ET - Energy Transfer And Enterprise Products Offer High Yields But Only One Is A Buy

2023-08-23 07:42:26 ET

Summary

- Energy Transfer is yielding nearly 10%, is it a buy?

- The company is set to acquire Crestwood Equity Partners, but that might be a red flag.

- I explain how I evaluate ET relative to the stock of Enterprise Products Partners.

- It is important to look beyond the distribution yield in determining prospective value.

Energy Transfer ( ET ) has been in the news lately after the company announced an agreement to acquire Crestwood Equity Partners ( CEQP ). A lot has been said about this transaction, though sentiment has been most universally positive among my peers. I suspect a lot of that optimism may be due to the fact that ET remains cheap - extremely cheap. But that might present the very issue here: why is ET engaging in yet another large acquisition when its units are trading so cheaply and the company appears to be generating considerable free cash flow after paying for distributions and growth CapEx? It is useful to compare ET with my top energy pick Enterprise Products Partners ( EPD ) to understand why cheap stocks sometimes deserve to be cheap. It may be difficult to resist buying here, but I continue to recommend avoiding this stock in favor of names more likely to deliver stronger unitholder returns.

ET Stock Price

ET has delivered phenomenal returns for those who bought during the pandemic lows, as it has become clear (perhaps it was always clear to some) that the commodities market is here to stay. That said, ET is still trading below pre-pandemic levels in spite of having brought its distribution back to 2019 levels (the company had cut its distribution in 2020).

I last covered ET in October of 2022 where I stated that the units were "likely to always sustain a relative discount until there is a drastic change in capital allocation policies - a committed unit buyback seems like the most obvious catalyst." Around that same time, I also issued bullish reports for EPD and Magellan Midstream Partners ( MMP ). I still own EPD as one of my top holdings, and I remain neutral on ET in spite of the apparent undervaluation.

