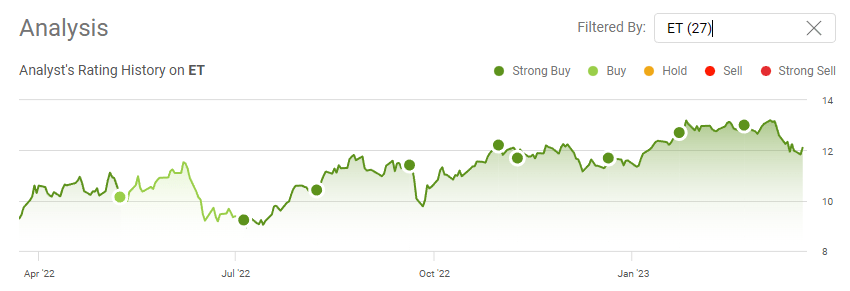

ET - Energy Transfer: Tollbooth To A 10% Dividend Yield Regardless Of Commodity Pricing

2023-03-24 09:00:00 ET

Summary

- The EIA released their latest energy outlook and it shows increased production in fossil fuels through 2050.

- As fossil fuel production increases, the need for energy infrastructure should increase causing producers to contract additional services and generate additional revenue for ET.

- The pullback has made ET more attractive, and this is an energy tollbooth with 90% of its adjusted EBITDA tied to fee-based contracts.

- I think shares are fairly valued between $19-$21 as this places ET inline with its peer group valuations and your getting paid 10% to wait.

The debate is over about how the Fed would lean, and on Wednesday, the Fed raised rates by an additional 25 bps. Jerome Powell and the rest of the policymakers seemed unphased by the banking scenario, and they're committed to reducing inflation at all costs. The Fed was outright hawkish, and Mr. Powell stated that regardless of tighter credit conditions, rate cuts will not be in the Feds base case for 2023. We are now at the highest Fed Funds Rate since October of 2007, and the Fed Dot Plot sees rates peaking at 5.1% in 2023 and possibly coming down to 4.3% in 2024. The risk on trade continues to feel pressure from the rising rate environment, and nobody can predict when the Fed will pivot or how drastic the rate decline will be. No matter what the Fed does or how low commodity pricing goes, I remain very bullish on Energy Transfer ( ET ) as I believe it's the most attractive energy infrastructure company among its peers. The U.S Energy Information Administration ((EIA)) released its Annual Energy Outlook 2023 on March 16, 2023. It is abundantly clear that oil and gas are here to stay as production for oil and gas will increase through 2050 while the United States remains a net exporter of petroleum products through 2050. ET is a tollbooth collecting fees as fossil fuels pass through its network to their final destination. Everyone needs sustainable energy, and no matter what the external factors impacting the market are, ET has become an irreplaceable company critical to our way of life. I think the recent dip is a buying opportunity for long-term investors.

{kind=link}

Data from EIA's critical energy report couldn't be more straightforward

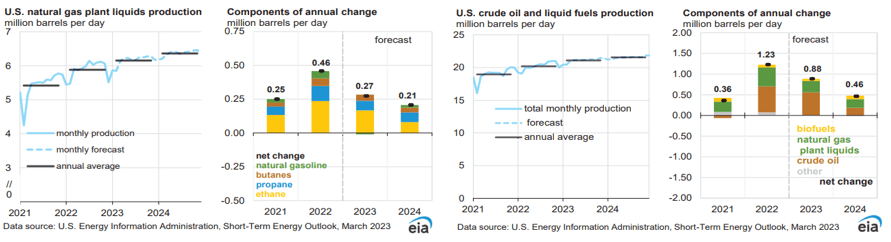

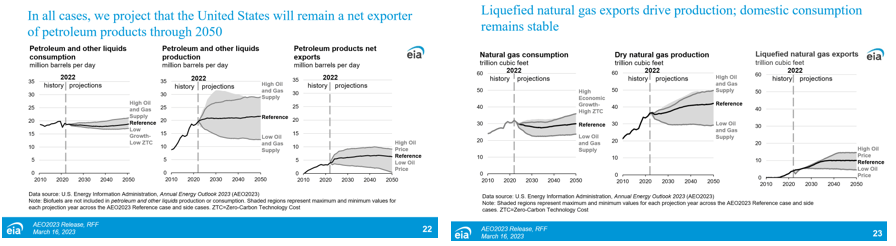

There are two critical reports that the EIA publishes, which include the International Energy Outlook (published every two years) and the Annual Energy Outlook . The Short-Term Energy Outlook from the EIA is clearly indicating that U.S crude oil and liquid fuel production, in addition to natural gas production, will increase over the next two years. The reference case in the Annual Energy Outlook from the EIA projects that petroleum and other liquid production will slightly increase from now through 2050, and dry natural gas production will increase by roughly 20% through 2050. The EIA is also projecting that the United States will remain a net exporter of petroleum products and liquified natural gas ((LNG)) through 2050. The equation is simple, the more fossil fuels are produced, the need for transportation, storage, and refining will increase, and midstream operators will continue to see elevated needs for their services.

