CA - Energy Transfer: New Guidance Paints An Even More Bullish Narrative

2023-11-06 05:11:23 ET

Summary

- Energy Transfer's financial results for Q3 2023 were mixed but mostly positive, with an increase in guidance that the market is overlooking.

- Revenue decreased, but the volume of product transported and profitability increased in various segments.

- ET continues to invest in growth initiatives, and the acquisition of Crestwood Equity Partners was just completed.

- Shares are incredibly cheap and warrant material upside from here.

Those who follow my work closely almost certainly know that one of my favorite holdings in my portfolio right now is midstream/pipeline operator Energy Transfer (ET). As of this writing, it is the third largest holding in my portfolio, accounting for 12.7% of total assets. So far, I've done quite well holding the stock, thanks not only to its hefty distribution but also to the appreciation I have seen on units. Well, after the market closed on November 1st, the management team at the business announced financial results covering the third quarter of the company's 2023 fiscal year. During that quarter, financial results were mixed but mostly positive. But what was most important in my eyes was an increase in guidance that I think the market is overlooking to some extent. When you look at this guidance adjustment and you see how shares are priced relative to similar firms, it becomes clear that the stock offers investors tremendous upside from here even after appreciating 13.2% year to date already.

The picture just keeps getting better

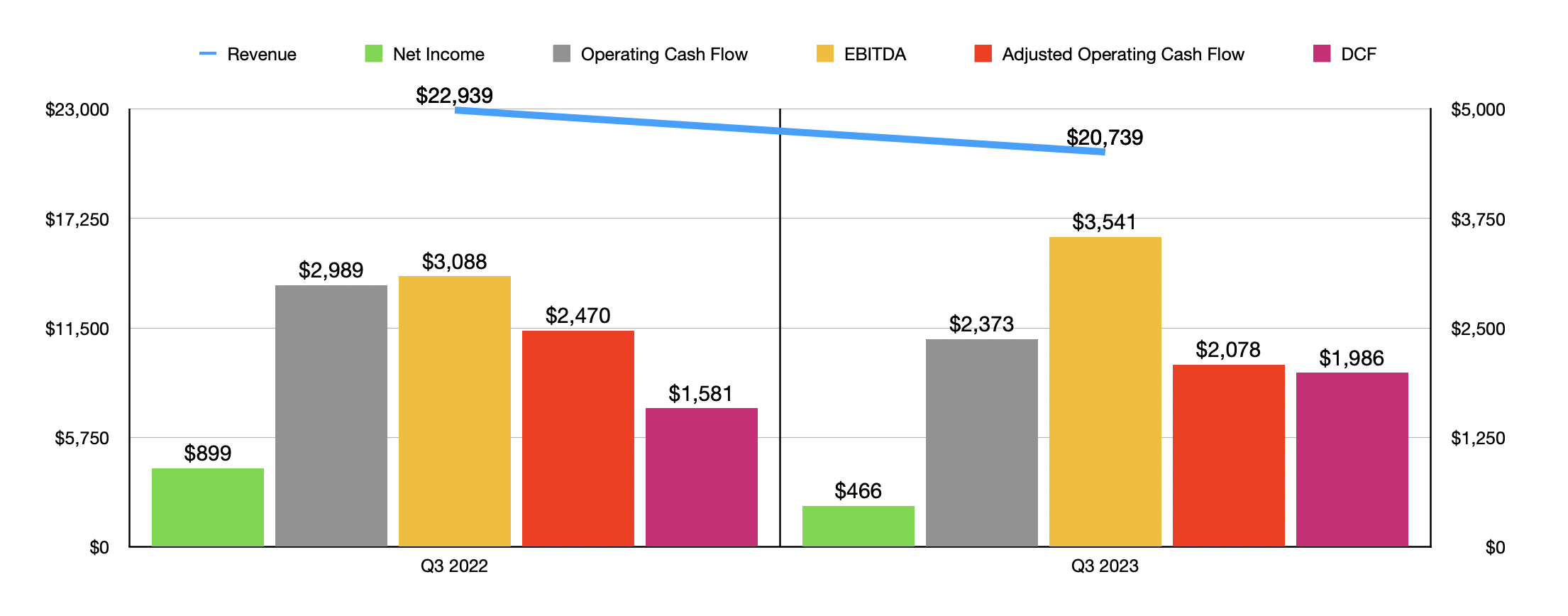

After the market closed on November 1st, the management team at Energy Transfer announced financial results covering the third quarter of the company's 2023 fiscal year. To those looking at just the headline news, some of the data might look scary. But it really isn't. The prime example I could point to is revenue. During the quarter, sales came in at $20.74 billion. That's 9.6% lower than the $22.94 billion generated one year earlier. But for companies like this, revenue is not all that significant. What's more important is the volume of product transported or otherwise processed, and the spread between the cost of achieving it and the value from selling it.

