ET - Energy Transfer: Q3 Results Show The Company Remains A Core Income Holding

2023-11-06 17:18:36 ET

Summary

- Energy Transfer LP reported mixed Q3 2023 earnings, beating revenue expectations but missing earnings.

- Revenue and earnings were down year-over-year due to lower natural gas liquids and natural gas prices.

- Despite the decline, the market was satisfied with the results, and Energy Transfer's unit price increased.

- Energy Transfer is positioned to deliver growth over the next few years as it has a number of projects in development and the Gulf Run Pipeline's volumes will increase.

- The company's overall financial strength and high distribution coverage remain intact, and the company continues to look like a core holding for any income investor.

On Wednesday, Nov. 1, 2023, giant midstream master limited partnership Energy Transfer LP ( ET ) announced its third quarter 2023 earnings results. At first glance, these results were mixed as the company managed to beat the expectations of its analysts in terms of revenue but missed earnings. However, both revenue and earnings were down year-over-year. That's generally what we have seen across the sector as lower natural gas liquids and natural gas prices adversely pressure the financial performance of natural gas processing facilities. We have discussed this in various previous articles, such as this one from late last week. Overall, though, we still see the typical stability that we have come to expect from most midstream corporations and partnerships.

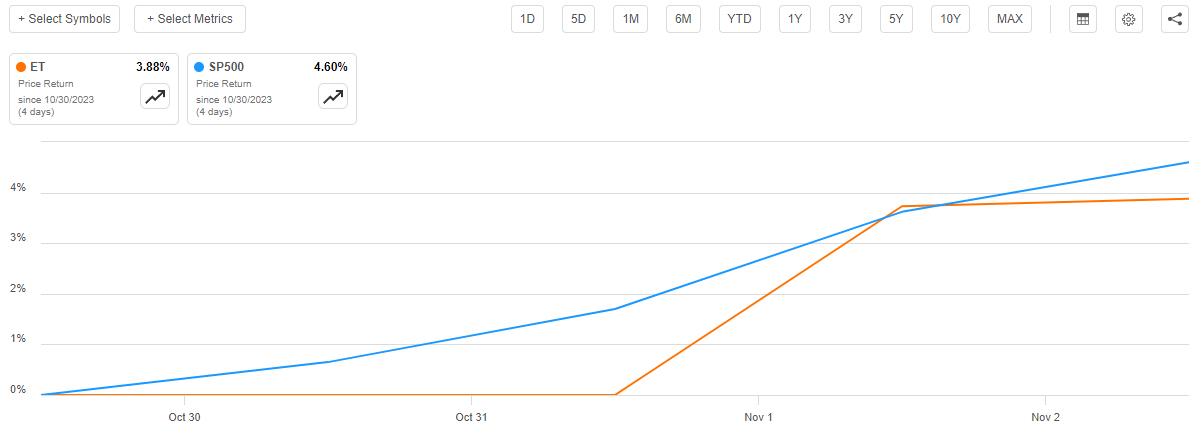

For its part, the market appeared to be satisfied with these results. Energy Transfer's unit price shot up in the first trading session following the results announcement, although the company did fail to beat the S&P 500 Index ( SP500 ) over the week:

{kind=link}

With that said, Energy Transfer has a 9.15% yield at the current price, so it does not need to outperform the S&P 500 Index in order for investors to obtain a reasonable return. In fact, most financial advisors and planners assume that 10% is a pretty respectable long-term return and Energy Transfer manages to get very close to that even if the company's unit price remained flat. Regardless, the point is that the market appeared to find the company's results acceptable.

As such, we should analyze Energy Transfer's earnings results ourselves and determine if the company still fits with our thesis with respect to long-term stability, moderate growth, and a high and sustainable distribution yield.

Earnings Results Analysis

As regular readers are no doubt well aware, it's my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Energy Transfer's third quarter 2023 earnings results:

- Energy Transfer reported a total revenue of $20.7390 billion in the third quarter of 2023. This represents a 9.59% decline over the $22.9390 billion that the company reported in the prior year quarter.

- The company reported an operating income of $2.2340 billion in the most recent quarter. This represents an 8.50% improvement over the $2.0590 billion that the company reported in the year-ago quarter.