{kind=link}

{kind=link}

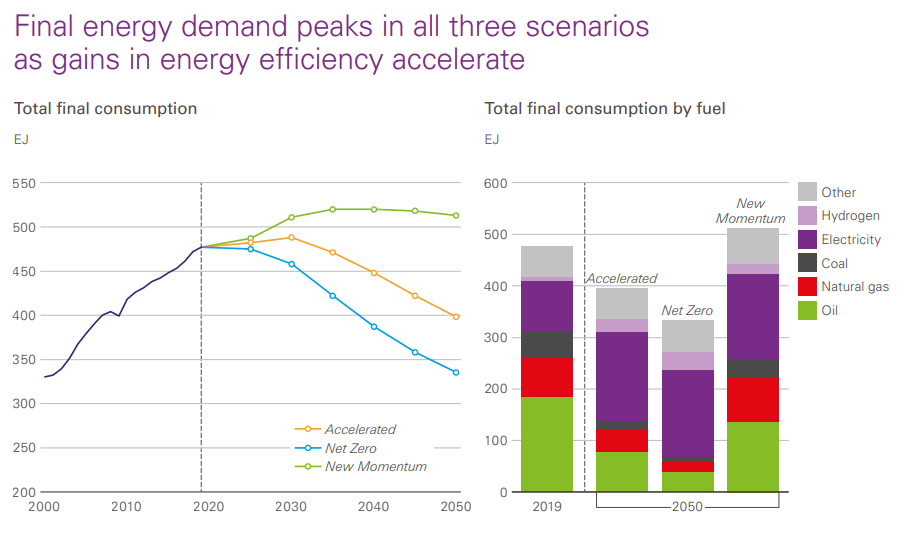

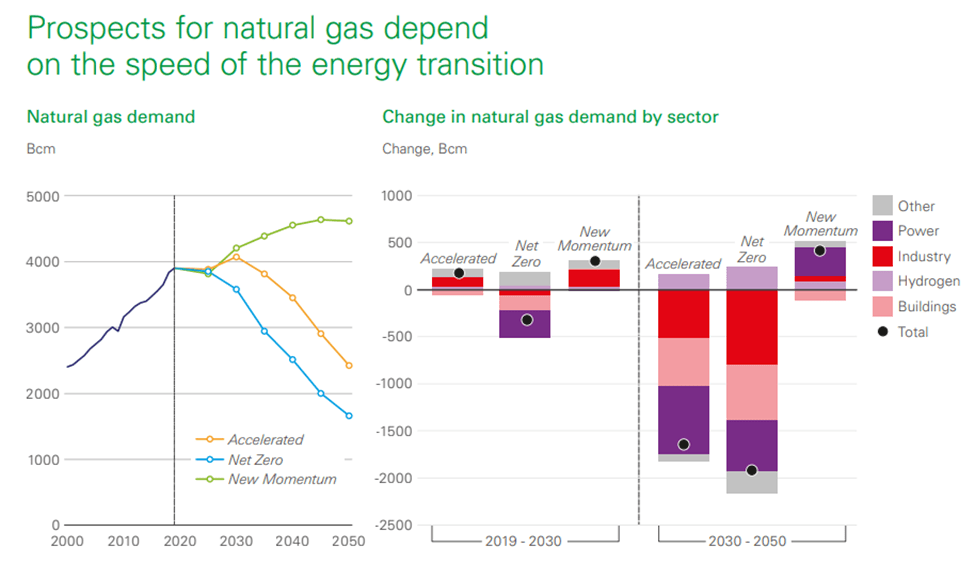

Outside of government agencies, I feel that BP p.l.c ( BP ) puts out the best comprehensive research in the energy industry. Their annual energy outlook provides a well-rounded look at the energy sector as a whole. The new momentum outlined in BP's Energy Outlook 2023 edition clearly indicates that the demand for energy will not have a lower utilization rate than the amount of energy consumed today. BP has provided a new momentum scenario that takes into consideration all of the changes the energy landscape has endured throughout 2022. The energy transition that grabbed media headlines and made oil & gas out to be obsolete isn't the picture being painted by the EIA or BP, which has been at the forefront of transitioning their business. Looking out to 2050, BP is seeing the world's energy consumption increasing while the amount of natural gas consumed increases and the amount of oil consumed slightly decreases. The common theme is that fossil fuels will play a critical role in humanity's way of life for decades to come.

