ET - Energy Transfer: 9.48% Yield C-Corp Currency Possible Undervalued By Roughly 50%

Summary

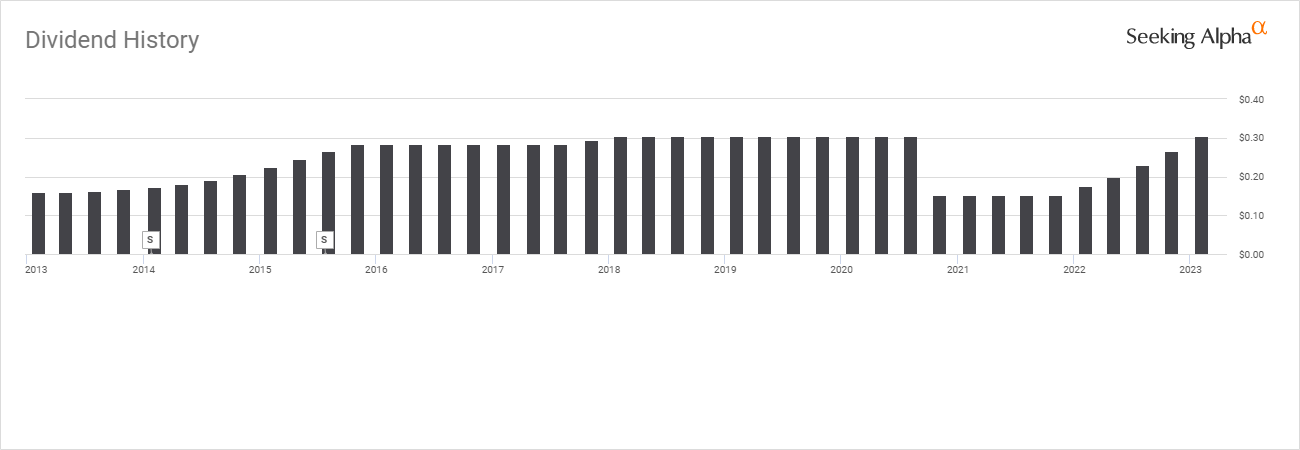

- ET is coming off a strong year as the distribution was increased each quarter and is now back to pre-pandemic levels of $1.22.

- Co-CEO Tom Long issued some color on possible C-Corp Currency, which in my opinion would be a strong catalyst as it could open up the door for new investors.

- ET stock still looks undervalued, and I believe fair value is more in line with $20 per unit based on DCF and adjusted EBITDA to market cap ratios.

There are many energy infrastructure companies that I am invested in and believe are undervalued, but none are more undervalued than Energy Transfer ( ET ), in my opinion. I have been a long-term bull on ET, and units are still significantly undervalued. After Q4, each bear thesis has been disproven by ET as the distribution has now been brought back to its former level of $1.22 per unit. I believe units of ET should be trading much closer to $20 per unit rather than their current level of $12.87, which I will outline in my reasoning later in the article. The bottom line is that management has delivered on their promises, the distribution is restored, and ET is generating higher levels of Adjusted EBITDA and distributable cash flow ((DCF)). ET is still a strong buy, and anyone who is still bearish on ET should read their Form 10-K ( can be read here) and conduct another round of due diligence with an open mind. ET was a gift in the single digits and is still significantly undervalued, below $15 per unit. There was also a critical piece of information in the Q4 earnings call that could be incredibly bullish for units of ET.

{kind=link}

Management kept its word and restored the distribution back to its prior level within 2.5 years

When management delivered the news back in 2020 that the beloved distribution would be reduced by -50% from $1.22 to $0.61, it left a negative stigma on units of ET. Many Seeking Alpha readers left negative comments on my ET articles and didn't believe management would restore the dividend after achieving their financial goals. Well, the quarterly distribution was slashed in half in November of 2020, and after 9 quarters, ET delivered 5 consecutive distribution increases to reinstate the distribution to its pre-pandemic level.

