ET - Energy Transfer Back To Distribution Growth And Yields 9.88%

2023-05-12 09:00:00 ET

Summary

- Management has delivered on its promises by increasing its distribution back to its previous levels and has now implemented 3-5% of annual growth going forward.

- Energy Transfer has repaid over $4 billion of its total debt since 2020 while acquiring Enable Midstream and Lotus Midstream, making its company stronger in the process.

- Energy Transfer still trades at a significant discount to its peers, and I believe their fair value is roughly $20.93, which would mean there is around 70% in appreciation on the table.

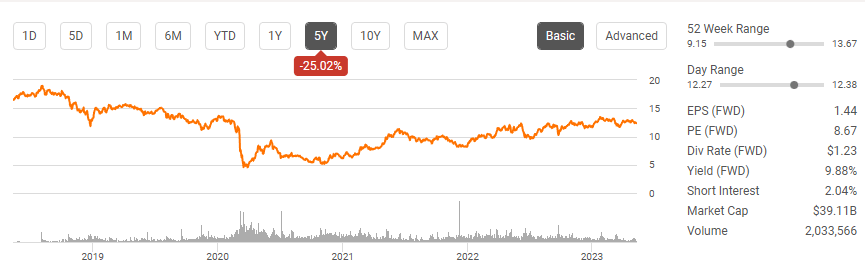

Energy Transfer (ET) has been unloved by Mr. Market for too long. Over the previous 5 years, units of ET have declined -25.02%, and they are off the 5-year highs by roughly -34.73%. Of the major U.S energy infrastructure companies, ET produces the most revenue, Adjusted EBITDA, and distributable cash flow ((DCF)) on a trailing twelve-month ((TTM)) basis, yet units trade at a significant discount to its peers on a DCF to market cap, Adjusted EBITDA to market cap, and enterprise value ((EV)) to adjusted EBITDA methodology. Regardless of what the critiques about ET were over the years, it's undeniable that management has accomplished what it set out to do. ET has reduced debt, restored the distribution to its previous level, grown through acquisitions, and implemented a forward distribution growth plan. Putting aside personal feelings about the viability of traditional energy sources, oil and gas are here to stay for at least several decades, and energy infrastructure is a focal point of the world economy. I am shocked that units of ET are selling off after earnings, and I believe that units of ET are a great way to generate high-yielding income with the prospects of producing capital appreciation. I think fair value is at least $20.93 per unit for ET, and units will continue to grind higher to their 5-year highs.

{kind=link}

Big news on the distribution front which every unit holder should be excited about

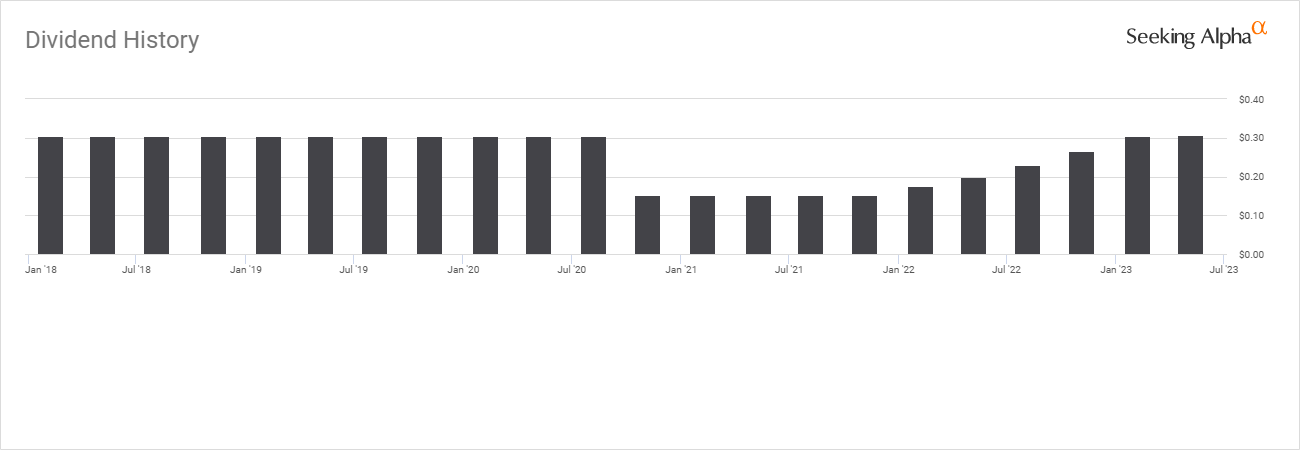

Leading up to the Q3 earnings report, ET made the decision to reduce its distribution by 50%. On the Q3 2020 conference call , Tom Long indicated that this reduction would generate approximately $1.7 billion of additional cash flow on an annual basis, and the decision was critical for the future of its business. This was a proactive decision that left unitholders divided, as many saw ET as a vehicle to deliver large amounts of yield within their portfolio. The distribution cut was explained as a way for ET to accelerate debt reduction and focus on a leverage target between 4 - 4.5x. During the call, Mr. Long stated that once ET was in a better position, management would reassess the capital allocation program and look to return additional capital to shareholders in the form of unit buybacks and distribution increases. A reduction in capital allocation to investors in the form of distributions or dividends is one of the last things anyone wants to hear. Some had speculated that the talking points were not to be trusted and there were many negative comments left on my ET articles about the situation. In my article on 11/17/20 ( can be read here ), I discussed the situation and indicated that I was disappointed but understaff why management had made this decision. About 2 ½ years later, ET has made good on their promises and went a step further.