{kind=link}

{kind=link}

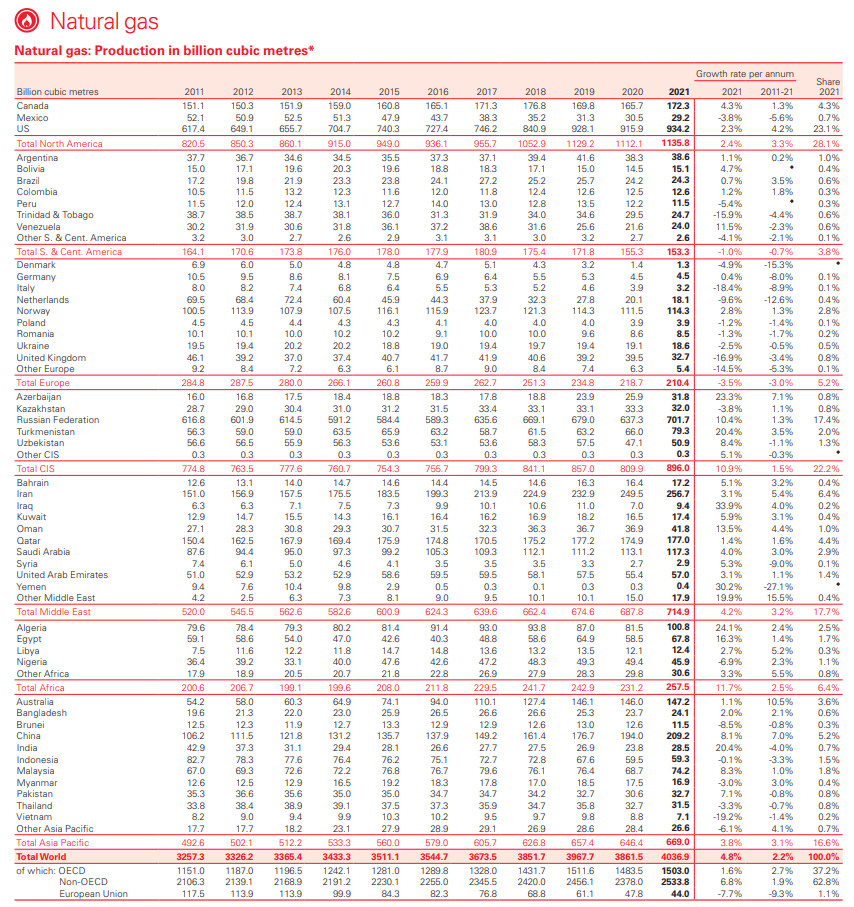

BP has not released its 2023 Statistical Review of World Energy yet, and I look to this for the drilling data. In the 2022 Statistical Review of World Energy BP provided a comprehensive breakdown of the global production of natural gas. The United States produced 934.2 billion cubic meters of natural gas throughout 2021, which was 23.14% of the global natural gas production level. When I add Canada to this figure, the global production increases to 27.41% as Canada produced 172.3 billion cubic meters of natural gas in 2021. Production has continued to increase, and the United States continues to be the larger producer of oil & gas globally. When oil & gas is produced, it needs to be refined, stored, and transported. Based on the global production and utilization trends from the EIA, and BP I don't see a world without fossil fuels for at least three decades if not longer, and the need for energy infrastructure will increase, not decline.

{kind=link}

Energy Transfer is a tollbooth for American energy, collecting fees throughout the value chain

I can't predict the future, but when the EIA is telling us that fossil fuels will be produced at a higher level in 2050 than they are in 2023, I pay attention. I put the political posturing aside, and I look at the hard data that is being presented. The EIA is telling us that over the next 27 years, fossil fuel production will grow and that the United States will be a net exporter of these products. From an investment standpoint, I look at the areas that benefit from this scenario, and the energy infrastructure community is at the top of the list.

