ET - Energy Transfer Yields 9.25% Has Distribution Growth And Is Still Undervalued

2023-11-20 08:30:00 ET

Summary

- A recession in 2024 is becoming more likely as economic data suggests a downturn, and the Fed may cut rates as early as March 2024.

- Capital is expected to flow into income-producing assets as the risk-free rate of return declines, benefiting sectors like REITs, utilities, and midstream operators.

- Energy Transfer is well-positioned to benefit from capital inflows, with a strong balance sheet, strategic acquisitions, and aligned management, making it an attractive investment in the midstream space.

One of my friends and I were talking about what lies ahead in 2024. As bankruptcies and unemployment continue to rise, a recession looks more likely to occur. For the better part of 2023, I didn't think we would see a recession in 2024, as an inverted yield curve isn't the end-all-be-all indicator that some were making it out to be. As the year progressed and additional data became available, the latest economic data is making me start to lean toward a recession is on the table for 2024. While a recession can still be avoided, the latest projections from the CME Group indicate the Fed is done raising rates, and the first-rate cut could occur as soon as March 2024. As 2024 progresses, I think we could see a sector rotation into unloved income-producing assets if the forward target rate projections are accurate. While midstream operators have done well in 2023, I think that the current trajectory can continue in 2024 as capital sitting on the sideline is likely to flow back into the markets as the risk-free rate of return becomes less attractive. Energy Transfer ( ET ) is still a battleground in the midstream space, with one side of the investment community still upset with management while the other side is incredibly bullish. After going through all the Q3 numbers, I am more bullish on Energy Transfer than I previously was, as management is truly aligned with unitholders, and I think it's the best-valued pipeline in the sector. While Energy Transfer looks to finish 2023 in a position of strength, I think its strategic investments will pay off, and investors will see further capital appreciation and distribution growth in 2024.

{kind=link}

Following up on my previous Energy Transfer article

In my last Energy Transfer article, published on 8/17/23 ( can be read here ) I discussed the acquisition of Crestwood Energy Partners and what it meant for Energy Transfer. The macroeconomic environment has changed a bit as Core CPI data continues to come in lower, while Fed Chair Powell remains adamant about rates higher for longer. With rates expected to decline in 2024 and 2025, capital from the sidelines could move into the market looking to replace the mid-single-digit yields that investors are accustomed to. I am going to discuss why I feel Energy Transfer will be a beneficiary of capital flowing into the markets and why I feel it's still my top pick for the midstream space.

Why I think capital is likely to flow into income-producing assets over the next two years

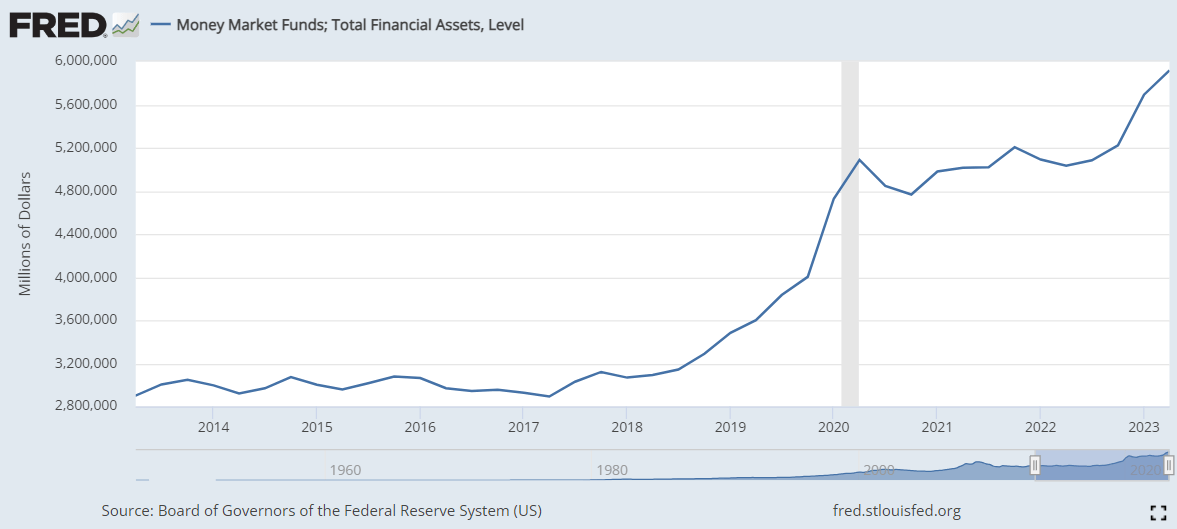

Over the past decade, we have seen interest rates go from being under 1% from the end of 2013 through the spring of 2017, rise to around 2.4% pre-pandemic, drop to basically nothing, then increase to the highest levels in the 5.25-5.5 range in the shortest period of time since the early 1980s. Looking at the 10-year chart for total assets in money market accounts , capital started flowing into money markets when rates started to get over 1.5%, dropped and consolidated during the pandemic, and increased again as rates surged. Today, you can find multiple financial institutions offering rates on money market accounts that exceed 5% as there is a total of $5.73 trillion of assets hiding out in these risk-free vehicles. As of 11/15/23, assets of retail money market funds increased by $10.52 billion to $2.23 trillion, while assets of institutional money market funds increased by $11.39 billion to $3.50 trillion.

