CA - Enghouse Systems: A Compelling Undervalued Opportunity

2023-08-04 11:12:22 ET

Summary

- Enghouse Systems is a leading Canadian SaaS provider in the telecommunications and healthcare sector.

- There has been a pull back in price and pricing multiples because of growth concerns.

- Growth concerns are overblown as the recent decrease in revenue growth was due to an unprecedented overperformance of one of their key assets (Vidyo) during COVID-19.

- Revenue is expected to start increasing again, with that should follow a higher share price as evidenced by a comprehensive discounted cash flow model.

- Enghouse has been increasing their dividend and consistently earns positive operating profits.

All figures are in unless otherwise stated.

All financial information comes from Capital IQ unless otherwise stated.

Price: $28.85

Dividend Yield: 3.05% ($0.88 Per Share)

Investment Thesis

Enghouse Systems emerges as an undervalued gem in the market, driven by its consistent operating profits, robust dividend growth, and it's currently trading below its historic multiples. With a solid financial foundation, a strategic focus on internal growth and acquisitions, and a compelling DCF valuation, the company presents an excellent investment opportunity. Investors have the chance to capitalize on the market's short-term sentiment and acquire shares at an attractive price, with the potential for capital appreciation as Enghouse's true value is recognized over time.

Introduction:

Enghouse Systems ( ENGH:CA ) is a Canadian-based technology company that operates in two different lines of business:

- Interactive Management Group ((IMG))

- Enghouse Interactive: Provides software and services designed for contact centers around the world.

- Enghouse Vidyo: Provides a means of visual communication with primary operations in telehealth and the financial services sectors.

- Asset Management Group ((AMG))

- Enghouse Networks: Develops and markets technology solutions to communications and media, utilities, and defense organizations looking to embrace digital transformation.

- Enghouse Transportation + Public Safety: Develops and delivers software solutions for transit, supply chain, and public safety companies.

With a market capitalization of just under $2 billion, Enghouse is one of the leading tech services providers in Canada. Any future reference to IMG or AMG refers to their operations within the respective segment.