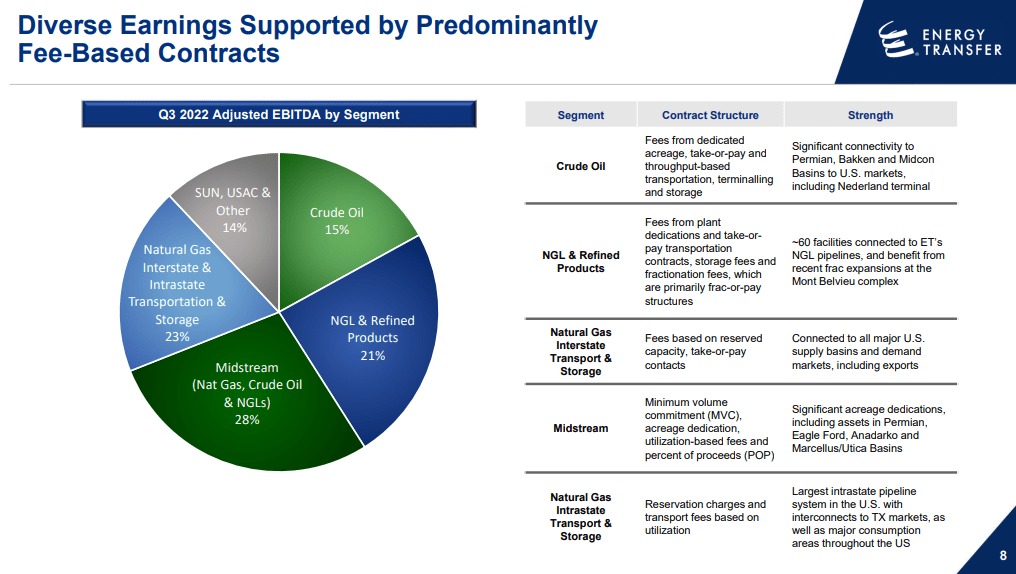

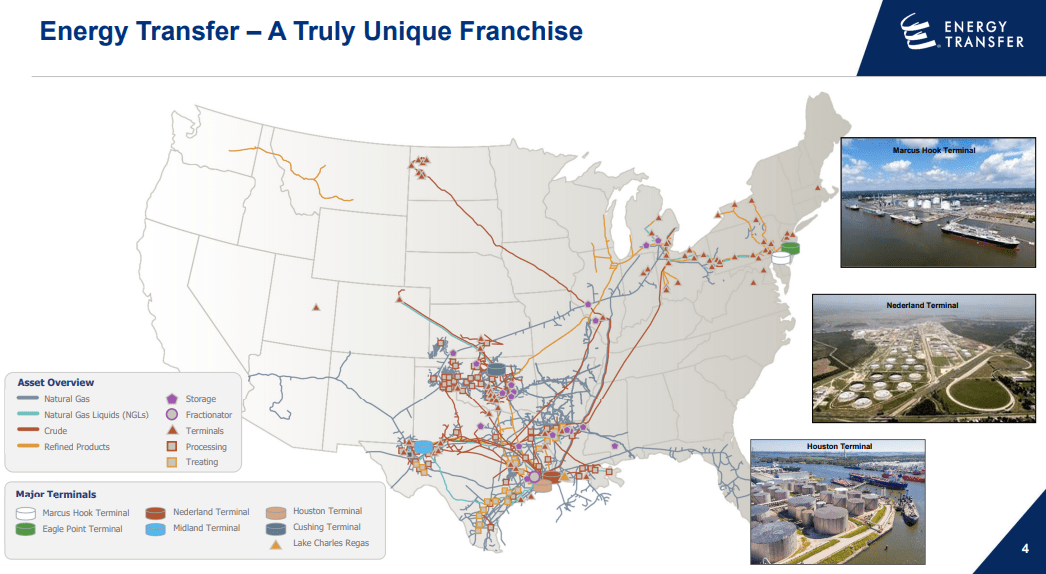

ET is a vertically integrated energy transfer company, and happens to have the largest infrastructure in the United States. ET has roughly 120,000 miles of pipeline, and its services span across natural gas, crude, natural gas liquids (NGLs), refined products, and LNG. When I say vertically integrated, I use this term because ET owns and operates every aspect throughout the value chain. With crude, ET collects fees throughout the gathering lines, storage, transmission lines, storage and refining, and transporting to end users. In natural gas, it's similar, ET collects fees from the gathering lines, processing and treating, transmission lines, storage, and transporting to the end users.

