ET - Energy Transfer: Why This Time 9.1% Dividend Is Safe?

2024-01-20 21:08:20 ET

Summary

- Energy Transfer offers an attractive dividend yield that is backed by durable business operations and a sound balance sheet.

- The dividend cut in late 2020 and current lawsuits make more bearish investors uncomfortable around ET's ability to accommodate the current yield in the long run.

- In this article, I elaborate on the key reasons behind the previous dividend cut and give a color on why I think that this time the situation is different.

Energy Transfer (ET) is a widely recognized yield-focused stock, which offers a combination of attractive dividend yield and durable business operations.

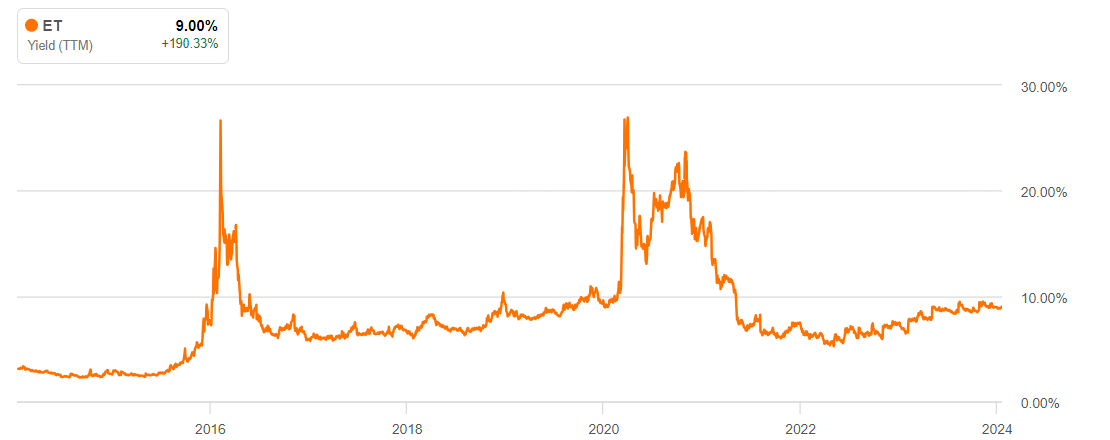

If we look at the historical yield level of ET, we will notice that currently, the dividend yield revolves around its historical average (excluding the outliers in 2016 and 2020 that were brought down by massive dividend cuts).

{kind=link}

There is a lot of chatter around ET's dividend attractiveness, where more bearish investors tend to refer to late 2020 when the annual dividend was cut by ~40%. On top of that bears pinpoint to the current lawsuits, which could potentially cause ET to adjust the distribution level just to pay off the penalty in case ET loses the case.

The objective of this article is to wrap our heads around what were the key drivers behind the dividend cut in late 2020 and whether ET investors should be worried about this repeating again.

The cut in 2020

If we had to provide the single most critical reason behind ET's decision to decrease the annual distribution by ~40% back in 2020, it would be leverage.

During Q2, 2020 conference call , an analyst (Shneur Gershuni) posed the following question:

And maybe as a follow-up question, the -- heading into this year there was a path for deleveraging, the goal was 4.5x. Obviously, COVID and OPEC have kind of derailed that. Can you talk about your path to how you think you'll get there on a go-forward basis? How you're thinking about the distribution versus the investment-grade credit rating if we were to hit that crossroad, just kind of interested in your overall thoughts with respect to both?

To which Tom Long - Chief Financial Officer - responded:

You bet. Clearly the investment-grade rating is very important. But I think it's also important to highlight the various levers we have to pull and the CapEx reductions that we announced today were obviously a big part of that. We're going to continue to work with the rating agencies. We're going to continue to work toward bringing our leverage down. And clearly the distributions are a topic when we discuss how to get the leverage down.

So, already before the decision was made to decrease the cash distributions, the Management seemed to be aware of a such possibility given just how far stretched the balance sheet was.

