ET - Energy Transfer: Continuing To Scale Up As An Energy Giant

2024-01-15 09:56:09 ET

Summary

- Energy Transfer is a valuable long-term investment with a valuation of almost $44 billion and a commitment to growing its infrastructure.

- The company has been expanding its footprint and developing new assets, such as a proposed offshore port and a growing NGL business.

- Energy Transfer has been making large acquisitions, including the recent acquisition of Crestwood Equity Partners, to support future shareholder returns.

Energy Transfer ( ET ) is among the largest midstream companies in the world, with a valuation of almost $44 billion. The company is also one of the most committed to growing its infrastructure, with an impressive portfolio of assets and a consistent focus on bolt-on acquisitions. As we'll see throughout this article, the company is a valuable long-term investment.

Energy Transfer Developments

The company has worked to build additional developments to continue helping its overall portfolio.

{kind=link}

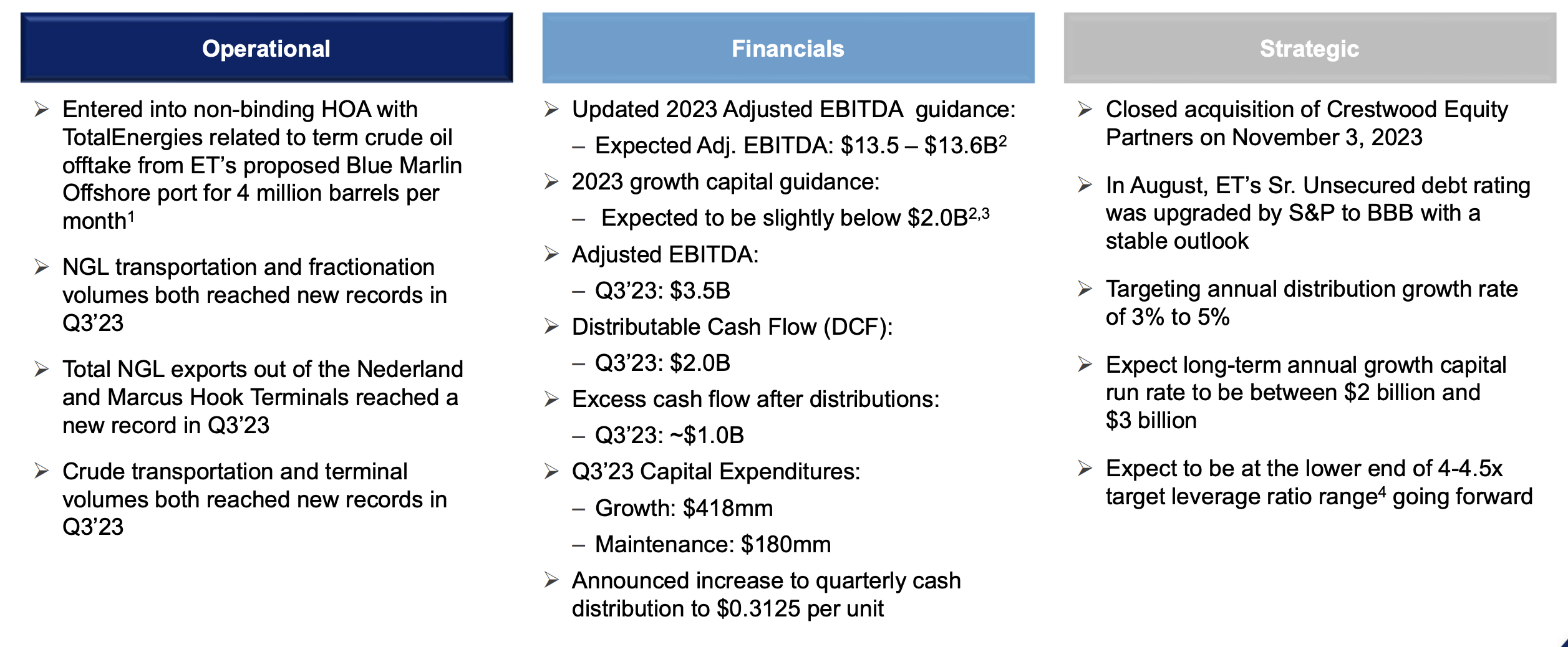

The company is proposing a new offshore port and TotalEnergies has represented interest in 4 million barrels / month. This is another example of an asset the company could build that would integrate well with its pipelines and all other assets. The company's budding NGL business has also expanded dramatically with fractionation and transportation volumes hitting records.

The company continues to hit new records for the growth rate of its asset portfolio. Financially, the company has updated its guidance to now expect $13.55 billion in EBITDA with just under $2 billion in growth capital. Adjusted EBITDA for the quarter, is expected to be more than 25% of its EBITDA showing its continued growth.