ET Stock Key Metrics

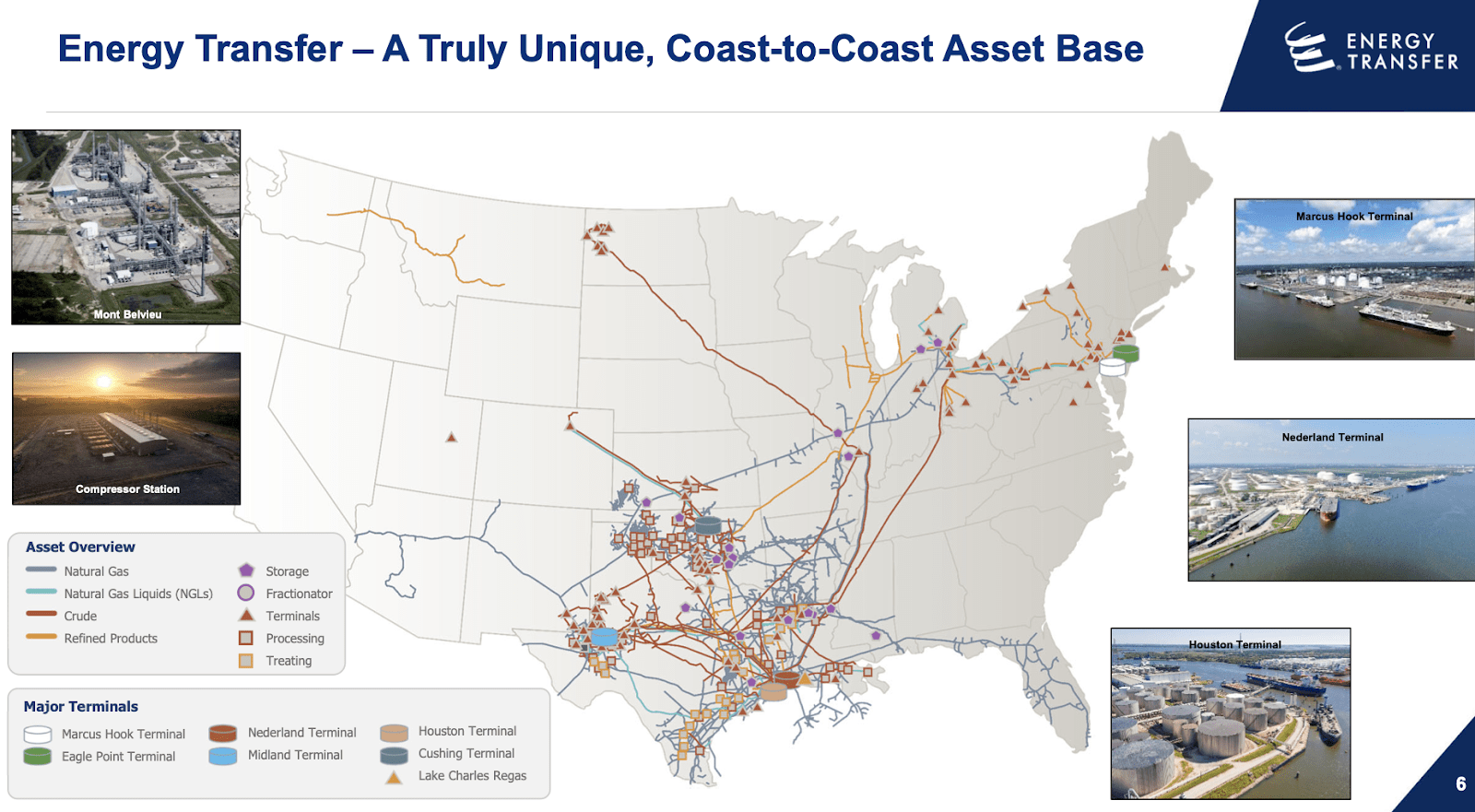

ET is one of the largest midstream companies in the country. While this report will highlight some of the issues with the company, size is not something I will argue.

{kind=link}

ET is diversified but has greater exposure to natural gas and NGLs. Nowadays, midstream operators with lower crude oil exposure have sometimes traded at premiums, but that is obviously not the case here.