{kind=link}

On 4/26/23, ET delivered critical news regarding its distribution. ET had suffered 5 consecutive quarters with a distribution that was 50% lower than its previous quarterly payments. From the Q1 2022 distribution to the Q1 2023 distribution, ET provided 5 consecutive increases, bringing the distribution back to previous levels. ET announced that the Q2 2023 distribution would be $0.3075, which was a slight increase from the $0.305 distribution in Q1. While management stayed true to their plan and rebuilt the distribution over a 2 ½ year period, they are rewarding patient shareholders. Management was clear that while they cannot guarantee future performance, they are targeting a 3% to 5% annual distribution growth rate.

This is exciting because ET now looks like a distribution growth company. If I use a 3% growth rate which is at the low end of management's projection, ET's annualized distribution would grow from $1.22 at the end of 2022 to $1.37 going into 2025. If I apply the midpoint at 4%, the distribution will grow to $1.43 going into 2025. In Q1 of 2023, ET generated $2 billion in DCF attributable to partners of ET, of which $967 million is earmarked for distributions. ET has a distribution payout ratio of 48.12% from its DCF in Q1 which means there is significant room for management to follow through on its 3-5% projections of annual distribution growth. ET has come a long way in a short period and went from a company that cut the distribution by 50%, to a company that has restored the distribution in full with annual distribution growth going forward.

| Year |

| Distribution |

| % Growth Rate |

| Distribution Growth |

| 2022 |

| $1.22 |

| 3.00% |

| $0.0366 |

| 2023 |

| $1.26 |

| 3.00% |

| $0.0377 |

| 2024 |

| $1.29 |

| 3.00% |

| $0.0388 |

| 2025 |

| $1.33 |

| 3.00% |

| $0.0400 |

| 2025 |

| $1.37 |

| Year |

| Distribution |

| % Growth Rate |

| Distribution Growth |

| 2022 |

| $1.22 |

| 4.00% |

| $0.0488 |

| 2023 |

| $1.27 |

| 4.00% |

| $0.0508 |

| 2024 |

| $1.32 |

| 4.00% |

| $0.0528 |

| 2025 |

| $1.37 |

| 4.00% |

| $0.0549 |

| 2025 |

| $1.43 |

ET continues to deliver for its unitholders in 2023

When I compare ET to its peers, I look at Enterprise Products Partners ( EPD ), Kinder Morgan ( KMI ), Williams Companies ( WMB ), MPLX Corporation ( MPLX ), ONEOK ( OKE ), Plains All American ( PAA ), Targa Resources Corporation ( TRGP ), and Magellan Midstream Partners ( MMP ). ET has grown into the largest energy infrastructure company in the U.S. as it generates the largest amount of revenue, Adjusted EBITDA, and DCF, while having the largest pipeline network from its peer group. WMB and OKE do not report DCF, and that is why I left those cells as $0.

| Pipeline Miles |

| Revenue |

| Adjusted EBITDA |

| Distributable Cash Flow |

| ET |

| 120,000.00 |

| $88,380,000,000.00 |

| $13,186,000,000.00 |

| $8,745,000,000.00 |

| EPD |

| 50,000.00 |

| $57,622,000,000.00 |

| $9,373,000,000.00 |

| $7,852,000,000.00 |

| KMI |

| 82,000.00 |

| $18,795,000,000.00 |

| $7,545,000,000.00 |

| $4,889,000,000.00 |

| WMB |

| 30,000.00 |

| $11,209,000,000.00 |

| $6,702,000,000.00 |

| $0.00 |

| MPLX |

| 16,000.00 |

| $11,187,000,000.00 |

| $5,901,000,000.00 |

| $5,039,000,000.00 |

| OKE |

| 40,000.00 |

| $21,462,900,000.00 |

| $4,472,800,000.00 |

| $0.00 |

| PAA |

| 18,300.00 |

| $55,989,000,000.00 |

| $2,997,000,000.00 |

| $1,854,000,000.00 |

| TRGP |

| 28,600.00 |

| $20,491,200,000.00 |

| $3,216,000,000.00 |

| $2,513,200,000.00 |

| MMP |

| 13,000.00 |

| $3,395,400,000.00 |

| $1,479,100,000.00 |

| $1,175,400,000.00 |

In Q1 2023 , ET recognized incremental increases across its business segments as NGL fractionation volumes increased 18%, NGL Transportation volume increased 13%, midstream gathering increased 14%, Intrastate transportation increased 5%, interstate transportation increased 11%, and crude transportation increased 6%. This is a testament to energy consumption continuing to increase. These volume increases led to ET delivering $1.11 billion in net income attributable to ET partners, $2.01 billion in DCF, and $3.43 billion in adjusted EBITDA. ET redeemed $2.15 billion aggregate principal amount of its senior notes and reduced its long-term debt by approximately $1.0 billion. This has led to ET reducing its total debt by -8.98% (-$4.31 billion) from $52.33 billion to $48.02 billion since the close of 2020. While reducing its debt load by -8.98%, ET has acquired Enable Midstream, and Lotus Midstream, which should lead to enhanced synergies and more opportunities to drive adjusted EBITDA and DCF in the future.