Catalysts

Consistent Operating Profits & Dividend Growth

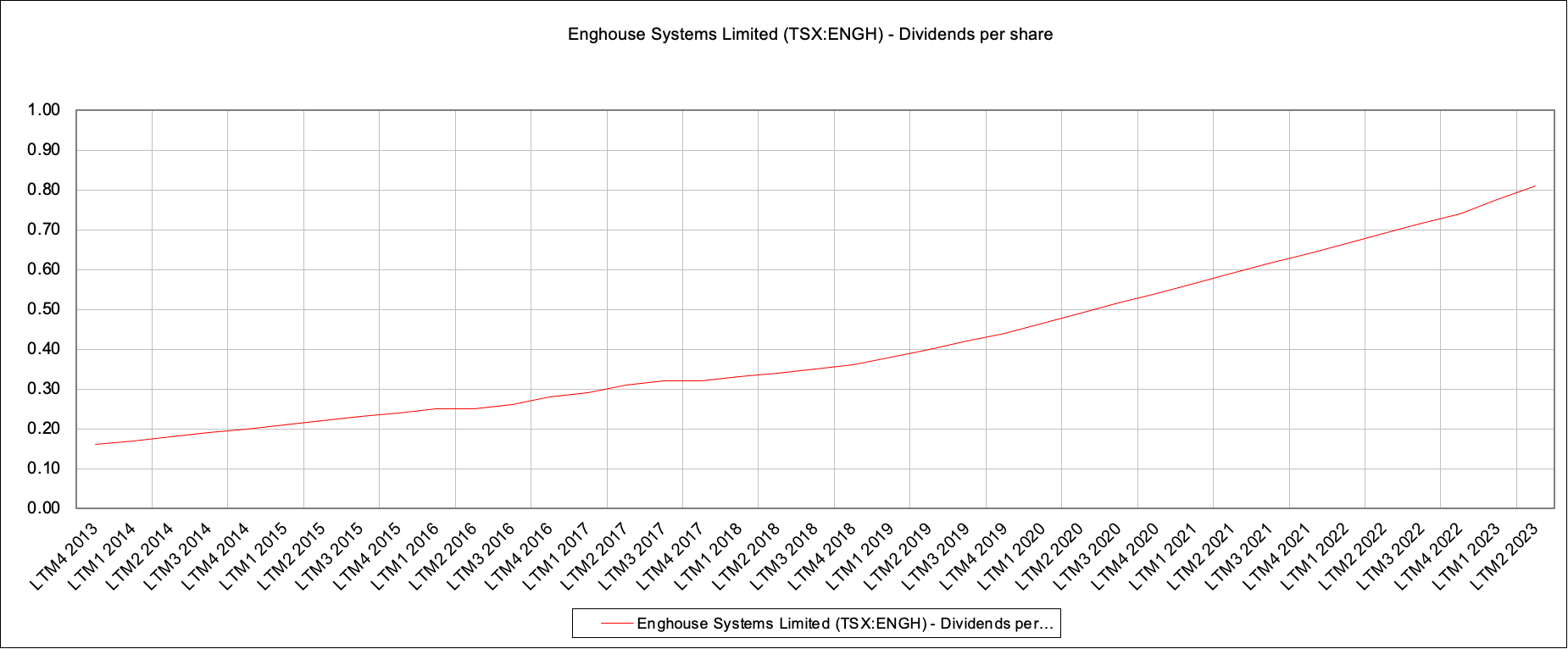

Enghouse has consistently maintained positive free cash flow all while growing their dividend at an attractive rate:

The figure above shows the LTM cash from operations over the past 10 years which hasn't been below $50 million since late 2016. As Enghouse doesn't have any debt, they have quite a bit of flexibility in what they choose to do with their operating profits. This has translated to them increasing their dividend in order to return capital to their shareholders - an increase of 406.25% over the past 10 years making for a compounded annual growth rate of ~17.61%.

Dividend Per Share (Capital IQ - Author's Illustration)

{kind=link}

When Enghouse isn't increasing their dividend they are still putting their money to good use. Given the build-up in cash on Enghouse's balance sheet, they fund acquisitions and share buybacks to further propel growth.