{kind=link}

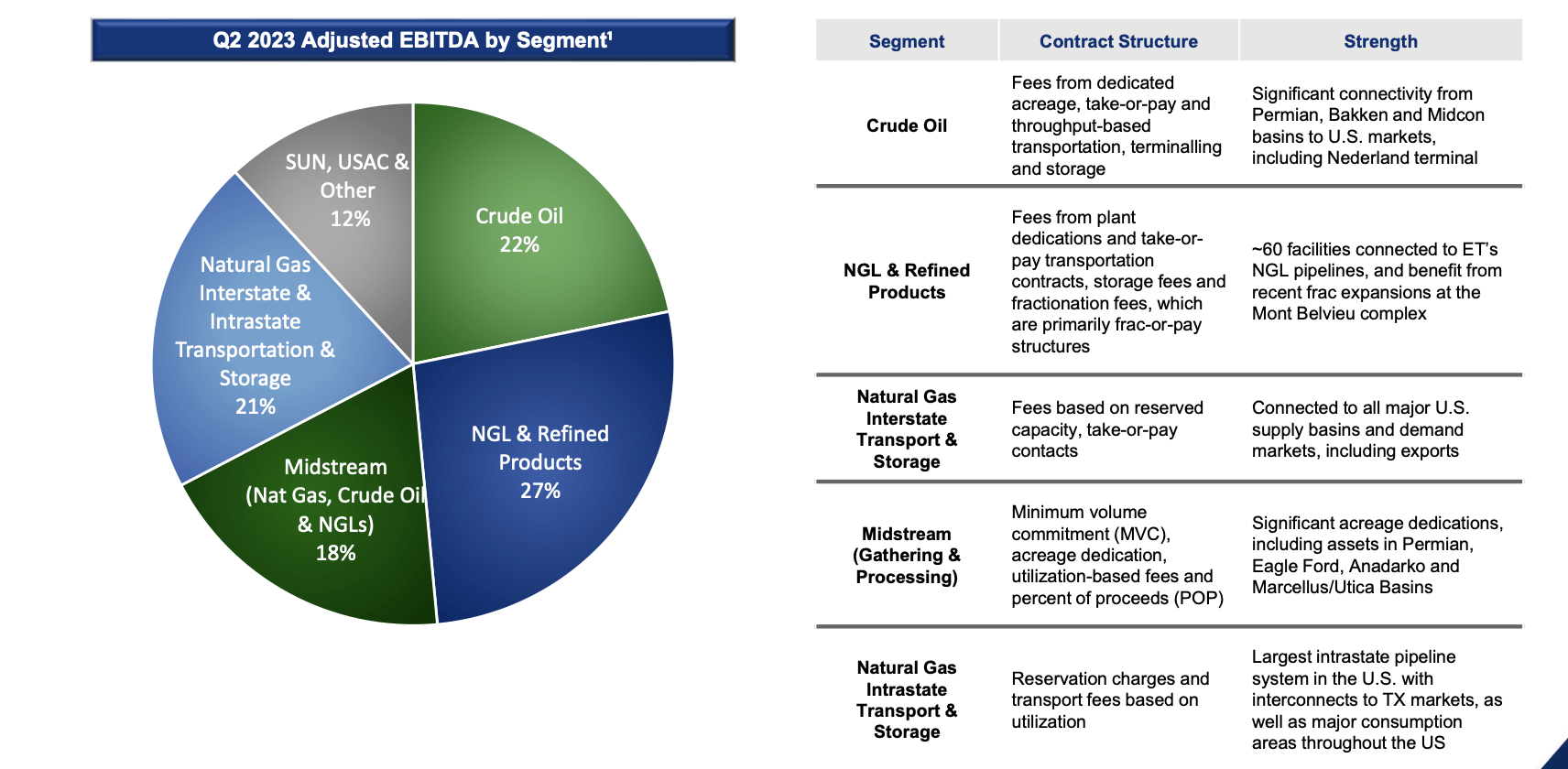

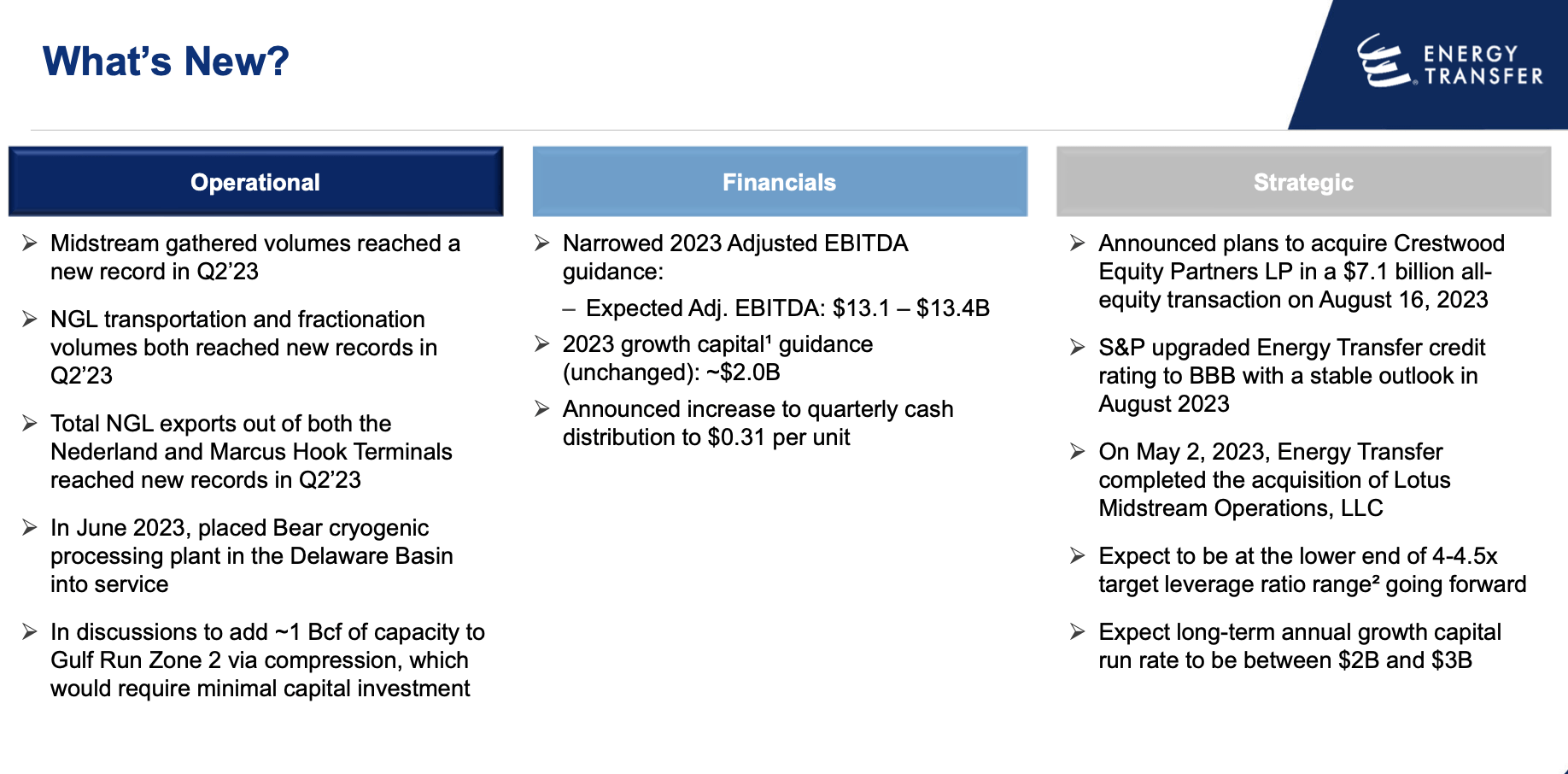

Even as commodity prices lap tough 2022 comparables, ET is still guiding for solid growth to up to $13.4 billion in adjusted EBITDA. On the conference call , management noted that they were able to partially offset lower NGL prices with record volumes. After increasing the distribution to $0.31 per unit, management has finally brought the distribution to higher than pre-pandemic levels, fulfilling a recent unitholder promise. Management is targeting annual distribution growth in the 3% to 5% range. With units fetching a yield close to double-digits, that may look like an appealing investment proposition.

