ET - Energy Transfer: The 9.6% Yield Your Portfolio Is Missing

2023-11-09 11:44:08 ET

Summary

- Energy Transfer offers a safe and attractive 9.6% dividend yield, with potential for growth and increased shareholder returns.

- The company has managed its balance sheet well, leading to increased cash flow and a low debt ratio.

- Energy Transfer owns a diverse portfolio that is heavy in natural gas.

Many investors are searching for yield as the market remains volatile and extremely unpredictable. Ideally, in an industry that has legs and will be around for decades to come. That takes me to the energy industry, and more specifically natural gas pipeline companies. Energy Transfer (ET) meets that criteria. Currently paying out a 9.6% yield, it's worth a deeper look. Energy Transfer has managed its balance sheet extremely well in recent years. This has led to a surge in cash from operations and a low debt ratio. This is why the stock is a screaming buy at current levels.

Who/What Is Energy Transfer?

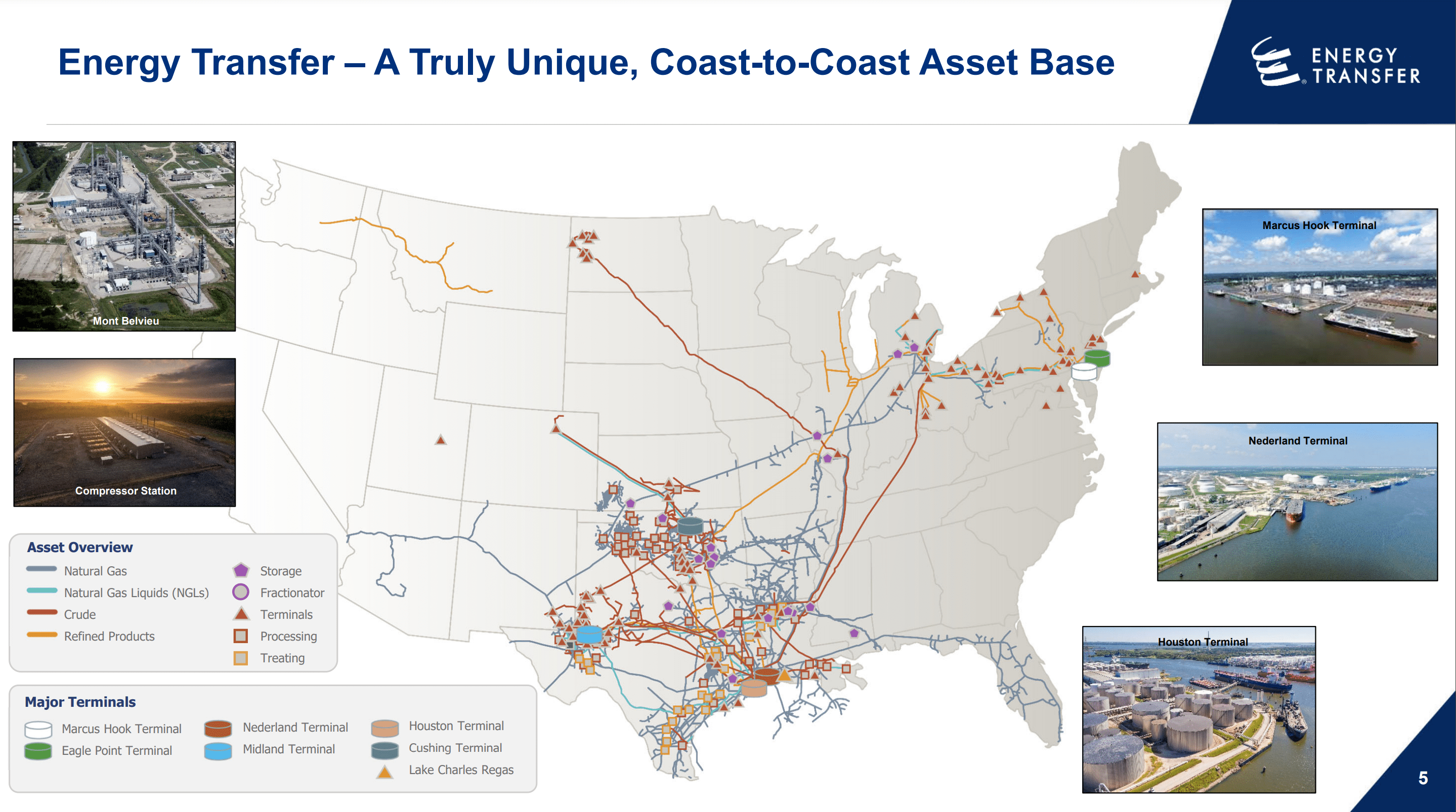

Energy Transfer owns and operates a diverse portfolio of energy assets. Their export terminals and ~125,000 miles of pipe move energy products across the United States, and the rest of the world. Energy Transfer operates in over 49 countries worldwide. This makes it one of the country's largest midstream service providers and allows it to deliver "best in class" logistics and transportation platforms for natural gas, natural gas liquids, crude oil, and refined products. Can you spell diversification?

{kind=link}

I mentioned that I look for natural gas earlier, you might ask yourself why that is. When one thinks of pipelines, the first thought is often Oil. But, as you will see from the map above, there are various kinds of pipe and materials that flow through them. In Energy Transfers case, they provide natural gas gathering, compression, treating, transportation, storage, and marketing services for natural gas, using nearly 90,000 miles of pipeline, 252 Bcf of working storage capacity, and more than 75 natural gas processing and treating facilities. Often we think the shift in energy is headed towards renewables, so why invest in natural gas? It's not going anywhere. Natural gas is resilient because of its lower carbon intensity. Because of this, it dodges some of the heat that oil gets concerning carbon footprint. The good news is that it needs to be transported somehow, which is where Energy Transfer comes in.

How Is The Balance Sheet?