{kind=link}

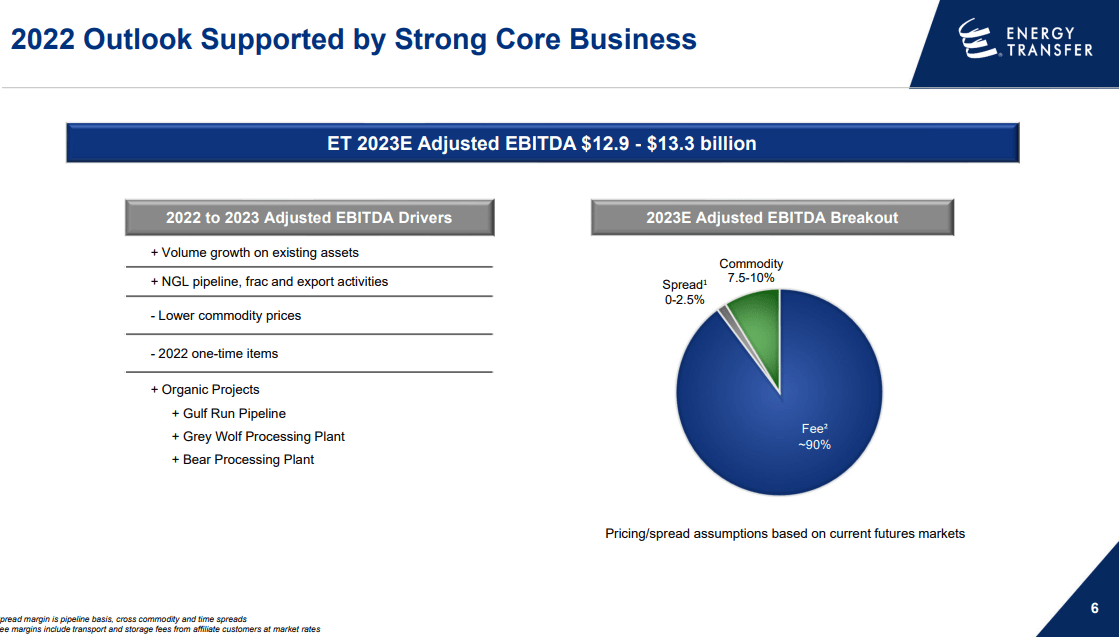

ET's business is predominantly protected by one of my favorite structures, which is fee-based contracts. 90% of ET's 2023 Adjusted EBITDA is tied to fee-based contracts. This is where a fixed rate is negotiated upfront between ET and its customers. The revenue which is generated from fee-based contracts is based on volume, which passes through the system as the fee has already been set. Fee-based contracts are also a mitigation method to an uncertain commodity market as fees are agreed upon upfront, so whether commodity prices increase or decrease, ET is generating a revenue amount that is attractive to their overall business.

{kind=link}

I look at ET as a tollbooth as it has 90% of its services tied to fee-based contracts, and its infrastructure is required to move fossil fuels. In 2022, ET generated $89.88 billion in revenue, of which $9.25 billion was DCF on a consolidated level. ET produced $7.4 billion of DCF attributable to partners of ET. There was $4.4 billion of excess cash flow remaining after distributions from the $7.4 billion attributable to partners of ET. The largest energy infrastructure in the United States is operated by ET, and it's a profitable business with an outlook that continues to grow. Putting the Fed aside, and the economic uncertainty, everyone needs sustainable energy, and fossil fuels play an important role in powering the country.

{kind=link}

After the slight selloff units of ET look very attractive

I track the market cap, enterprise value, revenue, Adjusted EBITDA, distributable cash flow ((DCF)), and total debt so I can compare the following ratios, Adjusted EBITDA to market cap, EV to Adjusted EBITDA, DCF to Market Cap, Debt to Adjusted EBITDA, and Price to Sales. The energy infrastructure companies I compare ET against are:

- Enterprise Products Partners ( EPD )

- MPLX LP ( MPLX )

- Kinder Morgan ( KMI )

- Plains All American Pipeline ( PAA )

- Williams Companies ( WMB )

- Targa Resources ( TRGP )

- Magellan Midstream Partners ( MMP )

- ONEOK ( OKE )