The company's DCF for the quarter was a massive $2 billion, with $1 billion after an almost 9% dividend yield. The company's capital expenditures for the quarter were $418 million growth and $180 million maintenance. Annualized that's ~$2.5 billion in total capital expenditures.

Going forward, the company continues to work to close the acquisition of Crestwood Equity Partners. It had its debt target recently upgraded, and it continues to target an annual distribution growth rate of 4%. Long run it expects annual growth capital run rate to be $2.5 billion and expects to sit at the lower end of its target leverage with which would be ~$54 billion debt.

Energy Transfer Footprint

As the company continues its expansion, its footprint continues to grow into essential infrastructure.

{kind=link}

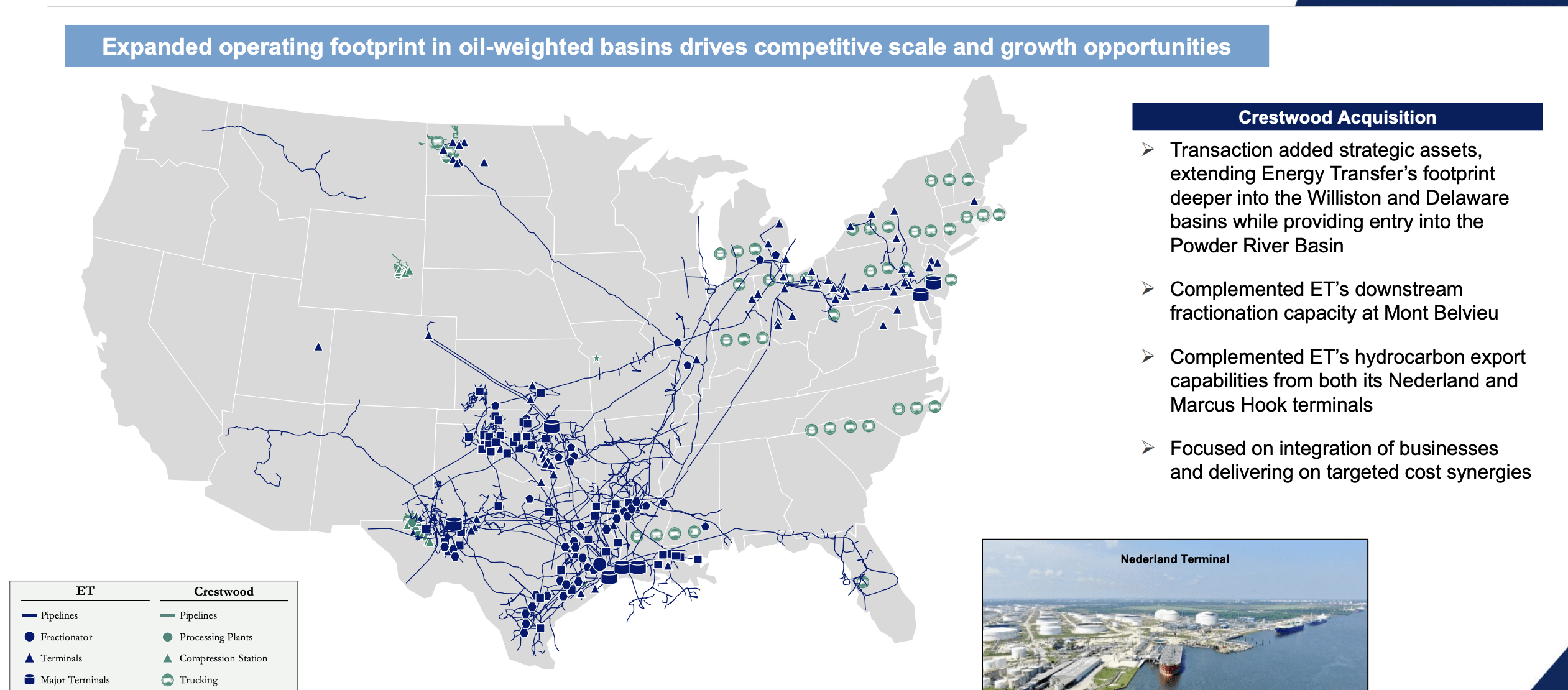

U.S. shale is the largest energy producing area in the world, and the north-east coast along with various population centers in between represent some of the largest energy consumption areas in the world. The company's massive existing footprint, along with recent acquisitions, give the company room for numerous bolt-on acquisitions.

The company has also worked to expand the overall export capacity of the United States. For example, the Netherland Terminal, additional fractionation capacity, and additional export terminals. All of that expands the addressable market for the company to earn more for every barrel moved.

