ET - Energy Transfer: Buy This 9%-Yielding Partnership With Distribution Growth

2023-11-07 04:54:10 ET

Summary

- Energy Transfer’s distribution coverage ratio of 1.9 through the first nine months of 2023 is very safe.

- The MLP posted solid all-around results in the third quarter.

- Energy Transfer is also healthy from a balance sheet perspective.

- If my assumptions for the dividend/distribution discount model are any indication, units of the partnership could be priced 24% below fair value.

- Energy Transfer’s 9.2% distribution yield and even slight growth prospects could lead to annual total returns comfortably in the low-double-digits.

One of the all-time most popular sayings within the personal finance sphere is that cash is king. As I found out recently with my fortunately brief job loss, this mantra does carry an awful lot of weight.

Knowing that I had an emergency fund to fall back on at that time made it that much easier to quickly rebound and land back on my feet. This life event was quite a wake-up call to me. It was so much the case that I decided to bolster my emergency fund up to nine- to 12 months of expenses (up from four months).

Yet, if cash is king, then cash flow is the supreme emperor. Before losing my job, my passive income had already covered about 25% of my monthly expenses. This is why cash flow from investments coupled with an adequate emergency fund can make your balance sheet a fortress. On a small scale, it can become the equivalent of an AAA-rated corporation like Johnson & Johnson ( JNJ ) or Microsoft ( MSFT ).

As I highlighted in an article last month , Energy Transfer ( ET ) is an anchor within my passive income portfolio. The partnership comprises 2.5% of my annual passive income, which is good enough to make it my fourth largest investment holding by passive income.

Since that time, Energy Transfer has shared its financial results for the third quarter ended September 30, 2023. Let's dig into the company's recent fundamentals and valuation to elaborate on why I still believe the MLP is still a table-pounding buy for income investors.

Distribution Coverage Remains Impressive

As most reading this are probably aware, the definition of high yield is subjective and constantly changes based on the risk-free rate. The 5% or 6% yields that used to be "high yields" just two years ago are now not particularly high versus the 10-year U.S. treasury yield of 4.7% . The current risk-free rate represents a tripling from the mere 1.5% yield of the 10-year in November 2021.

Even with the 10-year yield the highest it has been since 2007, Energy Transfer's 9.2% distribution yield clocks in at double the rate. More cautious investors would probably ask themselves the following: What's the catch? Is this a yield trap?