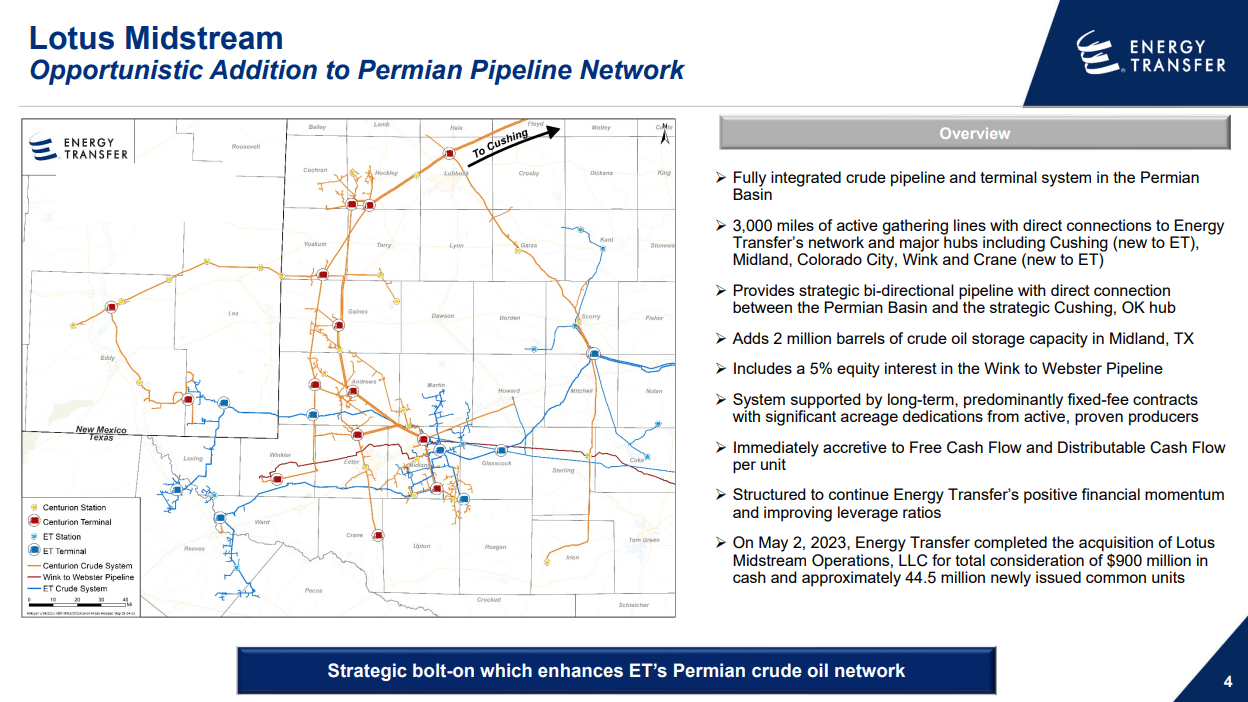

ET has officially completed its acquisition of Lotus Midstream for f $900 million in cash and approximately 44.5 million common units. This adds 3,000 miles of crude oil gathering and transportation pipelines that extend from Southeast New Mexico across the Permian Basin of West Texas to Cushing, Oklahoma. ET is working on integrating Lotus's assets into its network and constructing a 30-mile pipeline, and conducting a terminal optimization project that is expected to enhance connectivity within the Permian Basin and provide a direct link between Midland and Cushing. This has allowed ET to provide additional guidance for 2023 and is now projecting they will generate between $13.05 billion and $13.45 billion in adjusted EBITDA, which is up from its previous range of $12.9 billion to $13.3 billion.

{kind=link}

Why I want to be invested in Energy Transfer for the long-haul

I believe further consolidation will occur within the energy infrastructure space, and we will see larger companies continue to make acquisitions. The energy sector, specifically energy infrastructure, is one of, if not the most heavily regulated sector in the U.S. People aren't raising money to start new pipeline companies as the barriers to entry are treacherous. You can't just decide to build a pipeline out of thin air. You need to acquire the land, get zoning permits, get approvals from FERC, conduct environmental studies, map out connectivity, deal with local ordinances, and get engineering plans approved for starters. With a lack of new competitors entering the space, I believe the larger companies will continue to grow and become the winners that take the most in the industry.