{kind=link}

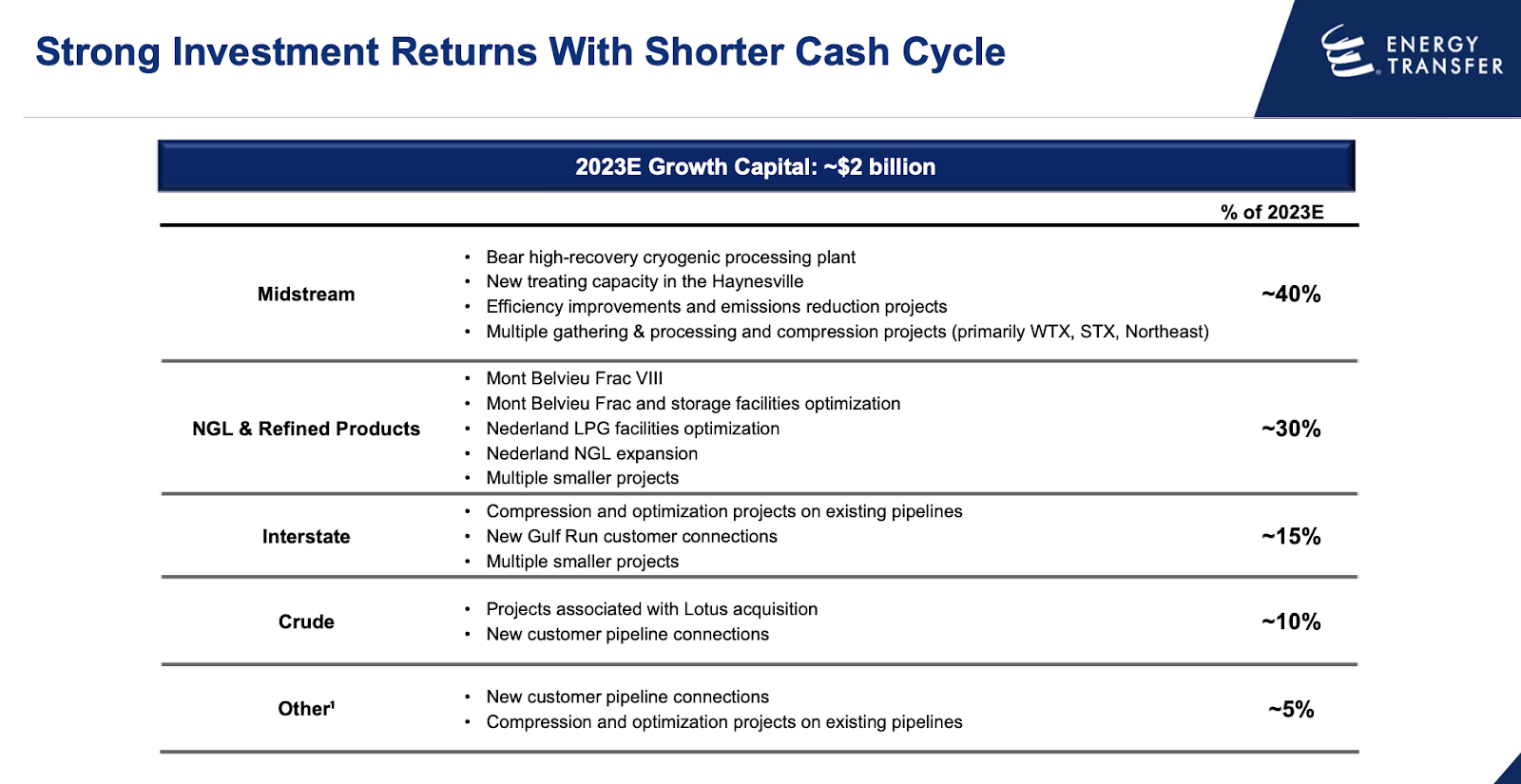

Management is guiding for growth CapEx to hover around $2 billion to $3 billion annually. I expect it to trend near the high end of that target based on management's past tendency to favor expansion above all else.

{kind=link}

Midstream names typically can get solid returns from growth projects due to already having solid foundations to invest upon. I previously covered why I am of the view that ET has shown worse execut ion than peers in terms of getting their projected returns from growth CapEx.