Unitholders who stuck with ET, had 5 quarters at the reduced quarterly distribution level of $0.1525. Starting in Q1 of 2022, ET raised the quarterly distribution by 14.75% to $0.175, then by 14.29% in Q2 to $0.2. In Q3 of 2022, ET raised the distribution by another 15% to $0.23, and finished 2022, providing another 15.22% increase to $0.265. In Q1 of 2023, ET provided its 5th consecutive increase, raising the quarterly distribution by another 15.09%, bringing it back to pre-pandemic levels of $0.305.

{kind=link}

This is a quote from my article ( can be read here ) on 11/17/20:

Selfishly as a unitholder I was really annoyed when the distribution cut was announced. I was of the mindset that even if ET never cracked $10 per unit the compounding distribution would be more than enough for me. Putting the business first instead of my selfishness this was a smart move. ET is taking a similar step to what Kinder Morgan ( KMI ) did back in 2015. KMI slashed its growing quarterly dividend by 75% and held it at $0.125 for 9 consecutive quarters. Since Q3 of 2015 KMI has reduced its net debt by $10 billion. Since the beginning of 2018 KMI has provided investors with 3 increases raising its dividend by 110% from $0.125 to $0.2625 on a quarterly basis. I am not sure how long it will take ET to meet their goals of deleveraging and obviously the business environment could change in the future. While the distribution cut isn't what I wanted to see I understand why they did it and agree it was the correct stance to take.

Management talked a lot about the distribution on the Q4 conference call. The DCF came in at $7.4 billion, which resulted in excess cash flow after distributions of approximately $4.4 billion. Co-CEO Tom Long thanked unitholders who stuck by ET during the period of lower distributions and indicated that the steps taken would allow ET to better capitalize on opportunities that will lead to future success for the partnership and stakeholders. He specifically indicated that future distribution increases would be evaluated on an annual basis while balancing ET's leverage targets, growth opportunities, and potential unit buybacks.

In 2022, ET generated $9.25 billion of DCF on a consolidated level, and $7.4 billion of DCF attributable to partners of ET. There was $4.4 billion of excess cash flow remaining after distributions from the $7.4 billion attributable to partners of ET. In Q4 2022, ET generated $1.9 billion of DCF attributable to partners of ET compared to $1.6 billion YoY with excess cash flow of $965 million after distributions were paid. There is more than enough room for future distribution increases as current projects come online, and capital allocated toward growth projects is redeployed. I have a suspicion management will provide a slight increase to the distribution in Q1 of 2024 and bring the quarterly distribution to its highest level in a decade.

Tom Long discussed the potential of C-Corp Currency during the Q&A portion of the conference call which isn't getting enough attention

Some investors love that energy infrastructure companies such as ET have MLP status, and others stay away due to the K-1 schedule tax form . I am not an accountant, so please discuss all tax implications with a CPA.

MLP investors are treated like business owners meaning that the MLP taxes flow through to the investor, who is considered a partner. When tax time comes around, MLP investors are treated as owners rather than traditional investors and are issued a K-1 schedule. Schedule K-1 reports the gains, losses, interest, dividends, earnings, and other distributions from certain investments or business entities for the previous tax year. These are usually pass-through entities that don't pay corporate tax themselves because they directly pass profits on to their stakeholders or investors. Participants in these investments or enterprises use the figures on the K-1 to compute their income and the tax due on it. You can read more on Schedule K-1 forms here .

I am not going to give an opinion on Schedule K-1 forms as my accountant handles them. What I found interesting on the conference call was that Marc Solecitto from Barclays asked Tom Long about his thoughts on a potential C-Corp currency and if this is something that would be on the table in 2023? This is how Tom Long responded:

Yes, Mark, this is Tom Long. We do have a team that's working on that. I guess the way I would tell you is that we are spending quite a bit of time on evaluating that. And we feel pretty good about probably 2023. We're going to be a little bit careful about putting in guidance out there right now. But it's something that we still think makes a lot of sense and are spending a lot of time. But can't really guide you any closer than that.