{kind=link}

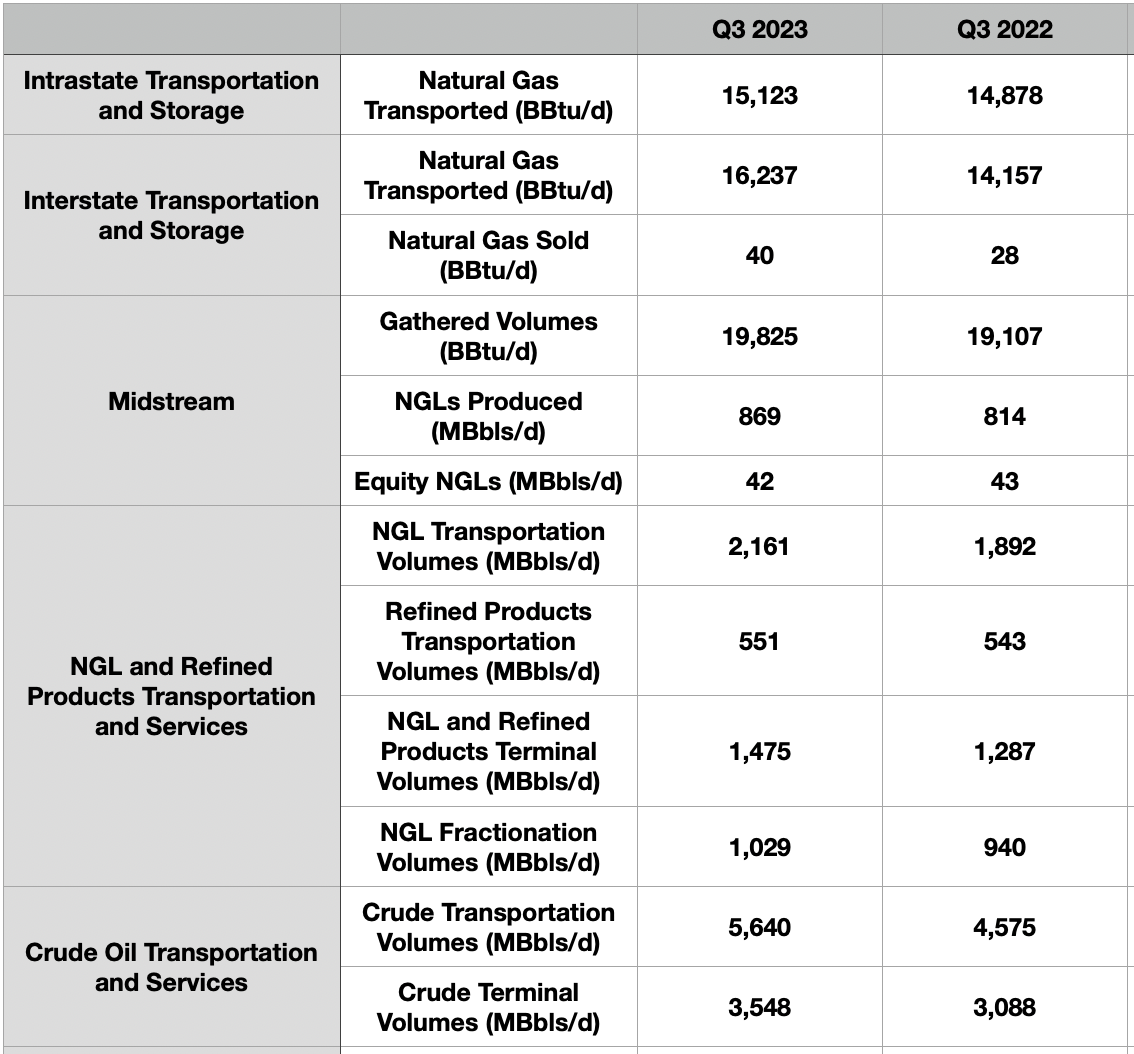

As an example, I would like to point to the Intrastate Transportation and Storage segment of the company. Revenue plummeted from $2.38 billion to only $973 million. But the actual volume of natural gas transported grew by 1.6%. The segment EBITDA did decline. But it was a more modest 18.9% from $301 million to $244 million. Other segments reported a drop in revenue but a corresponding increase in profitability. The NGL and Refined Products Transportation and Services segment, for instance, reported a decline in revenue from $6.08 billion to $5.26 billion. Even so, NGL transportation volumes jumped by 14.2%. Refined products transportation volumes inched up 1.5%, NGL and refined products terminal volumes jumped 14.6%, and NGL fractionation volumes managed to increase by 9.5%. These increases, combined with various changes like marketing and transportation margin improvements, growth in terminal services margins, and reductions in costs thanks to lower gas and power utility expenses, still allowed segment EBITDA to jump from $634 million to $1.08 billion.

