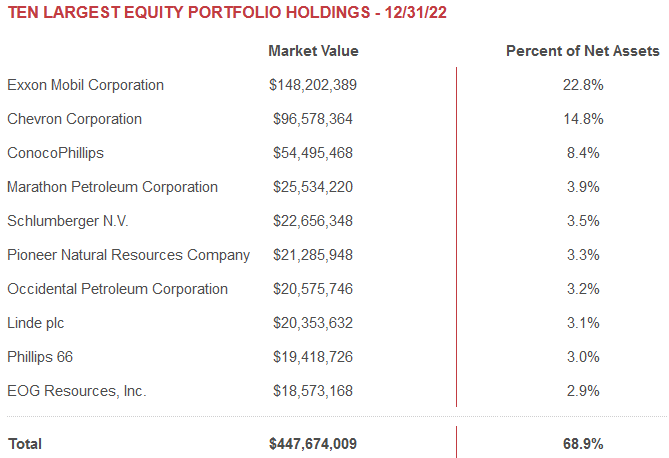

Top-10 Holdings

The top-10 holdings (as of year-end 2022) are shown below and were taken directly from the Adams Funds' PEO webpage , where you can find more detailed information on the fund. As you can see, the top-10 holdings equate to 68.9% of what I would call a very concentrated portfolio of 57 companies:

{kind=link}

The fund is even more heavily concentrated when you consider that 46% of the entire fund is allocated to its top-3 holdings.

The #1 holding is a 22.8% position in Exxon Mobil ( XOM ). As my followers know, since the activist Engine #1 announced it was running a handful of candidates for Exxon's board-of-directors, and was receiving strong support from institutional, pension, and professional money managers who were tired of a decade of negative returns while CEO pay zoomed 30% higher, Exxon's CEO Darren Woods began making significant changes to the company's strategy that arguably he should have been making all along. Exxon dropped its unrealistic production growth targets, slashed the massive over-spending on cap-ex, and starting selling significant non-core low-margin assets and focusing on corporate cost-efficiencies. What's left is a company that is much more focused on key upstream assets - like Guyana and the Permian. As a result, and as a 40-year shareholder, I am more bullish on Exxon today than I have been in over 10-years. Consider reading my popular Seeking Alpha article How Tiny Engine #1 Was Able To Turn Exxon Around . for more information on how Engine #1 acted as a "White Knight" to rescue long-suffering XOM shareholders.

Indeed, and partly as a result of the big changes #1 was able to influence, last year Exxon earned $55.7 billion ($13.26/share) and delivered a whopping $62.1 billion in free-cash-flow. As a result, Exxon is up 39.2% over the past year and currently yields 3.23%. What so many XOM shareholders don't seem to understand was that Engine #1's top priority was never environmental - #1's primary goal (which was published) was to increase Exxon's total returns for ordinary shareholders. And that is exactly what #1 has done.

The #2 holding is Chevron ( CVX ) with a 14.8% weight. My followers know that for many years I have considered Chevron to be the best integrated international major due to its pristine balance sheet, excellent free-cash-flow profile, and its strong mix of long-life LNG and oil production assets (like TCO and in the GoM) combined with its very cost-efficient short-cycle shale position in the Permian Basin.

Chevron also had a very strong 2022, delivering earnings of $35.5 billion ( $18.28/share) and a record $37.6 billion in free-cash-flow. However, and like Exxon, Chevron's CEO Mike Wirth has decided to massively over-emphasize share buybacks and, as a result, the dividend was raised only 6.3% this year. While on the surface that seems like a decent dividend increase, as I explained in my Seeking Alpha article Chevron: What A Big Dividend Disappointment , the 6.3% increase actually pales in comparison to the massive step-up in Chevron's yoy earnings and free-cash-flow and in light of its already pristine balance sheet and massive cash hoard ($18 billion).

ConocoPhillips ( COP ) is the #3 holding with a 8.4% weight. COP too had a very strong 2022 with a record $18.7 billion in earnings ($14.57/share).

