ET - Energy Transfer: Time To Double Down

2023-11-27 12:00:00 ET

Summary

- Energy Transfer reported solid Q3 earnings results with increased adjusted EBITDA and record volumes transported.

- The company is benefiting from the tight natural gas market and the decline in Russian gas exports to Europe.

- Energy Transfer is expanding its business through acquisitions and is expected to continue to thrive in the current favorable environment.

Back in August, I called Energy Transfer ( ET ) the potential energy trade of the decade and reiterated my BUY rating. Since that time, the company reported decent Q3 earnings results and there are reasons to believe that Energy Transfer would continue to be one of the best investments in the energy sector in the foreseeable future.

The Restructuring Of The Energy Market Is Far From Over

At the beginning of this month, Energy Transfer reported its Q3 earnings results which showed that the company’s revenues decreased by 9.6% Y/Y to $20.74 billion, but were above the estimates by $350 million. What’s more important is that the adjusted EBITDA increased from $3.09 billion a year ago to $3.54 billion in Q3. Those were solid results and there are reasons to believe that Energy Transfer would be able to exceed most of the expectations in the future thanks to the several growth catalysts that the company has going for it.

If we look closely at the report, we’ll see that the last few months were the best in the company’s history in terms of transported volumes. The NGL transportation volumes increased by 14% to 2.2 MMbpd, while the fractioned volumes were up 9% to 1 MMbpd. At the same time, thanks to the increase in international demand, the company’s NGL export volumes were up 20% in Q3, which helped Energy Transfer account for almost 40% of all U.S. NGL exports. The company will likely increase its market share even more once the expansion of its Nederland export terminal is completed in 2025. The same is true for the midstream segment, as gathered gas volumes increased by 4% to 19.8 million MMBtu/day.

What’s more is that as the volume increases, the prices are unlikely to fall anytime soon due to the tight natural gas market. In most of my previous articles on Energy Transfer and Exxon Mobil ( XOM ), I have noted that due to Russia’s war against Ukraine, the energy market is in the middle of a massive restructuring that would last for a few years as supplies are being diverged while the demand isn’t decreasing.

The International Energy Agency in its latest major report on natural gas stated that the market remains tight and as Russia’s piped exports to Europe are declining, all the other non-Russia natural gas actors such as the United States use this as an opportunity to expand their presence on the old continent. This would remain to be the case for a while as the report states that the Russian gas exports to the European Union dropped from 140 bcm/yr in 2021 to around 20 – 25 bcm/yr in 2023 and would likely decrease even more to 15.75 bcm/yr from 2025 as others capture the Russian market share.

Considering this, it makes sense to believe that the Energy Transfer midstream business will continue to thrive as the current favorable environment is likely going to lead to a further increase in transportation volumes at elevated prices due to the tight market.

More Growth On The Horizon

In such an environment, it makes sense for Energy Transfer to accelerate the expansion of its business by acquiring its competitors and realizing synergies. Earlier this month, the company completed the acquisition of Crestwood Equity Partners, which would help it gain a foothold in the Powder River Basin, increase the number of its downstream assets, and realize around $40 million in annual synergies.