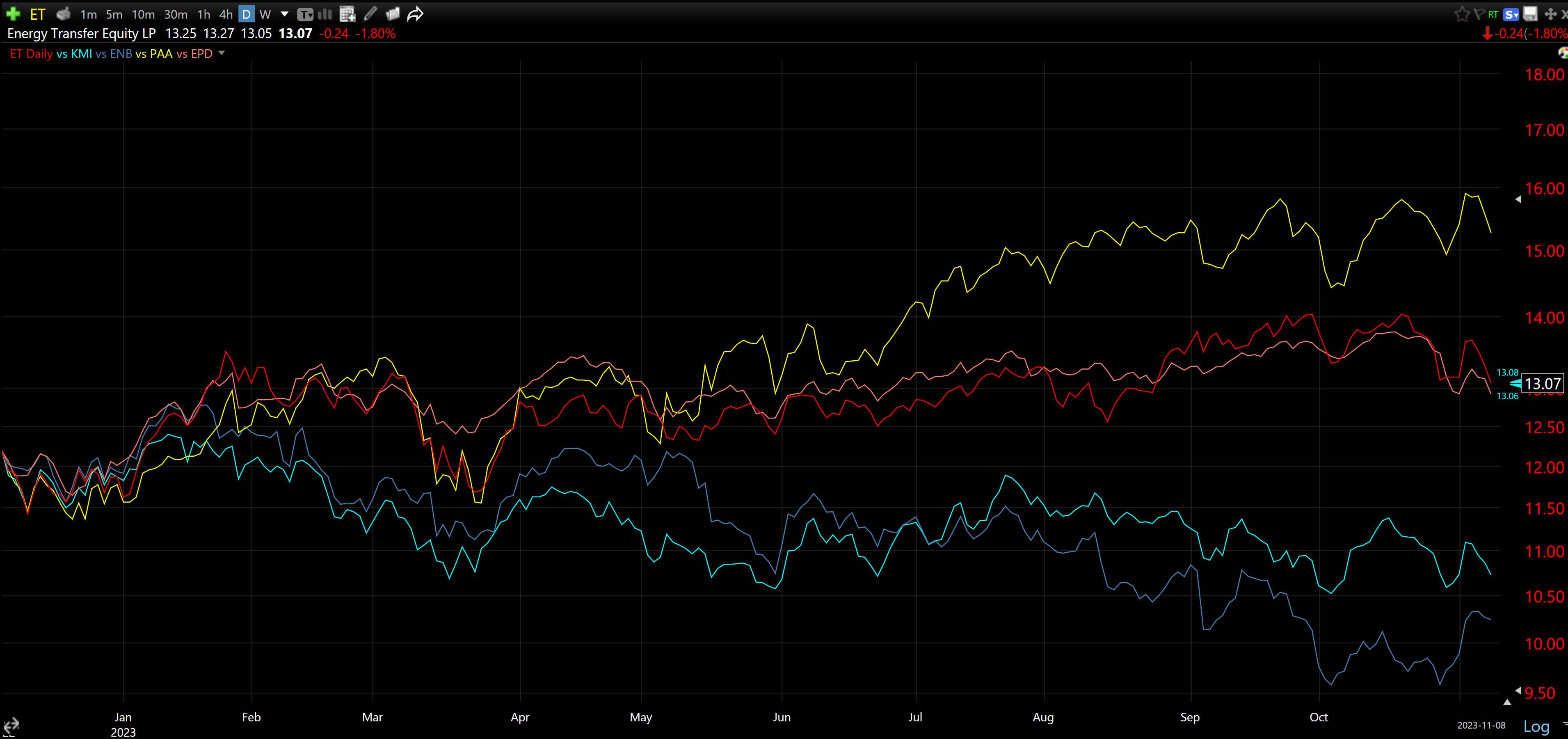

Often, one of the biggest red flags with respect to energy infrastructure companies is the balance sheet. Especially in an environment where the cost of debt is higher than we have seen in years. If you want to see which pipeline companies produced the best raw returns over the last year, line them up in order of lowest LTM Net Debt/EBITDA and there won't be any surprises. Using Energy Transfers' largest competitors: Kinder Morgan ( KMI ), Enterprise Products Partners ( EPD ), Enbridge ( ENB ), and Plains All American Pipeline ( PAA ), you get the following ratios. KMI - 4.77x, ET - 3.93x, ENB - 5.28x, EPD - 3.35x, PAA - 3.41x. Given where rates are, these companies are doing their best to keep the ratio below 4.0x. Some are doing better than others. Ranked in best market return over the last year:

- Plains All American Pipelines - 3.41x - 25% YTD

- Energy Transfer - 3.93x - 8% YTD

- Enterprise Product Partners - 3.35x - 6% YTD

- Kinder Morgan - 4.77x - (12%) YTD

- Enbridge - 5.28x - (16%) YTD

{kind=link}

If you stretch this chart out over the last two years, both Energy Transfer and Plains All American have returned ~30%. Three years and Energy Transfers pulls ahead at over 100% returns, while Plains All American has a very respectable 70% gain.