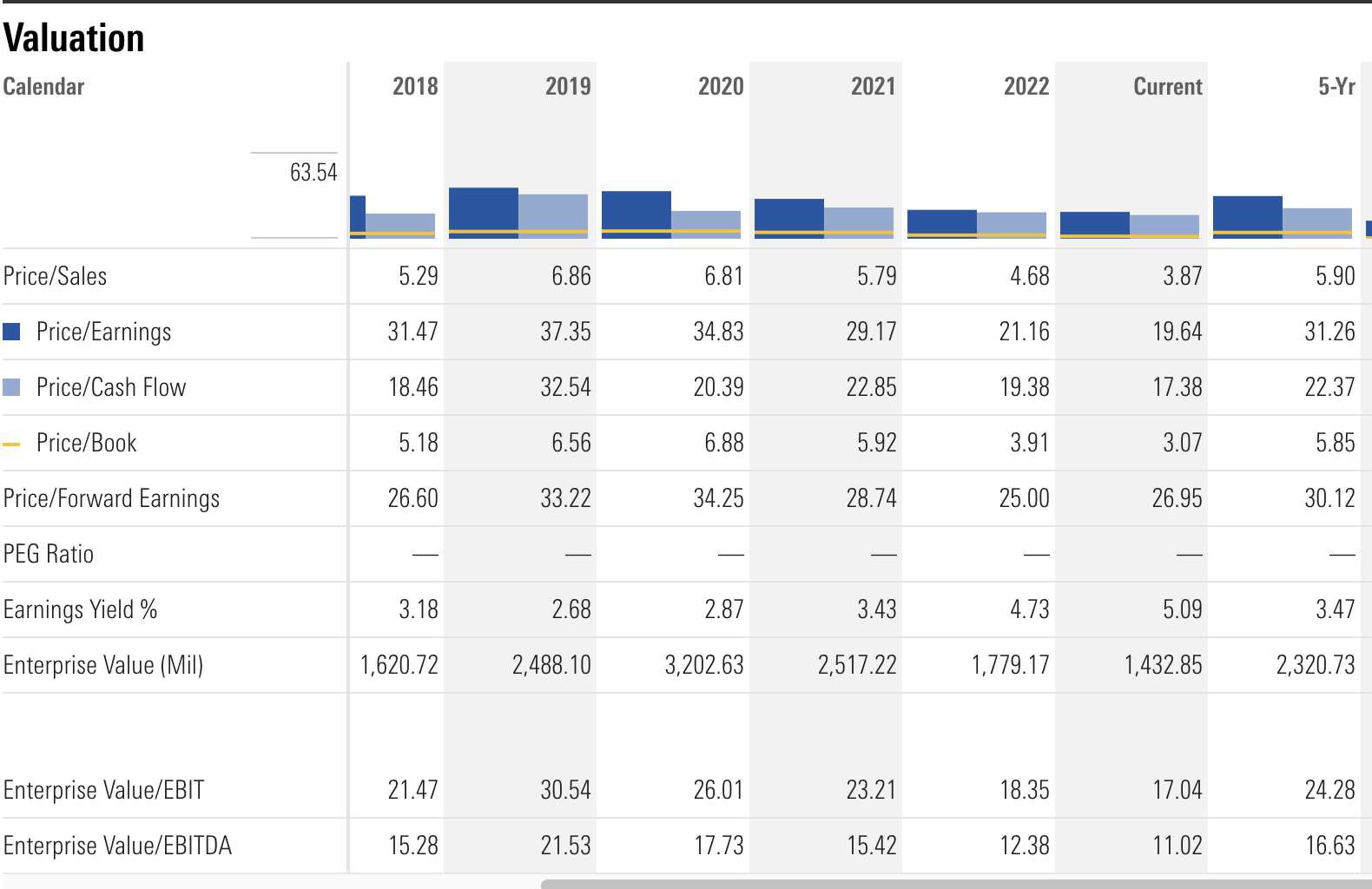

Trading Below Their Historic Multiples

Enghouse has been long considered a growth story by many analysts however, that growth has slowed down since COVID. Multiples in the technology industry were also a bit higher over the past few years because of this perceived growth. That being said, Enghouse is still trading well below their 5-year averages which leads me to believe they are undervalued.

Historical Multiples (Morningstar Canada)

{kind=link}

If Enghouse was trading at the same multiple as the 5-year average multiples their price would be around:

- P/S: $45.83 (LTM Sales of 430,067,000 * 5.90 / Shares Out. 55,270,239)

- P/E: $47.80 (LTM EPS of $1.52921 * 31.26)

- P/B: $56.93 (Book Value of $9.73 * 5.85)

Taking a weighted average of these 3 metrics gives us a theoretical price of $50.19 (~70% different than the current share price).

Enghouse experienced a remarkable surge in growth during the pandemic, primarily fueled by the widespread adoption of video communications. The Vidyo segment played a big role in driving rapid sales growth, prompting Enghouse to reward shareholders with a special dividend as a show of success. However, as the surge in Vidyo's revenue normalized post-pandemic, overall revenue witnessed a subsequent decrease in the following periods.

Enghouse's growth trajectory has seen a revival, as evidenced by their latest quarterly results, which boasted a 6.72% year-on-year increase in revenue. Analysts are optimistic about the company's future prospects, with projected FY2023 revenue estimated to reach $491 million, representing a 16.1% growth compared to 2022 and a 6.9% rise from 2021. Support has also come from management quoting their Q2 earnings report: "As we see a growing demand for SaaS, as with all our revenue streams, we are careful to ensure that this is achieved without sacrificing profitability".

While I don't expect the multiples to revert as high as pre-pandemic levels, with the increase in revenue expected to continue, I see the multiples moving back toward that range, and thus, the share price to follow.

No Debt & Acquisitions

Enghouse has historically fueled revenue growth by acquiring new companies and then growing them internally. With acquisitions occurring in more than 25 different countries, Enghouse focuses on vertically focused enterprise software companies they can buy and hold with r evenue greater than $5 million.

In 2022, Enghouse completed 3 acquisitions for $24.9 million:

- June 23, 2022: Acquired Competella AB which provides a complete SaaS contact center platform created to enhance the offering of MS teams.