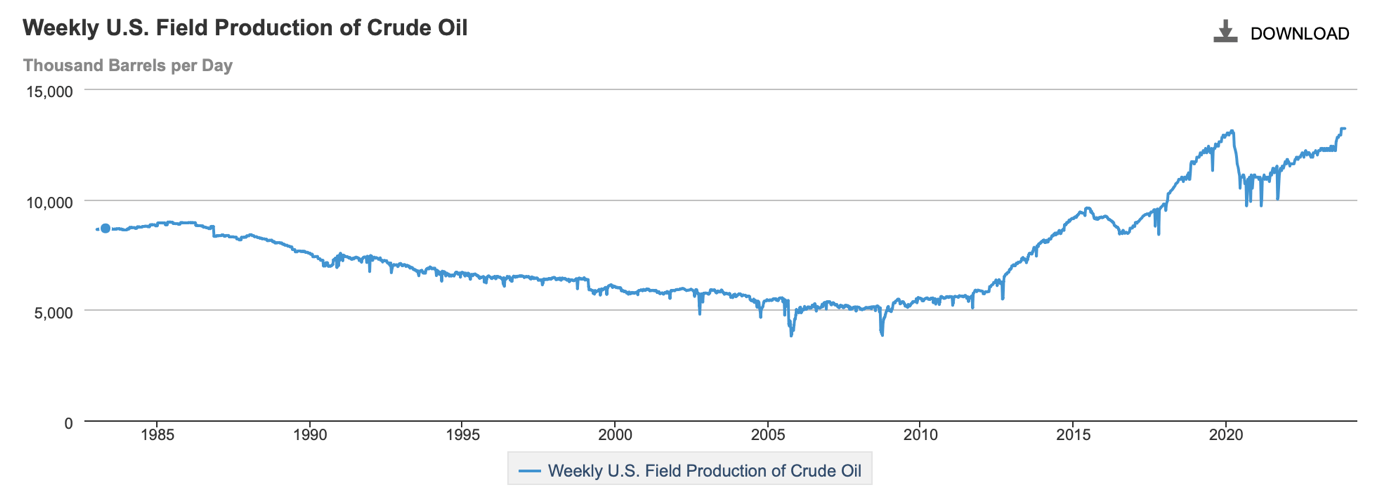

At the same time, the acquisition of Lotus Midstream earlier this year is already benefitting Energy Transfer, as its crude transportation volumes in Q3 were up 23% to 5.6 MMbpd. Considering that the United States has become the biggest producer of crude oil and recently its oil production has exceeded the pre-pandemic levels to over 13 MMbpd, it makes sense to believe that the transportation volumes are not going to decrease anytime soon. As such, Energy Transfer’s 2023 acquisitions are certainly going to continue to give a great boost to the company’s performance in the foreseeable future.

{kind=link}

U.S. Production Of Crude Oil (EIA)

Is Energy Transfer Still A ‘BUY’?

When it comes to Energy Transfer’s financial well-being and its excessive debt load, it’s safe to say that the situation is more than manageable at this point. Even though the company had $47.01 billion in long-term debt and only around $2.12 billion in liquidity at the end of Q3, its leverage ratio has been improving. Considering that for the midstream company, a standard leverage ratio is somewhere in the range from 4x to 5x, Energy Transfer is no different from its peers as it expects to have a leverage ratio of around 4x to 4.5x in the foreseeable future. At the same time, S&P increased its credit rating to BBB with a stable outlook a few months ago and Fitch would likely do the same thing after the company successfully priced $4 billion in senior notes and used its proceeds to cover some of its borrowing.