{kind=link}

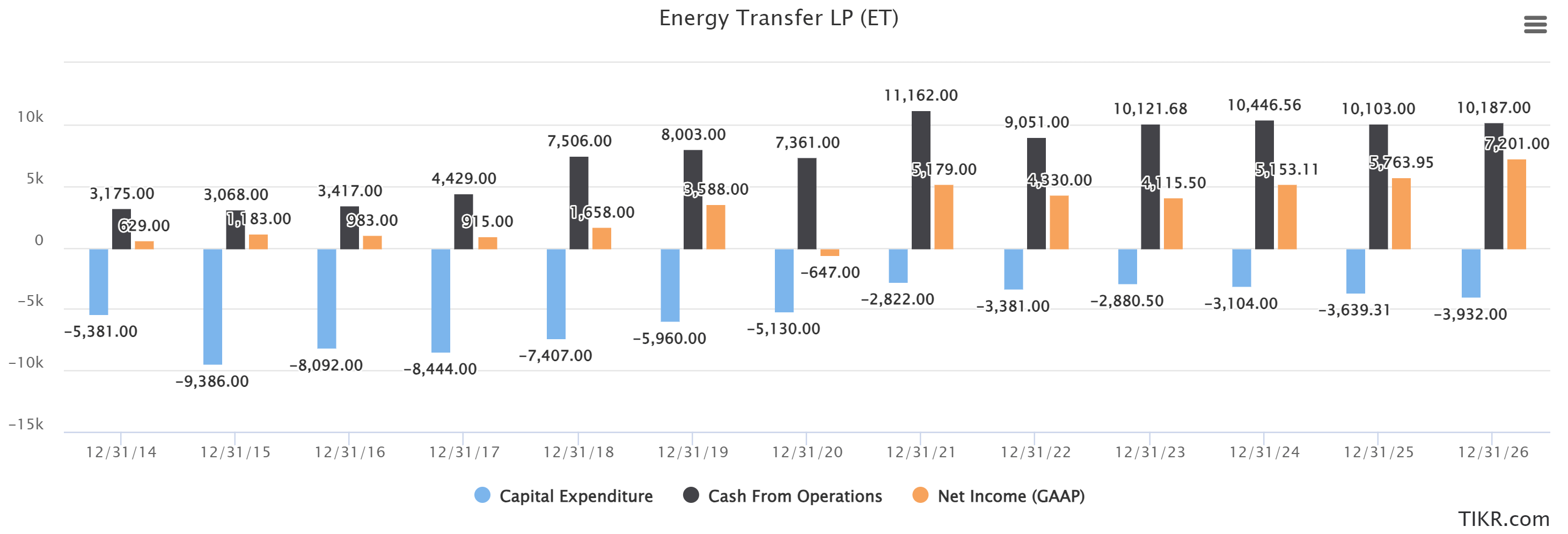

These two companies are head and shoulders above the rest concerning generating returns for investors over the last few years. Energy companies in general are in a sit back and relax state at this point. When I say relax, I mean count the money. Any company that has been around for some time committed a bunch of cash into various projects to help them grow organically from 2012-2015ish. As the industry crashed, we saw CapEx tighten up, and cash from operations started to grow as these projects paid off. Then Covid-19 hit and really put a damper on CapEx across the industry. Since then, commodity prices have gone nuts, and the companies have just sat back and counted the money flowing in. Looking below, we can see exactly that as I have laid out Energy Transfers CapEx, cash from operations, and net income all in the same chart.

{kind=link}

Now you have a company that is making more money than they ever have, and spending the least they have in over 10 years. I don't foresee an energy market where we see CapEx ramp up again either. I believe these companies will continue to rake in the cash, strengthening the balance sheet year after year. If Energy Transfer is going to grow, it will be through acquisition, just like the Lotus earlier this year. That equates to shareholders getting a larger piece of the pie as the years go on thanks to dividend increases and share buyback plans.

How About That 9.6% Yield?

This brings us to the main reason to own Energy Transfer. Many market enthusiasts will tell you that an average of 8-10% annual return on a portfolio over its lifetime is fantastic. Well, you can get that by simply owning Energy Transfer. The first question anyone will ask is: "Is it safe? Check out that payout ratio!". At first glance, it appears to be due for a cut with an earnings payout ratio of 116%. BUT, that is not how pipeline companies determine the dividend. Something to always keep in mind when looking at pipeline stocks like Energy Transfer is that net income is somewhat irrelevant due to the depreciation of assets. This drags on net income overall and makes things look worse than they are. So what's the go-to indicator, say hello to distributable cash flow, or DCF.

For 2023, Energy Transfer is expecting $7.50 billion in DCF. At 1.25 per share this year, the dividend will cost ~$3.93 billion. That works out to 52%, which is just fine. How does the rest get spent? 7-20% is allocated for debt paydown and share buybacks. The remaining 27-40% is tagged for growth capital . I believe we will see an increase in buybacks as the company can manage the debt very easily below 4.0x. This also means there's potential for an increase in the dividend.