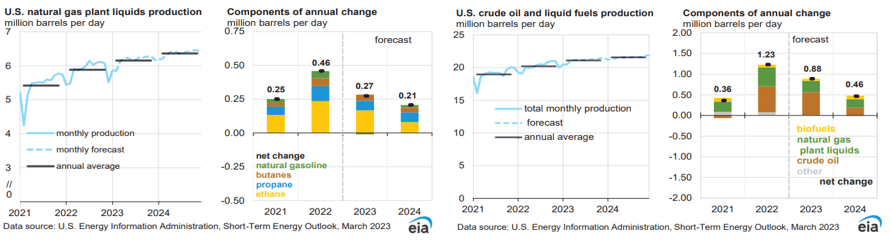

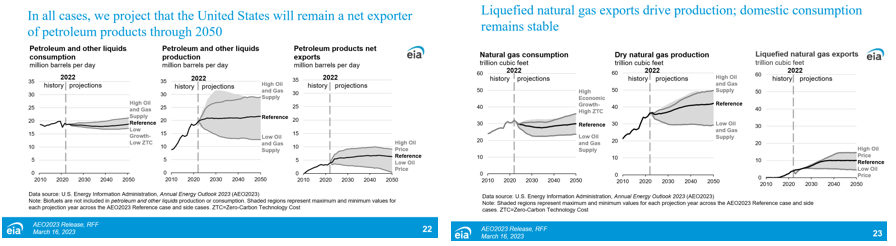

There are two critical reports that the EIA publishes, which include the International Energy Outlook (published every two years) and the Annual Energy Outlook . The Short-Term Energy Outlook from the EIA is clearly indicating that U.S crude oil and liquid fuel production, in addition to natural gas production, will increase over the next two years. The reference case in the Annual Energy Outlook from the EIA projects that petroleum and other liquid production will slightly increase from now through 2050, and dry natural gas production will increase by roughly 20% through 2050. The EIA is also projecting that the United States will remain a net exporter of petroleum products and liquified natural gas ((LNG)) through 2050. The equation is simple, the more fossil fuels are produced, the need for transportation, storage, and refining will increase, and midstream operators will continue to see elevated needs for their services.

I like businesses that have moats, and ET has a large moat around it which is enhanced by the barriers to entry. We're going to need oil and gas for decades to come, and I don't see a situation where this changes. I think that ET will benefit from a growing demand for energy which will lead to increased contracted volume across its network, which will lead to additional revenue, adjusted EBITDA, and DCF.

{kind=link}

{kind=link}

Energy Transfer still looks drastically undervalued and I believe fair value is around $20.93

Q1 2023 earnings is winding down, and I have updated all of my numbers. For those of you who are new to how I compare valuations in the energy infrastructure sector, I track the market cap, enterprise value, revenue, Adjusted EBITDA, distributable cash flow, and total debt. I compare ET to its peer group across the following ratios, Adjusted EBITDA to market cap, EV to Adjusted EBITDA, DCF to Market Cap, Debt to Adjusted EBITDA, Price to Sales, and dividend yield. The peer group is the same as my pipeline comparison earlier:

- Enterprise Products Partners ( EPD )

- MPLX LP ( MPLX )

- Kinder Morgan ( KMI )

- Plains All American Pipeline ( PAA )

- Williams Companies ( WMB )

- Targa Resources ( TRGP )

- Magellan Midstream Partners ( MMP )

- ONEOK ( OKE )