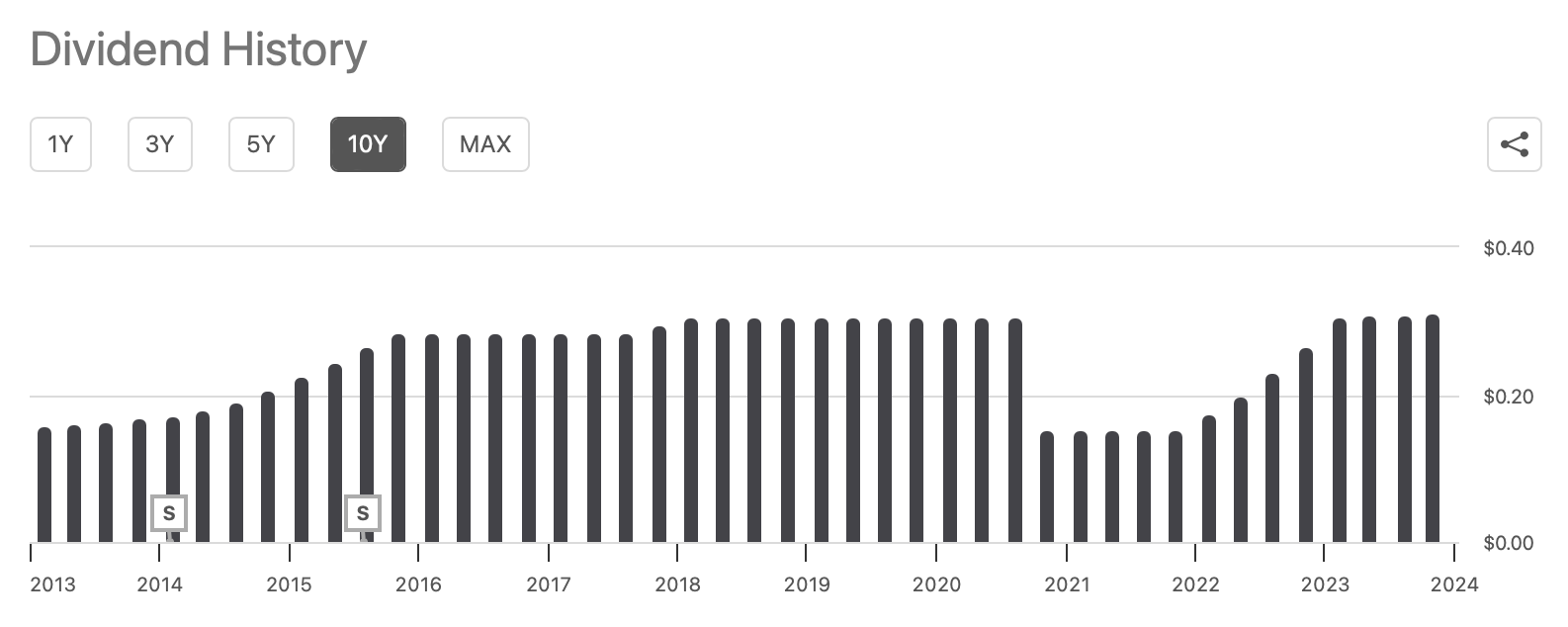

What’s more, is that Energy Transfer is also able to reward its investors as it improves its balance sheet. In Q3, the distributable cash flow assigned to partners was $1.99 billion, up from $1.58 billion a year ago. Given the favorable macro environment, which was described earlier, it’s likely that Energy Transfer would continue to transport record volumes that would lead to higher adjusted EBITDA and potentially bigger payments to investors next year.

{kind=link}

Energy Transfer's Dividend History (Seeking Alpha)

Considering all of this, it’s safe to say that there’s nothing not to like about Energy Transfer at this stage. The company expects to generate an adjusted EBITDA of $13.5 billion to $13.6 billion in FY23, while its capital run rate is expected to be in the range of $2 billion to $3 billion this year.

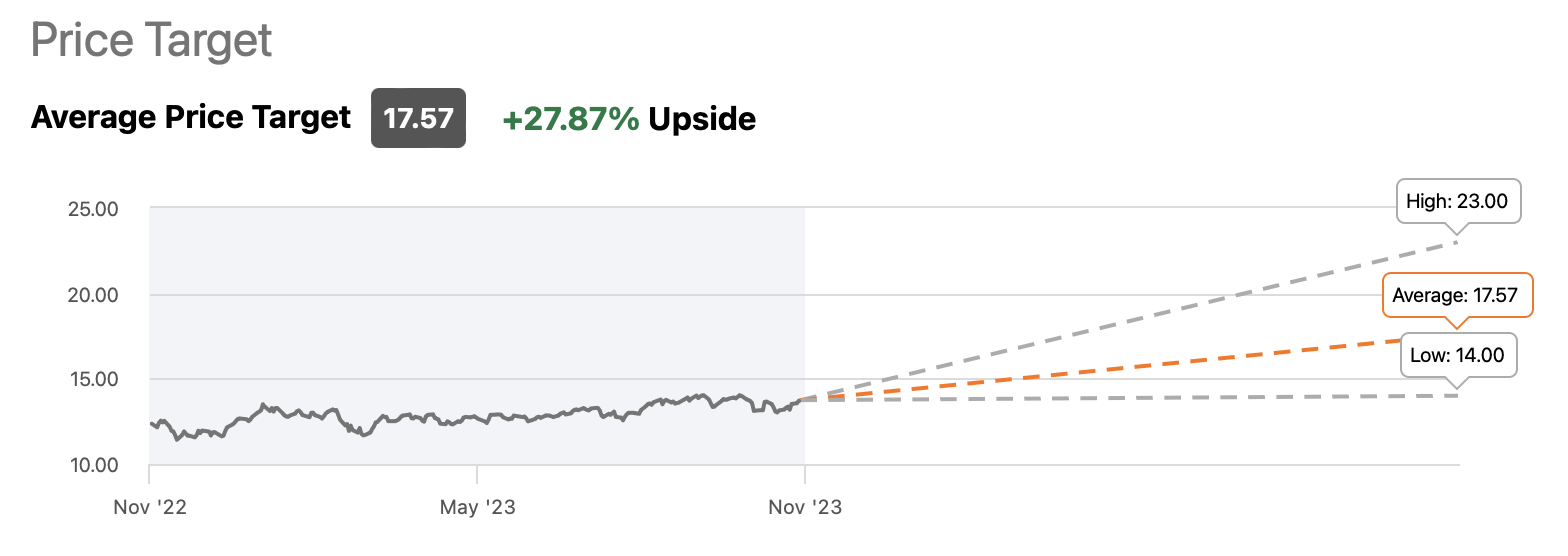

What’s more is that Energy Transfer trades at a forward P/E of only 10x against the market average forward P/E of 25x, while the company’s forward P/S ratio is less than 1x against the sector’s average ratio of 1.3x. At the same time, Energy Transfer has an enterprise value of over $100 billion, and yet its market cap of ~$43 billion is similar to its much smaller competitors, which indicates that the company is most likely undervalued. Add to all of this the fact that Energy Transfer offers a forward yield of ~9% at the current price, while the street believes that its upside could be nearly 30% and it becomes obvious that there’s nothing not to like about the company at this stage.