{kind=link}

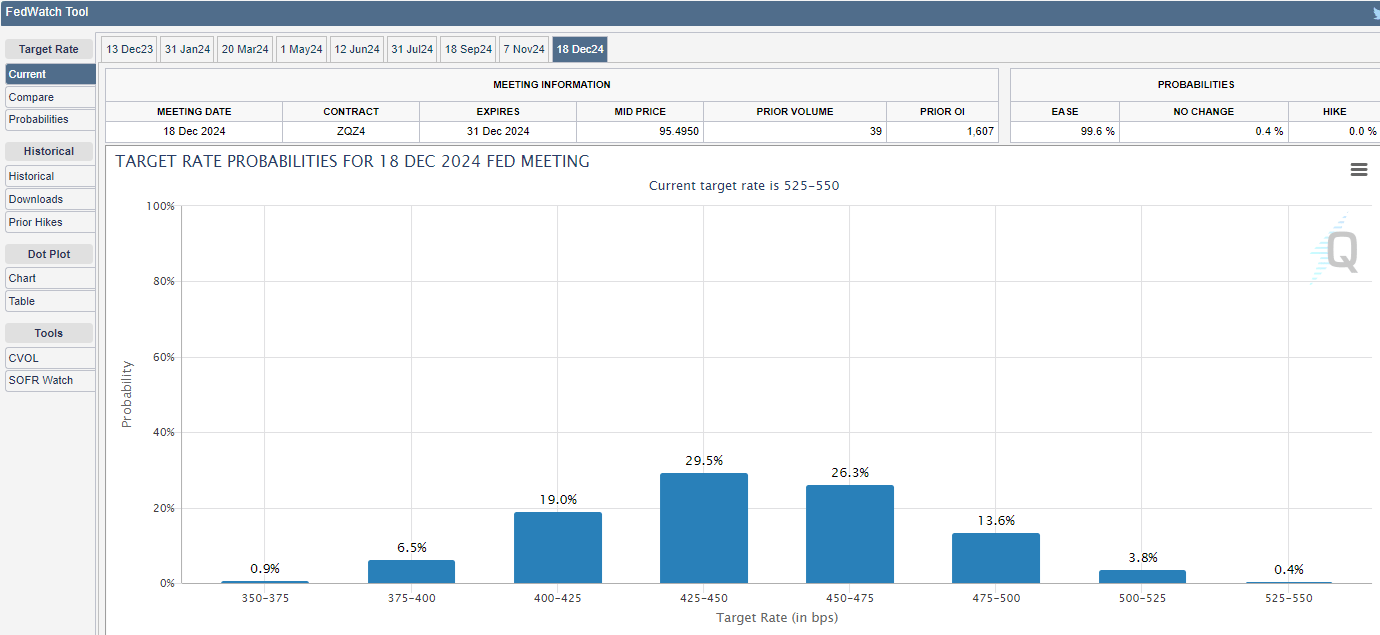

In the current economic environment, investors are able to generate a modest return risk-free by parking cash in a variety of risk-free assets. With CDs and money market accounts generating more than 5%, institutions are still able to park client cash on the sidelines, but at some point, this is going to change because individual investors aren't paying advisory fees to sit in cash. Eventually, institutions will need to deploy capital to earn their fees, and on the individual side investors will likely look to rebuild their income-producing strategies as the risk-free rate of return falls. Looking out to the end of 2024, CME Group is projecting that there is an 88.4% probability that rates are between 400–500 bps, a 7.4% chance that rates are between 350–400 bps, and only a 4.2% chance that rates are between 500-550 bps. UBS sees deeper rate cuts than what the market is projecting as they feel we could incur 275 bps of easing starting in March. If that wasn't enough Morgan Stanley ( MS ) is projecting that the Fed will reduce rates to 2.375% by the end of 2025.

{kind=link}

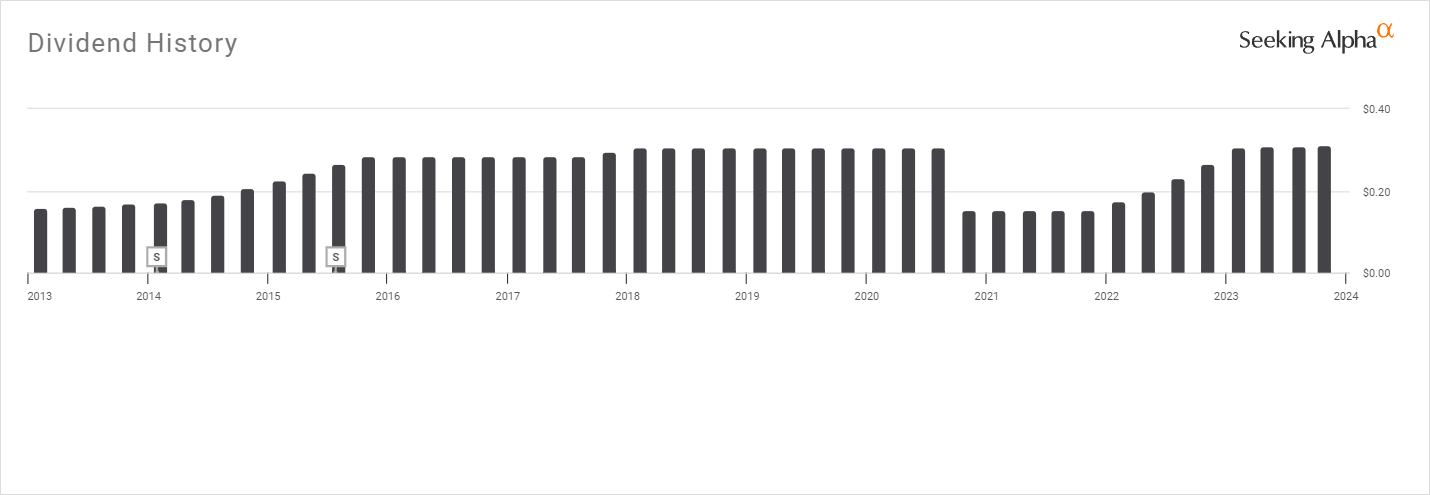

Investors have become accustomed to generating high rates of return from cash, as we have seen with the amount of assets that are stashed away in money market accounts. As rates decline, there is a good chance that investors will start to look at how to rebuild the lost yield they were used to producing. I think that several sectors will catch a bid, including REITs, utilities, and midstream operators. Energy Transfer is not the same midstream operator it was a few years ago, as they have strengthened its balance sheet, made strategic acquisitions, and rebuilt its large quarterly distribution. My feeling is that individuals sitting in cash are not necessarily going to chase big tech because if they were, they would have already allocated capital while big tech started rebounding after the large drawdown of 2022. I think they are going to look for income-producing assets that have large moats around their businesses and are cash-flow machines. Pipelines fit these categories as it's a sector that is almost impossible for new competitors to penetrate, and no matter what the rhetoric is, fossil fuels are not disappearing anytime soon. Energy Transfer is back to distribution growth, and its 9.25% yield could look very enticing for investors who we're used to generating over 5% risk-free as the additional percentage points could be the incentive to take on individual equity risk.