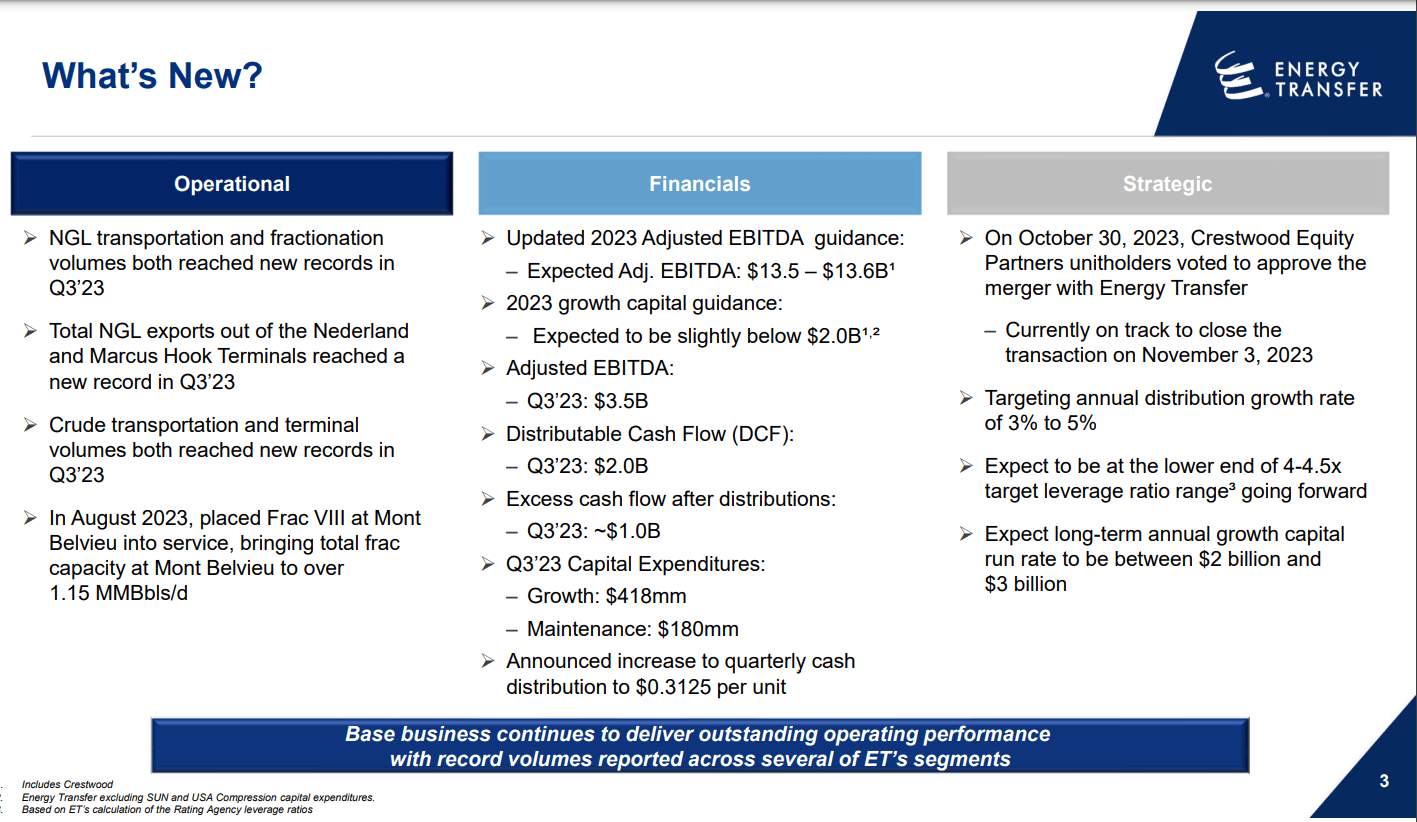

Fortunately, that is far from the case for Energy Transfer. Through the first nine months of 2023, the company has generated $5.5 billion in distributable cash flow. Against the $2.9 billion in distributions paid during that time, this equates to a distribution coverage ratio of 1.9.

As I'll further explain in the section below, this is a highly sustainable distribution obligation for Energy Transfer. That's why management is comfortable targeting 3% to 5% annual distribution growth moving forward.

Energy Transfer's Results Are What I Like From My Investments

Once again, Energy Transfer shared another quarter of encouraging financial results. The company's adjusted EBITDA surged 16.1% higher year-over-year to $3.5 billion during the third quarter. Higher interest expenses from surging interest rates couldn't hold Energy Transfer back, either: The MLP's distributable cash flow soared 25.9% over the year-ago period to $2 billion in the quarter.