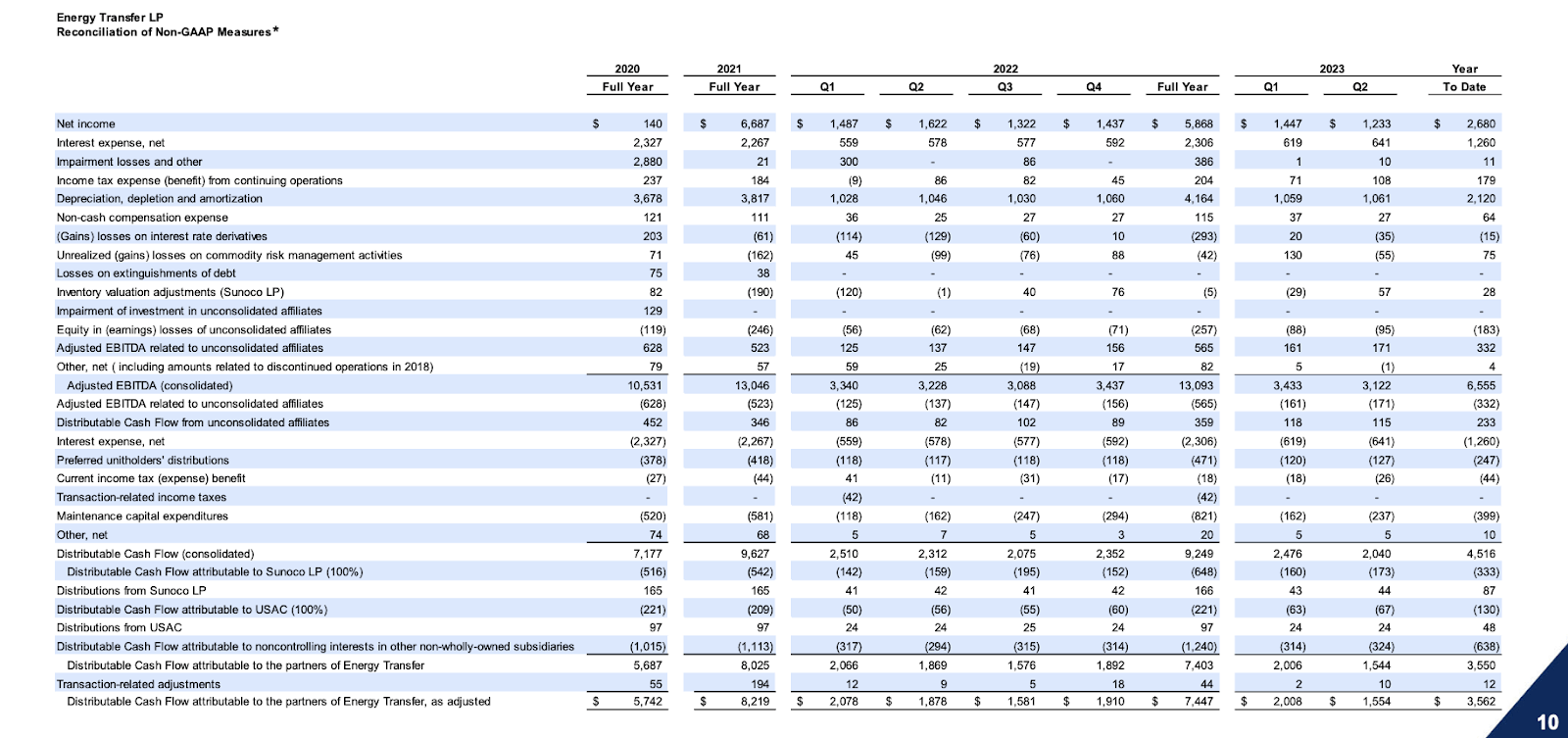

Even so, ET is gushing cash. The company generated $7.4 billion in distributable cash flow in 2022 and I expect the company to generate a similar amount this year.

{kind=link}

After paying around $3.95 billion in distributions and funding $2 billion in growth CapEx this year, that leaves around $1.45 billion of excess cash flow that can be used for debt paydown, unit repurchases, accelerated distribution growth, or more growth CapEx. Even after accounting for growth CapEx, ET is trading for around 6.7x free cash flow. That is dirt cheap.

