ET - Energy Transfer: High-Quality Midstream Play Is Far From Done (Rating Upgrade)

2023-11-20 16:30:02 ET

Summary

- Energy Transfer LP's dip buyers returned with conviction, helping to stem further downside volatility in early November. It's getting ready for the next upswing.

- The LP posted robust performances across its business segments, delivering strong financial results in Q3. It has justified its outperformance against its closest peers.

- The recent Crestwood Equity Partners acquisition has strengthened its market leadership, benefiting unitholders.

- ET remains attractively priced, suggesting previous pessimism was misplaced. Buyers looking to add exposure should capitalize on its recent pullback before it surges higher.

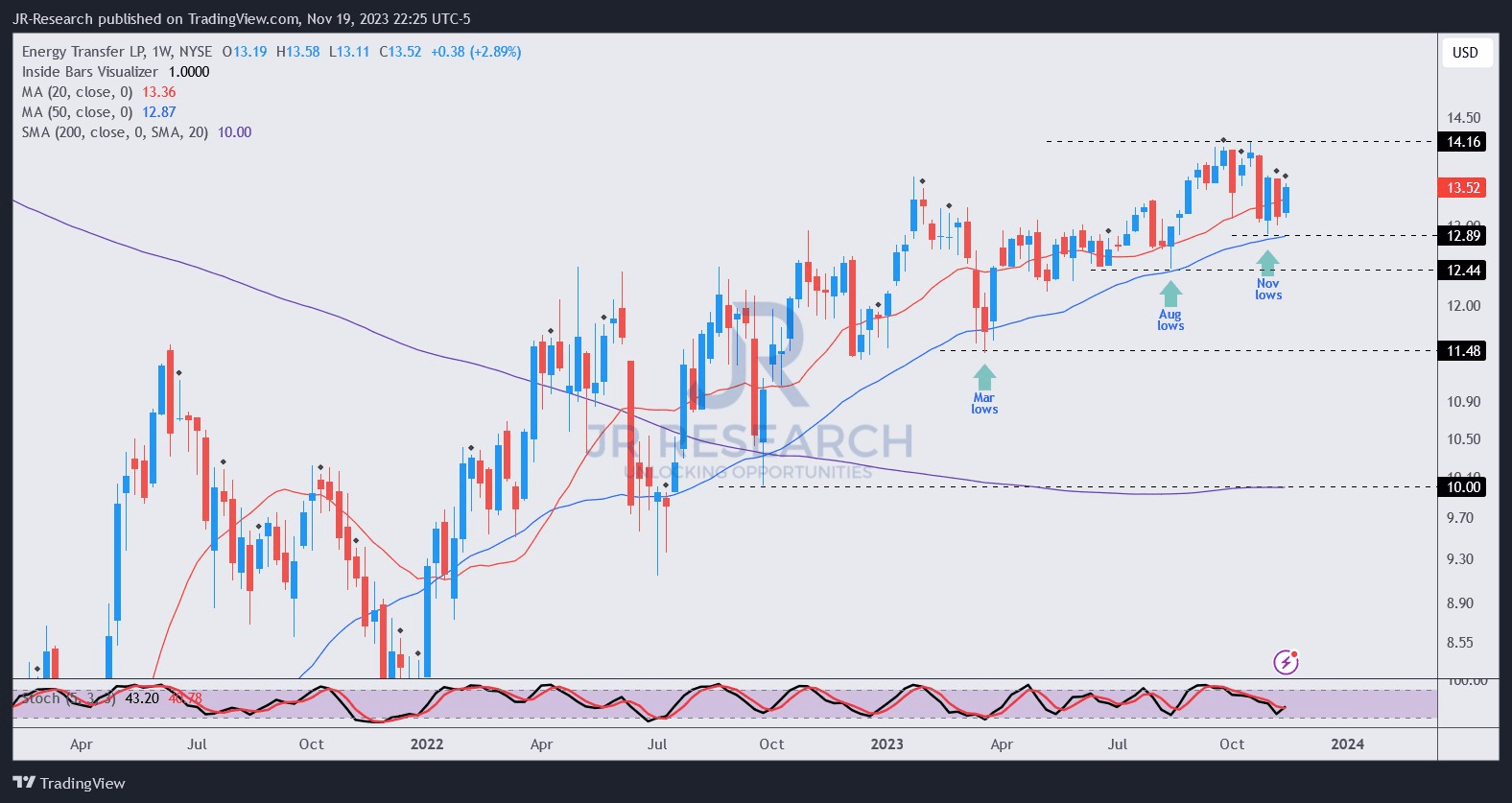

I urged unitholders in leading midstream player Energy Transfer LP ( ET ) to wait for a steeper pullback before adding exposure in my previous update in mid-September. That thesis panned out as ET topped out in mid-October at the $14.20 level before falling nearly 10% in price-performance terms, bottoming out in early November.

It's a pivotal development for bullish ET unitholders, suggesting dip buyers returned with conviction to help stem further downside volatility. The defense also coincided with Energy Transfer's impressive third-quarter or FQ3 earnings release earlier this month.

Accordingly, Energy Transfer posted robust performances across its business segment, " including record volumes in NGL pipelines, fractionators, NGL, and refined products terminals, as well as record volumes in the crude segment." As a result, ET delivered an adjusted EBITDA of $3.54B in Q3, up nearly 15% YoY. The LP also delivered $1.99B in distributable cash flow or DCF to its unitholders, which was about $0.63 per share, up more than 23% YoY.

As a reminder, Energy Transfer closed its Crestwood Equity Partners acquisition this month. The deal has firmed up the LP's ambitions as it "extends its position in the value chain deeper into the Williston and Delaware basins." The DCF-accretive acquisition is expected to complement Energy Transfer's "downstream fractionation capacity at Mont Belvieu and hydrocarbon export capabilities from Nederland and Marcus Hook terminals."