What we know from this answer is that a team at ET is working on some type of C-corp structure. There isn't enough detail to know which direction they will be heading, but it's being discussed, and news will probably break sometime in 2023. There isn't enough information today to determine if there will be a dual share class of existing MLP shares and new C-corp shares or if ET will go in a different direction.

I think a C-corp investment in ET will be bullish for long-term value. By eliminating issuing a K-1 ET could become an investible asset for additional funds or income investors who exclude companies that issue a K-1 from their investments. I know plenty of income investors who refuse to invest in companies that issue a K-1 because they don't want to wait for the form to come, they don't want to deal with the tax implications, and they don't want to be burdened with unrelated business taxable income that can trigger unrelated business income tax. If ET just issued a 1099 it would be much cleaner come tax season, and I think ET would see a surge of investors adding ET to their portfolio.

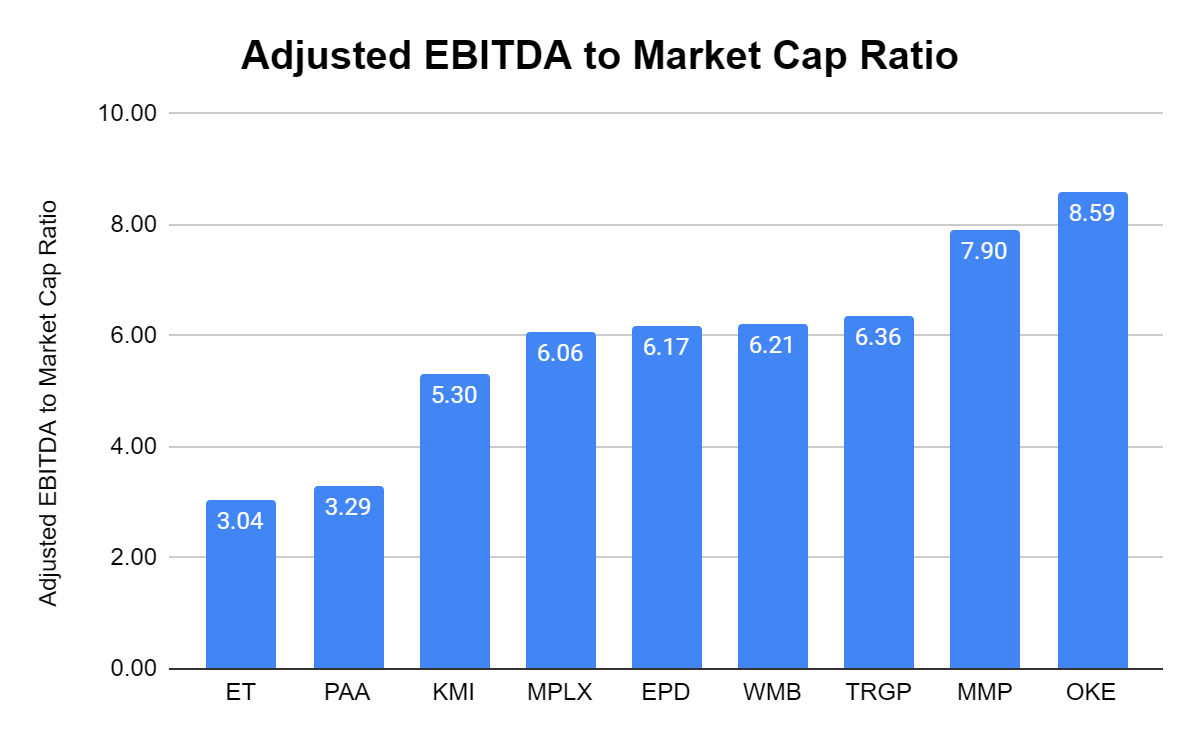

Energy Transfer is still very undervalued when I compare them to their peer group.