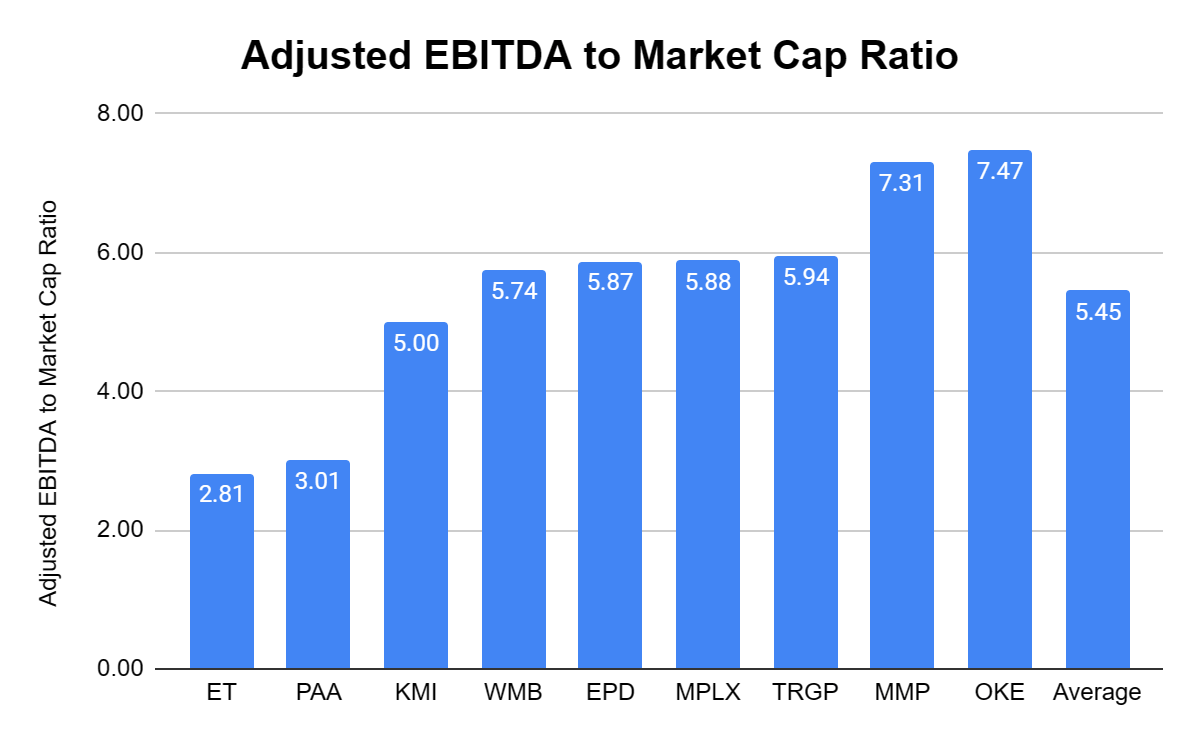

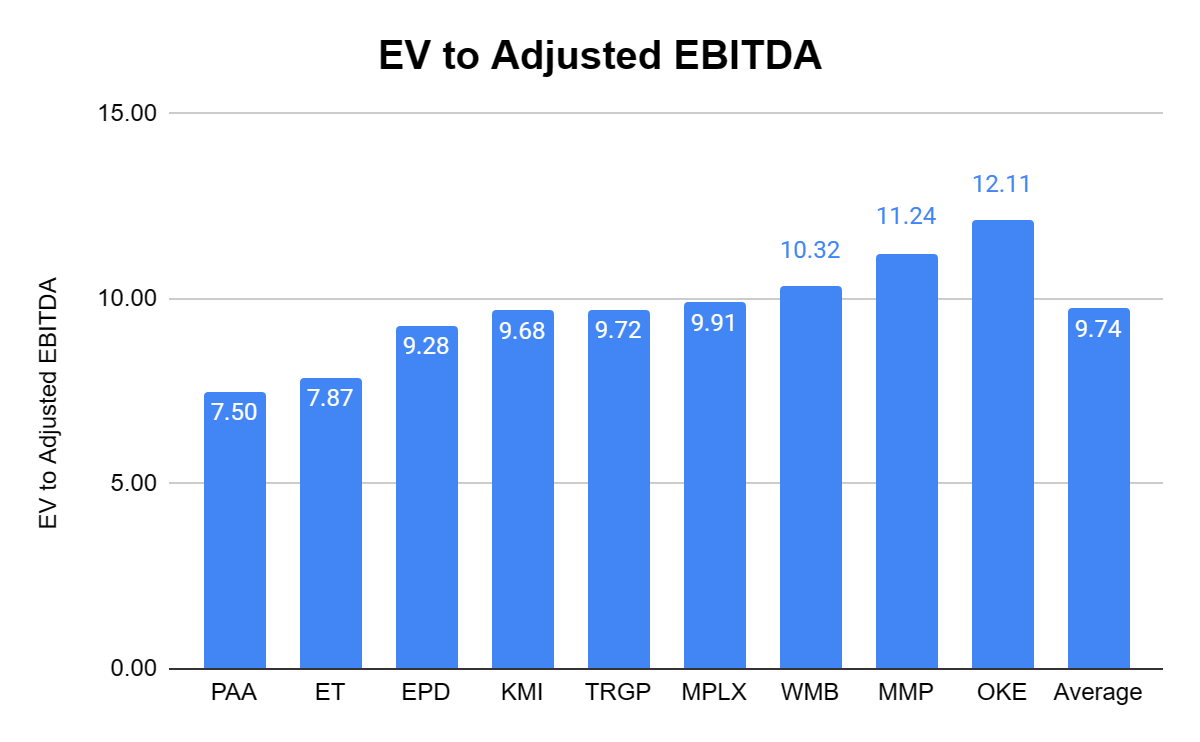

ET trades at an Adjusted EBITDA to market cap ratio of 2.81x compared to the peer group average of 5.45x. MMP and OKE are above 7x, and MPLX, KMI, EPD, WMB, and TRG trade between 5-6x. ET is not given the premium on their Adjusted EBITDA that their peers are, yet ET generated $13.09 billion of Adjusted EBITDA in 2022, and the next largest amount came from EPD with $9.31 billion . The EV to Adjusted EBITDA ratio is popular because it compares the value of a company, debt included, to the company's cash earnings less non-cash expenses. ET has the second lowest EV to Adjusted EBITDA ratio at 7.87x, which is significantly lower than the peer group average of 9.73x. ET also looks significantly undervalued by this metric as well.