{kind=link}

Energy Transfer is positioned to benefit unitholders going forward

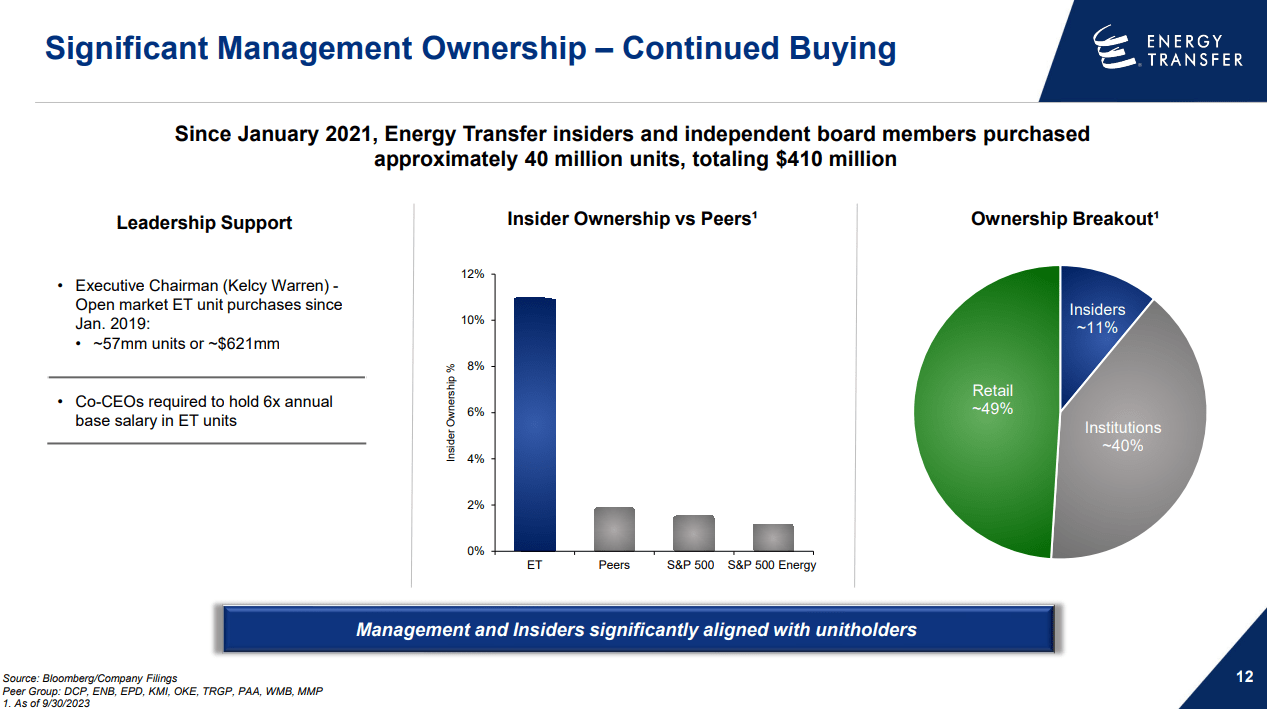

One aspect that I feel is overlooked is management's ownership of Energy Transfer units . The executive team at Energy Transfer is completely aligned with individual and institutional investors. When I am investing in companies, I always look favorably upon a management team that is putting their personal capital at risk along with their investors. Insiders at Energy Transfer own roughly 11% of the issued units, and Kelcy Warren has personally purchased $621 million worth of units since the beginning of 2019. When Energy Transfer makes decisions, they aren't just impacting the capital outside investors have allocated toward Energy Transfer, they have overwhelming implications for the executive team. This is what I want to see because it ensures that management is aligned with investors, and they are rewarded when Energy Transfer succeeds.