I track the market cap, enterprise value, revenue, Adjusted EBITDA, distributable cash flow ((DCF)), and total debt so I can compare the following ratios, Adjusted EBITDA to market cap, EV to Adjusted EBITDA, DCF to Market Cap, Debt to Adjusted EBITDA, and Price to Sales. The energy infrastructure companies I compare ET against are:

- Enterprise Products Partners ( EPD )

- MPLX LP ( MPLX )

- Kinder Morgan ( KMI )

- Plains All American Pipeline ( PAA )

- Williams Companies ( WMB )

- Targa Resources ( TRGP )

- Magellan Midstream Partners ( MMP )

- ONEOK ( OKE )

ET trades at an Adjusted EBITDA to market cap ratio of 3.04x compared to the peer group average of 5.88x. MMP and OKE are above 7x, and MPLX, EPD, WMB, and TRG trade between 6-7x. ET is not given the premium on their Adjusted EBITDA that their peers are, yet ET generated $13.09 billion of Adjusted EBITDA in 2022, and the next largest amount came from EPD with $9.31 billion .

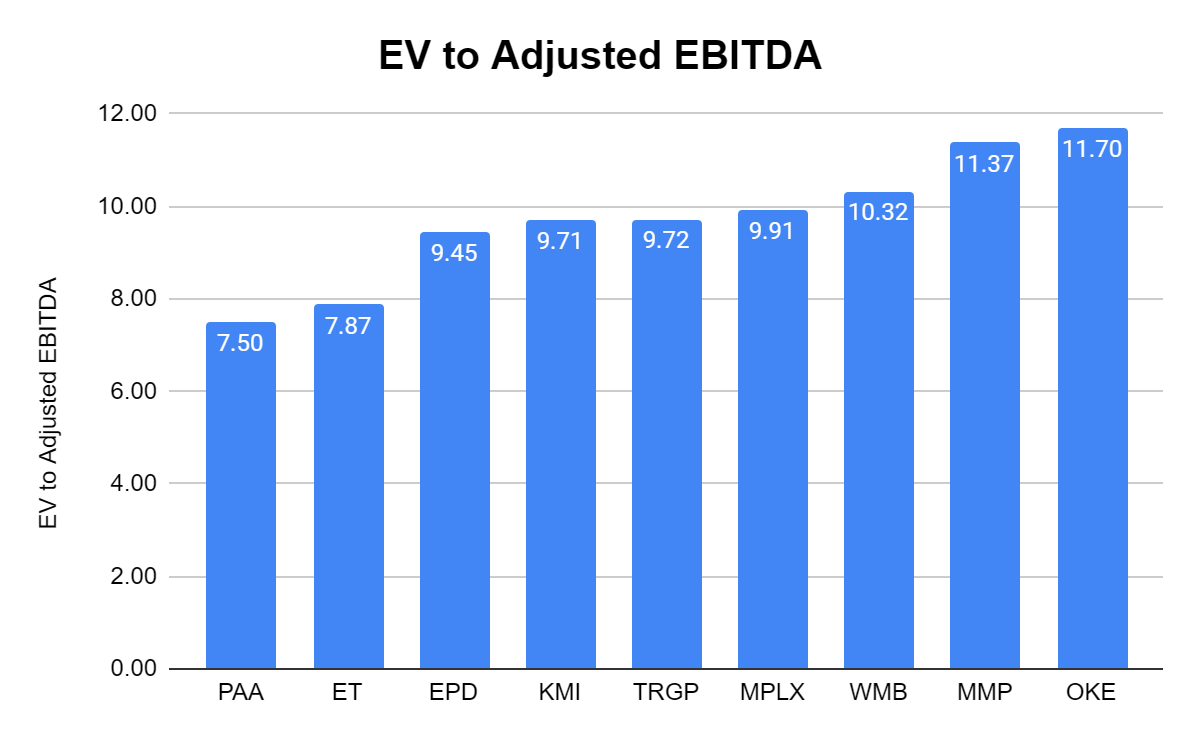

Several readers asked if I could look at Enterprise Value to Adjusted EBITDA also, and I have incorporated it into my valuation. The EV to Adjusted EBITDA ratio is popular because it compares the value of a company, debt included, to the company's cash earnings less non-cash expenses. ET has the 2nd lowest EV to Adjusted EBITDA ratio at 7.87x, which is significantly lower than the peer group average of 9.73x. ET also looks significantly undervalued by this metric as well.

