ET - Energy Transfer: Deleveraging And Distribution Increases To Send Units Higher

- Energy Transfer units currently trade at a safe 8.3% yield.

- The current unit price is too low given ET’s prospects for leverage reduction and distribution increases.

- Our price target for ET units is $15.25, nearly 70% above the current price.

{kind=link}

Energy Transfer LP ( ET ) units currently sport a safe and attractive 8.3% distribution yield. However, investors who buy the units today can obtain a sustainable 12.7% yield once ET raises its annual distribution to management's $1.22 target. Over the next two years, we expect distribution increases toward that target will serve as catalysts to increase the unit price. When the distribution reaches $1.22, we expect its units' yield to compress to 7.5%, which would send the unit price to $16.27, nearly 70% above the current price of $9.60.

ET Management's Objectives to Benefit Unitholders

ET's leadership is a determined bunch. For all their faults as long-term stewards of shareholder capital, one thing is clear: they tend to get their way. Whether they're completing projects in the face of stiff opposition or pursuing expansionary deals - or, for that matter, abandoning them - ET management goes to great lengths to achieve its goals.

ET's management under Chairman Kelcy Warren is currently pursuing two goals, both of which we expect it to reach. First, management plans to reduce ET's leverage ratio to its target of between 4.0 and 4.5-times. Second, it intends to increase its common distribution to $1.22 annually, up from the current $0.80 distribution.

These goals are laid out in ET's April 26 press release declaring its first-quarter distribution, as shown below.

{kind=link}

ET must achieve management's first goal before it can accomplish the second. Reducing leverage takes precedence, so ET can remain in good standing with the credit rating agencies, which currently rate ET at their lowest investment-grade rating. Management clearly wants to increase ET's credit rating so that it can lower the company's cost of capital and begin increasing distributions more aggressively.

We believe management's leverage goal is within sight. In fact, we estimate that ET's leverage ratio stood at 4.6-times at the end of the first quarter, just a hair above management's 4.5-times target.

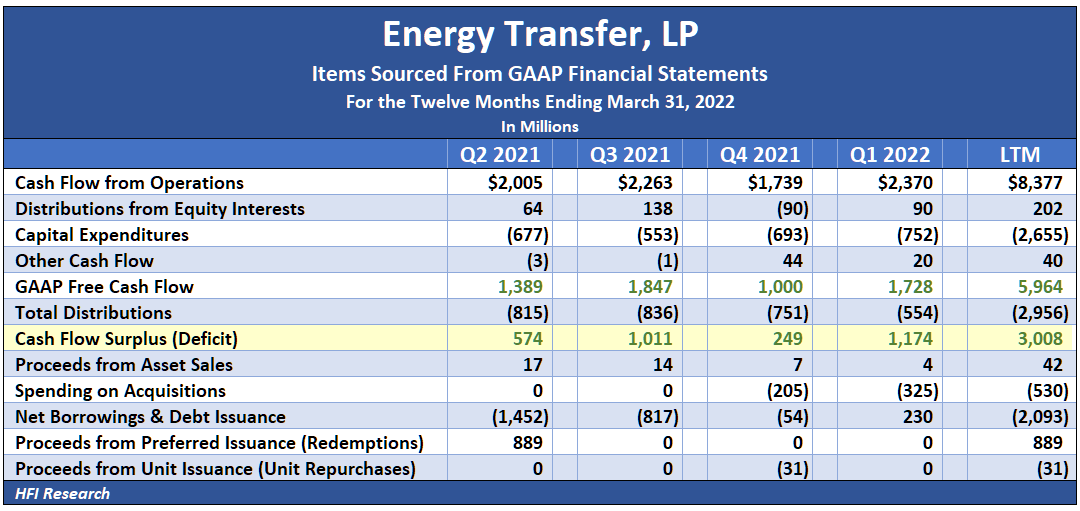

ET's financial statements make it difficult to tease out the company's organic operating and balance sheet results since ET's partially-owned subsidiaries - namely, Sunoco LP ( SUN ), USA Compression Partners ( USAC ), and the Dakota Access Pipeline ("DAPL") - are consolidated into ET's GAAP financial statements. Their results have to be stripped out of ET's consolidated accounts to arrive at a leverage ratio as calculated by the rating agencies. The following table shows our adjustments:

HFI Research

Using ET's first-quarter 2022 balance sheet and its trailing twelve months EBITDA, we estimate the company has to pay off an additional $950 million to achieve a 4.5-times leverage ratio. We believe that doing so shouldn't be a problem over the course of this year. Consider that over the past four quarters, ET generated a cash flow surplus of $3 billion.

