CA - Enerplus Likely To Miss Q4 Guidance On Weather And Nat Gas Prices

Summary

- Weather and nat gas prices will likely cause ERF to miss its Q4 guidance.

- While not expensive, the stock's valuation is in line with its closest peer.

- ERF should consider divesting its non-operated Marcellus assets.

Enerplus ( ERF ) is a solid E&P company that primarily operates in Bakken. However, harsh winter weather in North Dakota, along with weak natural gas prices that hurt its non-operated assets in the Marcellus set the company up for a miss in Q4.

Company Profile

ERF was the original Canadian oil and gas royalty trust. Today, it doesn't have any Canadian assets, having divested the remainder of them in December to Surge Energy.

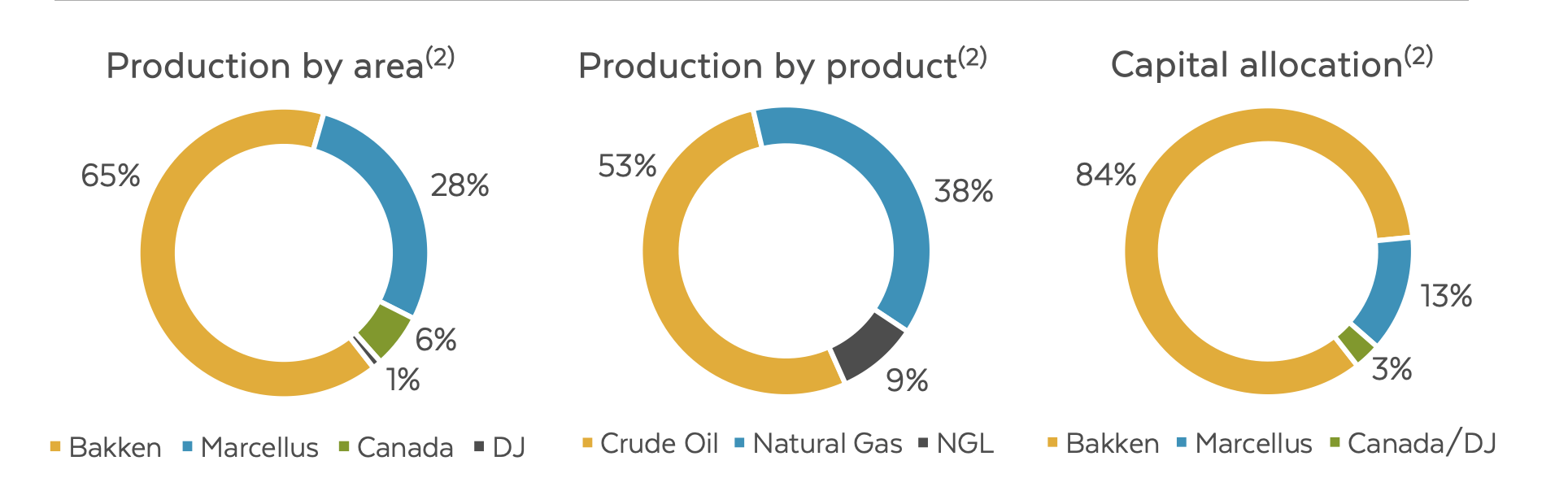

The E&P now operates in two primary basins: the Bakken and the Marcellus.

