XOM - Energy Transfer: A 15.2% Distribution Increase Going Into Q3 Earnings Is Absolutely Bullish

Summary

- Energy Transfer just delivered another 15.2% distribution increase, placing its annual increase at 73.77%.

- Energy Transfer could be 1 more distribution increase away from restoring its distribution to its 2020 level of $1.22 annualized per share.

- The Oil Majors are increasing production, and I believe this is bullish for Energy Transfer going into earnings as it could lead to additional revenue and DCF.

- Energy Transfer still looks undervalued after reviewing its valuation metrics, and I believe $20 per unit is its fair value.

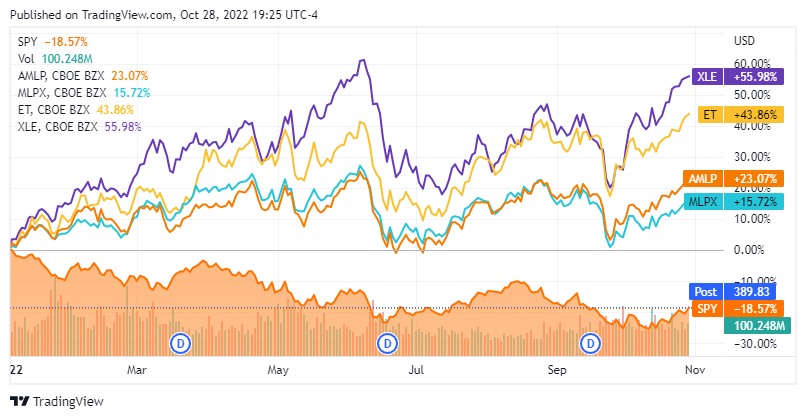

For some time, Big Tech was the market's crown jewel, and energy companies couldn't catch a bid. While big tech still represents the largest segment of the S&P 500, on a YTD basis, not even Apple ( AAPL ), which I consider the best company in the market, was impervious to Mr. Market's wrath. While growth companies plummeted and big tech saw their valuations compress, the energy trade was alive and well. The SPDR S&P 500 Trust ( SPY ) has declined by -18.57% YTD, slightly retracing out of bear market territory, while the Energy Select Sector SPDR ETF ( XLE ) has appreciated by 55.98%. Two of the largest energy infrastructure ETFs have also provided safe havens in 2022 as the ALPS Alerian MLP ETF ( AMLP ) has increased by 23.07%, and the Global X MLP & Energy Infrastructure ETF ( MLPX ) has appreciated by 15.72%.

Energy Transfer ( ET ) has been a longtime favorite of mine in the MLP space, and I have indicated on many occasions that its valuation wasn't justified. Going into Q3 earnings ET has delivered some powerful news and, most recently, increased its distribution by 15.2% just days before the 11/1 earnings release. The distribution will be paid on 11/21 for shareholders as shares will trade ex-dividend 11/3. ET could have declared this in their earnings release, but they didn't. I believe this news being published prior to earnings is bullish and that the earnings report will be full of positive news. I believe the combination of Kelcy Warren buying 3 million additional units of ET, the LNG agreements with Shell, and the 15.2% Distribution increase are all bullish signs, and ET's earnings will act as a catalyst for units to break out to the upside.

{kind=link}

Energy Transfer is delivering on its promise of reinstating the distribution to its previous levels