- Energy Transfer carried an average of 5.640 million barrels of crude oil per day through its pipeline infrastructure during the most recent quarter. This represents a substantial 23.28% increase over the 4.575 million barrels of crude oil per day that the company transported on average during the equivalent quarter of last year.

- The company reported a distributable cash flow of $1.984 billion in the reporting period. That represents a 25.49% increase over the $1.581 billion that the company reported in the same quarter of last year.

- Energy Transfer reported a net income of $584.0 million during the third quarter of 2023. This represents a disappointing 41.89% decline over the $1.0050 billion that the company reported in the third quarter of 2022.

One of the first things that I immediately noticed in these results is that Energy Transfer substantially increased the volume of crude oil that it transported compared to the prior-year quarter. The reason for this was the acquisition of Lotus Midstream which was completed back in May. This acquisition gave Energy Transfer an additional 3,000 miles of crude oil gathering and transportation pipelines compared to its pre-acquisition level. Energy Transfer acknowledged in its earnings press release that this acquisition was primarily responsible for the tremendous volume growth that the company experienced year-over-year:

Crude transportation volumes were higher on our Texas pipeline system due to higher Permian crude oil production, higher gathered volumes, and contributions from assets acquired in 2023. Volumes on our Bakken pipeline were also higher, driven by continuing crude oil production growth in the Bakken. Volumes on our Bayou Bridge Pipeline were relatively consistent due to continuing strong Gulf Coast refinery demand.

The Lotus Midstream acquisition was the only crude oil acquisition that Energy Transfer engaged in during 2023 that was anywhere near large enough to cause the company's crude oil transported volumes to grow as dramatically as they did. While the company does cite higher production growth in both the Bakken Shale and Permian Basin, neither one of these basins experienced year-over-year production growth that was large enough to increase the company's crude oil volumes by 1.065 million barrels per day. We can see that here:

U.S. Energy Information Administration

Thus, it appears essentially certain that the biggest contributor to the company's year-over-year crude oil volume growth was the Lotus Midstream acquisition. This is despite Energy Transfer not specifically mentioning it by name in the earnings report. Energy Transfer raised its guidance following the completion of the merger, so it appears that it was correct that the acquisition is contributing positively to its results. After all, Energy Transfer's cash flows directly correlate with its transported volumes for reasons that I have explained in numerous previous articles on this company.

There were a few other contributors to the company's year-over-year growth besides the Lotus Midstream acquisition. These were largely in the natural gas space. The company's intrastate and interstate natural gas pipeline systems experienced volume growth compared to the prior-year quarter. We can see that here:

| Q3 2023 |

| Q3 2022 |

| Intrastate Transportation Volumes (BBTU/d) |

| 15,123 |

| 14,878 |

| Interstate Transportation Volumes (BBTU/d) |

| 16,237 |

| 14,157 |

Energy Transfer specifically cites the Gulf Run pipeline system as a contributor to the interstate transportation volume growth. The Gulf Run pipeline system is a natural gas pipeline running south across the state of Louisiana:

Energy Transfer

This system was originally part of Enable Midstream's natural gas infrastructure network, which was acquired through a merger a few years ago. This project has been in the works ever since that date as a means through which Energy Transfer is hoping to take advantage of the tremendous natural gas demand growth coming out of the emerging liquefied natural gas export sector. Regular readers may recall that we have discussed this project several times over the past few years and it has been part of our growth thesis surrounding this company. The system started operation in December of last year, so every quarter this year has been experiencing higher natural gas volumes than in the prior year's quarter due to contributions from natural gas moving through this system.

The Gulf Run Pipeline will be able to be a greater source of growth for the company going forward than it already has been. This is because of a few contracts that the company has with its customers for the use of the pipeline. As the map above shows, the Gulf Run Pipeline system consists of two zones. Zone 1 has a total capacity of 1.4 billion cubic feet of natural gas per day. Zone 2 is larger, as it boasts a total capacity of 1.65 billion cubic feet of natural gas per day. For the next year or so, Zone 2 is slightly undersubscribed and has some excess capacity. However, this changes in January of 2025. Energy Transfer has managed to secure contracts for the full capacity of the pipeline beginning on that date. This will result in the amount of natural gas moving through the pipeline going up and thus directly increasing the cash flow that's being generated by the pipeline. This additional cash flow will prove to be directly accretive to Energy Transfer's consolidated results. Thus, we can expect a bit of an incremental cash flow increase during the first quarter of 2025.