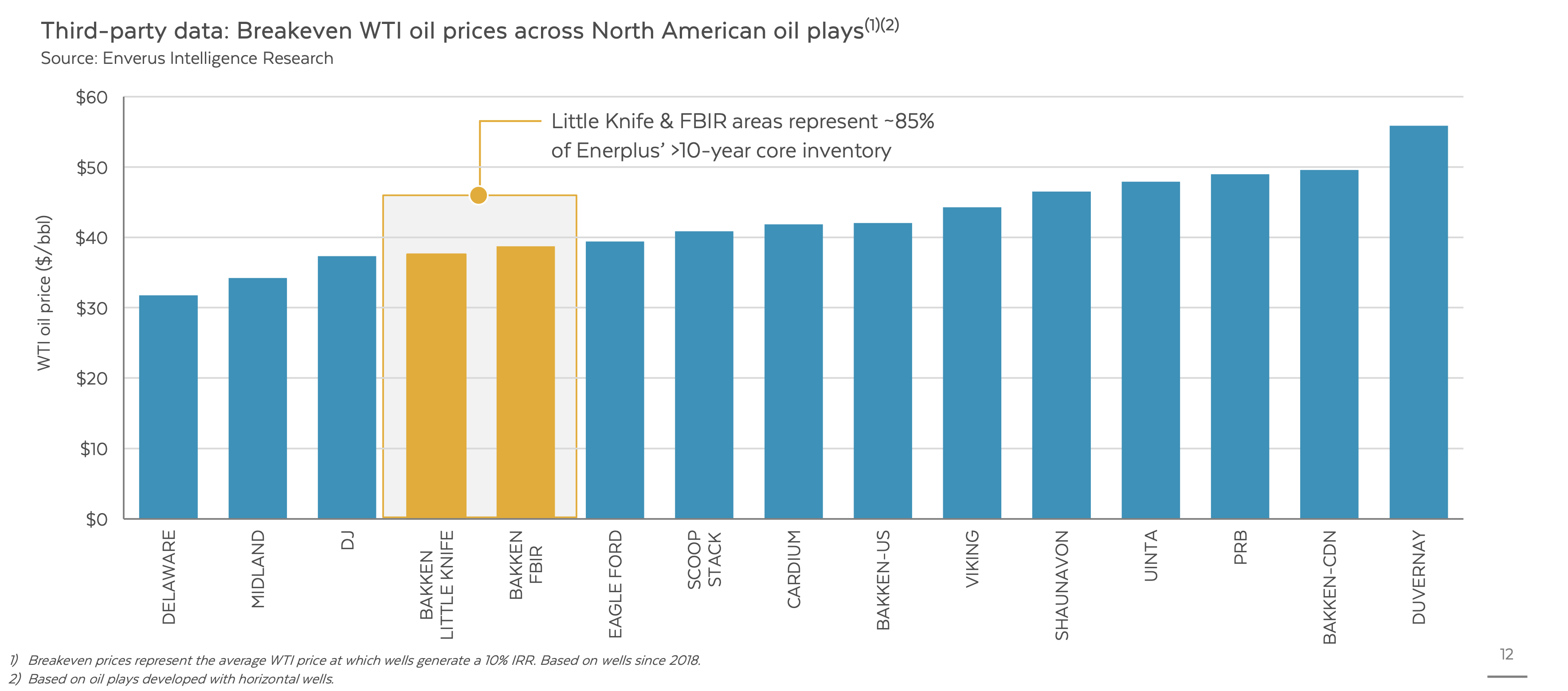

Over two-thirds of ERF's production comes for the Bakken, where the company has over a decade of core drilling inventory. The bulk of the company's inventory is the Little Knife and Fort Berthold Indian Reserve (FBIR) plays, both of which have WTI breakevens under $40.

{kind=link}

The company has over 550 drilling locations in the Bakken core, which has largely been de-risked given the activity in the area. This includes the FBIR, as well as Northern Dunn County and eastern Williams County. It also has over 100 locations in the extended core in southern Dunn county, where it can get solid returns midcycle. Finally, it has about 250 drilling locations that can be viable at higher oil prices or with well cost improvements.

Of its core drilling inventory, about 60% of its locations are in the FBIR, 25% in the Little Knife, and 15% in eastern Williams country. Its extended core locations are in Murphy Creek.

In the Marcellus, ERF has as non-operating position in the dry gas core. It has about 32,700 net acres with 160-170 MMCf/d of production.

The company also holds about 34,7000 net acres in the northern extension of the Wattenberg field in the DJ Basin in Colorado.

Recent Asset Transactions

ERF has been busy the last two years tightening up its asset portfolio. It sold out of its Canadian acreage position this year in two separate deals. On Halloween, it closed a deal selling its Alberta assets to Journey Energy for C$140 million. The assets included ERF's Ante Creek and Medicine Hat operations as well as some other interests in Alberta.

Then, in December, the company exited Canada with the aforementioned deal with Surge Energy. The E&P received approximately C$245 million in the transaction.

In 2021, ERF made both acquisitions and divestitures in the Bakken. In March, the company acquired Bruin for US$465 million. Bruin owned 151,000 net acres in the Bakken and had production of ~24,000 BOE. The deal was done at a 3x multiple of Bruin's 2021 forecast EBITDA using a US$50 per barrel WTI oil price. Then in April, it acquired 77,800 net acres in Dunn County from Hess (HES) for US$312 million. The deal included 110 tier-one undrilled locations. The assets were producing 6,000 BOE per day at the time.