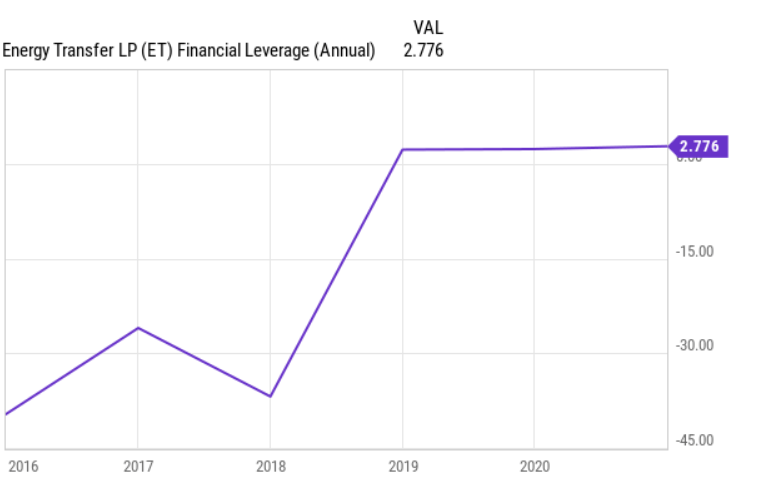

Looking at the chart below, we will understand why.

{kind=link}

In a period of ~4 years (starting from 2016 until the cut was made in 2020), ET assumed massive loads of external leverage to fund both M&A and organic growth activity that failed to bear fruit. Right before the dividend got cut, ET's debt to EBITDA stood at ~7.5x, which is extreme and characteristic of high yield and/or speculative grade businesses.

As a result, ET had to tap into the distributable cash flows in order to close the gap between debt service cost and the incremental cash generations that were associated with the new investments. A significant part of this equation was also ET's efforts to land into investment grade territory that would help keep the cost of capital in check and make further investments inherently more attractive (i.e., the spread effect).

Why this time it is different?

The answer lies in an improved balance sheet, de-risked business, and the communicated ambition to keep the leverage profile balanced.

For example, since ET announced that it will decrease the distribution level in a notable fashion, the retained proceeds have allowed the Company to optimize the balance sheet.

The financial debt to EBITDA metric has shrunk by ~50%, while the annual EBITDA figure has gone up by ~30% or more than $3 billion compared to 2020 levels.

{kind=link}

Granted, one could argue that in 2020 and 2021 the interest rate environment was completely different and that each dollar in the debt costs way more now. This is true, where we can see that although the debt has dropped, the annual interest expense item has remained the same at ~$2.3 billion level.

Having said that, the real game changer here is the underlying growth in EBITDA that has allowed ET to expand the base of distributable cash flows by ~28%.