{kind=link}

There were other parts of the company that did see revenue drop and profitability drop as well. But without exception, these segments saw increases in volumes of their respective products. The one really bright spot for the company involved its Crude Oil Transportation and Services segment. Higher oil prices, combined with higher transportation and terminal volumes of 23.3% and 14.9%, respectively, pushed revenue up from $6.42 billion to $7.29 billion. And at the same time, segment EBITDA for the company skyrocketed from $461 million to $706 million.

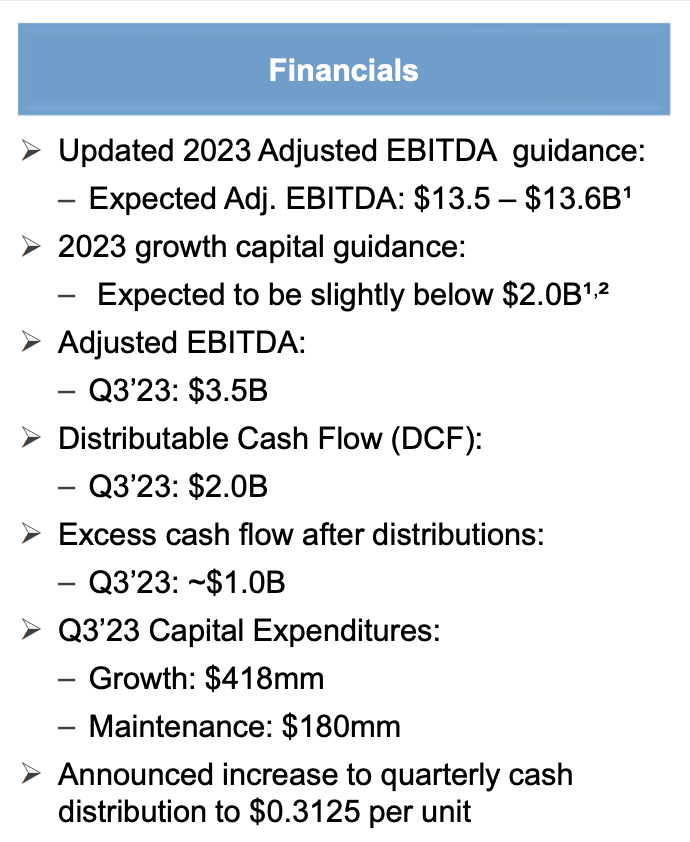

Even though net profits for the business were slashed from $899 million in the third quarter of 2022 to $466 million the same time this year, other profitability metrics fared quite well. DCF, as an example, shot up from $1.58 billion to $1.99 billion. And finally, EBITDA for the company jumped from $3.09 billion to $3.54 billion.