Then later in 2021, it divested its Sleeping Giant acreage in Montana and Russian Creek acreage in North Dakota for US$115 million.

Opportunities

ERF has done a nice job upgrading its asset portfolio through asset purchases and divestitures. The company made some shrewd acquisitions when oil prices were low, and then was able to divest its Canadian assets a year later when prices were high.

From an operating standpoint, the company is almost a Bakken pureplay now. Its core positions in the FBIR and Little Knife, meanwhile, have some of the best breakevens in North America outside the Delaware.

{kind=link}

Risks

Oil and natural gas prices present the biggest risk to ERF. While oil prices have held up well, the same can't be said for natural gas prices, which have seen a precipitous decline from their 2022 highs. The company had some nice hedges in place for Q1 of 2023 at the end of Q3, and a decent amount through October 2023. When looking at the chart below, remember that just the Marcellus alone has nat gas production of 160-170 MMCf/d.

{kind=link}

However, the hope would be that ERF locked in more hedges before the decline in nat gas prices. If not, its non-operated Marcellus assets are going to see a pretty big decline in cash flow that gets worse throughout the year.

The company also is now very tied to the Bakken and faces basin risk. The biggest risk with the Bakken is a takeaway risk, as there are still challenges with the Dakota Access Pipeline (DAPL) that could potentially shut it down. This seems like a long shot now, but it's not out of the realm of possibility. If it did happen, though, companies should have to shift to rail, and basin differentials would blow out.

There is also a very good chance that ERF misses Q4 guidance due to severe winter weather in the Bakken. Crestwood ( CEQP ) does the gathering and processing for ERF in the FBIR, and it had to lower Q4 Bakken volume guidance due to the harsh weather conditions. This is just a temporary delay, but it will show up in Q4 results. ERF raised its guidance in early November just ahead of the severe weather in the region.

{kind=link}

Valuation

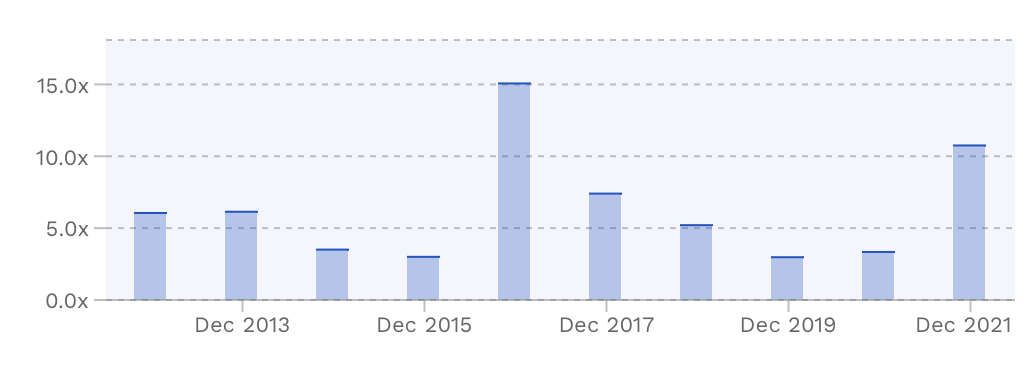

ERF trades at under 4x the 2023 EBITDA and 2024 EBITDA consensus of $1.12 billion and $1.05 billion, respectively.

{kind=link}

On a PE basis, it trades at 5x EPS estimates of $3.33. Based on the 2024 consensus for EPS of $3.52, it trades at 4.8x.

Chord Energy ( CHRD ) is likely the closest comparison, given that it's a Bakken pure play. It trades at 2.5x 2023 EBITDA and a PE ratio of 5x.

Both ERF and CHRD have strong balance sheets.

Conclusion

While ERF has done a good job upgrading its assets and turning its focus to its core asset, harsh winter weather in the Bakken and a huge decline in natural gas prices are likely to hinder Q4 results. In the medium term, natural gas prices are the bigger worry if the company didn't act quickly to add additional hedges. This is also a non-operated, non-core asset that I would have liked to seen divested while nat gas prices were high.

While the stock appears attractively valued, it's in line with a peer that doesn't have the same natural-gas price exposure. Its multiple is also pretty much in line with where it has traded historically in recent years - even a bit higher.

As such, I think this is a stock investors can consider shorting into a potential earnings miss.

For further details see:

Enerplus Likely To Miss Q4 Guidance On Weather And Nat Gas Prices