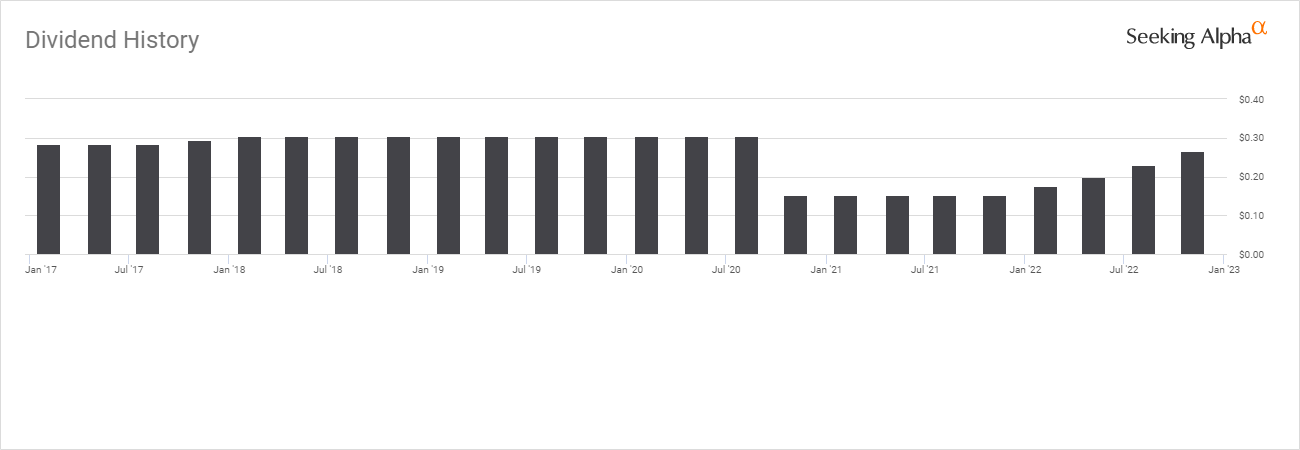

The bears are living in the past and not giving credit where credit is due. Some investors can't get over the fact that ET has never recovered from its 2015 levels, some disagree with management's decisions on acquisitions as the debt level is still large, and others disapproved of the previous distribution reduction. The facts are that in the fall of 2020, ET made the decision to reduce the amount of Distributable Cash Flow [DCF] it paid to shareholders in the form of its distribution to increase its retained DCF and focus on reducing its leverage. Management has been transparent since the decision to reduce the distribution, and on the Q2 earnings call, Tom Long reiterated that future increases to ET's distribution would be evaluated quarterly. Mr. Long also stated that ET's goal is to return the distribution to $0.305 per quarter or $1.22 annually while balancing ET's leverage ratio. We're probably 1 more distribution increase away from those goals as ET is living up to its promises which is a hard pill for the bears to swallow.

The quarterly distribution was reduced by 50%, declining from $0.305 to $0.1525 in Q3 of 2020. For 5 consecutive quarters, ET kept its quarterly distribution payment at $0.1525, and throughout 2022, ET has done nothing but provide quarterly distribution increases. In Q1 of 2022, ET provided its first distribution increase of 14.75% to $0.175. In Q2, ET raised its distribution again by 14.29% to $0.20. In Q3, ET delivered another 15% distribution increase, bringing its quarterly distribution up to $0.23. Going into the Q4 earnings call, ET has provided its 4th distribution increase, raising its quarterly distribution by another 15.2%, placing the quarterly distribution at $0.265. For any investors who were skeptical of ET's plan, there is no reason not to trust management now. The average quarterly distribution increase in 2022 has been 14.81%. If ET was to raise its dividend by its 2022 average quarterly rate, the distribution paid in Q1 of 2023 would be $0.3043, which is, for all intents and purposes, where it was prior to the distribution reduction. If ET delivers a strong earnings report, there is a good chance investors will see the Q1 2023 quarterly distribution reflect $0.305, and ET will have accomplished its goal of returning the distribution back to $1.22 annualized.

This should be looked at as bullish, and any investors who have entered into a position over the past two years should be extremely pleased. Long-term investors have experienced nothing but capital destruction along the way, but things are getting better, and ET is slowly grinding its way higher. If ET wasn't in a strong financial position, they wouldn't continue to increase the distribution, and investors should put their grudges from years past aside and trust that the management team they are invested in will continue to deliver in the future.

{kind=link}

I think ET is going to post strong Q3 results and here is why

Exxon Mobil ( XOM ) just reported their most lucrative quarter as Q3 net income totaled $19.66 billion. Q3 revenues increased 52% YoY from $73.78 billion to $112.07 billion as its production totaled3.7M boe/day. XOM posted a quarterly record from the Permian Basin of nearly 560K boe/day, and gas realizations increased 22%. Chevron ( CVX ) reported $66.64 billion of revenue in Q3 , which was a 49% YoY increase. CVX's net liquid production increased by 49 MB/D, net natural gas oil-equivalent production increased by 49 MB/D YoY. The oil majors are increasing production, and this means more fuel will be moving through ET's system.