{kind=link}

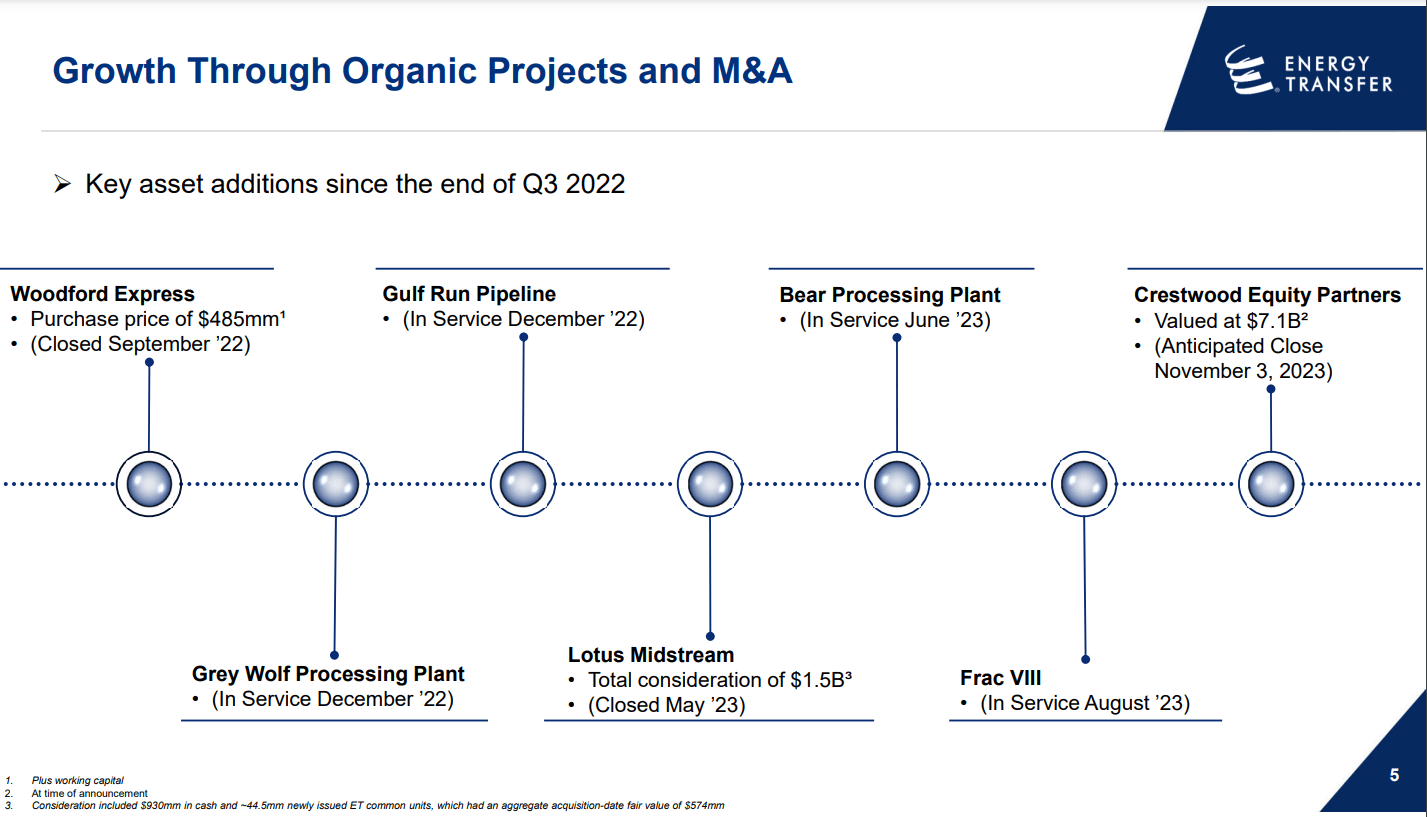

So, what was behind these respectable operating results? Well, steady demand for the company's services was one factor. Not to mention that from Sept. 30 last year through Sept. 30 of this year, Energy Transfer has closed on two acquisitions. The company also placed assets into service over that time, such as the Grey Wolf cryogenic gas processing plant and the Gulf Run natural gas pipeline. This explains how according to Co-CEO Tom Long's opening remarks during Energy Transfer's Q3 2023 earnings call , record volumes for natural gas liquids, refined products, and crude oil were transported through its infrastructure.

{kind=link}

Moving forward, the company should be able to sustain its operating momentum for a variety of reasons.

First, the partnership brought Frac VIII at Mont Belvieu into service in August. That brings Energy Transfer's total frac capacity from that asset to 1.15 million barrels a day.

Secondly, the company closed its deal for Crestwood Equity Partners just last week. This appears to be a smart deal because not only is it neutral to Energy Transfer's leverage, but it is expected to be immediately accretive to DCF per unit.

Finally, the partnership's total free cash flow after distributions was approximately $1 billion for the third quarter. After considering the nearly $600 million in growth and maintenance capex during the quarter, Energy Transfer is generating enough cash to continue repaying debt. As more of the company's projects come online and debt is repaid, its leverage ratio should easily remain at around four in the quarters ahead.

Risks To Consider

Setting operational records, Energy Transfer is a business firing on all cylinders. However, the partnership has risks investors must be comfortable with before buying.

From the last time I covered Energy Transfer, its risk profile is virtually unchanged. As I noted in my previous article, counterparty and energy transition risks remain two of the biggest risks facing the company.

There is the risk that Energy Transfer may not ultimately realize the anticipated benefits from the Crestwood acquisition. While it appears to be a match made in heaven from what I have seen, only time will tell if that plays out.

Additionally, another general risk that Energy Transfer faces is opposition from activists and the legal system toward ongoing or future projects. If there is enough litigation to gum up the works, the company may not bring projects into service on time and budget or even at all. This could weigh on Energy Transfer's growth prospects.

Finally, it's worth noting that Energy Transfer is an MLP, issuing a K-1. This comes with special tax considerations that everyone should consider before buying.

A Deeply Underappreciated Partnership

Down 2% since my last article as the S&P 500 was down a fraction of a percent, Energy Transfer has become an ever so slightly more attractive buy in the past month. Here's what my variables for the dividend discount model (or in this case, distribution discount model) imply units of the partnership are worth.

Investopedia

The first input into the DDM is the expected dividend per share or annual distribution per unit. Following Energy Transfer's 0.8% raise in its annualized distribution per unit, that amount is currently $1.25.

The second input for the DDM is the cost of capital equity. This refers to the annual total return rate that an investor seeks from their investments. I target at least 10% annual total returns.

The third and final input into the DDM is the annual distribution per unit growth rate. Given Energy Transfer's stable fundamentals, I'm reiterating my 3% annual distribution growth rate for the long run.

Using these inputs for the DDM, I arrive at a fair value per unit of $17.86. Relative to the current unit price of $13.52 (as of November 6, 2023), Energy Transfer is 24.3% undervalued and could appreciate by 32.1% upon reverting to fair value.

Summary: Energy Transfer Is A Good Business For A Great Valuation

In the business world, you're either stagnating/circling the drain or you're consistently setting operational records. Since Energy Transfer is in the latter camp, I am especially optimistic about its operating fundamentals.

The company's measured acquisition activity as of late and continued investments in growth capex also bode well for the future. Best of all, units look to be discounted by over 20% at its sub-$14 unit price.

Energy Transfer's 9.2% yield and conservative low- single-digit annual DCF/unit growth alone could deliver double-digit annual total returns through 2033. Along with the potential for a 2.8% annual valuation multiple expansion, this is precisely why I am maintaining my strong buy rating for Energy Transfer.

For further details see:

Energy Transfer: Buy This 9%-Yielding Partnership With Distribution Growth