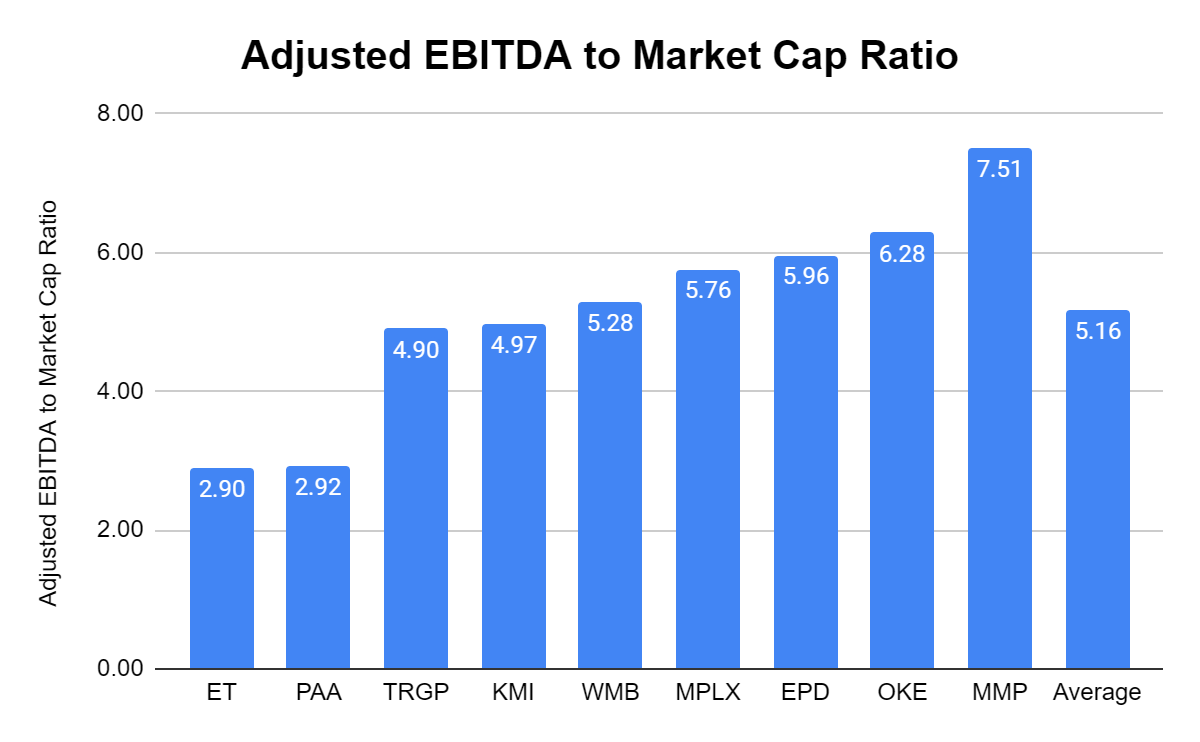

ET trades at an Adjusted EBITDA to market cap ratio of 2.9x compared to the peer group average of 5.16x. ET is not given the premium on their Adjusted EBITDA that their peers are, yet ET generated $13.19 billion of Adjusted EBITDA in the TTM, and the next largest amount came from EPD with $9.37 billion . By this metric ET looks undervalued.

{kind=link}

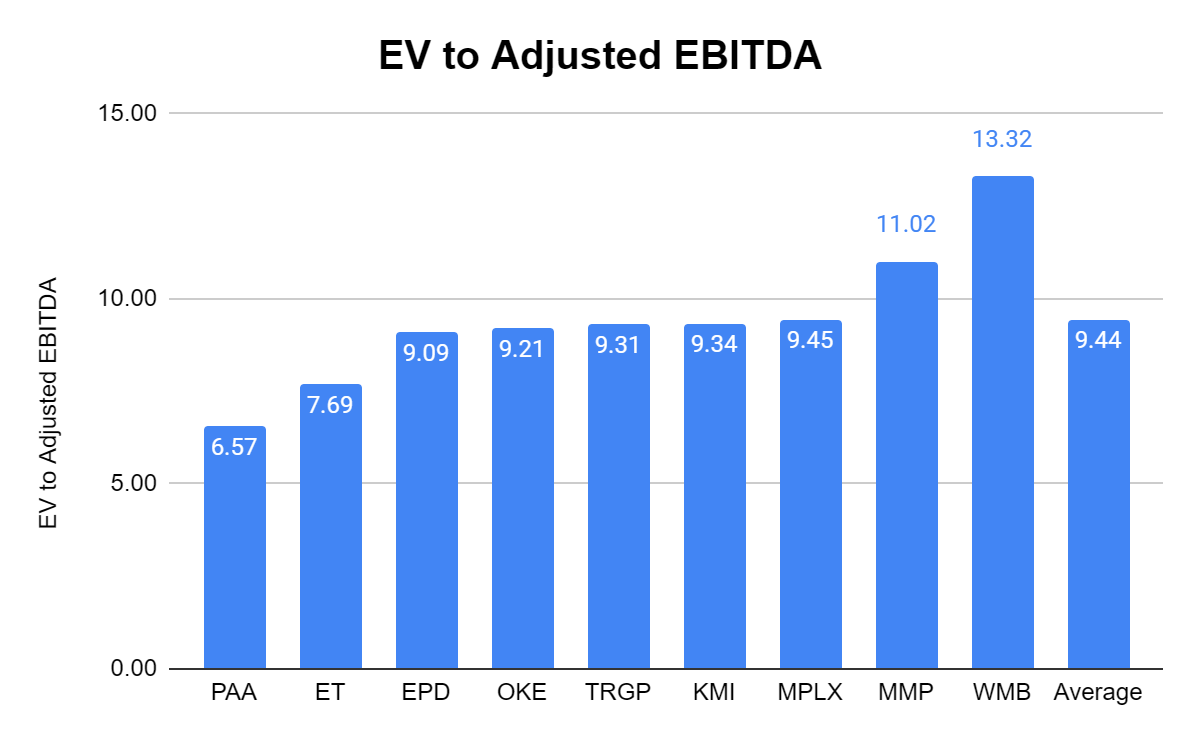

The EV to Adjusted EBITDA ratio is popular because it compares the value of a company, debt included, to the company's cash earnings less non-cash expenses. ET has the second lowest EV to Adjusted EBITDA ratio at 7.69x, which is significantly lower than the peer group average of 9.44x. ET also looks significantly undervalued by this metric as well.