{kind=link}

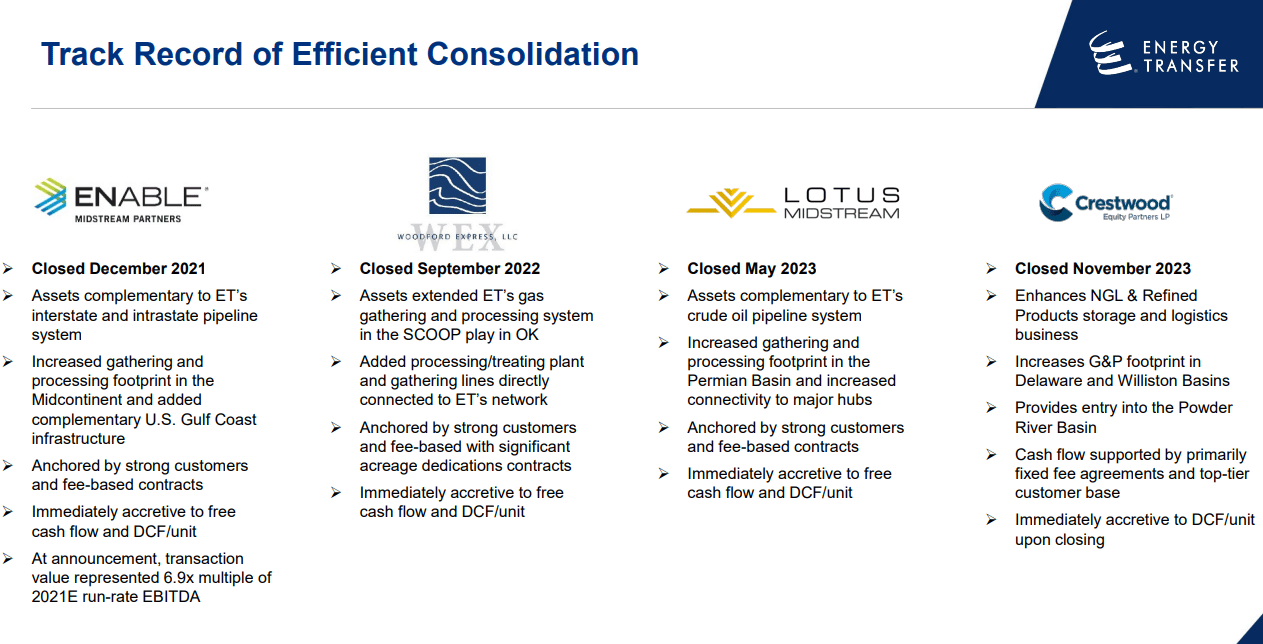

Energy Transfer many have the same name, but it's a much stronger company than it was several years ago. Energy Transfer finished 2020 with $51.41 billion in long-term debt, $32.15 billion in equity, generated $9.54 billion in EBITDA , and produced $7.36 billion in cash from operations . Since 2020, Energy Transfer has acquired Enable Midstream Partners, Woodford Express LLC, Lotus Midstream, and Crestwood Equity Partners. While acquiring these strategic assets to strengthen its operations, Energy Transfer also excelled in its operating metrics. In the trailing twelve months ((TTM)), Energy Transfer has generated $12.24 billion in EBITDA, produced $9.6 billion in cash from operations, increased its total equity to $41.06 billion, and reduced its long-term debt to $47.08 billion. While Energy Transfer was busy fortifying its operational territory, they significantly improved the fundamental business. Energy Transfer acquired these four companies while eliminating -$4.34 billion (-8.43%) of its long-term debt, increasing the total equity on the books by 27.71% ($8.91 billion) and producing an additional 28.28% in annualized EBITDA and 30.38% in annualized cash from operations.

It's difficult to argue that Energy Transfer hasn't done the right thing by its investors. Management has been a steward of operational efficiency and growth, their balance sheet is in a stronger position, and the distribution wasn't just repaired; it's now generating more income than before the distribution cut in Q3 of 2020. In 2020 Energy Transfer finished the year with a net-debt to EBITDA ratio of 5.45x, and based on the most recent financials Energy Transfer's net debt to EBITDA ratio is 3.95x. This is a management team that has proven they can get the job done and create value for unitholders. Energy Transfer has been put in a position to capitalize on the newly built foundation that has been assembled.

{kind=link}

I thought Q3 2023 was a huge step in the right direction for Energy Transfer. Their NGL transportation volumes were up 14%, NGL fractionation volumes increased by 9%, NGL exports jumped by more than 20%, Intrastate natural gas transportation volumes grew by 2%, Interstate natural gas transportation volumes increased by 15%, and crude transportation and terminal volumes were up 23% and 15%. In August, Energy Transfer's senior unsecured debt rating was upgraded by Standard and Poor's to BBB with a Stable outlook. Energy Transfer is expecting to generate between $13.5 billion and $13.6 billion in Adjusted EBITDA for the 2023 fiscal year as it continues to benefit from an expanded asset portfolio.