While COP is also over-emphasizing share buybacks, it has at least implemented a (base+variable) dividend policy , something that Exxon and Chevron have refused to do, and paid out a total of $4.49/share in dividends last year - significantly more than Exxon's current $3.64/share annual dividend:

Conoco Philllips

As a result, COP has significantly beaten Chevron and Exxon when it comes to total returns over the past five years (not to mention PEO, which it left eating its dust:

The PEO fund also has a significant position in refining in its top-10 holdings, with Marathon Petroleum ( MPC ) and Phillips 66 ( PSX ) combining for a 6.9% weight. With top-10 holdings in Pioneer Natural Resources ( PXD ), Occidental Petroleum ( OXY ), and EOG Resources ( EOG ), PEO also has a solid 9.4% position in the more pure-play Permian shale producers.

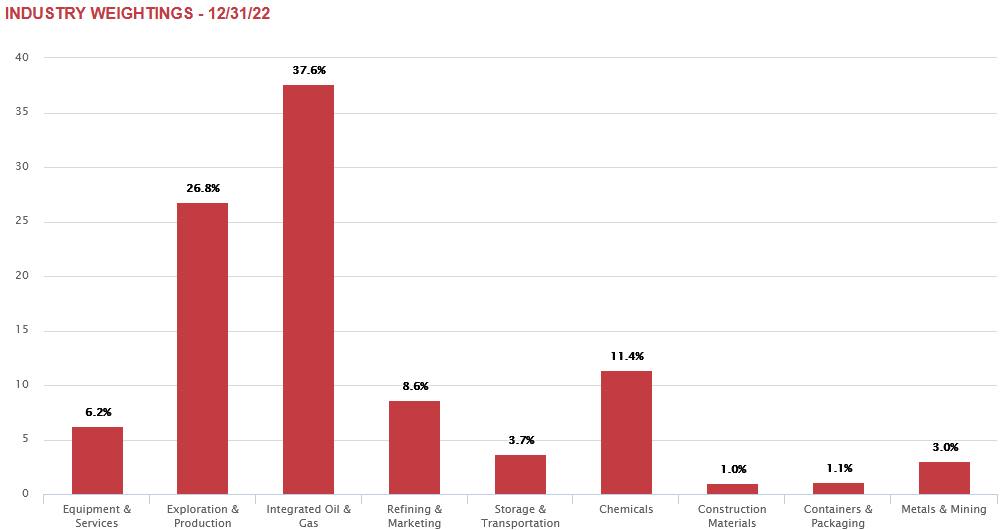

Not surprisingly given the list just examined, the portfolio as a whole gives investors the most exposure to the integrated O&G companies and E&P sub-sectors. Perhaps surprisingly given current and very strong refining margins, the fund has decided to invest more into chemicals (11.4%) as compared to the refiners (8.6%), which I think is a miscalculation on PEO's part given the current global economic environment which is much more advantageous for refiners in my opinion:

{kind=link}

Performance

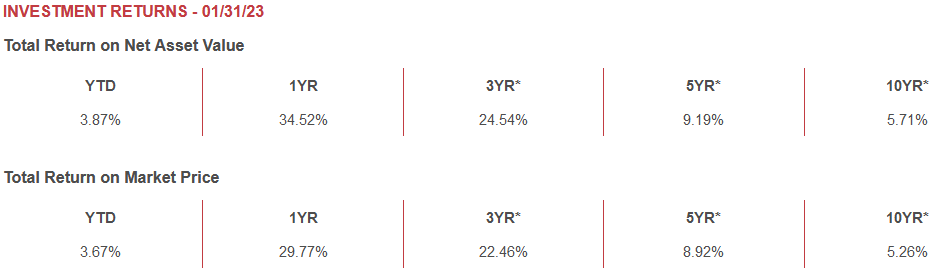

As of the end of January, and as you might expect, PEO has a relatively strong 1-year and 3-year performance track record, but its 10-year returns are a rather pathetic 5.71%:

{kind=link}

The following graphic compares the PEO fund with that of the XLE over the past three years:

As can be seen, the XLE has outperformed PEO by 10%+, much of that likely coming from the fact that XLE's expense ratio of 0.10% compares very favorably to PEO's 0.56% fee.