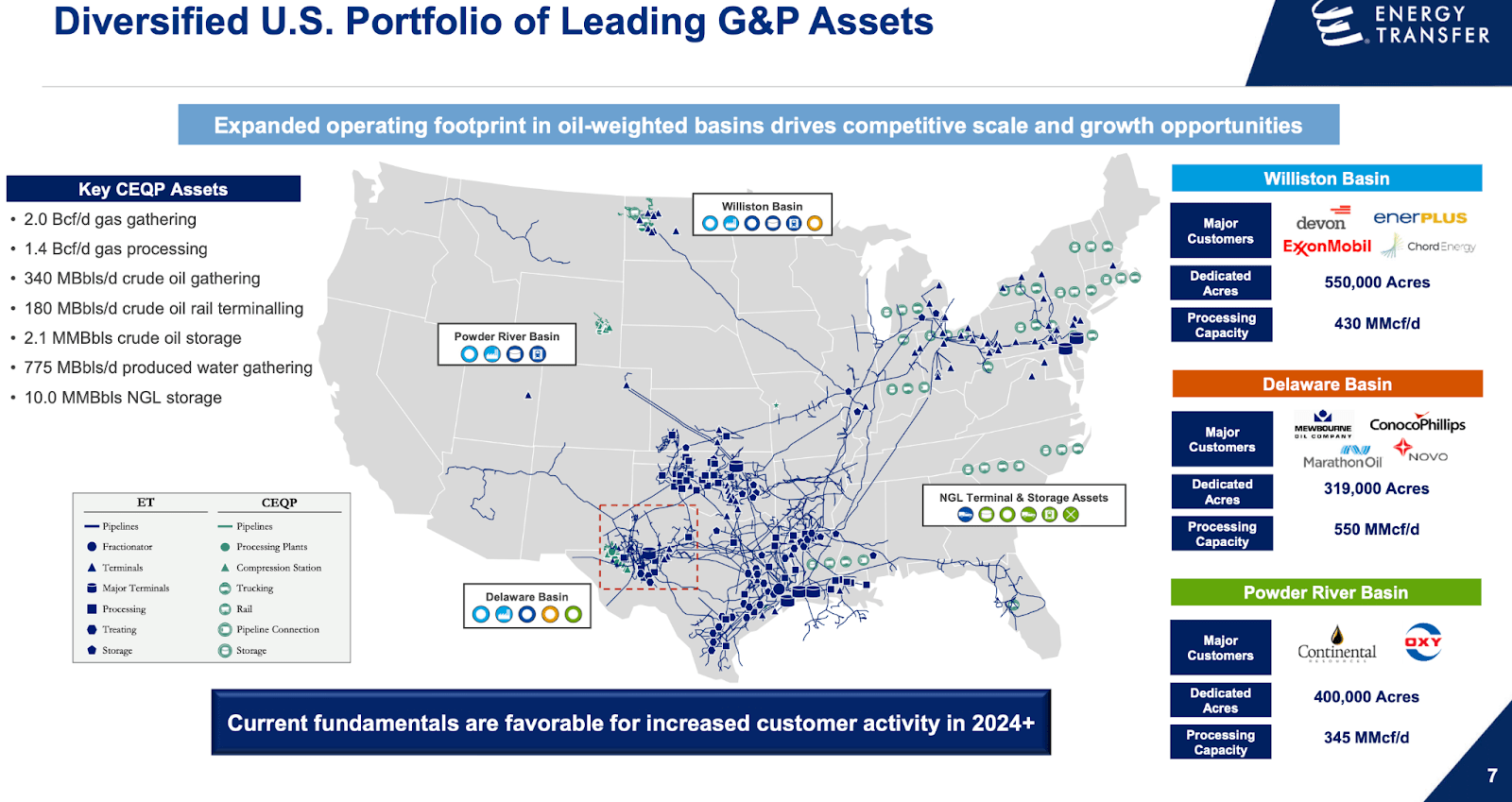

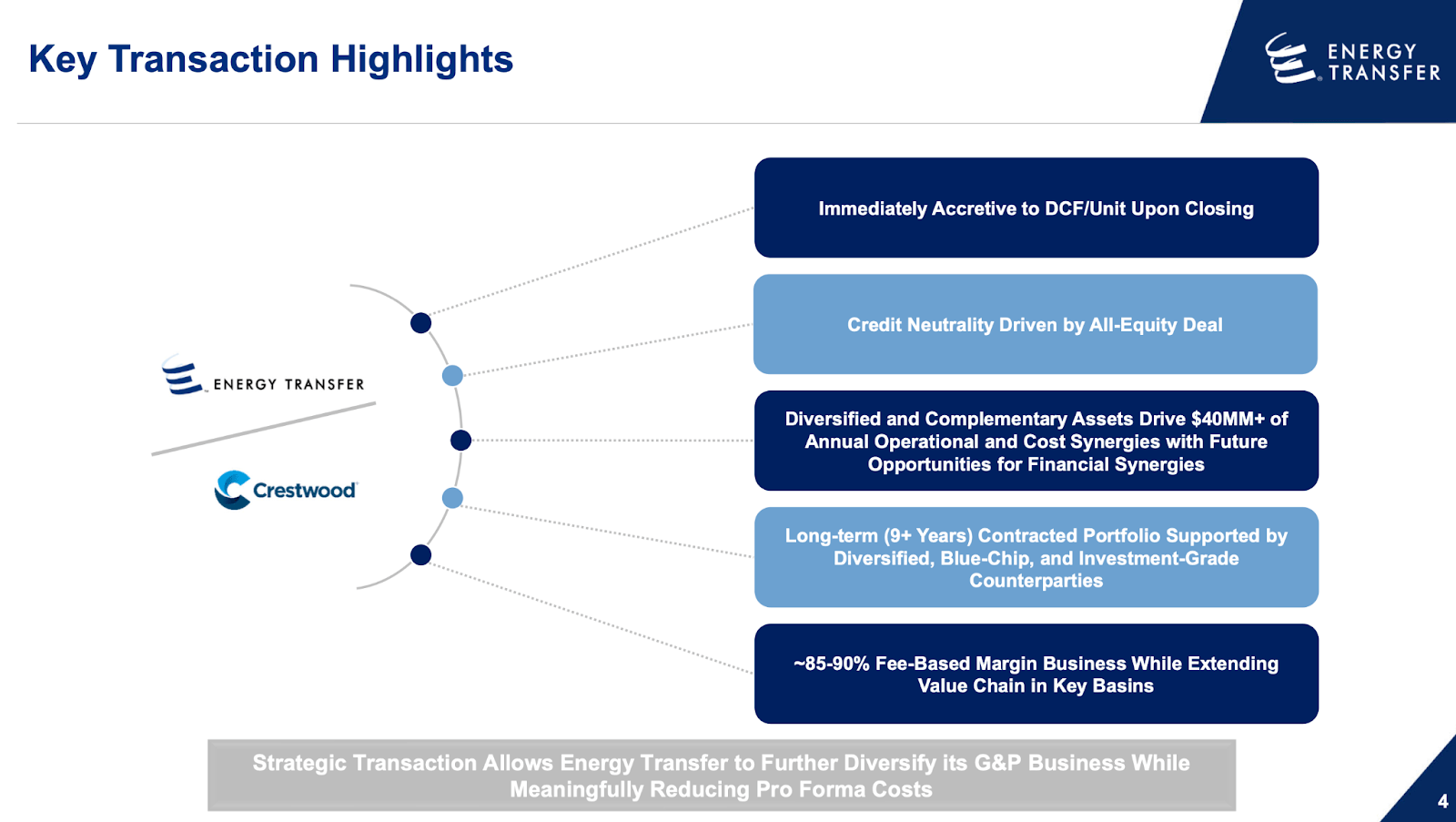

On the call, management stated that they did not have "intentions of going back above from a leverage standpoint." That is good to hear, but then they also stated that they believe that they have "a great currency to be able to work with here," referring to their units for M&A. There is a clear discrepancy here and that discrepancy has been around for a long time, as ET stock has historically traded at discounted valuations even as the company remained highly acquisitive and invested heavily in growth CapEx. That commentary foreshadowed their recent announcement that they were acquiring CEQP for $ 7.1 billion in an all-stock deal. The deal is expected to increase ET's presence in the Williston and Delaware basins among others, as well as offer significant synergy opportunities.

{kind=link}

Management has stated that this deal will be immediately accretive and neutral to their credit metrics.

{kind=link}

It is not immediately clear how management came to that conclusion. Based on their recent financial filings , I estimate CEQP's debt to EBITDA ratio to stand at around 5.4x, whereas ET's debt to EBITDA ratio stood at around 4.5x (based on 2022 adjusted EBITDA and including preferred stock) and management had guided for it to hover near 4x by the end of this year. In terms of valuation, CEQP was trading at a notable premium to ET, trading near 9x EV/EBITDA versus 7.8x at ET. And again, we must ask the question, with the stock trading at 6.7x free cash flow, why is management taking on additional execution risk here?

Is ET Stock A Buy, Sell, or Hold?