{kind=link}

Energy Transfer's Consensus Price Target (Seeking Alpha)

Major Risks To Consider

The biggest risk for Energy Transfer is without a doubt the potential worsening of the macro conditions that could result in lower economic activity and less demand for energy, which would lead to a decrease in transported volumes. While there are no reasons to panic right now, given the latest positive GDP and CPI data, it’s still something that investors need to consider before deciding whether it’s worth it to invest in Energy Transfer at this stage.

Another major risk is the inability of Energy Transfer to complete its Lake Charles LNG export facility on time or complete it when it’s no longer needed. There has been a lot of uncertainty in recent years around this project, which is expected to give Energy Transfer an entrance into the LNG export business. The company’s request to extend the deadline to complete the project has been denied by the Department of Energy earlier this year and currently, the company needs to complete it by December 2025, which it believes won’t be possible at this stage.

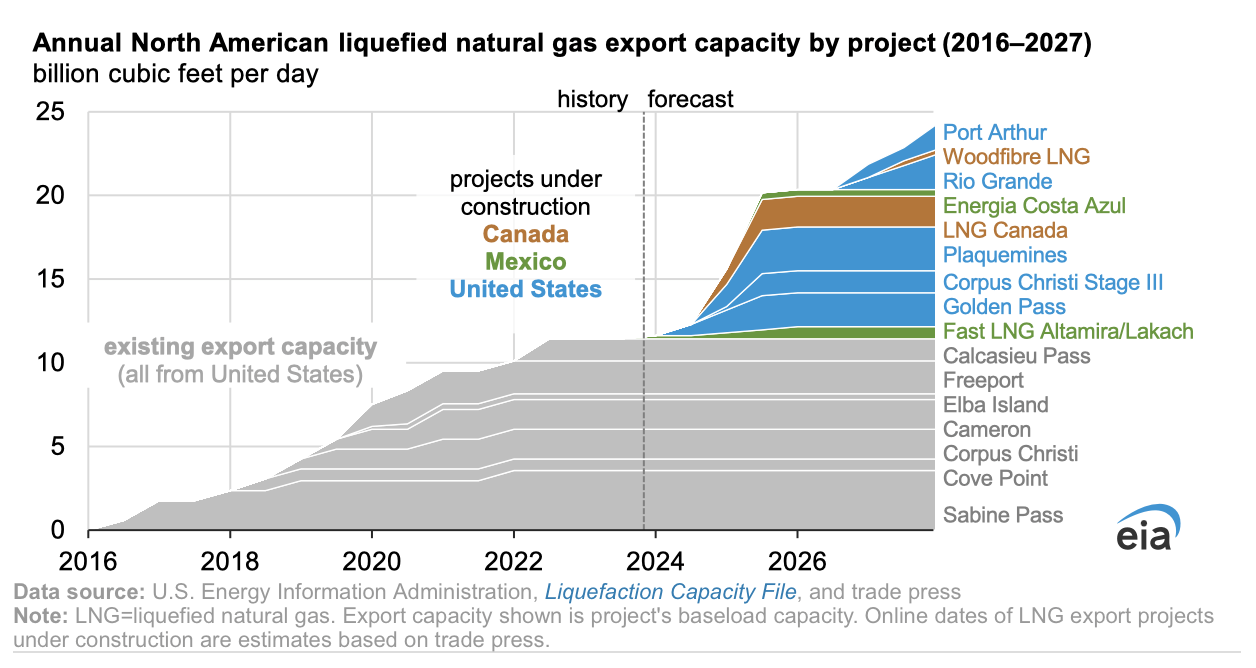

While the management looks for ways to get approval for the extension next year, my biggest issue with the Lake Charles LNG export facility is whether it’s even worth pursuing it at this stage. The IAE report that was mentioned earlier in the article stated that the global LNG supply is expected to increase by 25% between 2022 and 2026 and most of the supply increase will happen in 2025 and 2026.

The EIA in a separate report expects the North American LNG export capacity to increase substantially in the upcoming years thanks to the completion of major export facilities on the continent. Considering that Energy Transfer won’t be able to complete its export facility by the end of 2025, it’s doubtful that the project would be able to generate solid returns after that period when the normalization of the natural gas market would likely take place. Even though the management has been vocal in its commitment to retain only a 20% stake in the export facility so that it doesn’t fund it on its own, the longer it takes to reach a final investment decision and extend the deadline, the less attractive the project will become.

{kind=link}

North American LNG Export Capacity Forecast (EIA)

The Bottom Line

The ongoing restructuring of the energy market creates a favorable environment for Energy Transfer in which it can continue to generate solid returns in the foreseeable future. While there are some risks associated with the company, its overall business remains robust, and it has more than enough growth catalysts that could help it exceed expectations and reward its investors at the same time.

For further details see:

Energy Transfer: Time To Double Down