{kind=link}

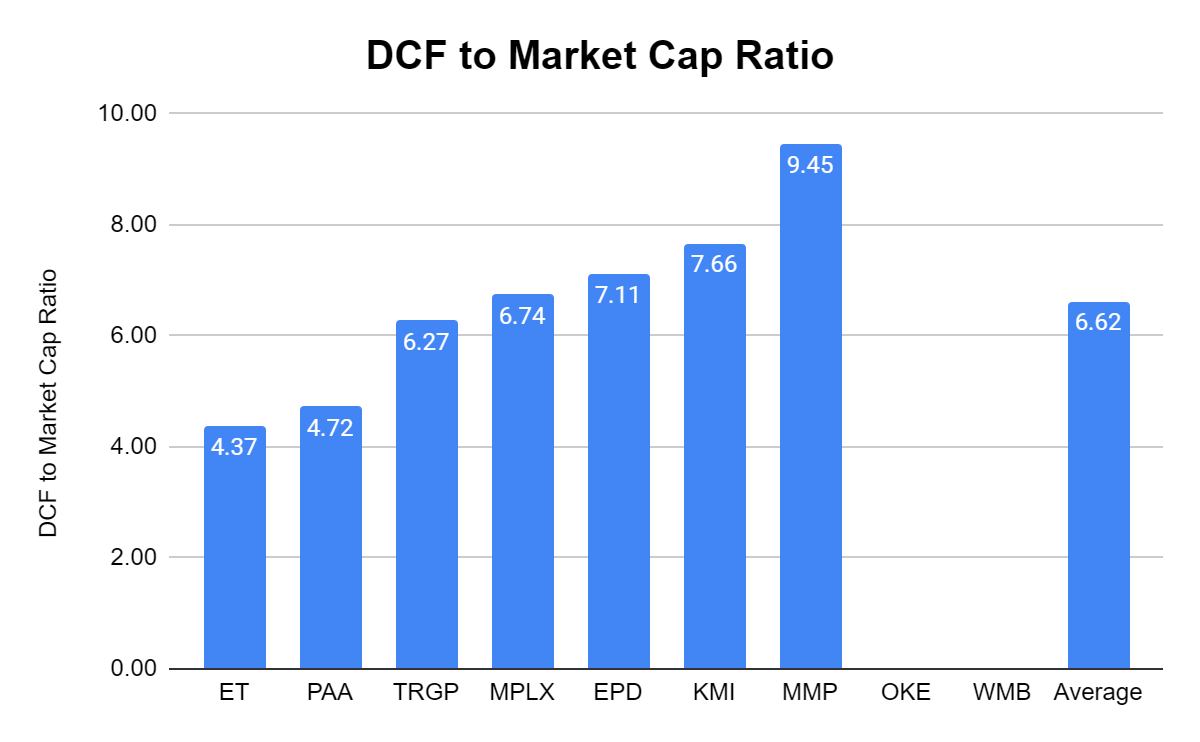

DCF is the lifeblood for investors of energy infrastructure companies as this is where distributions are paid from and how capital growth projects are funded. I want to pay the lowest multiple I can for a company's DCF. WMB and OKE don't provide the DCF in their reports, so they are excluded from this metric. ET has the lowest DCF to market cap ratio of 4.37x. Compared to its peer group average of 6.62x, ET looks inexpensive. ET generates $8.75 billion of DCF attributable to its partners, and the market continues to discount its market cap on this metric.