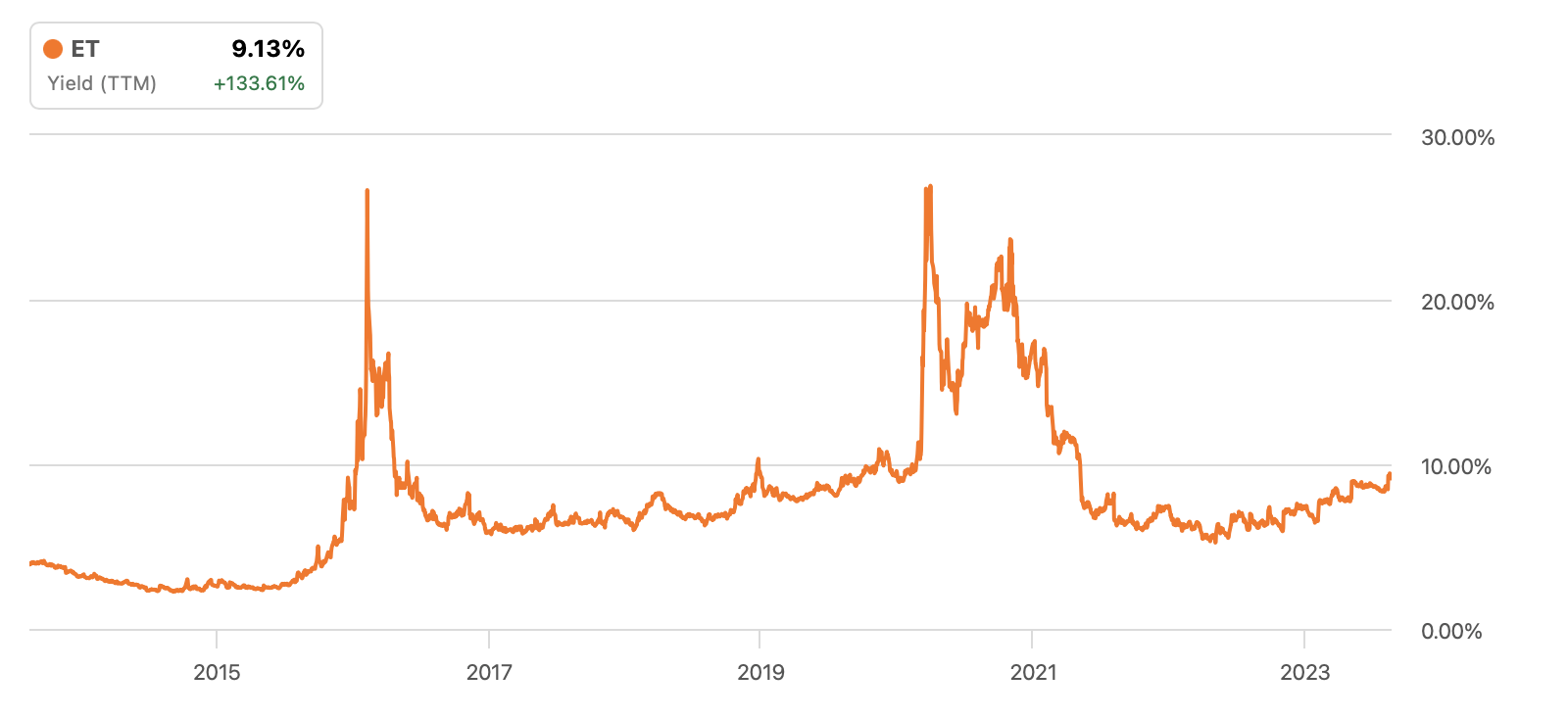

As of recent prices, ET was trading close to a double-digit distribution yield, its highest yield over the past decade (excluding the 2016 and pandemic crashes).

{kind=link}

Investors might be tempted to buy ET over EPD given that the latter is yielding "only" 7.5%, but this would be a mistake in my view. As I discussed in my deep dive on EPD, the company has historically maintained one of the more conservatively managed balance sheets in the sector and has recently earned a credit rating upgrade to A- due to their commitment to a lower leverage ratio. In contrast, the higher debt load at ET may pose significant headwinds over the coming years as it seeks to refinance maturing debt. We can see below that ET has a sizable amount of debt maturing in the near term.

2022 10-K

I have previously analyzed the elevated im pairment costs at ET and those concerns remain ever-relevant given this announced acquisition.

I now aim to answer the question asked many times in this report: why does management constantly forgo buying back their ultra-cheap units in favor of growth CapEx or M&A? The answer is revealed in an analysis of their bonus compensation structure as described in their annual filings :

For each calendar year or any other period designated by the Energy Transfer Compensation Committee (the "Performance Period"), the Energy Transfer Compensation Committee will evaluate and determine an overall funded cash bonus pool based on achievement of (i) an internal Adjusted EBITDA target ("Adjusted EBITDA Target"), (ii) an internal distributable cash flow target ("DCF Target") and (iii) performance of each department compared to the applicable departmental budget ("Departmental Budget Target")...The performance criteria are weighted 60% on the achievement of the Adjusted EBITDA Target, 20% on the achievement of the DCF Target and 20% on the achievement of the Departmental Budget Target (collectively, "Budget Targets").

Notice how management is highly incentivized to grow the business through growth CapEx and M&A, even if it is not accretive to unitholders or leads to strong unitholder returns. In contrast, EPD's bonus compensation structure is based on per unit metrics as well as total returns (emphasis by author).

This general consideration takes into account a number of our financial measures, including cash flow from operating activities per unit , distributable cash flow per unit , gross operating margin, return on invested capital , and our 3-year and 5-year equity total return performance relative to peers .

Now we return to the question of valuation. Are these risks priced in at this point, given that ET is yielding 9.5% and trades at 6.7x free cash flow versus EPD which trades at a 7.5% yield and around 11x free cash flow? First, I must point out that the distribution yield should be preferred over free cash flow in determining valuation due to the reliance on growth CapEx to drive distribution growth. As stated earlier, ET had cut its distribution in 2020 during the pandemic. EPD has 25 consecutive years of growing its distribution. With both firms targeting 3% to 5% distribution growth moving forward, my pessimistic take is that ET unitholders should ignore the excess cash flow as management seems more likely to put that cash flow towards M&A or more growth CapEx, without clear indication that it'll accelerate their distribution growth prospects. To substantiate that thought, consider that ET has historically had one of the most aggressive growth CapEx programs in the sector, yet its distribution growth over the long term still leaves much to be desired.

It is easy to see scenarios where EPD trades up to a 6.5% dividend yield or even lower, given its A- balance sheet and excellent track record. On the other hand, it is easy to see ET continuing to trade at elevated distribution yields due to the elevated debt as well as history of worse execution. I'd argue that ET deserves to trade with a substantial risk premium relative to EPD. Even if we are targeting some multiple expansion upside for ET, perhaps targeting a 7.5% distribution yield, that must imply that EPD re-values higher as well. If ET were to trade at a 7.5% yield, then I'd expect EPD to trade at around a 5.5% to 6% yield. I am bullish on EPD but even I find it unlikely for the stock to reach such a low dividend yield. But more importantly, those targets suggest that EPD is offering around the same multiple expansion upside in spite of trading at a lower distribution yield. That further means that the main difference between the two is just the 2% differential between the yields. That might still be enough for some to justify owning ET, but in my view that excess yield is not enough to compensate for the higher risk profile of the stock. I see a path for EPD to deliver 12% to 15% annual returns moving forward and I have high confidence in that outlook. For me to buy ET, I'd need more than a 2% greater potential annual returns to justify the higher risk. I reiterate my neutral rating for ET and would not upgrade that rating unless it traded at a larger discount to EPD.

For further details see:

Energy Transfer And Enterprise Products Offer High Yields, But Only One Is A Buy