ET - Energy Transfer: An Old Adversary Threatens A Material Future Change

2023-09-17 09:20:54 ET

Summary

- Energy Transfer faces potential shutdown of the DAPL pipeline as the Army Corps of Engineers presents five alternatives, ranging from increased operation to removal.

- The ongoing court case and uncertainty surrounding the pipeline's future overshadow Energy Transfer's other activities and contribute to its cheap valuation.

- The quant system is unable to accurately forecast the impact of the potential liability. Management likewise has a similar stance but believes the liability is insignificant.

- The Quant system "Hold" rating appears to demonstrate some market trepidation about the future despite the relatively low price and high distribution yield.

- Once the DAPL decisions have been made based on the report from the Army Corps of Engineers, the court fights are likely to resume again.

Energy Transfer ( ET ) has had a quiet time since the Army Corps was ordered to come up with a new study on the effects of the DAPL pipeline. That has led more than a few investors to think that the issue died away and there was nothing left to it. In another words, Energy Transfer escaped another close call. But even though these things move very slowly, the Army Corps of Engineers has now prepared that court ordered study and now has five alternatives listed from leaving the pipeline operated at roughly double the current volume to removing the pipeline. In terms of costs, that range goes from a lot more profits to some potentially very large costs. That makes this issue very unacceptable to income shareholder despite the large yield.

Making matters dicier was the fact that the company continued to operate the pipeline and finished construction knowing there were court issues outstanding (as I had noted in past issues). Also, an Illinois court had vacated an expansion permit of the pipeline. That means there were now both a permit in Illinois, and the easement in North Dakota that needed resolution. This situation did allow the pipeline (in both cases) to continue to operate until the federal review was completed. The study by the Army Corps was originally expected months before now. But it had been delayed.

Now it looks like the process will again get going. One of the main issues in the past included the Energy Transfer operator record in Pennsylvania. Those issues are now settled and a matter of record. How those results weigh into what is about to happen is another matter.

Here is the note from Phillips 66 Partners, which is now part of Phillips 66 ( PSX ):

" Since 2016, there has been ongoing litigation challenging permits and easements issued by the U.S. Army Corps of Engineers to Dakota Access, LLC related to the Dakota Access Pipeline. The outcome of the litigation is uncertain, and there can be no assurances that the pipeline will not be shut down, either temporarily or permanently."

Source: Phillips 66 Partners Fiscal Year 2020 10-K .

Before this discussion continues, it needs to be noted that Energy Transfer management has long held that the company has strong defenses and at this time considers this litigation a normal part of business where the liability either cannot be determined or is likely to be insignificant. Whether the upcoming public comment time period of court action after that changes this stance is pure speculation at this point.

Since Phillips 66 Partnership was the smallest partner in the DAPL partnership and was its own legal entity at the time, there was a good deal more detail on the ongoing dispute in the legal filings of this entity (until it was merged into Phillips 66). This management stated in several conference calls that they expected the court fight to continue for years.

The problem was that everything "died down" until the latest study was complete. There really was nothing legal to be done until the results became public. Now it appears there will be a period of public commenting before the next step. That means that any court filings are likely to happen next year.

The key is that as the operator of this partnership, this news is likely to overshadow anything else Energy Transfer does and the uncertainty surrounding this issue is one significant reason that the partnership common units are considered cheap and are likely to stay cheap until this issue is resolved.

Profitability

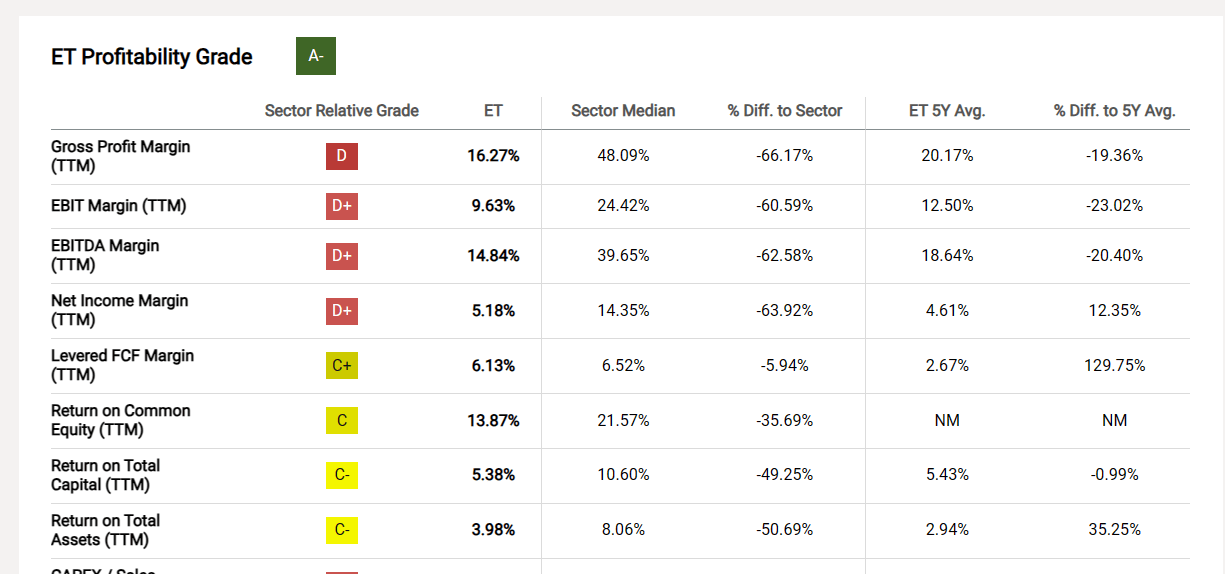

Those of us who have followed Energy Transfer long term know that the record here is probably on the minimal side from all these issues that are likely to detract from profitability.