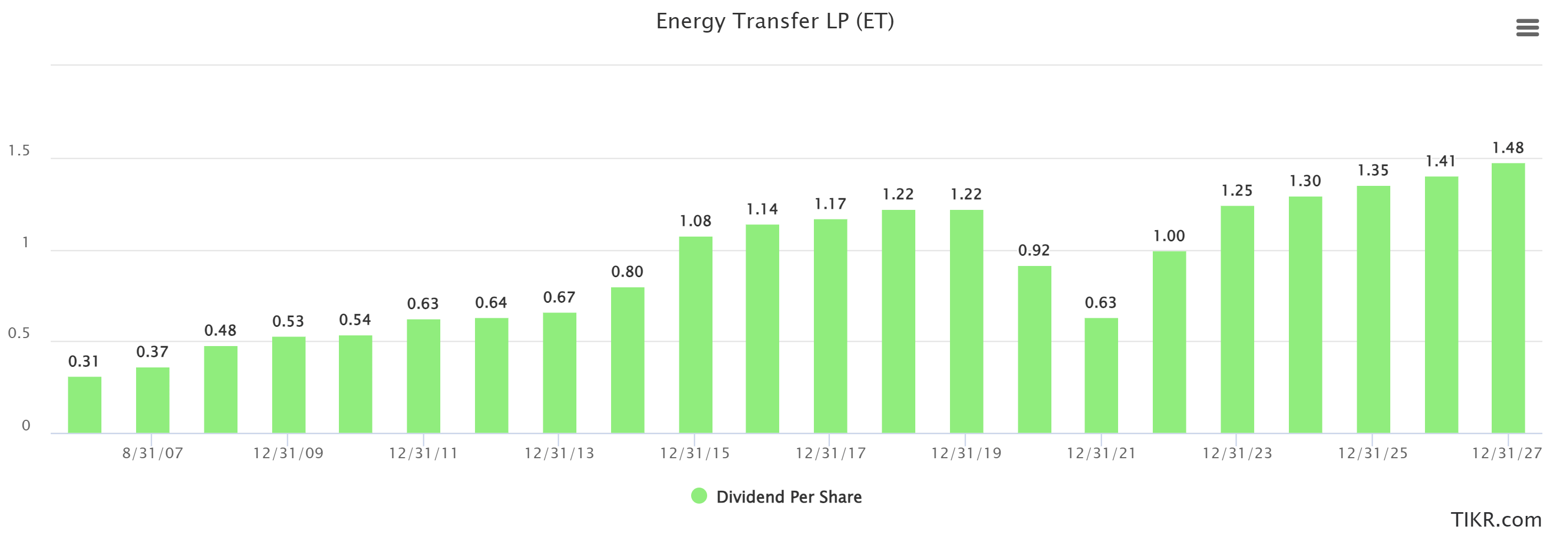

{kind=link}

Looking above, you can see the history of the dividend. Something they did during COVID-19, which I applaud is cutting the dividend. While many were very upset with the cut, it's much better to be safe than sorry. With the recent increase, the dividend for 2023 will be at an all-time high. Given the strong balance sheet and the growing revenue, I fully expect to see continued annual increases of 4%+.

In short, yes the dividend is safe.

What Are The Risks?

There are only 2 real risks here in my opinion.

The first is energy prices. Regardless of how much money Energy Transfer is bringing in or what the dividend is, if the price of oil tanks, so will the stock. Like it or not, they are tied together.

The second is the government/activists. Although necessary to move products across North America, they are out of favor for many. We may not see any major lines added ever again. It is as good as a coin flip with respect to getting energy projects approved right now. This will hurt the long-term growth. The good news is the company already has miles of pipe in the ground in key routes that will continue to pay dividends long-term, literally.

What Does The Price Say?