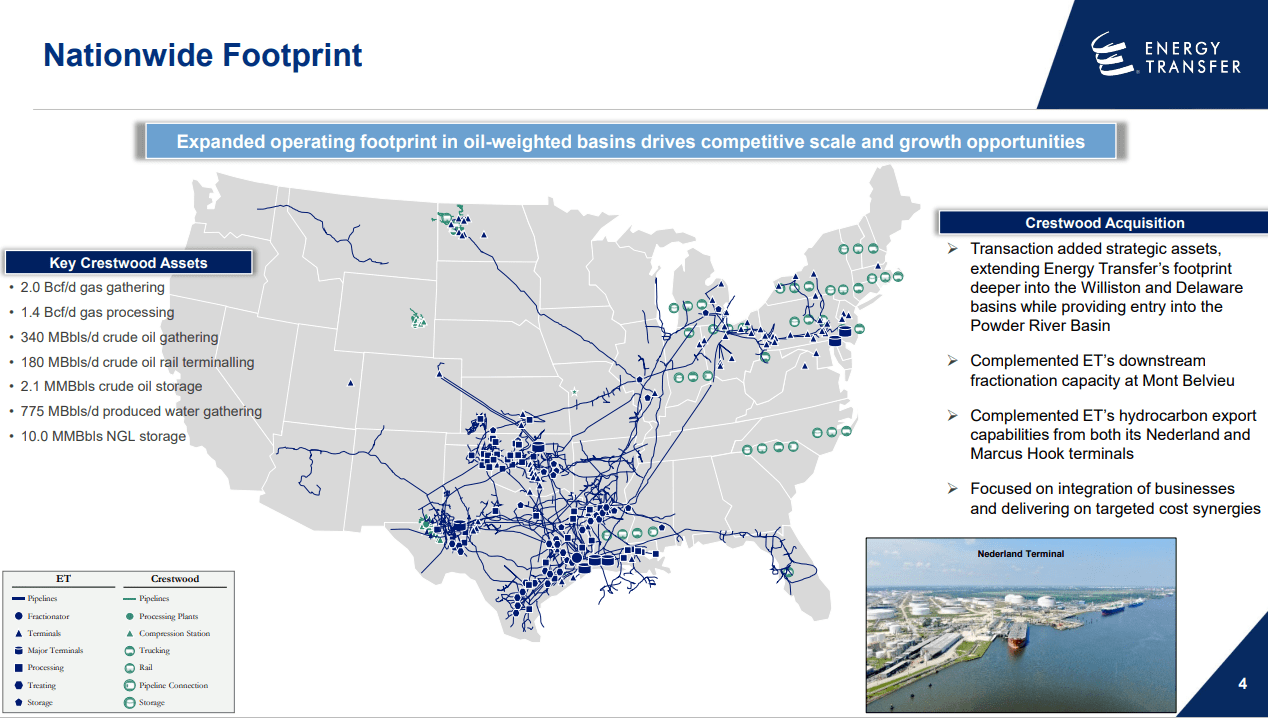

In Q3, Energy Transfer generated adjusted EBITDA of $3.5 billion, which was a $400 million increase YoY and $2 billion in distributable cash flow ((DCF)). After distributions, Energy Transfer retained $1 billion of its DCF, which provides them with ongoing capital to allocate toward organic growth projects and further strengthening the balance sheet. During Q3 , Energy Transfer allocated $418 million toward growth projects and completed the sale of $4 billion of aggregate principal amount of senior notes. The proceeds were used to repay borrowings on its revolving credit facility and pre-funded 2024 maturities. Energy Transfer continues to set themselves apart from others in the pipeline industry and has created one of the most extensive networks in the United States. I think Energy Transfer will continue to grow through organic growth projects and acquisitions, and I wouldn't be surprised if a large takeover is on the table for 2024. The Crestwood acquisition increased Energy Transfer's footprint in the northeast and upper central America. Based on their previous deals, I wouldn't be surprised if Energy Transfer acquires a company that has pipelines that can connect these assets to the rest of its infrastructure.

{kind=link}

Energy Transfer still looks undervalued compared to its peers

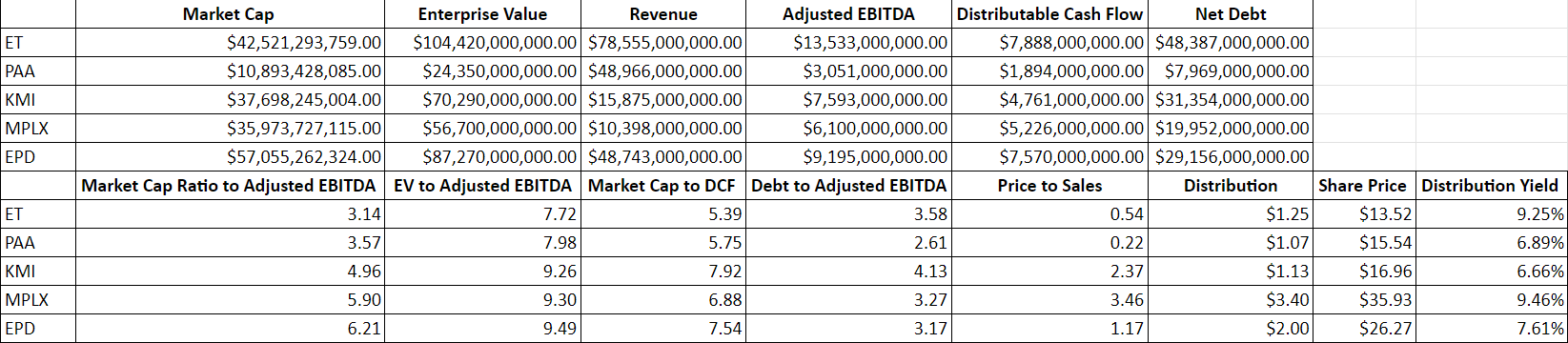

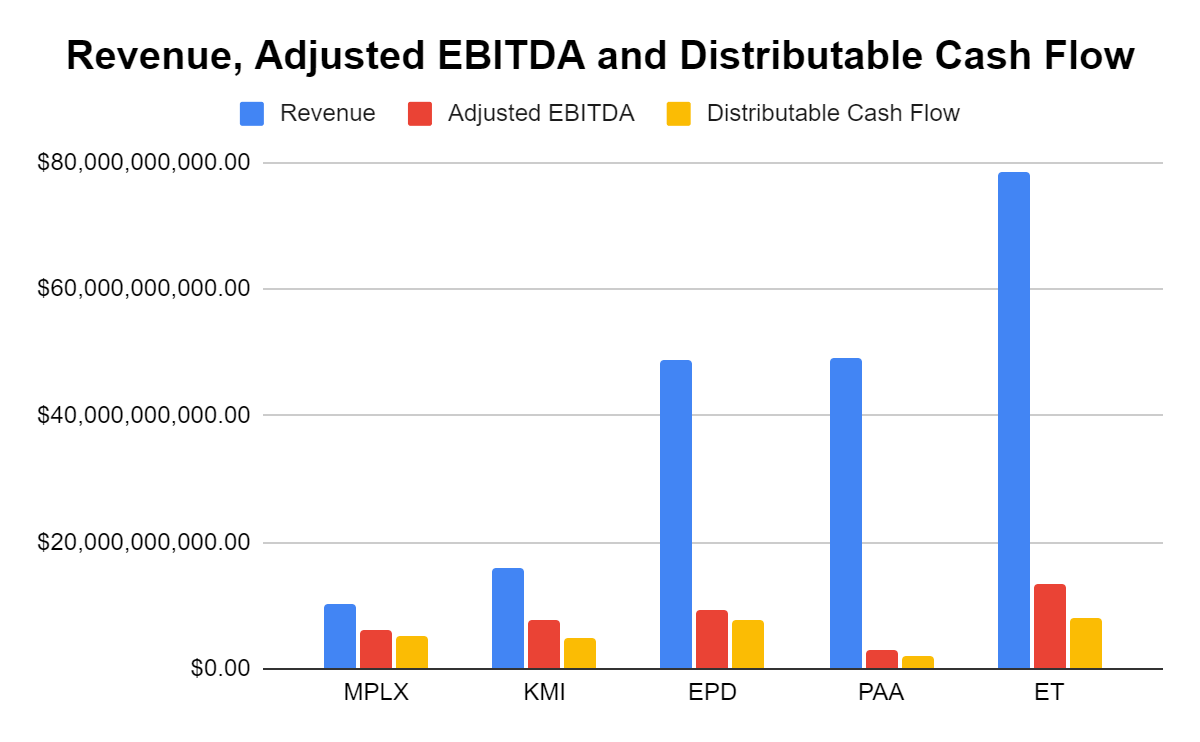

I compared Energy Transfer to Plains All American ( PAA ), Kinder Morgan ( KMI ), MPLX LP ( MPLX ), and Enterprise Products Partners ( EPD ), and still feel that there is an opportunity in Energy Transfer at its current levels. Energy Transfer generates the largest amount of revenue, Adjusted EBITDA, and DCF from its peer group and trades at a compelling valuation.