{kind=link}

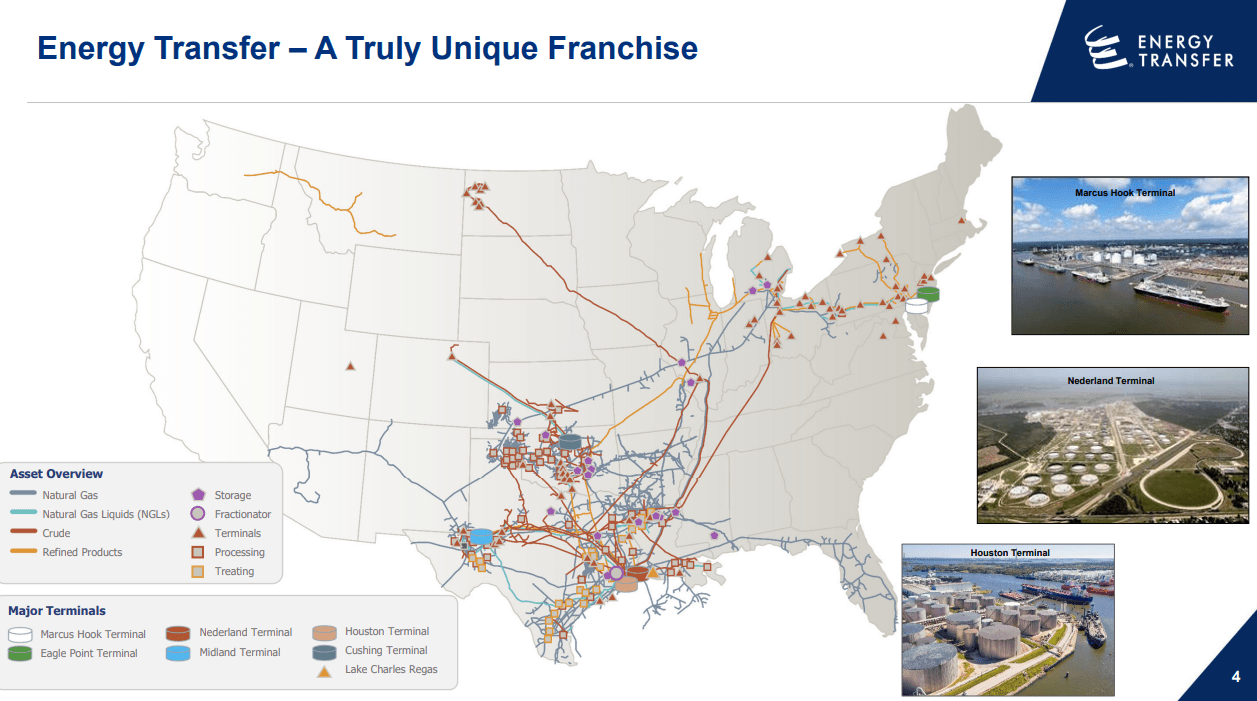

Regardless of where the rigs are, a large portion of the fuels extracted on American soil are transported through ET's infrastructure . ET has 11,300 miles of crude pipelines with 1 million BPD of takeaway capacity in the Permian alone. ET is connected to 6.8MMbbls/d of domestic refining capacity and owns 1.1MMbbls/d of export capacity on the gulf coast. ET also has 65.6 million barrels of terminal capacity in its crude segment. When it comes to NGLs, ET has 5,200 miles of pipeline, then another 3,600 miles of pipeline dedicated to refined products. ET has 53,500 miles of pipelines in its midstream segment with 11.2Bcf/d of processing capacity and 26,900 miles of interstate pipelines with 31 Bcf/d of throughput capacity and 147 Bcf/d of storage capacity.

The majors are increasing production, and that probably means that others, such as Occidental Petroleum ( OXY ), and ConocoPhillips ( COP ), have also increased production. There is a strong possibility that this will mean more fee-based and take-or-pay contracts for ET as their system will be needed to transport excess production. When more drilling occurs the need for transporting these fuels increases, and ET has one of the largest systems connected to every need, from exporting facilities to fractionation terminals. I think this is a strong setup for increased revenue, not just in Q3, but for several quarters in the future.

ET's valuation is still attractive going into Q3 earnings even though its units have increased significantly in 2022.

Going into Q3 ET's valuation is still attractive, and I will compare them to the expanded peer group I created, consisting of

- Enterprise Products Partners ( EPD )

- MPLX LP ( MPLX )

- Kinder Morgan ( KMI )

- Plains All American Pipeline ( PAA )

- Williams Companies ( WMB )

- Targa Resources ( TRGP )

- Magellan Midstream Partners ( MMP )

- ONEOK ( OKE )