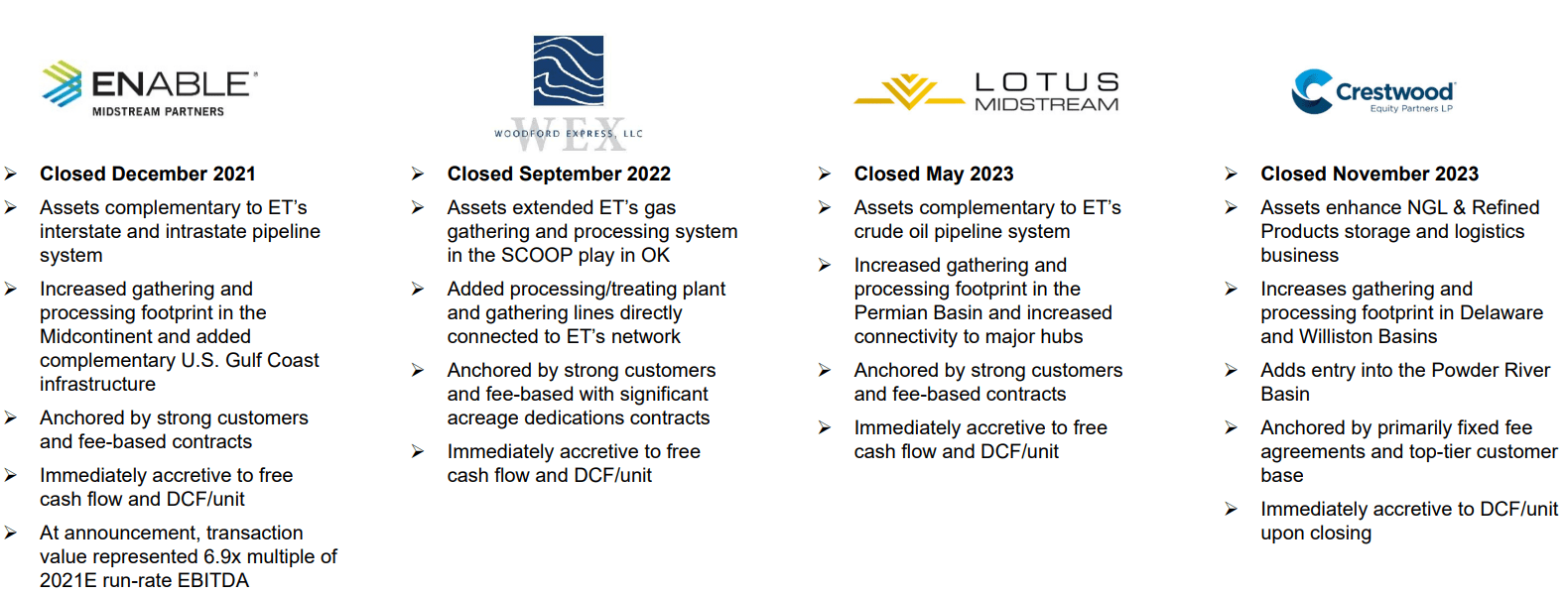

Moreover, during this time, ET has become a more diversified and larger-scale business, increasing its asset pool by more than $10 billion through a series of M&A maneuvers.

{kind=link}

On top of that, ET has clearly committed to targeting debt to EBITDA ratio at 4-4.5x range before venturing into the next M&A moves or doing share buybacks.

Finally, we have to also appreciate the fact that relatively recently ET has managed to obtain an investment grade credit rating, which for a stable and cash-cow type business is critical. This means that going forward, ET will be able to either refinance or borrow at cheaper levels thereby capturing greater cash flow effects from new investments.

What could be the source of another dividend cut?

From a fundamental perspective and based on the underlying financials, ET is clearly in a solid position to safely accommodate the current dividend as well as make additional investments via M&A and/or organic CapEx.

Yet, we have to be cognizant of the fact that ET has quite many outstanding lawsuits that could trigger massive penalties.

As of now, ET has reserved around ~$1 billion in the potential fines:

As of September 30, 2023 and December 31, 2022, accruals of approximately $947 million and $200 million, respectively, were reflected on our consolidated balance sheets related to contingent obligations that met both the probable and reasonably estimable criteria

Given the amount of quarterly cash generation and the remaining amount after distributions (on a cash basis), funding the current provisions should be a relatively easy thing to do for ET without impairing the balance sheet. We cannot completely rule out the possibility that ET would opt for a tactical and short-term reduction in the dividend to fund the potential penalty from different sources of capital (i.e., not only exhausting the available liquidity profile).

The main risk, however, stems from Dakota Access Pipeline lawsuit :

On July 27, 2016, the Standing Rock Sioux Tribe (“SRST”) filed a lawsuit in the United States District Court for the District of Columbia (“District Court”) challenging permits issued by the United States Army Corps of Engineers (“USACE”) that allowed Dakota Access to cross the Missouri River at Lake Oahe in North Dakota

The issue here is that the outcome is highly unpredictable with the worst-case scenario implying sizeable penalties (albeit not quantified) that would per definition force ET to halt distributions and even tap into debt financing pool.

The bottom line

Back in late 2020, when a ~40% dividend cut was made, ET's balance sheet was in a completely different state. Now, the Company has optimized its financial profile by strengthening the underlying business which has allowed it to achieve an additional ~$3 billion in annual EBITDA generation. Plus, the leverage has gone down by ~50%, which in turn has contributed to a solid investment grade credit rating.

While from the fundamental perspective, ET's distributions are safe and embody a notable margin of safety, the risk might come from current lawsuits. Currently, the Company has made notable provisions that could be funded without taking capital from the prevailing distributions. Yet, in case the Dakota Access Pipeline case goes really south (where better visibility will emerge early this year), I would not be surprised that ET opts for a tactical pause in the dividend in order to maintain the investment grade credit rating (instead of taking loads of leverage just to protect the dividend).

For me, ET presents an attractive opportunity to capture a 9.1% yield that is underpinned by resilient operations and strong financials.

For further details see:

Energy Transfer: Why This Time 9.1% Dividend Is Safe?