{kind=link}

{kind=link}

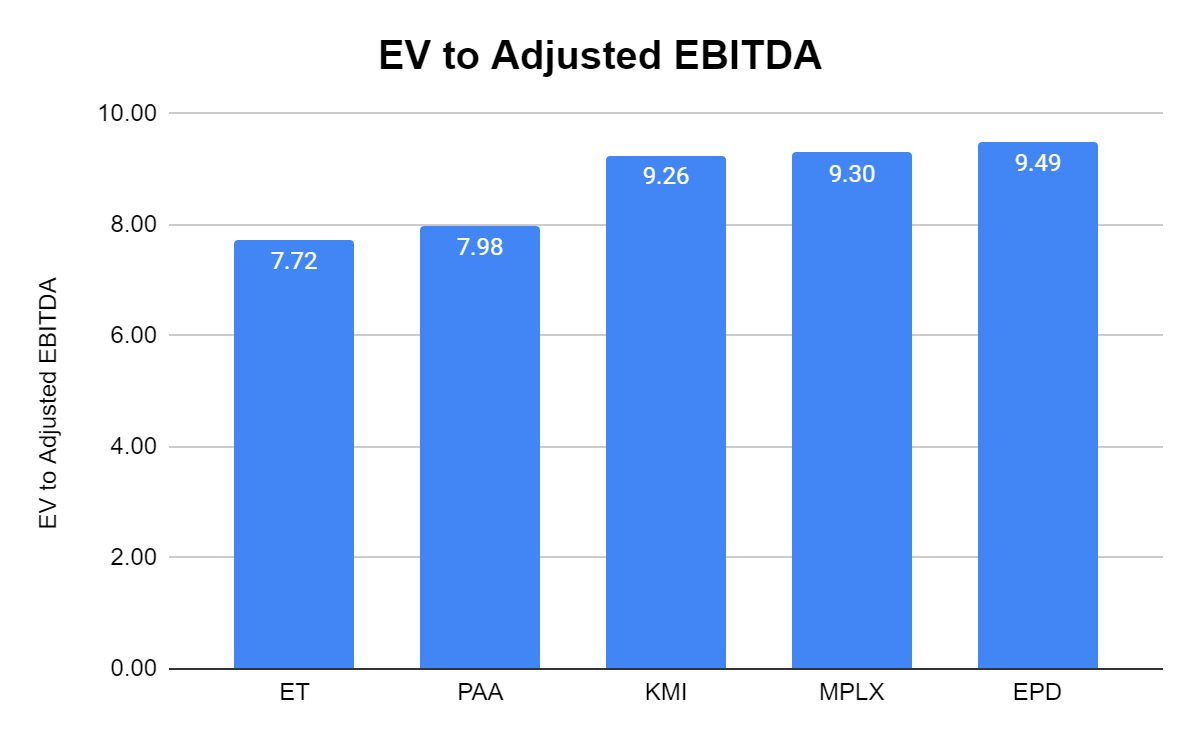

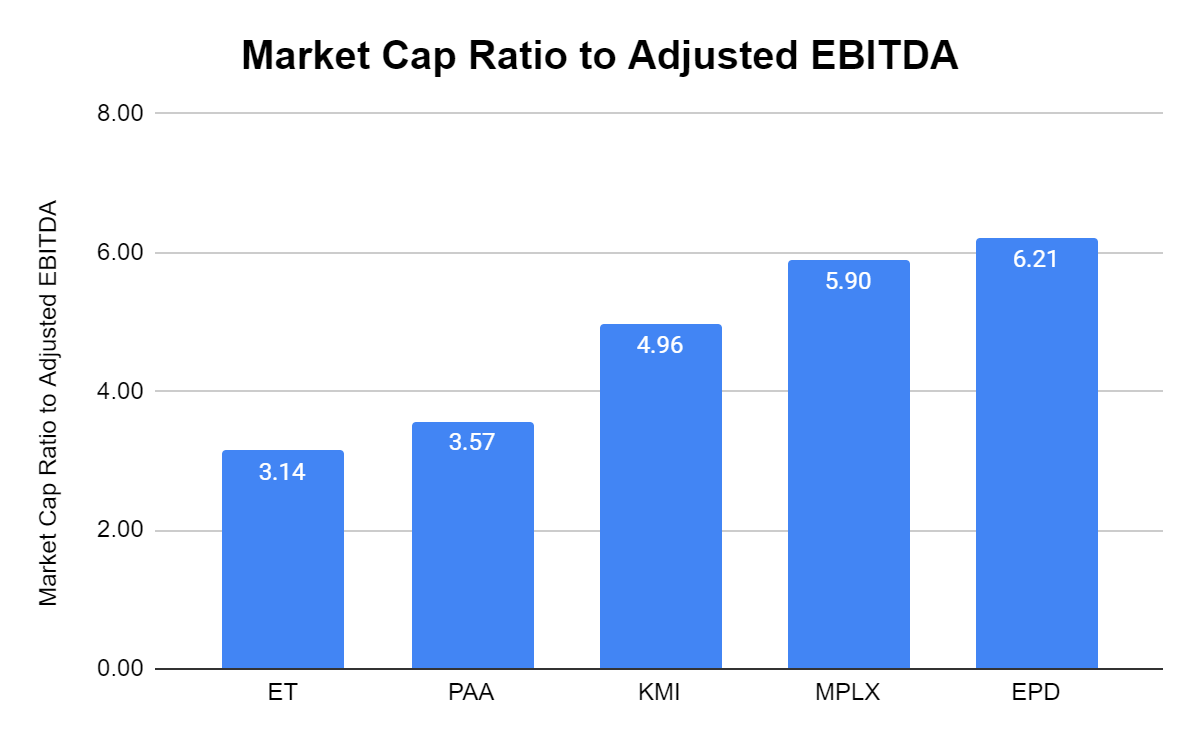

When I look at Energy Transfer on a market cap and enterprise value to Adjusted EBITDA methodology, it looks undervalued compared to its peers. Energy Transfer is currently trading at a 7.72x EV to Adjusted EBITDA ratio, which is the lowest in the peer group and significantly under the 8.75x peer group average. On a market cap to Adjusted EBITDA metric, Energy Transfer is trading at 3.14x, which is also extremely