{kind=link}

{kind=link}

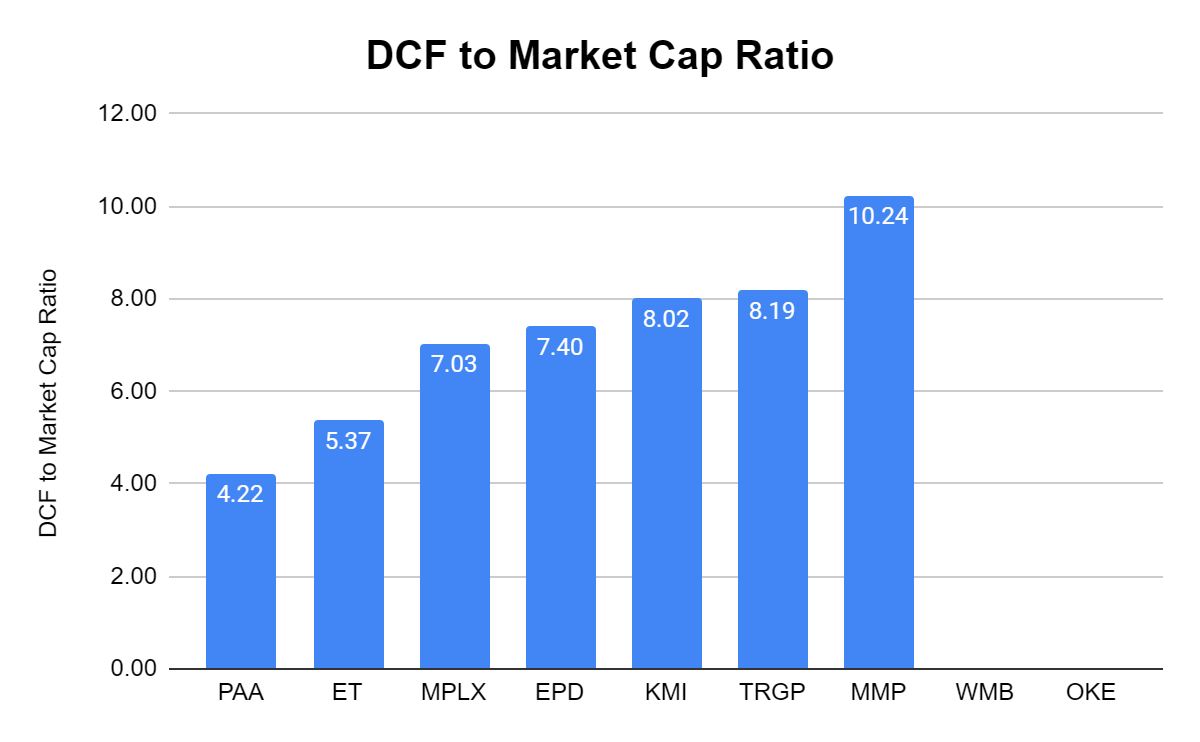

DCF is a critical component for energy infrastructure companies and I look at DCF the same way I look at free cash flow ((FCF)) for traditional equities or funds from operations (FFO) for REITs. When I look at the DCF to market cap ratio, I want to pay the lowest multiple I can for a company's DCF. WMB and OKE don't provide the DCF in their reports, so they are excluded from this metric. ET has the 2nd lowest DCF to market cap ratio of 5.37x compared to 7.21x for the peer group. ET generates $7.4 billion of DCF attributable to its partners, and the market continues to discount its market cap on this metric. ET looks like a steal compared to most of its peers.