Seeking Alpha Summary Of Energy Transfer Profitability Ratios (Seeking Alpha Website September 15, 2023, 2022.)

{kind=link}

As the Seeking Alpha website shows, this is one of the least profitable operators in the industry. It is also very large and investment grade. A court case like this, if it goes in a "big time" unfavorable direction, could have a material impact on the future of the company overnight.

Quant System

One of the things about the Quant system is that it is primarily a numbers system. There is really no impact on a system like this for something like the DAPL case that is really a footnote in most official reports. The only real cost at the current time is legal fees, which are likely to be very small compared to the operations of a big company like this.

Seeking Alpha Quant System Outlook For Energy Transfer (Seeking Alpha Website September 15, 2023)

Therefore, the quant system is really unable to forecast the effects of a potential liability like this. Instead, evaluating the liability is a qualitative process. Once the court case is decided and all appeals and other motions have been dealt with, then there will be considerably more certainty to the outlook that something like that quant system can deal with.

Still, the system has a "hold" rating on the common units. This does indicate some trepidation in the market that likely relates to the uncertainty of all options listed in the Army Corps of Engineers report (study).

Evaluating Risk

One of the things that investors nearly always under-estimate is risk. David Dreman in his latest book "Contrarian Investment Strategy: The Psychological Edge" has noted this. But so have many other authors.

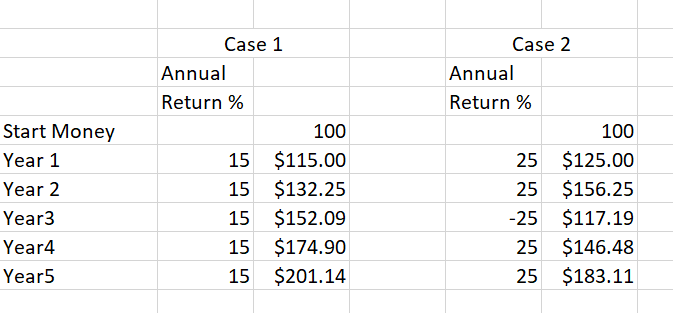

The mathematical argument would be something like this:

Comparison Of Returns To Show The Effect Of One Loss Year (Author)

{kind=link}

The reason is that many will go for Case 2 because the returns look good until a loss year happens. Many times, that loss year is far in excess of the 25% shown. But many investors assume that year will not happen because it did not in the past.

For me, I have followed many examples like this. The latest of those was my coverage of California Resources ( CRC ) up until the bankruptcy filing in fiscal year 2020. The comments to my articles clearly state that the company had "valuable land" that would get it out of trouble. Alternatively, the company had a lot of reserves behind each share (never mind that no one reviewed the high cost of those reserves or lack of profitability of the company compared to debt levels).

So, when California Resources soared before bankruptcy, clearly it was going to go far higher based upon those optimistic assumptions and actually many more. So, there was no reason to sell. That stock did rally again after that (but not as much). That was clearly time to back up the truck.

But then came fiscal year 2020 and my mailbox filled with investors that lost a lot of money and were disgusted. That was a total loss. The 100% brought more than a few investors to zero which was far worse than the chart above.

I have many more of these in my profile. One 100% loss can hurt a lot when you have "backed up the truck".

As against that are those who took that same level of risk and got away with it. Those comments are similar to the comments to my California Resources articles in the years leading up to the bankruptcy. Clearly there was no risk because nothing bad happened in the past. So exactly "what was I worried about?" Because clearly, there was nothing to worry about.

Key Ideas

Probably there is still a lot of sentiment that Energy Transfer as an investment carries no risk because it has because the dispute has had no consequences so far and the last 18 months or so have been quiet ("therefore there is no problem anymore").

The Army Corps of Engineers clearly states that shutting down the pipeline and removing it is an option. It also clearly states that allowing the pipeline to operating at a higher capacity is also an alternative. But that range of possibilities is too much for income investors that demand a safe level of returns.

There are many investors that assert that Energy Transfer is not going to go broke over this, and there certainly could be more years of court battles ahead. However, the company does not have to go under for that distribution to be cut or even eliminated in the future. Removing a pipeline under court order could prove to be expensive before you get to lawsuits claiming all sorts of things related to an unfavorable court outcome. There is a range of outcomes here, from a big negative number to a large positive number.

Suitability

That makes these common units (and probably the preferred as well) suitable for investors that can understand the risk. These investors can also take profits and walk away before trouble hits.

This happened in the past for me when Mcdermott ( MCDIF ) got financially stretched and eventually filed bankruptcy . I covered this as a speculative opportunity as McDermott had gotten stretched in the past. But the groups I knew got in and doubled their money and then were long gone before the company filed bankruptcy. So, for them, my coverage was an opportunity. It was not anything close to that for the average investor that cannot walk away.

Energy Transfer management has long held in official documents that any possible liability cannot be determined, and management has strong defenses. That may or may not turn out to be the case when this is over. But the key for any investor invested in any Energy Transfer security is "do you have a plan that protects you just in case?" Because so many investors have told me in the past that they did not and are now feeling the consequences.

For further details see:

Energy Transfer: An Old Adversary Threatens A Material Future Change