{kind=link}

{kind=link}

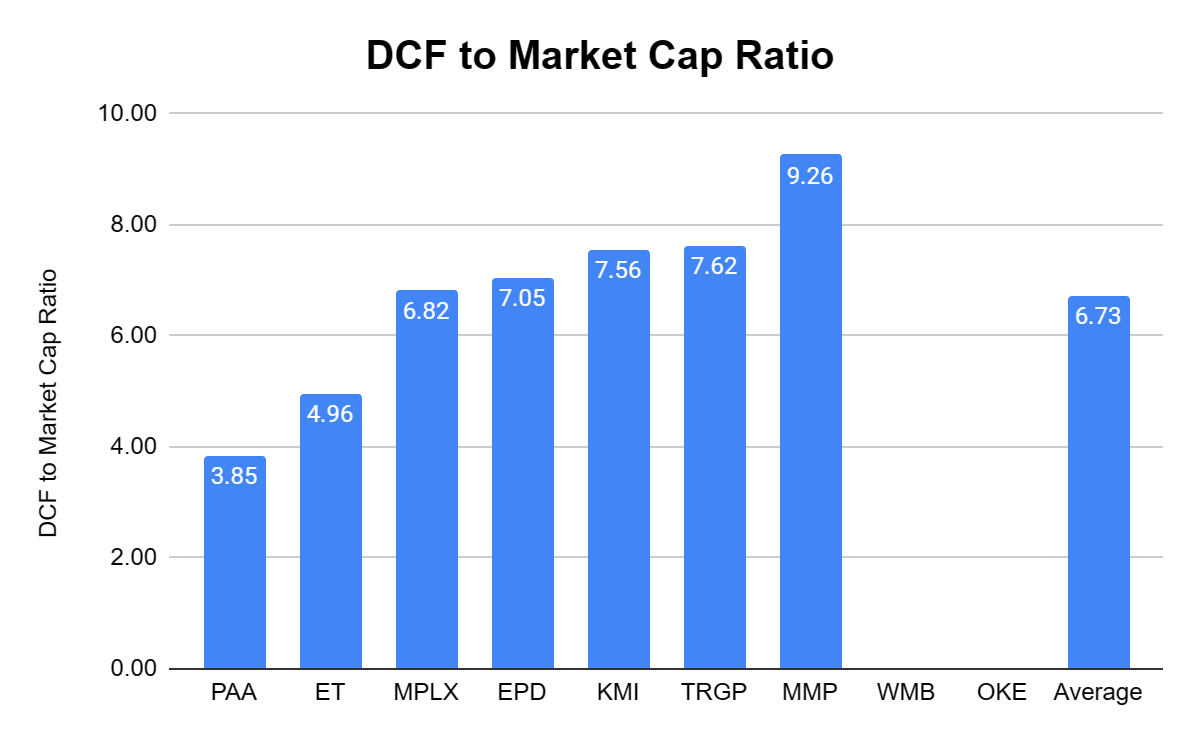

DCF is the lifeblood for investors of energy infrastructure companies as this is where distributions are paid from and how capital growth projects are funded. I want to pay the lowest multiple I can for a company's DCF. WMB and OKE don't provide the DCF in their reports, so they are excluded from this metric. ET has the second lowest DCF to market cap ratio of 4.96x, which fell from 5.37x the last time I looked at this metric. Compared to its peer group average of 7.21x, ET looks inexpensive. ET generates $7.4 billion of DCF attributable to its partners, and the market continues to discount its market cap on this metric.