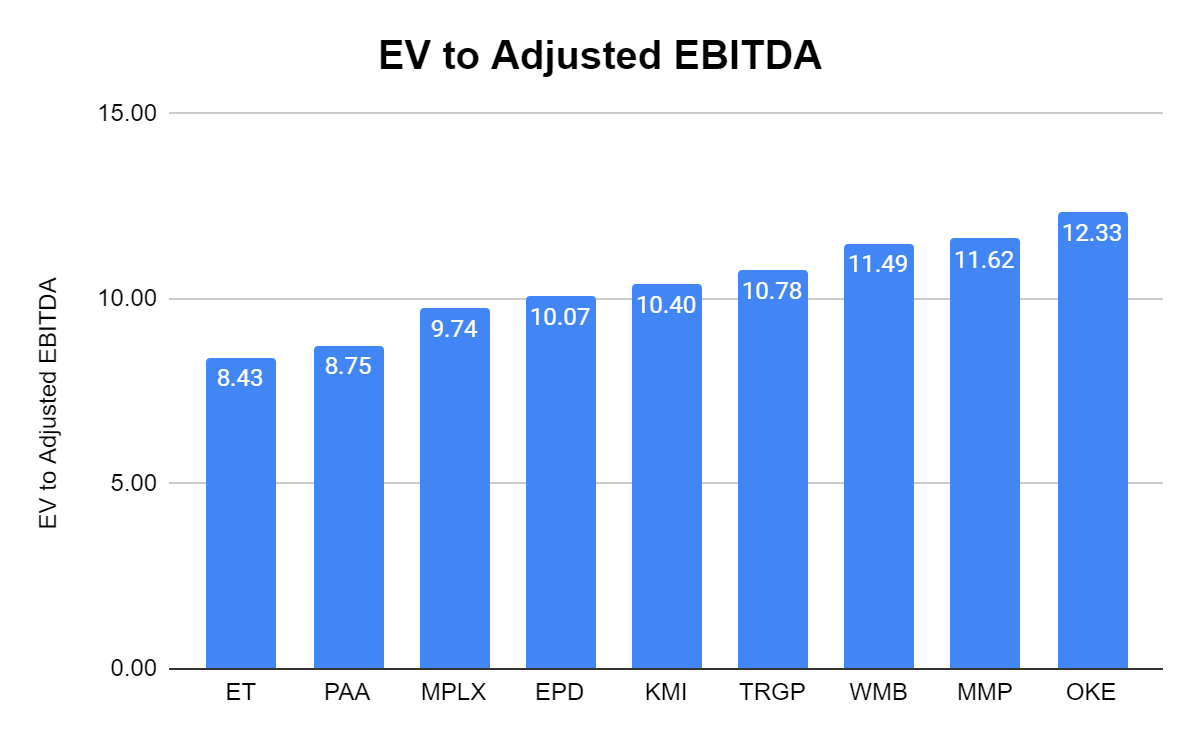

The EV/EBITDA metric is a popular valuation tool that helps investors compare companies as EV calculates a company's total value or assessed worth, while EBITDA measures a company's overall financial performance and profitability. ET trades at a 8.43x compared to the peer group average of 10.40x, indicating that it trades at a more attractive level than its peers.