{kind=link}

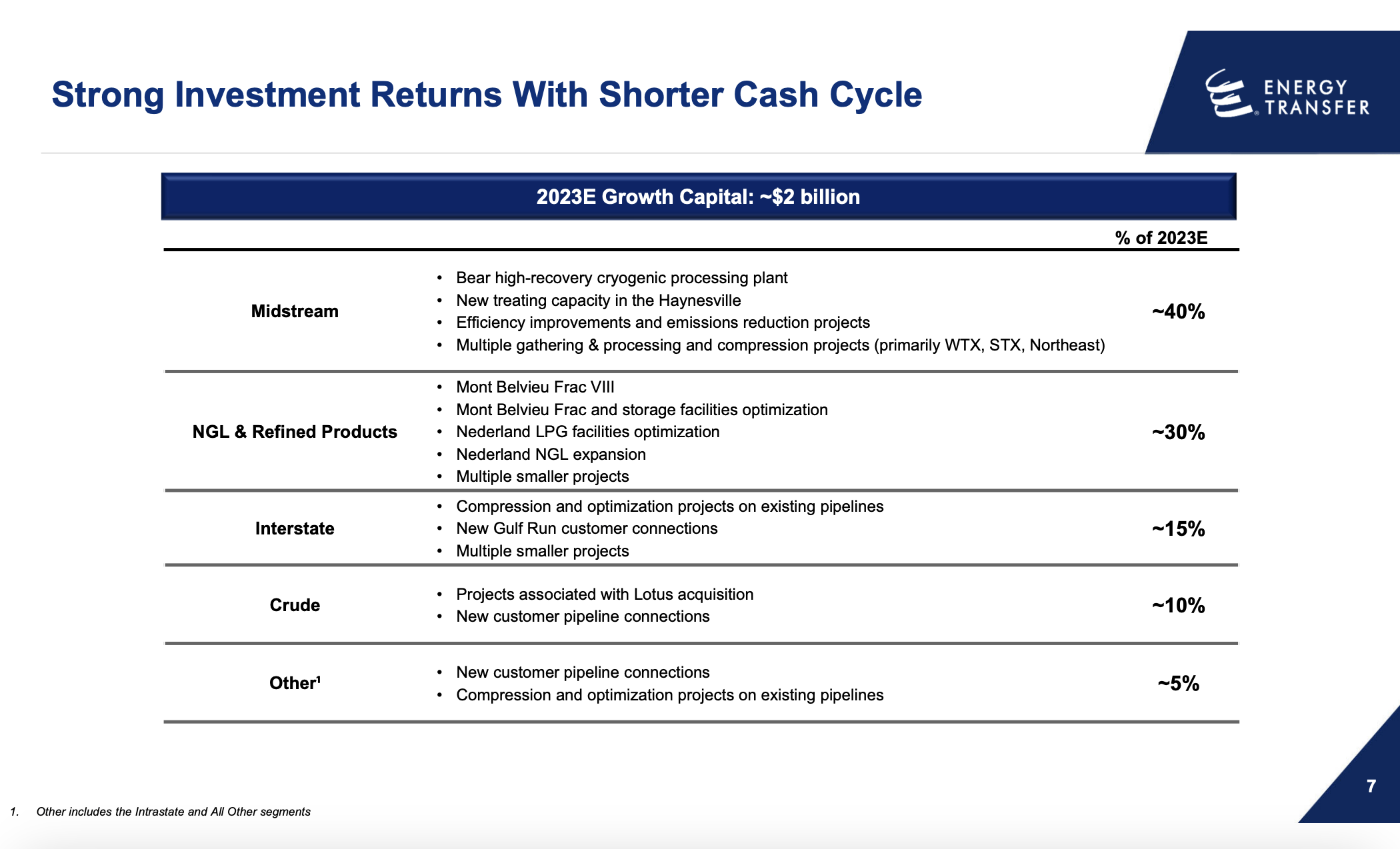

One of the really great things about Energy Transfer is that the company continues to invest in growth initiatives. This year, for instance, it is allocating around $2 billion of capital expenditures toward growth prospects. 40% of this falls under the midstream operations of the company such as adding new treating capacity in the Haynesville Basin and investing in multiple gathering and processing and compression projects across the nation. NGL and Refined Products is the second major area of focus, accounting for 30% of growth spending. This is followed up by Interstate projects in a distant third place with 15%. The rest of the proceeds are being allocated toward Crude and other projects.

All of this spending, it's worth saying, does not factor in the $7.1 billion acquisition that Energy Transfer is about to close. When that deal was first announced, with Energy Transfer acquiring Crestwood Equity Partners in an all-stock deal, I wrote an article wherein I talked about how the deal makes sense for investors. I did mention that I would have considered some sort of cash component to the deal to be superior. But at the end of the day, even without factoring in the synergies, the transaction should add value to investors. This includes the $40 million in initial annual run-rate synergies the firm announced with the closing of the purchase on November 3rd. But that means that we need to be extra careful when looking at the most recent data provided by the management team at Energy Transfer.

Management now believes that the company will generate EBITDA of between $13.5 billion and $13.6 billion for 2023 in its entirety. That's up from the $13.1 billion to $13.4 billion range previously anticipated. But when you look at the fine print, you see that this new guidance factors in the purchase of Crestwood, which itself is expected to generate between $780 million and $860 million worth of EBITDA this year. Very likely, according to management, this amount will be at the lower end of the range. So in the aforementioned article, I assumed that it would be roughly $800 million that the business would generate this year.

{kind=link}

Assuming that cash flows are fairly even in the two months in which they will be recorded for Crestwood relative to the rest of the year, this means that they should only account for roughly $133 million of the EBITDA generated by Energy Transfer this year. If we use the midpoint of guidance provided by management, this means that Energy Transfer is still getting an increase in guidance from the prior range to approximately $13.42 billion. When we add on the $800 million associated with Crestwood and factor in the purchase price of that into the value of our prospect, we can easily value the firm as a whole and see where things stand following this change in guidance.