As a result, market participants responded well to Energy Transfer's impressive execution, bolstering their confidence in the LP's ability to integrate its recent acquisitions. Management's commentary suggests the Crestwood acquisition is expected to contribute about $200M in adjusted EBITDA to FY23's overall performance. Consequently, management anticipates a revised full-year adjusted EBITDA range of between $13.5B and $13.6B.

However, Energy Transfer has refrained from providing its outlook for FY24, although the S-4 regulatory filings suggest an outlook of $15B adjusted EBITDA in 2024 remains possible. Analysts' estimates of $14.4B for the LP's FY24 adjusted EBITDA indicate uncertainties regarding management's estimates. Despite that, the LP's robust Q3 performance has underpinned the market's conviction about a strong 2024 update when Energy Transfer provides its outlook at its Q4 earnings call.

{kind=link}

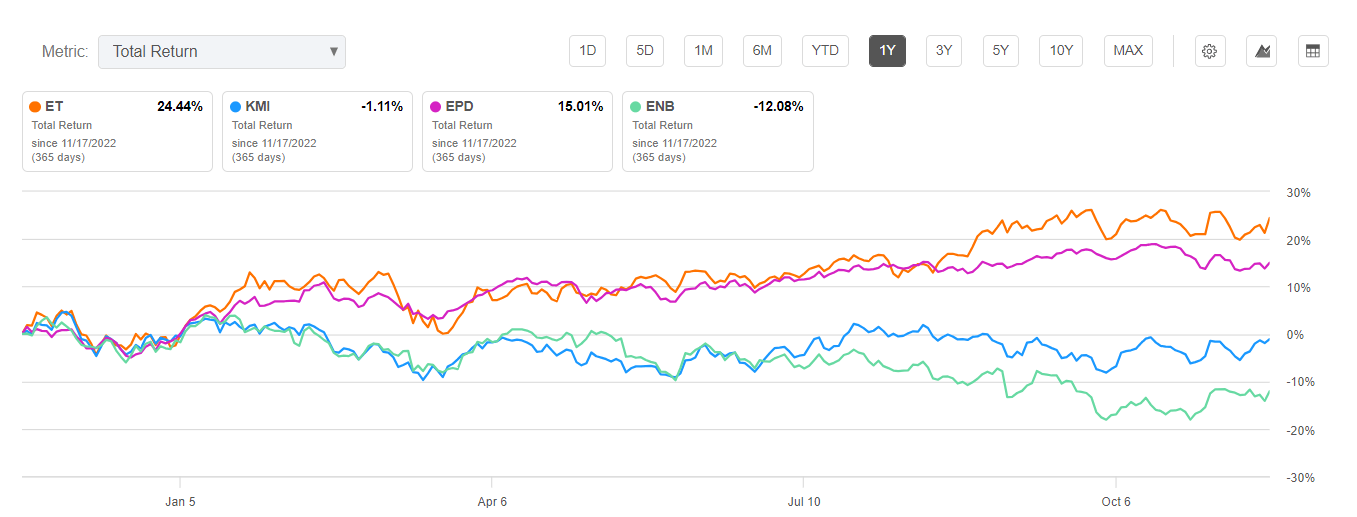

As seen above, ET has significantly outperformed its peers listed above. The outperformance is substantial, suggesting the market has been optimistic about the LP's performance. Its outperformance is justified, as seen in its recent Q3 performance.

{kind=link}

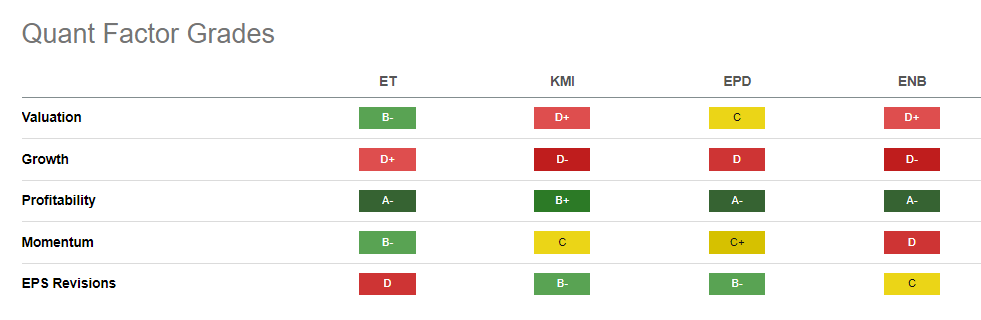

Moreover, ET remains attractive, assigned a "B-" valuation grade compared to its peers. Accordingly, ET's peers are priced at a much steeper premium than their energy sector ( XLE ) constituents.

As a result, the market's more pessimistic positioning of ET has likely supported ET's outperformance as investors rotated out of more expensive midstream plays, taking advantage of ET's relative valuation dislocation.

However, investors must note that previous outperformance doesn't necessarily indicate future results. Despite that, with ET's relatively attractive valuation, is it possible that dip buyers are still looking to buy into ET units at pullbacks?

{kind=link}

Based on my analysis, I expect ET to continue grinding higher as dip buyers return to defend the $12.90 zone confidently in early November. It sets the stage for ET's medium-term uptrend to be maintained, as ET looks ready to re-test and potentially break above its $14.15 zone decisively at the next upswing.

As a result, I gleaned buying opportunities for unitholders are still reasonable for investors who didn't manage to buy its early November pullback. ET has proved to be a solid play for midstream energy investors who defied previous pessimistic calls, given its solid execution and confident outlook.

Rating: Upgraded to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Energy Transfer: High-Quality Midstream Play Is Far From Done (Rating Upgrade)