{kind=link}

After ET's first-quarter distribution increase, it will have to pay out an additional $686 million over what it paid common unitholders in 2021. This should leave around $2.3 billion to allocate toward capital expenditures, M&A, repurchases, and/or debt paydown. This management team loves to spend on new projects and M&A, but we saw in 2001 that they're capable of prioritizing debt paydown when necessary. For example, in 2021 alone, ET paid down more than $6 billion of debt, which it partially funded with its $2.4 billion windfall from Winter Storm Uri in the first quarter.

We expect management to allocate $1 billion of ET's roughly $2.3 billion cash flow surplus to paying down debt over 2022. In light of our forecast of low-single-digit EBITDA growth in 2022, the debt paydown is likely to bring ET's leverage ratio down to management's targeted range.

Distribution Increases

We believe the odds are good that ET will reduce its leverage below management's target in 2022 and that as a result, ET will receive a credit rating upgrade. ET can then enter 2023 with lower leverage, at which point management can turn to its second goal of increasing the distribution toward $1.22.

An increase from the current annual distribution of $0.80 per unit would cost the company an additional $1.3 billion. We believe that in 2023 and 2024, ET's more than $2.5 billion cash flow surplus after an $0.80 per unit distribution leaves more than enough room to accommodate a $1.22 distribution.

Valuation

We value ET units in the range of $14.00 to $16.50. Our price target is the mid-point of our range, or $15.25. At the units' current price of $9.60, our price target implies 58.8% upside.