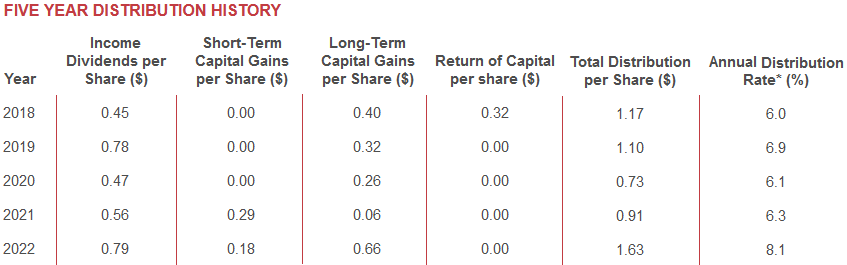

Another consideration for investors is PEO's distributions:

{kind=link}

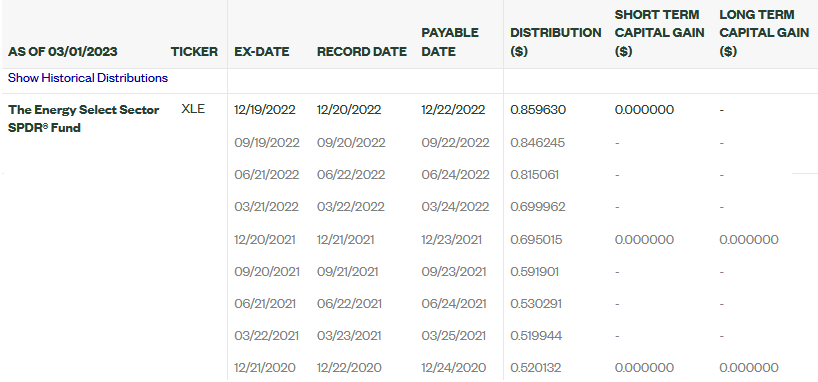

As can be seen, like many funds/ETFs, PEO pays out dividends and capital gains (both short- and long-term). These capital gains distributions can, at times, be considerable and impact your overall Federal tax-burden. On the other hand, the XLE ETF primarily returns qualified dividends to its shareholders with no big capital gains surprises:

{kind=link}

That being the case, investors need to look deeper into the published yield information of these two funds (Seeking Alpha currently reports a 7.41% yield for PEO and 3.69% for XLE), and consider that PEO's "yield" is also based off an equity price that trades at a 15.8% discount to NAV.

Risks

Oil & gas producers are commodity price-takers and, as a result, are directly impacted by global supply/demand fundamentals. The current high-inflation and rising interest rate environment - which is exacerbated by Putin's horrific war-on-Ukraine which continues to cause the planet to expend huge sums of money on a totally unnecessary war - will likely slow global economic growth. If that causes the world to slump into a recession, global demand could fall, and so too would prices. You also might consider reading my popular Seeking Alpha article Investing in the New Age of Energy Abundance: O&G, EVs, and Renewable for a more detailed discussion of global O&G supply/demand fundamentals.

An upside catalyst would be a successful China re-opening that could potentially increase global oil demand by as much as 2 million bpd.

Summary & Conclusion

Given PEO's exorbitantly high annual expense fee (0.56%), it's large discount to NAV (that historically has stayed large), and its arguably less than optimal distribution strategy (i.e. short-term capital gains), I see no reason to hold PEO as compared to a superior and low-cost fund like the XLE ETF. That said, the energy sector is one of the easiest sectors get diversified exposure without employing an ETF. For instance, an investor could simply buy a large integrated international company (say Chevron), a large shale O&G producer with excellent exposure to global LNG (say ConocoPhillips), and a large refiner (say a Phillips 66 or Valero ( VLO )), and attain excellent exposure to the energy sector without paying a fee, and with a known qualified dividend income stream.

For further details see:

Energy Investors: Sell PEO, Buy XLE