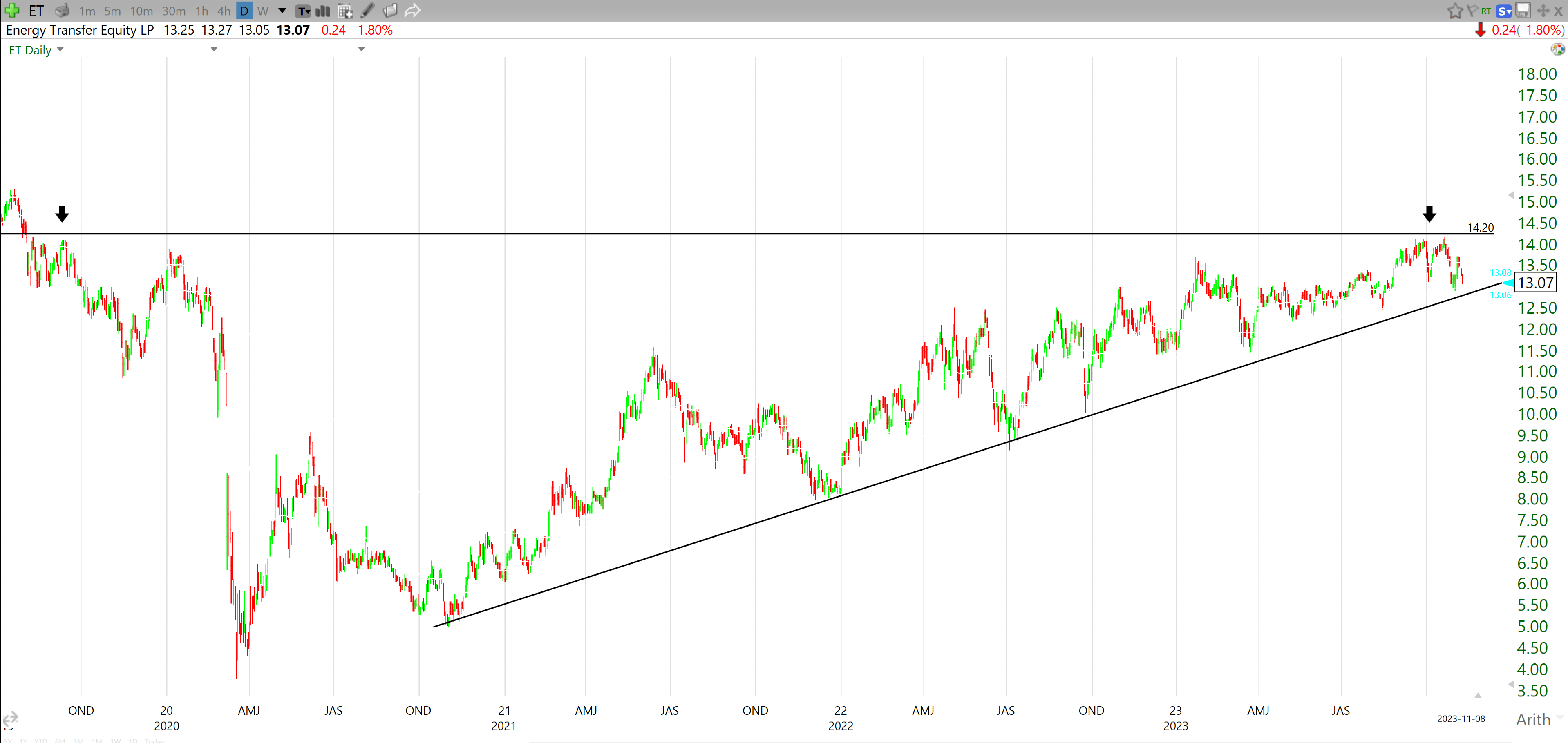

Yes, the dividend is fantastic. But what do we think the capital gains could look like over the next little while? I think they could continue to be quite good, but we're going to find out for sure in the near future. Looking below we can see a long trend line and a clear line of resistance at just under $14.20. The trend is always your friend until it's not.

{kind=link}

While I don't usually follow trend lines, when there's a strong one that is over 3 years long, it's hard to ignore. Especially as it approaches resistance. The reason is, we are either going to break through the resistance and move forward, or bounce back and test the trend. This leads me to my current price target of $16.00 which is about 23% from current levels.