{kind=link}

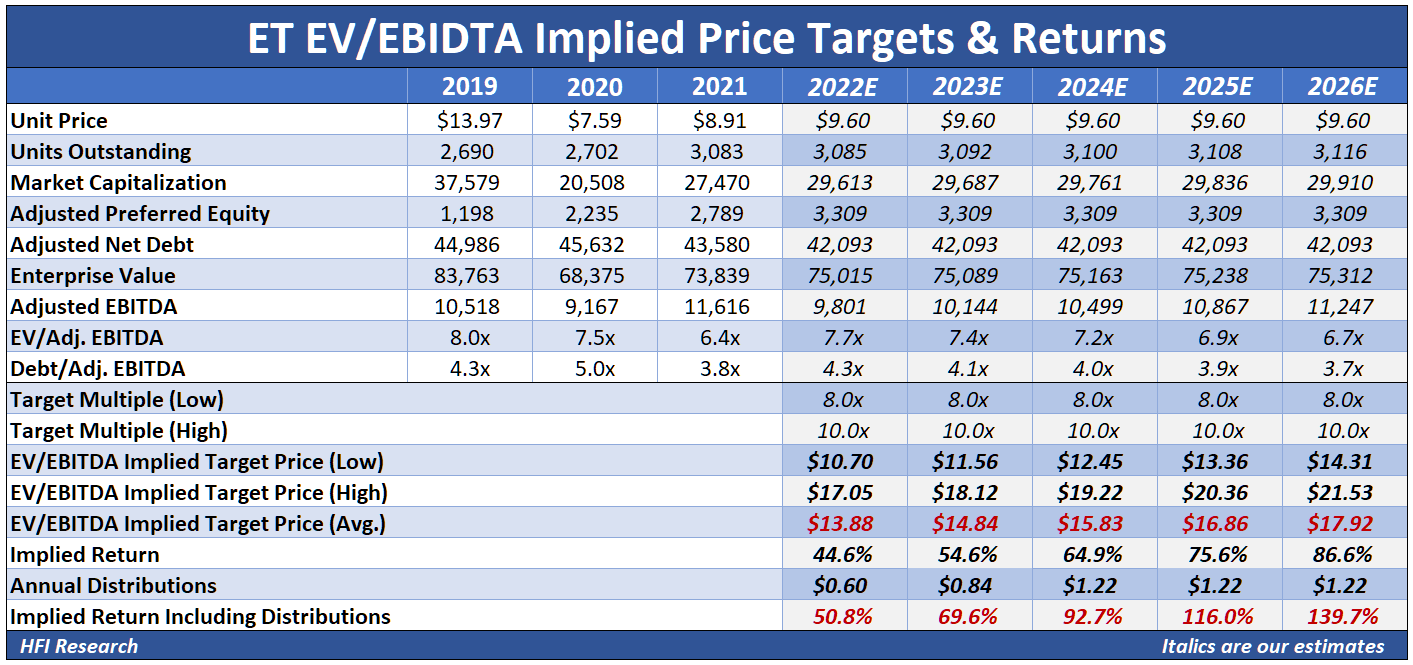

Our EV/EBITDA valuation using our adjusted figures implies ET units have 50.8% upside in 2022. Assuming that EBITDA increases by 3.5% annually and distributions increase by 5% in 2023 and then to $1.22 per unit in 2024, the implied total return increases to 139.7% by 2026.

{kind=link}

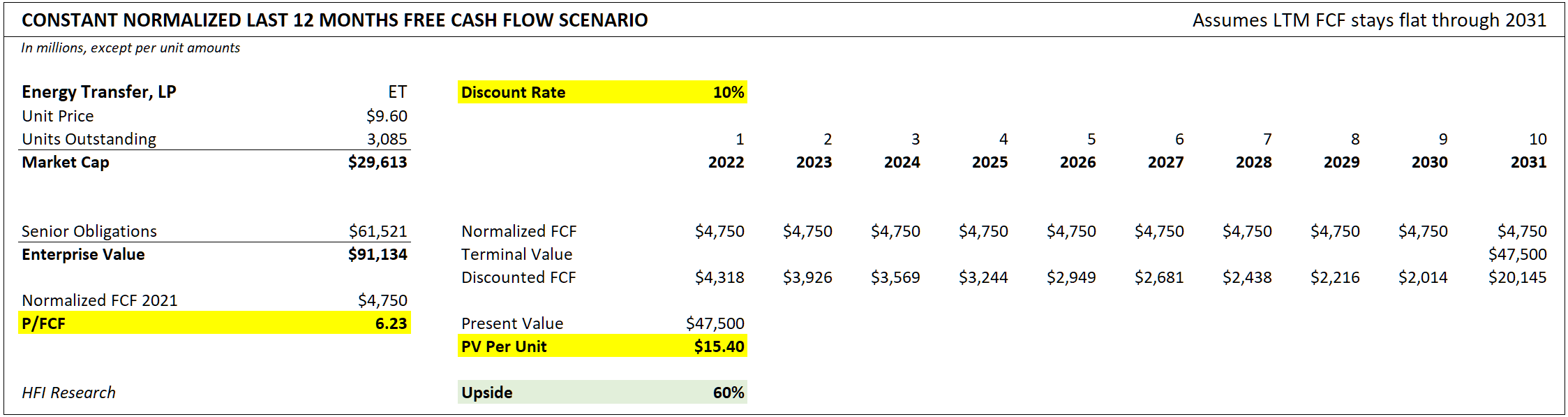

Our discounted cash flow valuation arrives at 2022 free cash flow by subtracting our adjusted interest and maintenance capex estimates. It values ET units at $15.40, which equates to 60% upside from the current price.

{kind=link}

We establish the top end of our valuation range by assuming that ET pays out $1.22 and its units trade at a 7.5% yield. The unit price would be $16.27 in that scenario.

Conclusion

In April, ET increased its distribution from $0.175 to $0.20. We view the move as a signal by management that the company's leverage is under control and that it plans to achieve its near-term leverage goal. Nevertheless, the units fail to reflect the likelihood of further leverage reduction and an eventual increase of the annual distribution to $1.22.

We expect ET to achieve its distribution goal by 2024. Investors should buy ET units now to benefit from the higher income and long-term capital appreciation that we believe will occur when that time comes.

For further details see:

Energy Transfer: Deleveraging And Distribution Increases To Send Units Higher