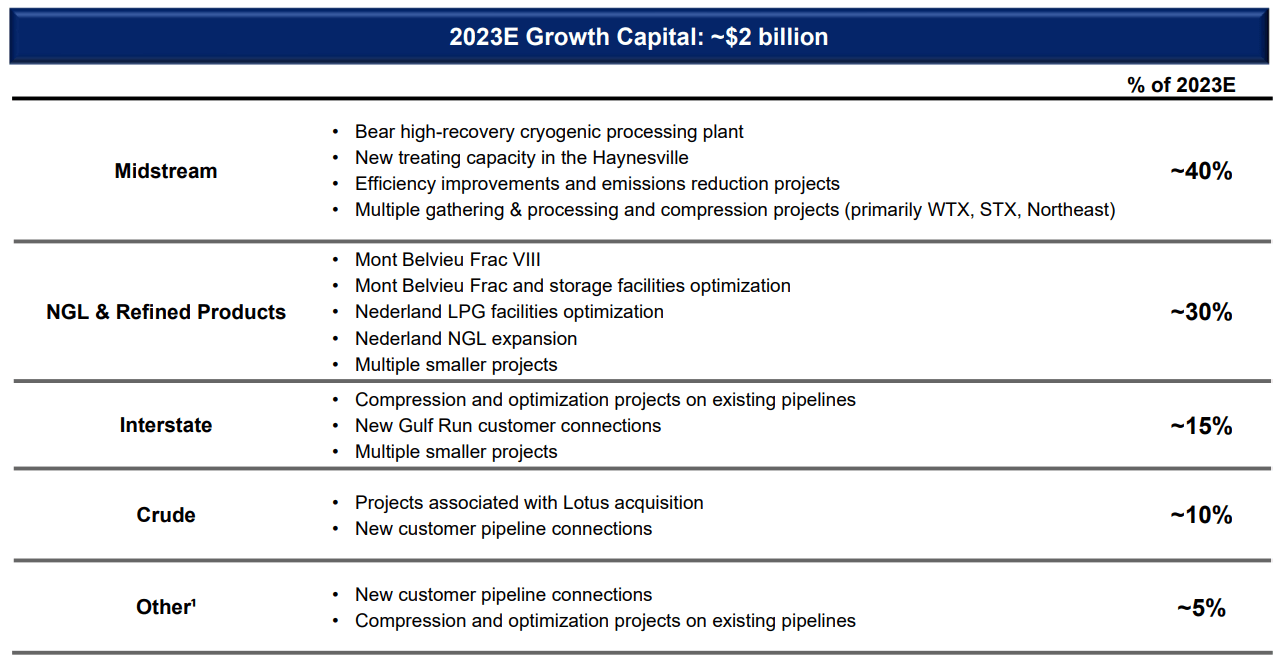

This pipeline will not be the only source of growth for Energy Transfer going forward. The company has a number of growth projects currently under development and is planning to spend a total of approximately $2 billion during 2023 alone on these projects:

{kind=link}

The nice thing about all of these projects is that Energy Transfer has already secured contracts from its customers for their use. After all, it does not make sense for the company to build new expensive projects that nobody wants to use. The fact that contracts are already in place also means that Energy Transfer can be relatively certain that they will generate positive cash flow once their construction is complete and they are placed into operation. Overall, this sets Energy Transfer up for cash flow growth over the next few years. Investors should be reasonably pleased with this.

Financial Considerations

As I pointed out in my last article on Energy Transfer:

It's always important that we analyze the way that a company finances its operations before investing in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. As new debt is issued with an interest rate that corresponds to the market interest rate at the time of issuance, this can cause a company's interest expenses to go up following the rollover. That is an especially big concern today because interest rates in the United States are at the highest levels that we have seen since 2001.

The usual method that we use to analyze a midstream company's debt load is its leverage ratio. This also is known as the consolidated debt-to-adjusted EBITDA ratio and it essentially tells us how long it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task.