{kind=link}

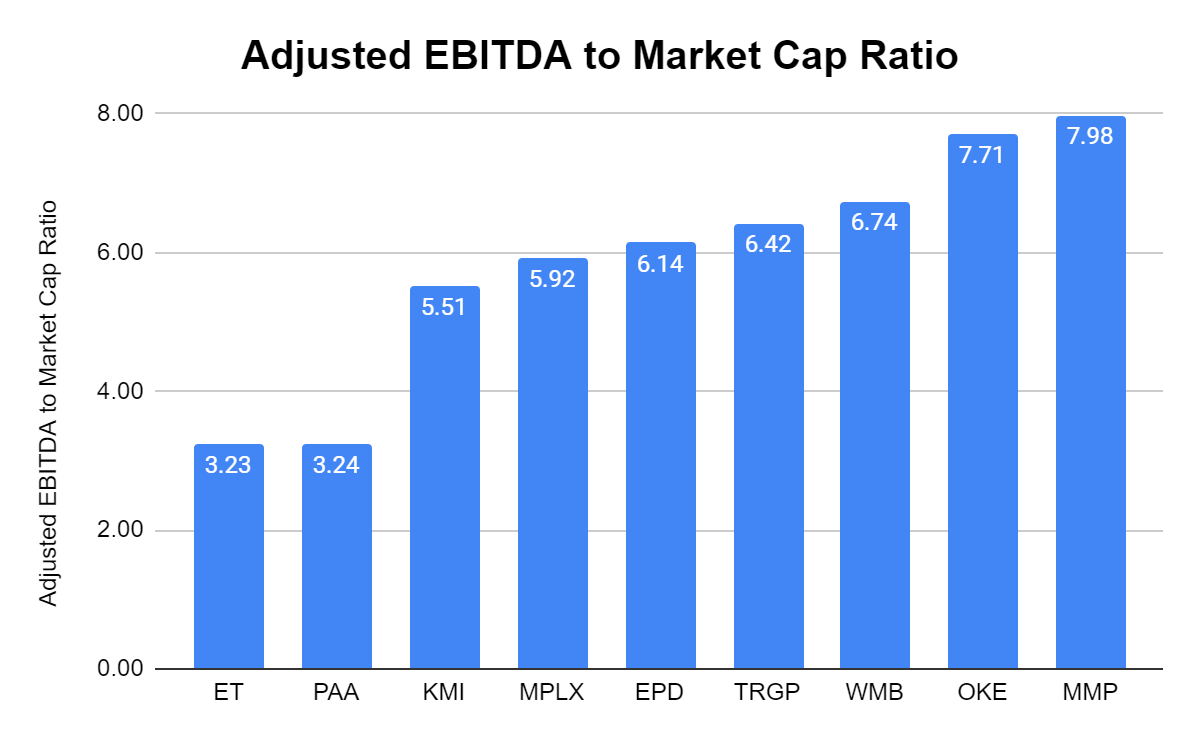

I am a strong believer in looking at the Adjusted EBITDA to market cap ratio because Adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) basically tells you how much cash is left over after paying the business operating costs, excluding one-time charges. I want to see how much I am paying for a midstream operator's Adjusted EBITDA. ET and Plains All American ( PAA ) are neck and neck at 3.23x and 3.24x multiples on their Adjusted EBITDA to market cap. By this metric, ET is drastically undervalued compared to its peers.

{kind=link}

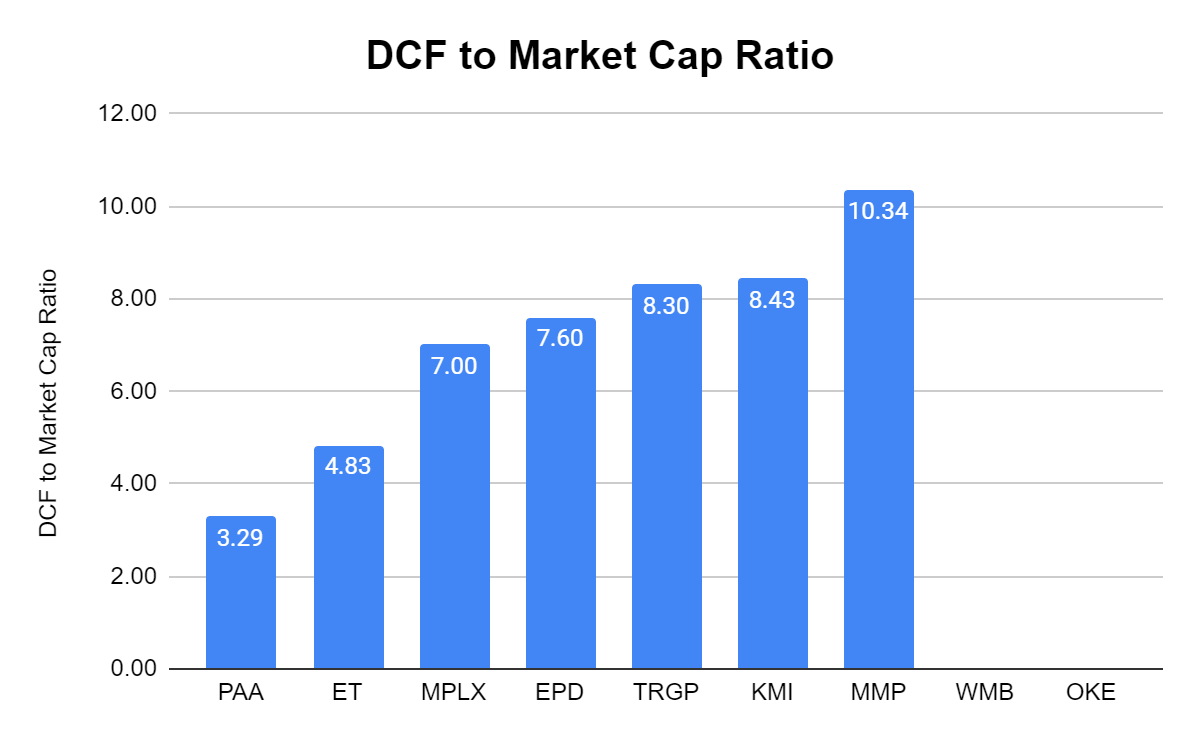

ET trades at a DCF to market cap ratio of 4.83x. WMB and OKE do not report DCF in their quarterly reports, so this is why their numbers are blank on this metric. From the other 7 companies, the DCF to market cap average is 7.11x. ET trades at the 2nd lowest valuation in its peer group on this metric.