{kind=link}

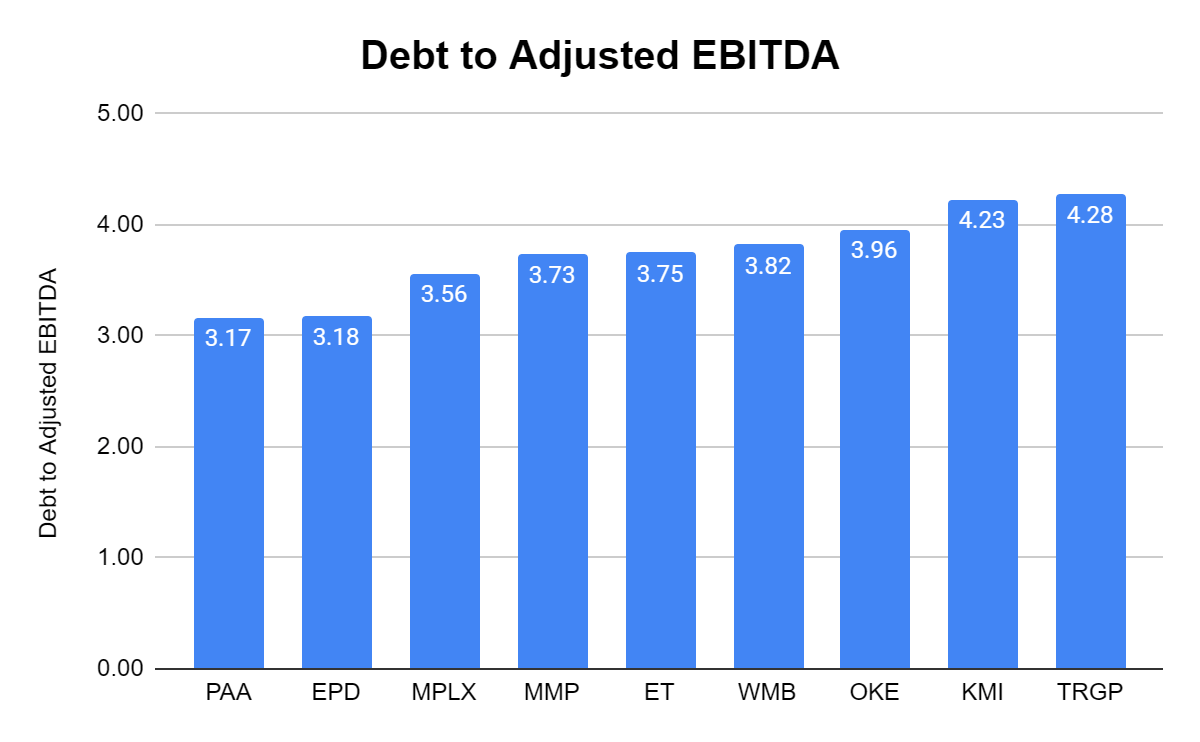

ET had a stigma for having too much debt on its balance sheet. One way to determine ET's debt load compared to its peers is by looking at total debt to Adjusted EBITDA. ET has $49.06 billion in total debt and generates $13.09 billion in Adjusted EBITDA placing its debt to Adjusted EBITDA ratio at 3.75x. The peer group average is 3.74x, placing ET right on the bubble. Based on the Adjusted EBITDA, ET's debt load doesn't look as concerning as it may seem just by looking at the number on its balance sheet.