below the peer group average of 4.76x. After the transformation Energy Transfer has undergone, it's still trading at a discount to its peers based on the amount of Adjusted EBITDA it produces.

{kind=link}

{kind=link}

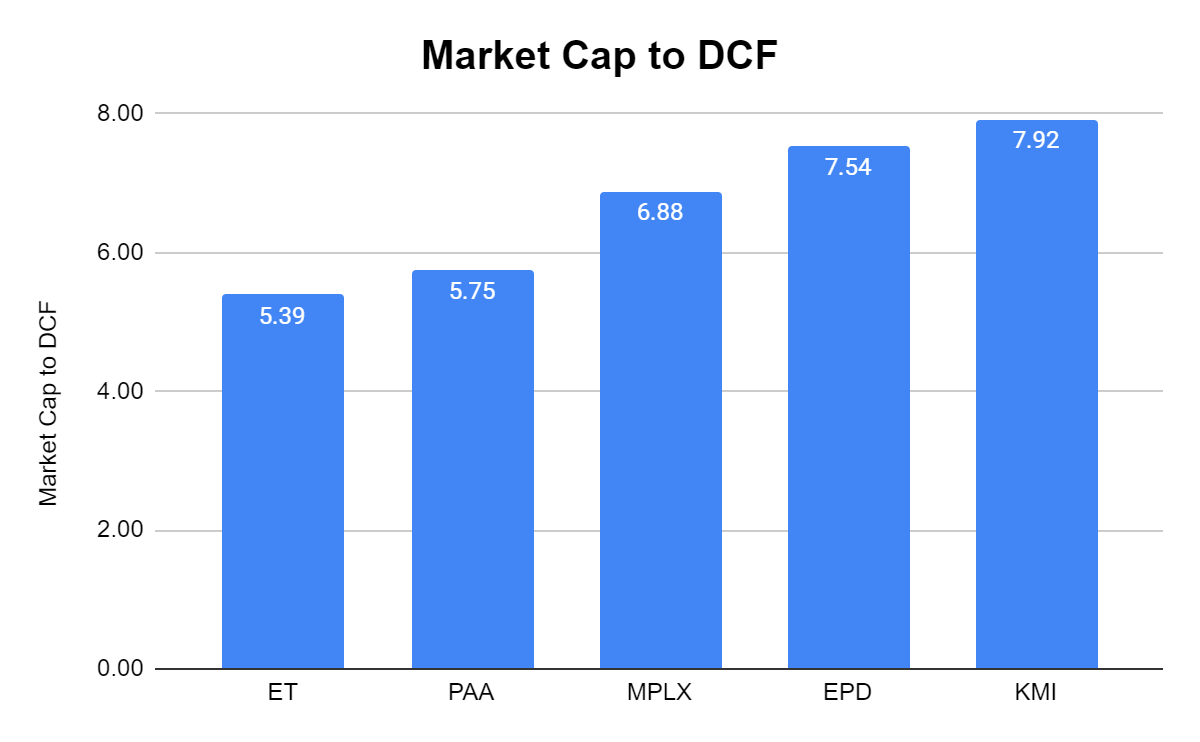

When I compared these companies on a DCF level, Energy Transfer's market cap trades at 5.39x its DCF while the peer group average trades at 6.7x. Energy Transfer is trading at the lowest market cap to DCF ratio in the peer group and produces the largest amount of DCF.