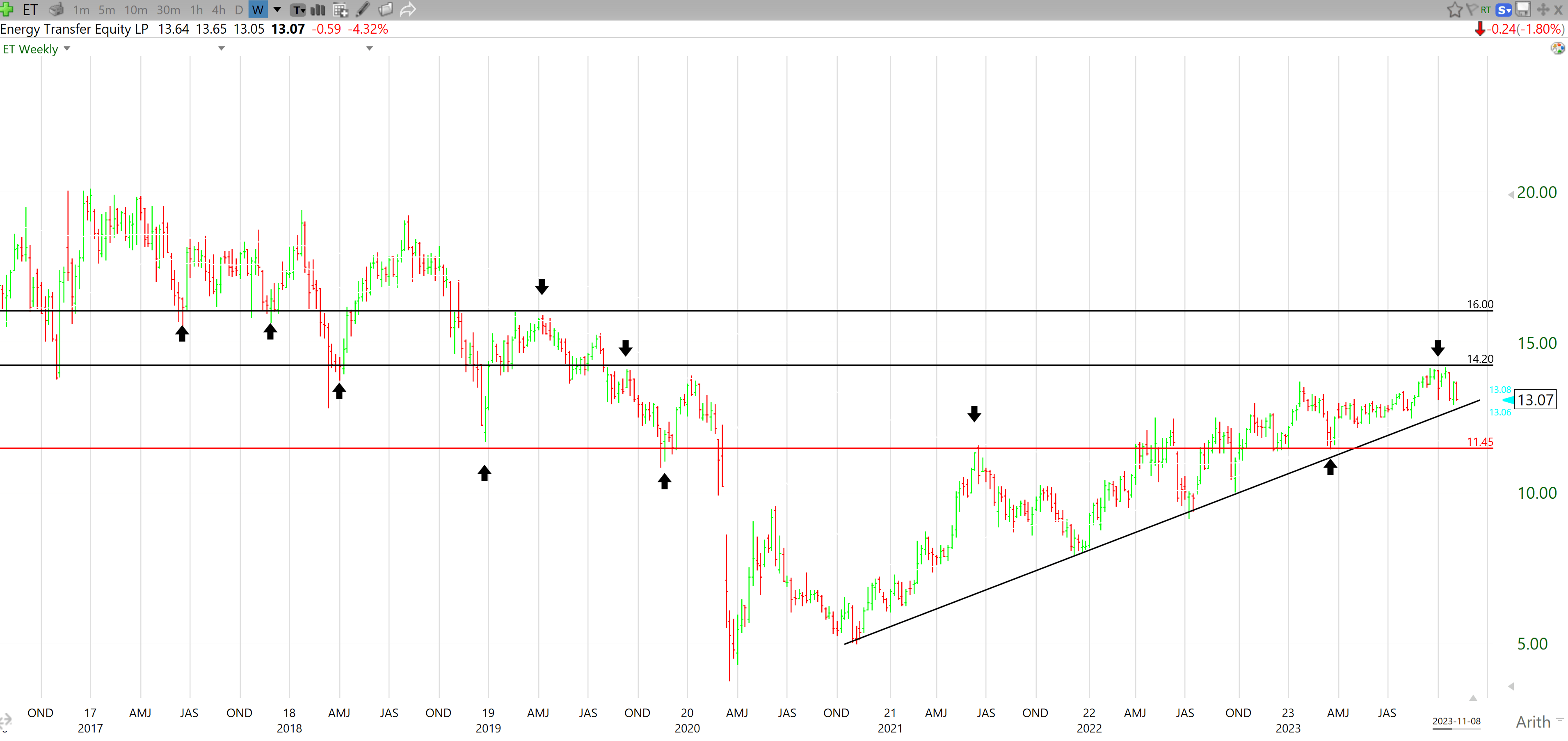

Looking below, you can see that after $14.20, the next line with multiple resistance points is $16.00. It really is as simple as that. The stock is finally back to pre-Covid levels and I think it will stay there.

{kind=link}

If it doesn't, there is a good point of support dating back to 2018 at $11.45. That leaves room for the stock to fall 13%. This would break the trend line and you don't want to own a stock that's swimming upstream. Now, the dividend does change things as you may want to tuck this away and just collect the yield for income or whatever it may be. I do think that in the long run, the stock will be just fine. Historically, infrastructure stocks are pretty slow movers. We could be due for some consolidation once we break through the $14.20 mark, which makes collecting the dividend easy. You're starting 9.6% up, which is a good place to be.

Wrap-Up?

As you can see, there is a lot to like about what Energy Transfer has to offer shareholders. The main draw is the very safe 9.6% dividend that is set to continue to grow. Obviously, the yield will change as the price does, but buying in at 9.6% is very attractive. With the strength in the balance sheet, this is a great stock for investors of all ages to own. It is for all of the reasons above that I am issuing a buy rating for the stock. You will sleep well at night with Energy Transfer in your portfolio.

For further details see:

Energy Transfer: The 9.6% Yield Your Portfolio Is Missing