{kind=link}

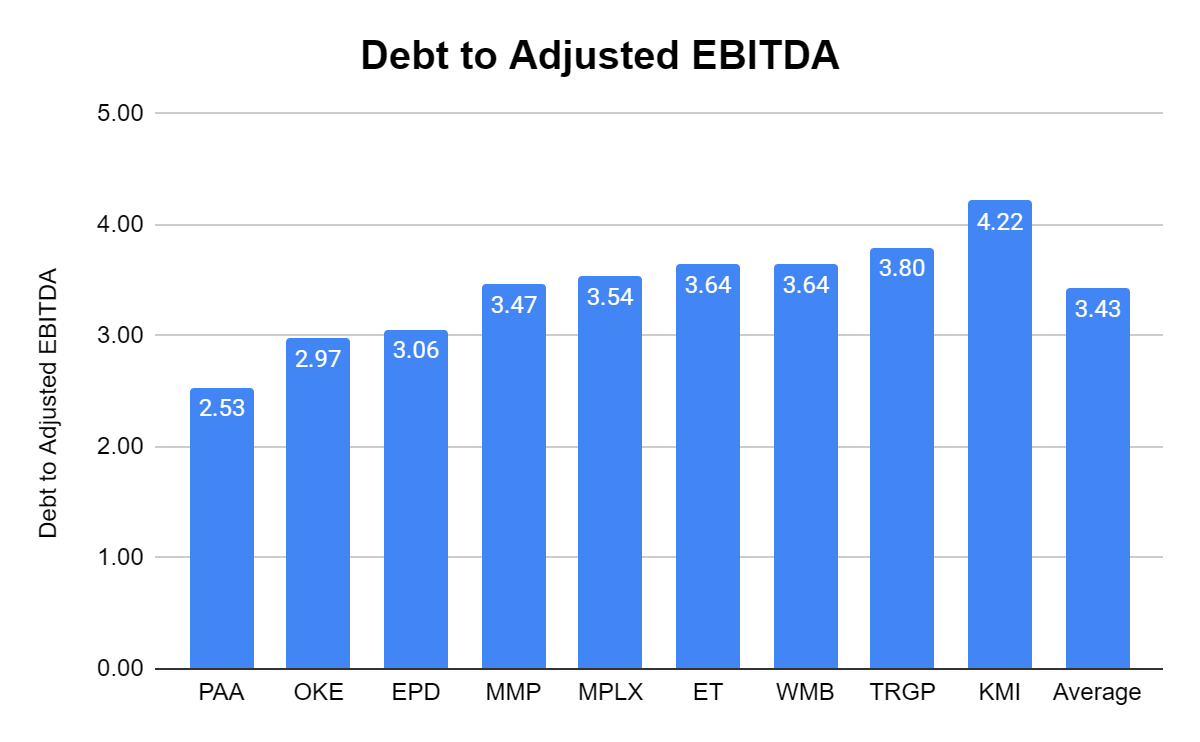

For years readers had left comments about ET's debt level. It's rare to find companies with $0 of debt, and it's important to look at a company's debt profile and their ability to facilitate debt. ET has a debt to Adjusted EBITDA ratio of 3.64x, which is slightly above the peer group average of 3.43x. There is nothing abnormal about this level as ET is in the middle of the pack, and the lowest ratio is 2.53x. Due to ET being in line with its peers and the amount of Adjusted EBITDA and DCF it produces, I am not concerned about ET meeting its debt obligations.

{kind=link}

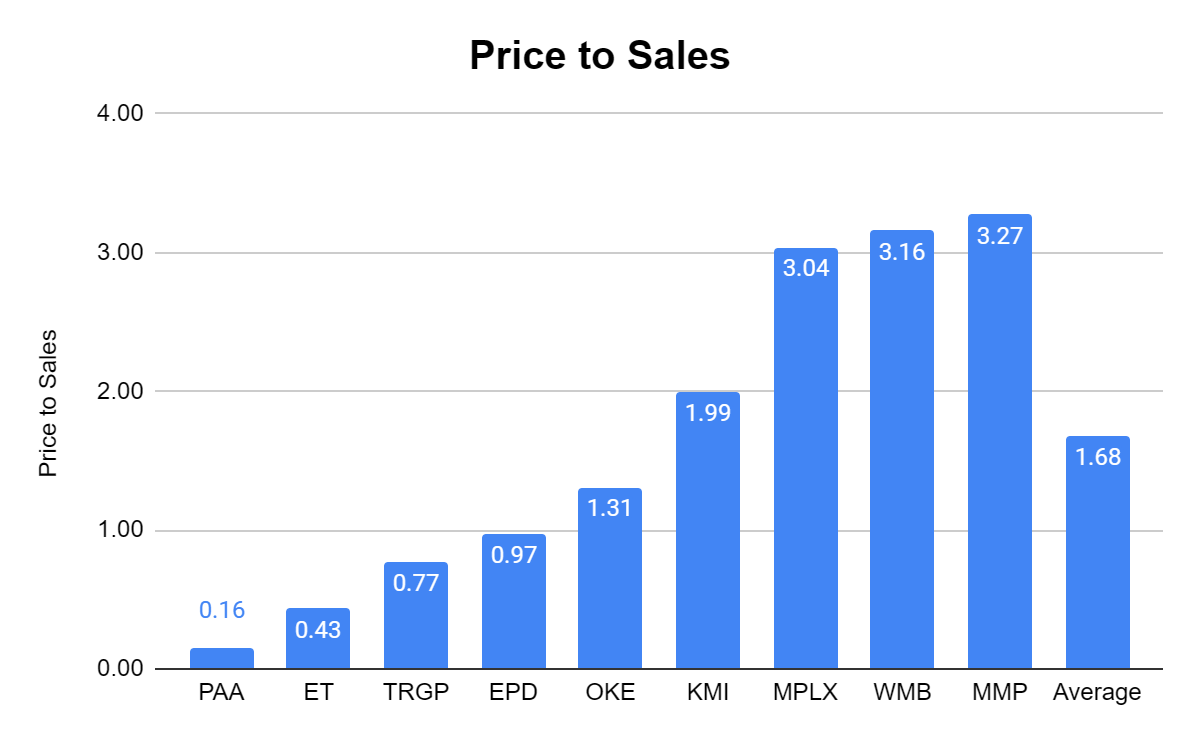

The P/S ratio isn't normally used, but sometimes I like to look at. In contrast, I would much rather value companies based on profitability; it's interesting how this group lines up on the P/S methodology. The peer group average is a P/S of 1.68x, with MPLX, WMB, and MMP trading above a P/S of 3. ET doesn't even trade at $0.50 on the dollar when it comes to P/S, as they have a P/S of 0.43. This makes ET look very undervalued.