Energy Transfer Acquisitions

The company has been on a bit of an acquisition spree recently to continue to expand its portfolio.

{kind=link}

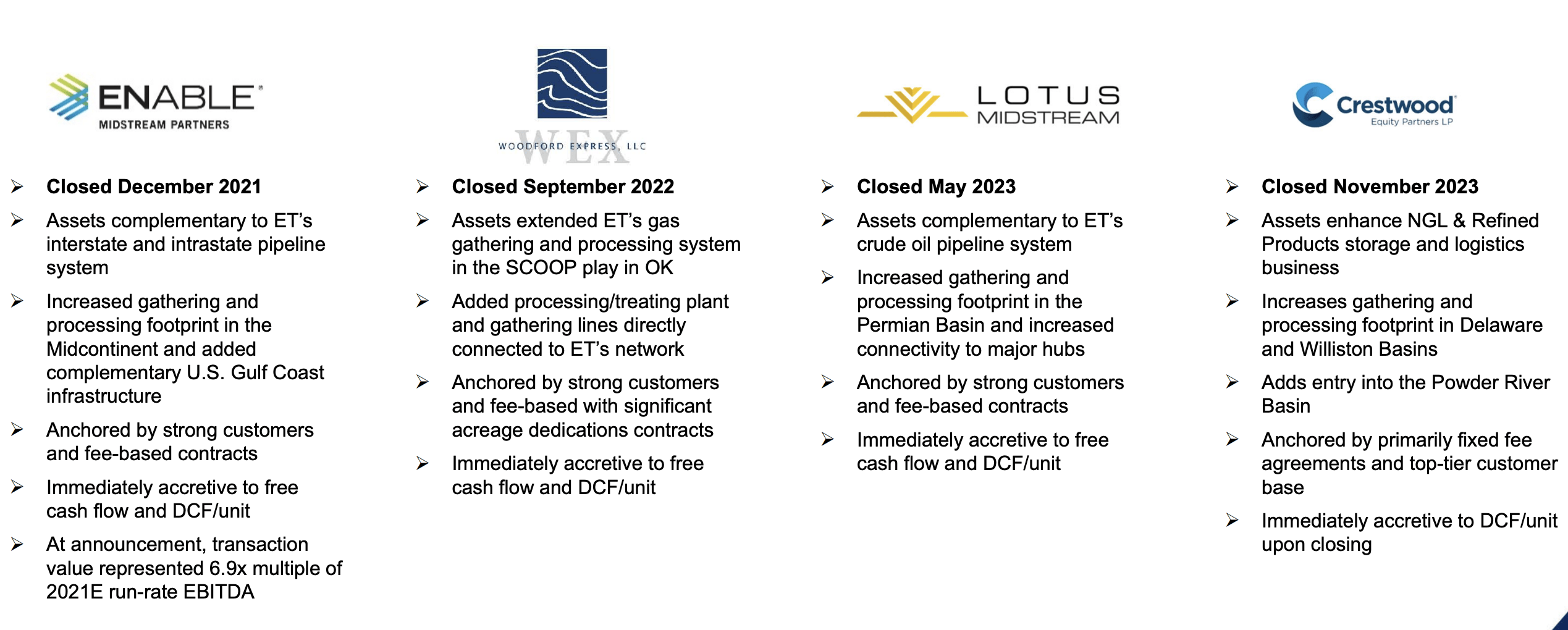

The company closed its major acquisition of Enable Midstream Partners in December 2021, and closed another acquisition Woodford Express in 2022. In 2023, the company managed to close 2 additional acquisitions. These are not small acquisitions, for a company with a valuation of almost $100 billion, the Crestwood Equity Partners acquisition alone was $7 billion.

The company is one of the few large midstream companies continuing to make large acquisitions. Those acquisitions have strong bolt-on abilities with the company's existing assets and will support future shareholder returns.