As of Sept. 30, 2023, Energy Transfer had a consolidated debt of $48.850 billion. In the third quarter, the company's adjusted EBITDA was $3.541 billion, which represented a 14.67% increase over the $3.088 billion that the company reported in the prior year quarter. The company's adjusted EBITDA from the current quarter works out to $14.164 billion on an annualized basis. This gives the company a leverage ratio of 3.45x based on its annualized third-quarter adjusted EBITDA. Wall Street analysts generally consider anything below 5.0x to be reasonable. However, as I have pointed out numerous times, the best companies in the industry have been working very hard to get their leverage ratios down over the past few years in an attempt to reduce their reliance on the market for financing. As a result, a 4.0x ratio is now the standard for a midstream company to have a strong balance sheet. As we can clearly see, Energy Transfer easily satisfies this requirement and as such we should not need to worry too much about its debt load right now.

Distribution Analysis

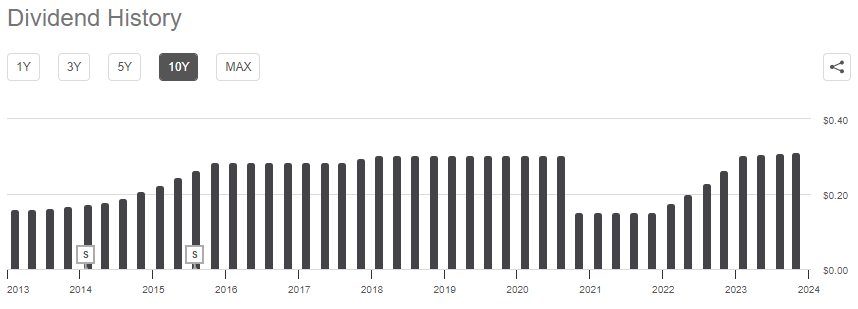

One of the biggest reasons why investors purchase units of midstream master limited partnerships like Energy Transfer is the high yield that these entities usually possess. Energy Transfer is certainly no exception to this as it boasts a 9.15% yield at the current price, which is high even by the standards of these companies. Unfortunately, Energy Transfer has a somewhat spotty distribution history, as it opted to cut the payout back in 2020 despite not actually needing to do so but it has since brought it back to the previous level:

{kind=link}

In conjunction with its third quarter results, Energy Transfer declared a distribution of $0.3125 per common unit. This is actually higher than the level that it paid in August 2020, which was the last distribution before the 2020 cut. Thus, not only has the company brought the payout back to the previous level but it has actually exceeded it. While the fact that the distribution was below pre-pandemic levels for a while was certainly annoying to long-term investors, overall the company seems to have proven its commitment to providing income to its investors.

As is always the case though, it's critical that we analyze the company's finances to ensure that it can actually afford its distribution. After all, we do not want to be the victims of another surprise distribution cut that reduces our income and almost certainly causes the company's unit price to decline.

The usual way that we judge a midstream company's ability to pay its distribution is by looking at its distributable cash flow. Distributable cash flow is a non-GAAP metric that theoretically tells us the amount of cash that was generated by a company's ordinary operations and is available to be paid out to the limited partners. As mentioned in the highlights, Energy Transfer reported a distributable cash flow of $1.984 billion in the most recent quarter. However, the company's distribution only costs it $984 million. That gives the company a distribution coverage ratio of 2.02x, which is very reasonable. Wall Street analysts usually consider anything above 1.20x to be sustainable over the long term. As we can clearly see, Energy Transfer currently exceeds this ratio by a substantial amount. Thus, the company is generating more than enough cash flow to generate the distribution and should be able to sustain it.

Investors should not have to worry too much about a distribution cut here, although that was also the case prior to the 2020 distribution cut so there's always a risk.

Conclusion

In conclusion, Energy Transfer was still adversely impacted by some of the trends that we have seen in other midstream companies. In particular, its revenues came in somewhat weaker than in the prior year quarter due mostly to lower natural gas liquids prices. However, this had a minimal impact on the company's cash flow, and overall Energy Transfer's financial performance held up much better year-over-year than some other midstream companies that we discussed. The company's overall balance sheet and distribution coverage remain strong and the company continues to look like it deserves a place in the portfolio of any income-focused energy investor.

For further details see:

Energy Transfer: Q3 Results Show The Company Remains A Core Income Holding