{kind=link}

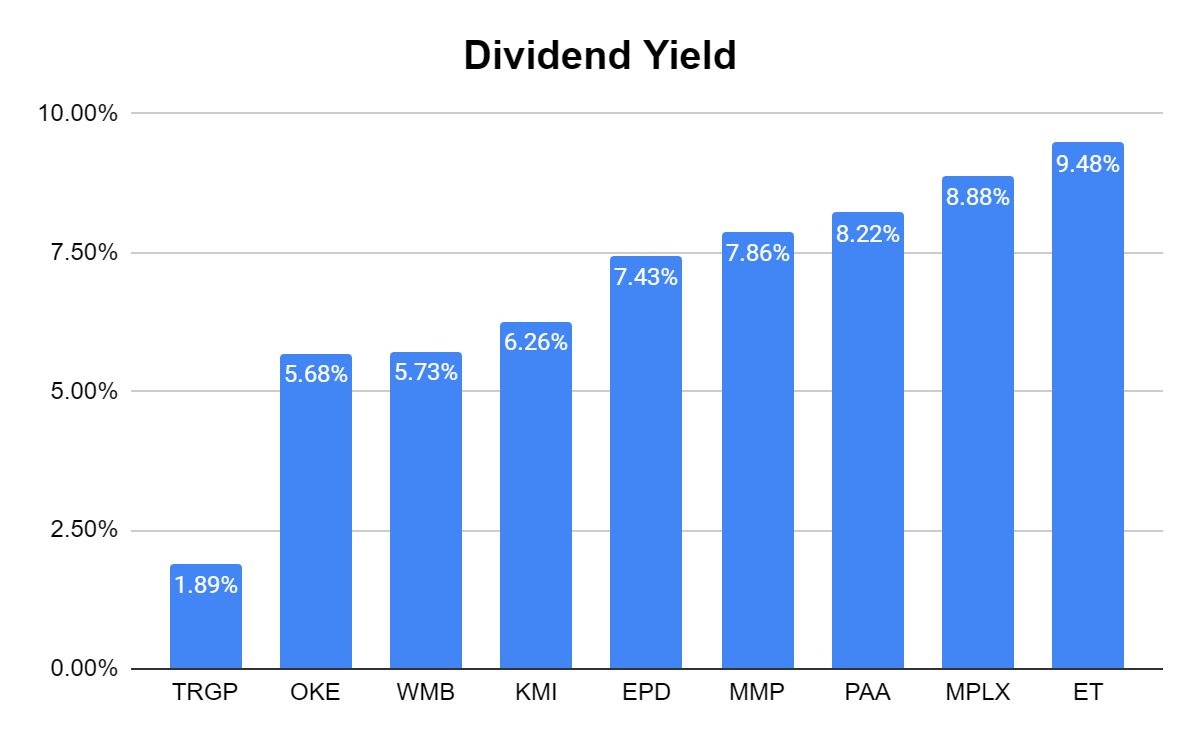

ET now has the largest distribution yield in its peer group. The recent distribution increase has brought its yield to 9.48%. This is the largest of its peers, and as I outlined from the excess DCF left over after paying distributions, the distribution is well covered. The average yield of the group is 6.83%, and when TRGP is excluded, it jumps to 7.44%. ET is still 2.04% larger than the group average when TRGP is excluded.

{kind=link}

Currently, the peer group has an average DCF to market cap ratio of 7.21x and an Adjusted EBITDA to market cap ratio of 5.88x. If ET had a market cap of $53.3 billion, its DCF to market cap ratio would be 7.2x. This would also put ET's Adjusted EBITDA to market cap ratio at 4.07x. If ET had a market cap of $75 billion, its Adjusted EBITDA to market cap ratio would be 5.73x compared to the current peer group average of 5.88x, and its DCF to market cap ratio would jump to 10.13x and compete for the largest multiple on DCF.

Depending on which multiple you would like to use, ET is undervalued by 34.09% to 88.69%. This would correlate to a unit price range of $17.26 to $24.28. I feel the fair value is somewhere around the $20 level, and shares are still drastically undervalued.

Conclusion

ET is still my favorite energy infrastructure company, and management gave us a lot to be thankful for in 2022. The distribution has been restored, future distribution increases are a possibility, C-Corp currency is a possibility, and guidance was strong. Tremendous progress has been made, and the market is still discounting units. While I believe it's not likely that units fall back into the single digits, a strong case can be made that units should trade for at least $17.26, and I think fair value is closer to $20. I will continue to reinvest each distribution and wait for the market to fairly value this company.

For further details see:

Energy Transfer: 9.48% Yield, C-Corp Currency Possible, Undervalued By Roughly 50%