Energy Transfer Capital Allocation

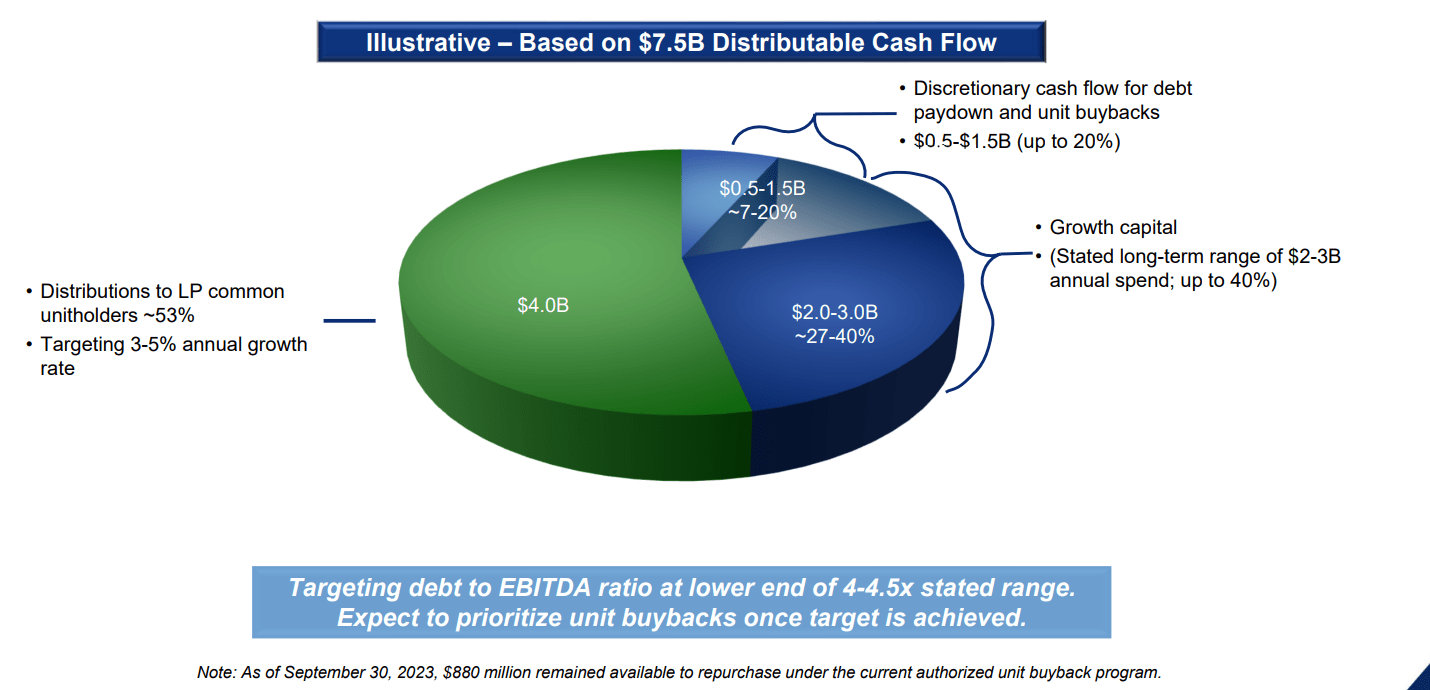

All four of the company's recent acquisitions were accretive on a DCF / unit basis and the company earned $2 billion in DCF in the most recent quarter.

{kind=link}

The company is illustrating what happens with $7.5 billion in DCF, but it's worth acknowledging that the company's current annualized run-rate for DCF is more than that. The company is currently spending roughly $4 billion on its dividend contributions. It is targeting a 4% annual growth rate, and its dividend is roughly 9%.

That makes up ~53% of the company's DCF in this case. From there, the company is planning to invest massively in its business. Its long-term capital spending for growth is expected to be ~$2.5 billion, or roughly 6% of its annual market cap, and we expect that spending to continue. That doesn't directly come to shareholders, but it does help in the long run.

That leaves the company's discretionary cash flow after all of that at $1 billion, peaking at up to 20% of the company's DCF. The company can use that for debt paydown or unit buybacks. The company is targeting debt to EBITDA at the lower end of the 4.0-4.5x range, which would be a range of $54-60 billion in debt, a massive amount more than its market cap.

At current interest rates, we'd like to see that range decreased, but the company's long-term debt is well positioned right now. We are excited to see the company's goal for share repurchases post debt reduction, and we would like to see the company accelerate that as it is able to.

Thesis Risk

The largest risk to the thesis for the company is a lack of adaptation to climate change. The company is continuing to move full steam ahead with oil and natural gas, and in the immediate term we expect the company to benefit. However, in the longer term we expect volumes to go down, and the core of the company's business, volumes, will decline.

That will hurt the company's ability to drive future shareholder returns.

Conclusion

Energy Transfer is an energy giant, one with an enterprise value of almost $100 billion. The company is committed to both continuing its growth and shareholder returns. The company has a dividend of almost 9%, one that it can comfortably afford, with just over 50% of its DCF, and one that it's committed to growing at 4% over the long-term.

That's a rate that will likely beat inflation. On top of that, the company is continuing to invest heavily in growth capital. That growth capital will fuel a DCF rate that's already almost 10% higher than the rate that's being assumed in the company's calculations. Past that, the company has cash for debt reduction and shareholder returns.

Its debt level is lofty but we'd like the company to focus a lot more on share repurchases, at its current valuation, enabling more substantial shareholder returns.

For further details see:

Energy Transfer: Continuing To Scale Up As An Energy Giant