- July 6, 2022: Acquired NTW Software GmbH which provides a suite of products, ranging from attendant consoles to contact centers.

- September 6, 2022: Acquired the business assets and certain liabilities of VoicePort LLC (provider of SaaS automated solutions).

In 2023, Enghouse has completed 2 acquisitions for a total of $30.1 million:

- February 8, 2023: Acquired Mobi All Tecnologia S.A. which provides SaaS-based enterprise mobility management solutions in managing and controlling critical mobile assets.

- February 9, 2023: Acquired Qumu (previously NASDAQ: QUMU) which provides cloud-based enterprise video technology.

Acquisitions in 2022 and 2023 have cost Enghouse $55 million. Because Enghouse has consistently earned operating profits they are able to fund acquisitions through cash on their balance sheet. As of April 30th, 2023, Enghouse had $234.5 million in cash and cash equivalents. Compare this figure with their total liabilities of $237.6 million and I feel confident in saying that Enghouse has an extremely safe balance sheet. Net debt for Enghouse is -$217.5 million making them a safe haven for investors looking to avoid the risk of rising interest rates.

A company that is able to fund their growth strategy through acquisitions without taking on any debt should command a premium on the market which is another reason I feel Enghouse is undervalued.

Discounted Cash Flow Analysis

I created a discounted cash flow analysis for Enghouse to illustrate the mispricing between their intrinsic value and the share price. The key assumptions used in the DCF are as follows:

- Tax Rate: 25%

- This is the Canadian corporate tax rate as per NYU Stern .

- Discount Rate: 8.8%

- I employ the CAPM model with an assumed equity risk premium of 6%, risk-free rate of 4%, and beta of 0.8. As Enghouse has remained debt-free, I assume this will continue and therefore, no cost of debt is used.

- EV/EBITDA Multiple: 14.33

- I used the average EV/EBITDA multiple over the past 5 quarters because it accurately captures the multiple in the current macro environment.

- Perpetual Growth Rate: 2%

- Canadian central bank's inflation target of 1-3% midpoint.

- Revenue Growth: 7%

- Based on analyst estimates

Based on the following key assumptions the DCF returns a price of $42.65 representing a ~48% upside from the current share price.

Waterfall for IV (Author's Illustration)

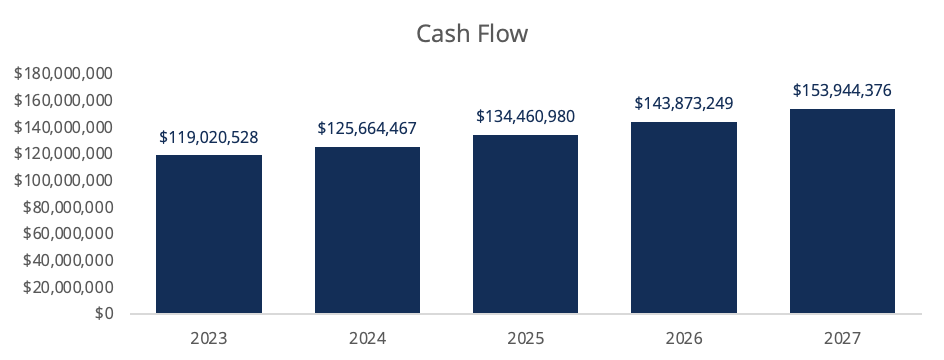

The free cash flow (free cash flow to the firm) forecast looks like this:

FCFF Forecast by Year (Authors Illustration)