{kind=link}

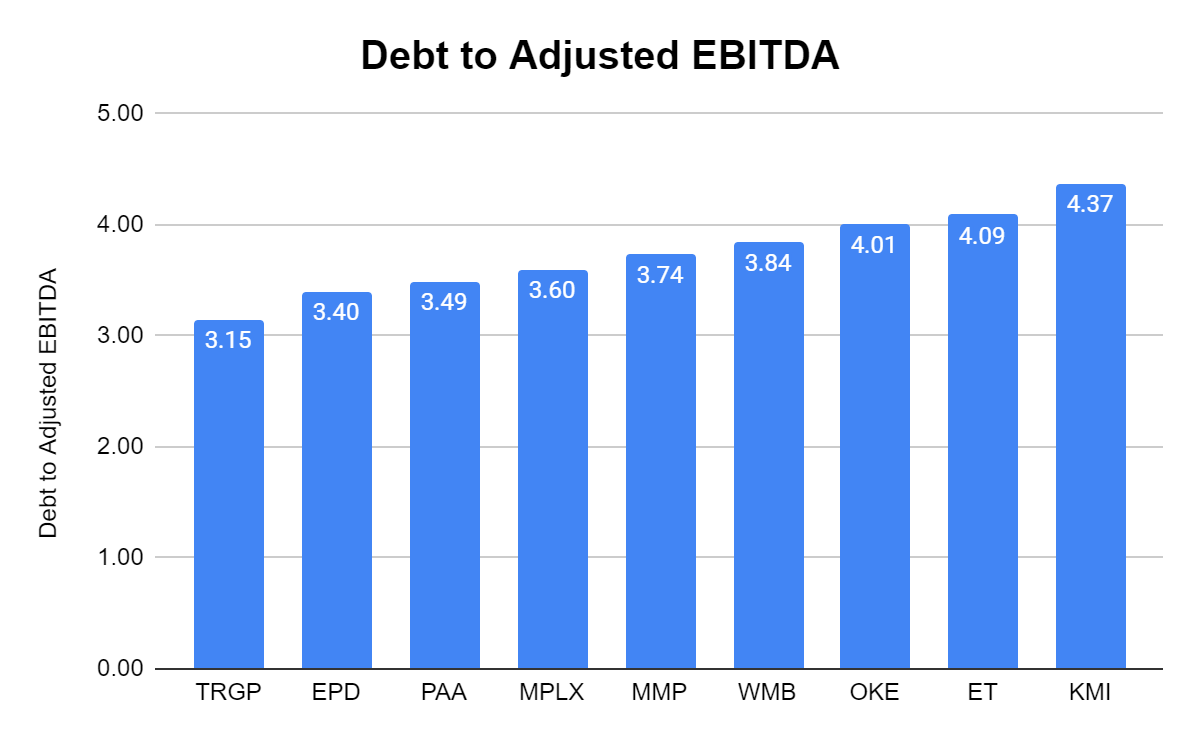

While ET certainly seems undervalued, a main complaint over the years has been its debt and leverage ratio. I look at the total debt to Adjusted EBITDA ratio to see if ET's debt is out of control or if it's in line with its peers. ET's debt is on the higher end of the spectrum, but it's a tight range of 3.15x to 4.37x. The peer group average is 3.74x, and ET trades slightly above it, around 4.09x.

{kind=link}

Conclusion

I believe Q3 earnings will act as a catalyst for units of ET. The majors are increasing production, which should drive revenue and DCF growth. ET has already announced its 4th distribution increase prior to earnings which I am taking as a bullish sign. Over the past year, ET has increased the distribution by 73.77%, and there is no reason why the distribution wouldn't be fully restored in the first half of 2023. I believe ET is drastically undervalued, and fair value is closer to $20 per unit, and if I am correct, investors will recognize significant capital appreciation while collecting a large distribution along the way.

For further details see:

Energy Transfer: A 15.2% Distribution Increase Going Into Q3 Earnings Is Absolutely Bullish