{kind=link}

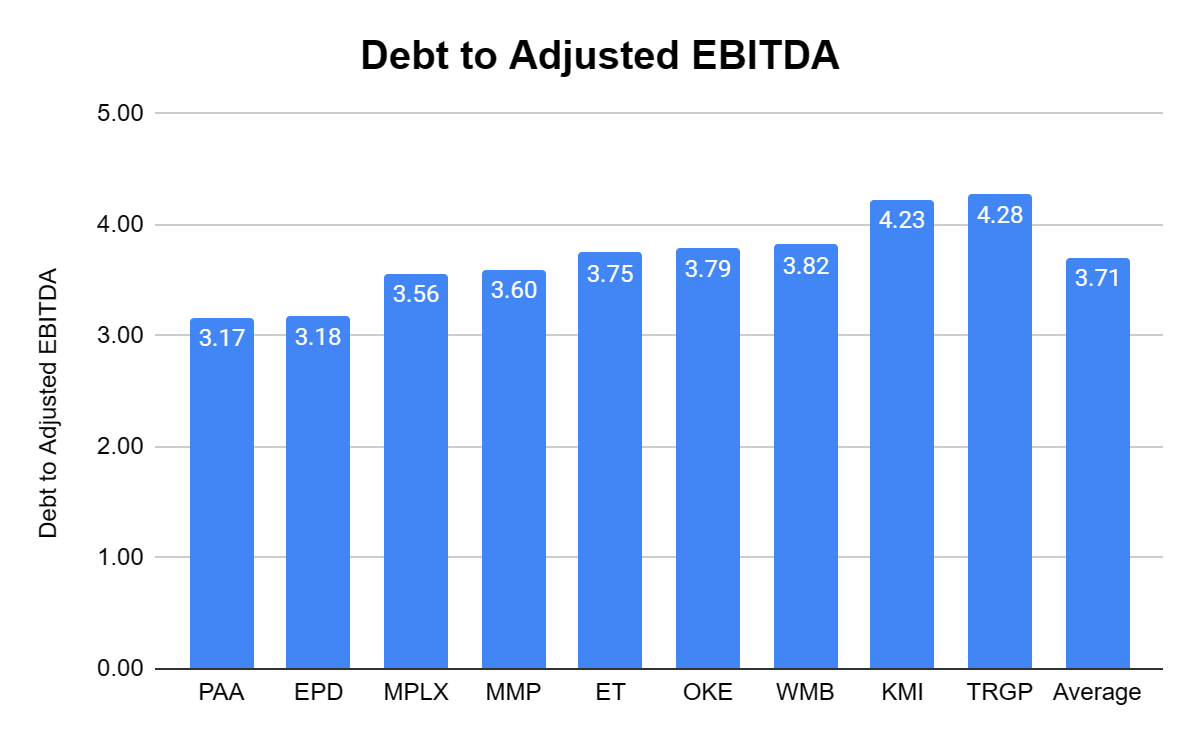

In several articles, there have been comments about ET's debt level. In a rising-rate environment, debt should be looked at as variable debt, and the higher cost of capital can cripple a company. ET has a debt to Adjusted EBITDA ratio of 3.75x, which is slightly above the peer group average of 3.71x. There is nothing abnormal about this level as ET is in the middle of the pack, and the lowest ratio is 3.17x. Due to ET being in line with its peers and the amount of Adjusted EBITDA and DCF it produces I am not concerned about ET meeting its debt obligations.

{kind=link}

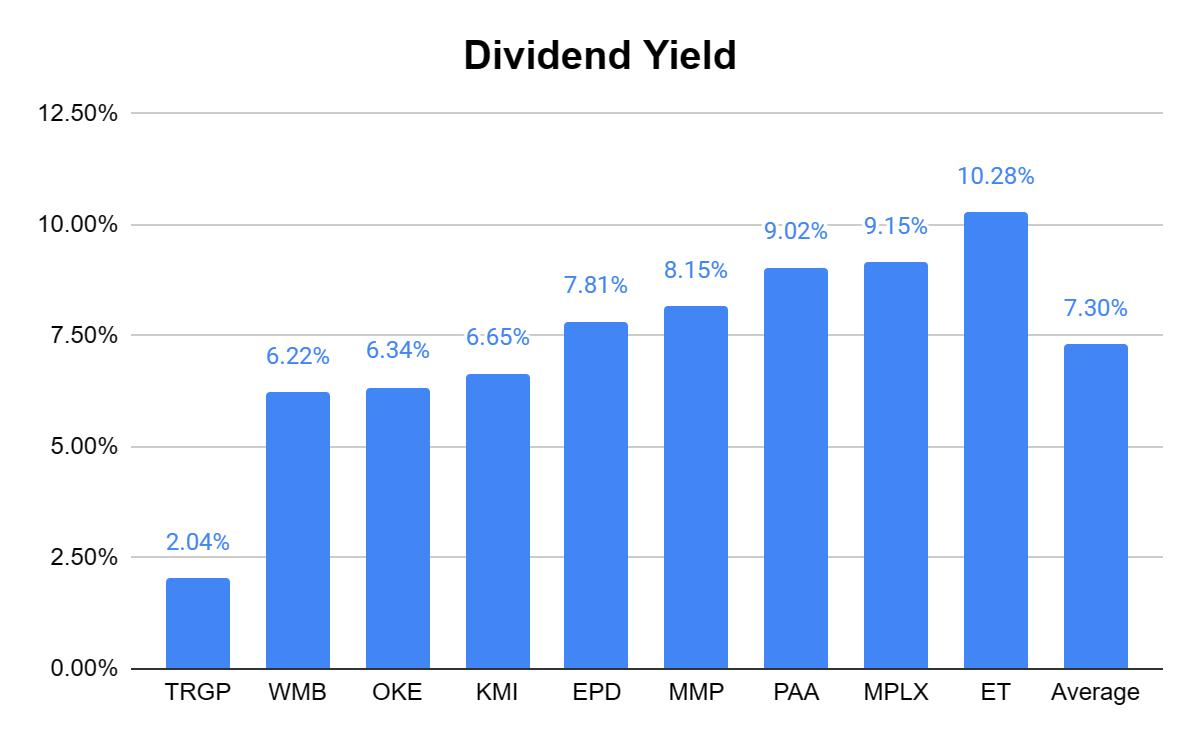

ET also has the largest dividend yield in its peer group at 10.28%. The peer group average is 7.3%, and ET is the only one in double digits. ET's unit price hasn't been valued properly, and the distribution is not at risk as management has just provided its fifth consecutive increase , raising the quarterly distribution by another 15.09%, bringing it back to pre-pandemic levels of $0.305.

{kind=link}

Conclusion

I believe energy infrastructure is undervalued. The EIA has released its latest energy outlook and is once again indicating that production of oil & gas will increase over the next 27 years, looking out to 2050. As more fossil fuels are produced the need for transportation, storage, and servicing throughout the oil & gas value chain will increase. ET is the largest energy infrastructure company in the United States, and its units are still trading at depressed values compared to its peers. The data indicates that the need for its services will continue to increase, and this is a growing sector, not one on the decline. Based on the peer group, I think ET should trade around $19-$21 as this would bring its metrics more in line with its peer group. I think the recent pullback is a gift, and investors are getting paid 10% while waiting for the story to play out.

For further details see:

Energy Transfer: Tollbooth To A 10% Dividend Yield Regardless Of Commodity Pricing