{kind=link}

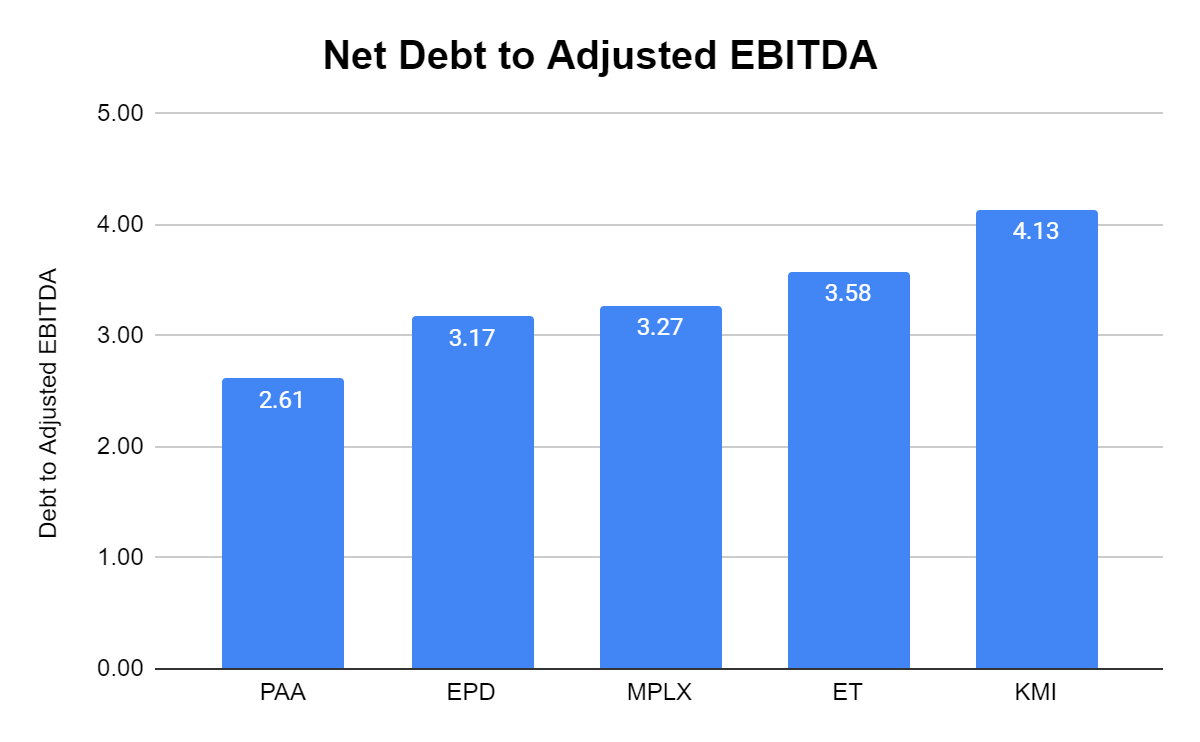

The net debt to Adjusted EBITDA metric was once Energy Transfers Achilles heel, but not anymore. Energy Transfer has a 3.58x net debt to Adjusted EBITDA ratio as this metric has significantly declined since 2020. Energy Transfer is above the peer group average of 3.35x, but not by much. The net debt to Adjusted EBITDA ratio is no longer the blemish it once was.

{kind=link}

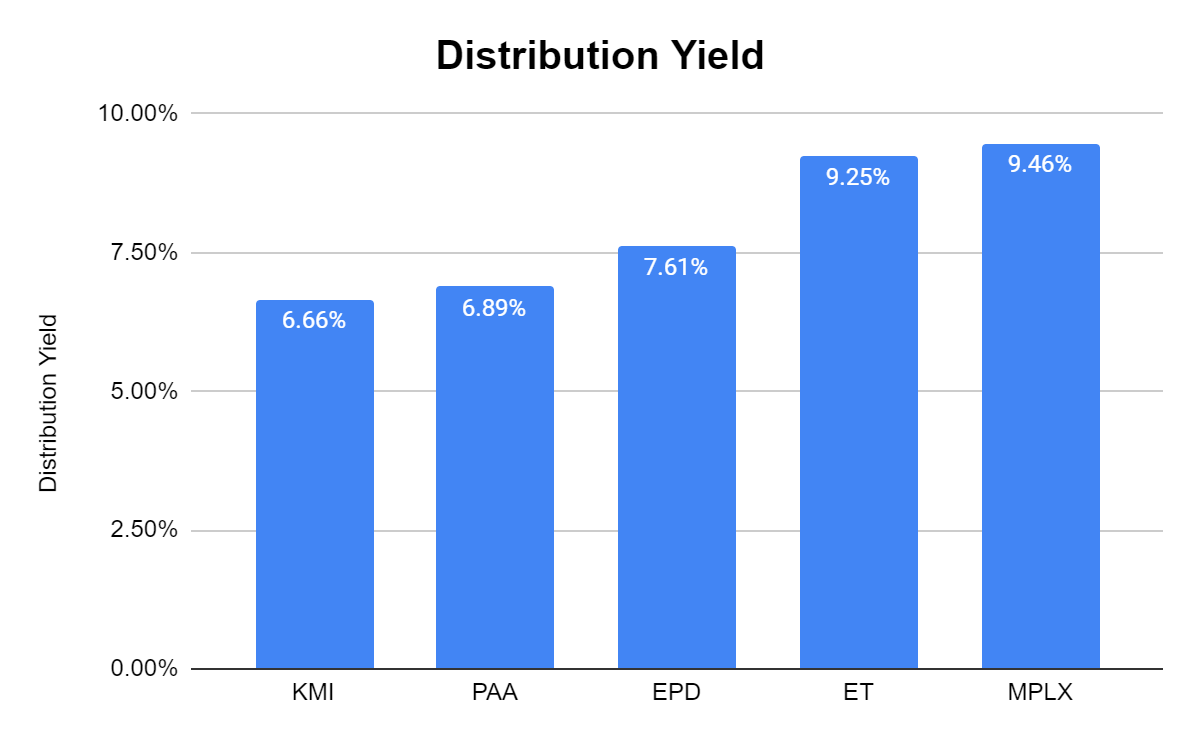

Energy Transfer has the 2 nd largest distribution yield from the peer group at 9.25%. This is well above the peer group average of 7.97%.

{kind=link}

Conclusion

While Chair Powell has stayed true to his message of higher for longer, the market is pricing in significant rate cuts on the horizon. With a Fed pivot expected as soon as March, a portion of the capital sitting on the sidelines is likely to flow into the markets as the risk-free rate of return declines. I think a portion of these investors will look to rebuild their income stream and allocate capital toward income-producing equities. Energy Transfer is positioned for continued growth as more capital projects come online, and it's the largest midstream operator by revenue and pipeline miles in the United States. I think MLPs will continue to have a strong year in 2024, and I think Energy Transfer is still trading at an enticing valuation. After looking at the TTM numbers for the peer group, it's hard not to be bullish on Energy Transfer. They are producing the largest amount of revenue, Adjusted EBITDA, and DCF while trading at the lowest Adjusted EBITDA and DCF multiples. While the valuation looks great, Energy Transfer has reduced its net debt to Adjusted EBITDA ratio to under 4x, yielding 9.25x. I think a fair value for Energy Transfer is much closer to $20 than its current level and that investors could see a significant upside in 2024 while collecting a larger-than-average distribution yield.

For further details see:

Energy Transfer Yields 9.25%, Has Distribution Growth, And Is Still Undervalued