{kind=link}

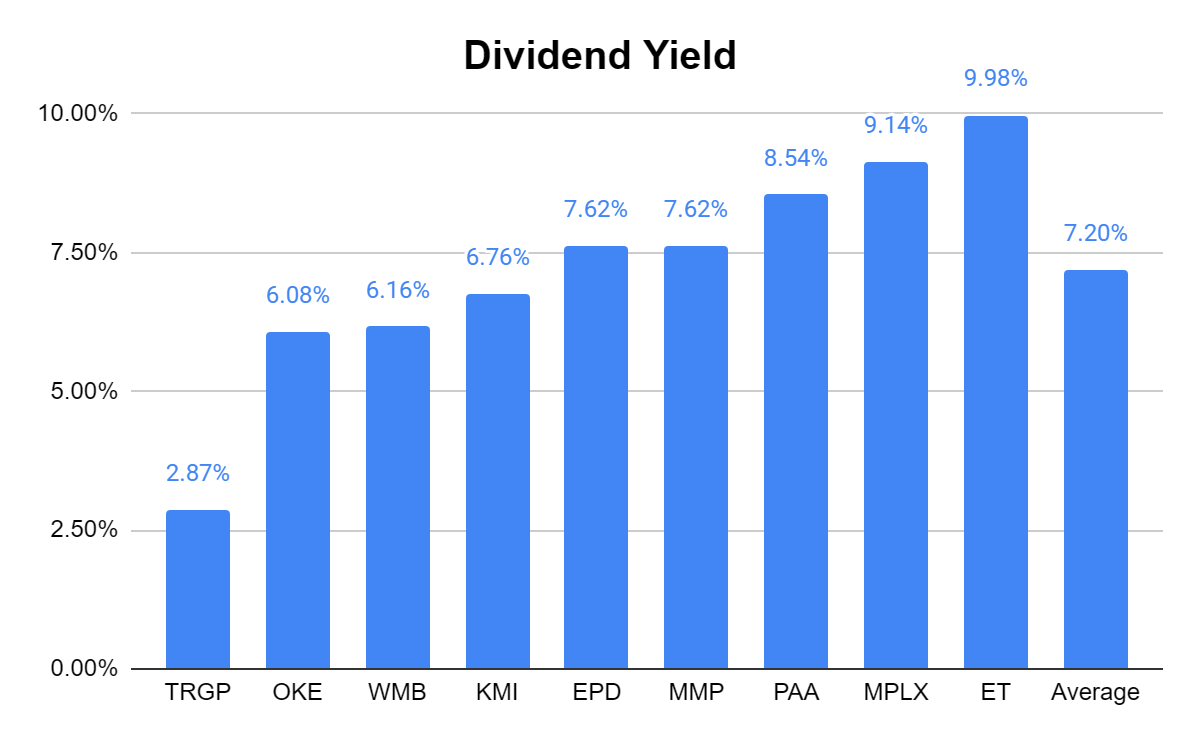

While ET looks undervalued by the metrics I look at, they also have the largest distribution yield in the peer group. ET has a dividend yield of 9.98% compared to the peer group average of 7.2%. As ET is back to becoming a distribution growth company, this is a yield that is hard to pass up as management is planning on 3-5% annual increases to its distributions.

{kind=link}

You may be wondering how I came up with such a specific fair value for ET's units of $20.93. I played around with the numbers, and if ET had a $65 billion market cap, its adjusted EBITDA to market cap ratio would increase to 4.93x compared to a 5.39x peer group average, and its DCF to market cap ratio would become 7.43x compared to a peer group average of 6.66x. While ET would be above the peer group average on the DCF to market cap ratio, ET would still have a smaller multiple on its DCF than KMI at 7.66x and MMP at 9.44x. ET would still have the third lowest adjusted EBITDA to market cap multiple at 4.93x, with WMB, MPLX, EPD, OKE, and MMP all trading over a 5x multiple. As ET generates the largest amount of DCF I feel it's fair for them to have an above-average multiple on its DCF, especially since the multiple on its Adjusted EBITDA is lower than the peer group average.

ET has a market cap of $38,198,707,408. If its market cap was to increase to $65 billion, this would be an increase of 70.16%. This would mean that units of ET would need to increase by 70.16% as well, which would add an additional $8.63 to each unit, bringing the unit price to $20.93. I don't think this is an unreasonable valuation at all, and while it may not occur, it would put ET more in line with its peer group.

Conclusion

ET is my favorite energy infrastructure company in the U.S. and I feel it's trading at a deep discount to where it should trade. ET has a lot of things going for it including its acquisitions of Enable and Lotus Midstream, paying down its debt by $4 billion, rebuilding its distribution to full capacity from the 50% reduction, and implementing a target of 3-5% future distribution growth annually. I think ET is the most undervalued energy infrastructure company, and fair value should be around $20.93. Investors can grab a yield that is 9.88% with future growth on the horizon while waiting for capital appreciation. Oil and gas aren't disappearing, and ET's infrastructure is critical to the U.S. Maybe units don't get to my fair value anytime soon, but I wouldn't be shocked if they exceed $15 over the next several months.

For further details see:

Energy Transfer Back To Distribution Growth And Yields 9.88%