{kind=link}

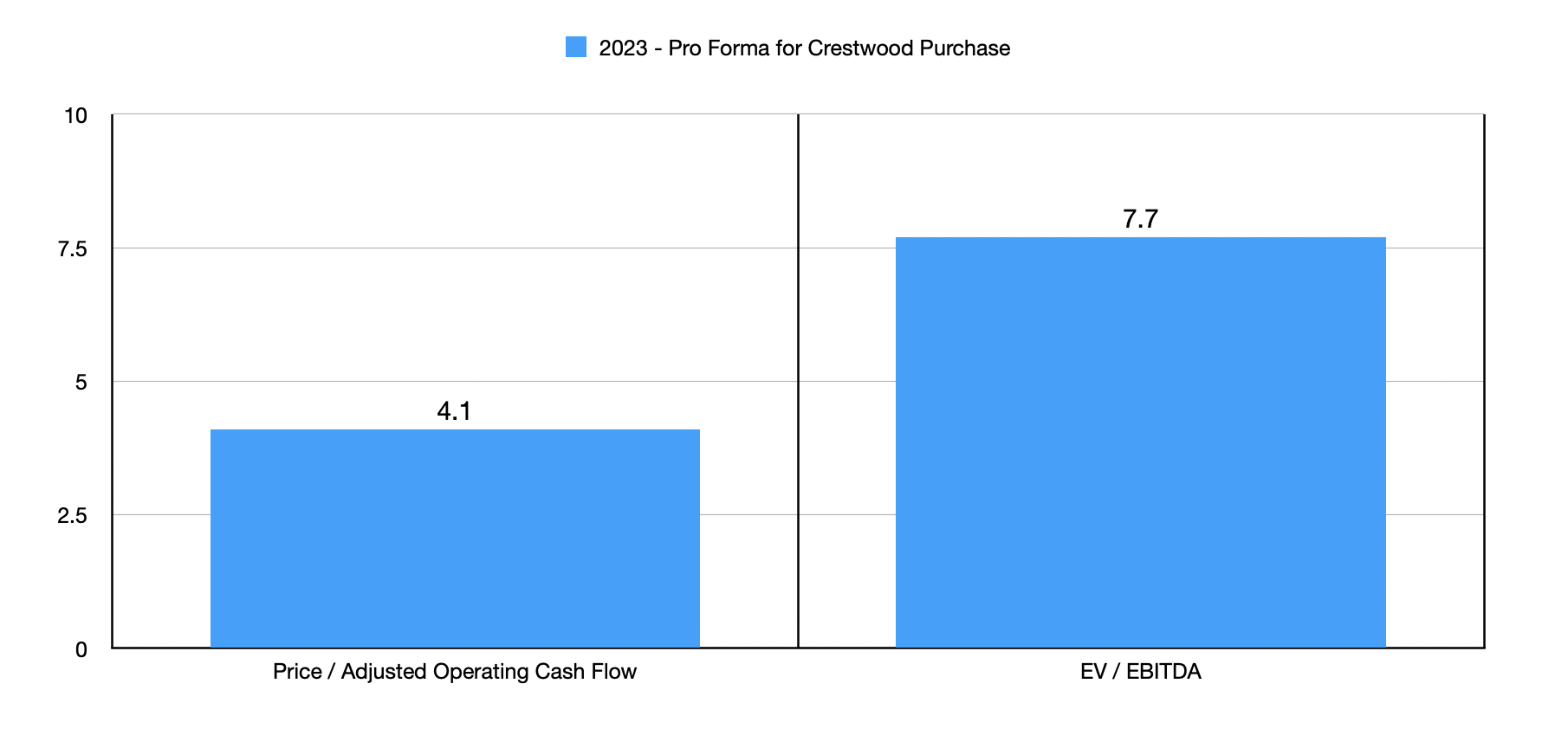

Using estimates for adjusted operating cash flow for both companies, I calculated a price to adjusted operating cash flow multiple for them, when combined, of 4.1. The EV to EBITDA multiple is a bit higher at 7.7. I then, in the table below, compared the combined entity to five similar firms. Using both of the valuation metrics, our candidate ended up being the cheapest of the group. I then, in the table below that, decided to see what kind of upside potential might exist for shareholders from this point on. If we assume that Energy Transfer should trade at the price to operating cash flow multiple of the cheapest of its five rivals, that would imply upside of 61%. If we strip out the most expensive of the five companies and average out the remaining multiples, upside increases to 72.1%. Using the same approach for the EV to EBITDA multiples of the company would yield upside of between 70.7% and 112.4%.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Energy Transfer |

| 4.1 |

| 7.7 |

| Kinder Morgan ( KMI ) |

| 6.6 |

| 10.5 |

| The Williams Companies ( WMB ) |

| 7.6 |

| 9.9 |

| Enbridge ( ENB ) |

| 6.7 |

| 12.9 |

| Enterprise Products Partners ( EPD ) |

| 7.9 |

| 9.7 |

| MPLX Inc. ( MPLX ) |

| 7.1 |

| 9.0 |

{kind=link}

Takeaway

As things stand, the fundamental picture for Energy Transfer is solid and getting better. The increase in guidance is incredibly bullish, especially when you consider that most of the improvement likely does not involve robust cash flows from Crestwood. After making certain adjustments, it becomes very clear to me that Energy Transfer remains one of the cheapest prospects on the market and I do believe that this will eventually pay off handsomely. As such, I feel very comfortable keeping it rated a 'strong buy' at this time.

For further details see:

Energy Transfer: New Guidance Paints An Even More Bullish Narrative