{kind=link}

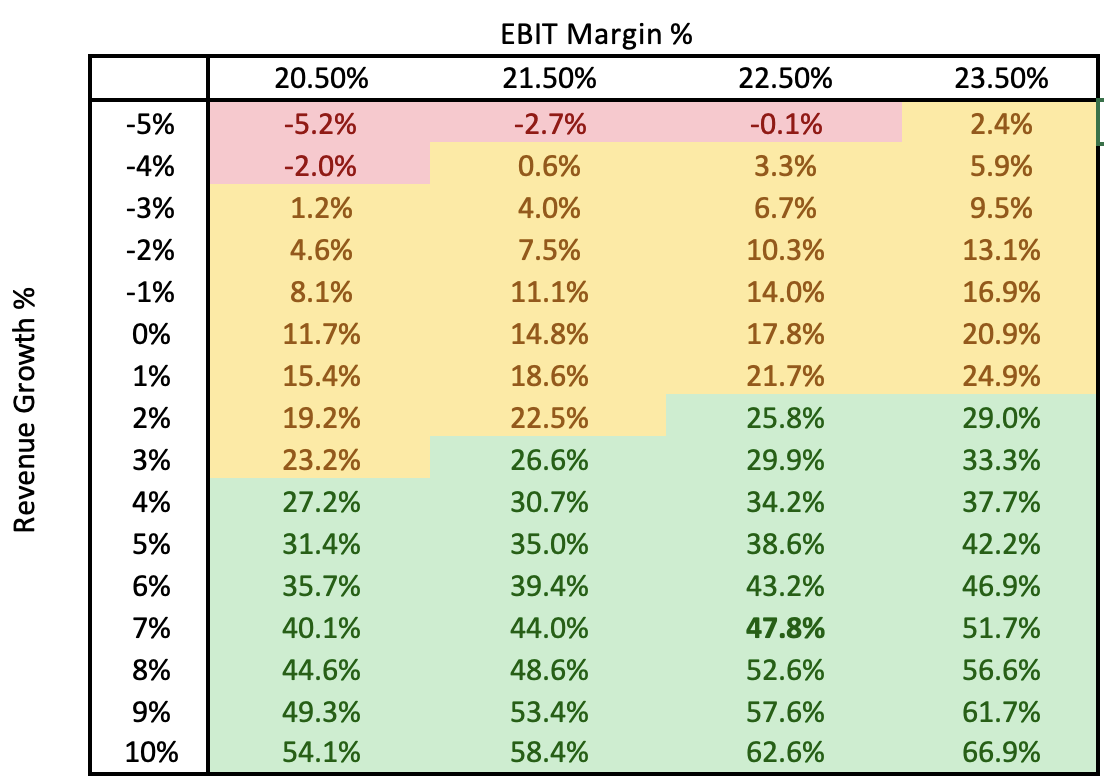

By running a scenario analysis we can see the target upside/downside by adjusting revenue growth and the EBIT margin. With revenue growth on the vertical axis and EBIT margin on the horizontal axis, I highlighted any upside scenario with a 25% upside in green, any scenario in red indicates a fair value less than the current price and anything in yellow is in between:

Scenario Analysis (Authors Illustration)

{kind=link}

Risks

Revenue Growth Fails to Materialize

Whenever I create a DCF for a company I try to ensure that the price target or upside is still preserved with considerable room for movement across the key variables. As I showed in the section above if revenue decreases by 3% and their operating margin decreases by 2% they are still considered 1.2% undervalued. While that may be true, the risk that revenue growth is negative or a decreasing operating margin is possible. Acquisitions tend to increase revenue initially but they also tend to sacrifice operating margins, one key consideration when accounting for their growth strategy.

Furthermore, competition, more specifically, product innovation in the SaaS industry could cause Enghouse to lose market share and therefore, revenue. As the Canadian economy enters into unprecedented times of debt and economic uncertainty, the risk that revenue growth doesn't materialize is something to consider.

A decrease in revenue or even stable revenue may also cause the valuation multiples to decrease further. Deflated multiples would have a considerable impact on the price.

High Proportion of Goodwill

Enghouse boasts an impressive balance sheet, with a substantial cash reserve, enhancing their financial stability. However, it would be imprudent to overlook their significant goodwill, accounting for about a third of their assets.

As active participants in M&A, the potential for impairment should be carefully considered, though Enghouse's prudent management has yet to incur any impairment charges over the last 5 years. In my opinion, this track record attests to their adept strategic acquisitions and sound accounting practices, instilling confidence in the company's financial health.

Conclusion

Enghouse Systems emerges as an undervalued gem in the market, as evidenced by consistent operating profits, dividends that have been increasing, the fact they are trading below their historic multiples, and a compelling discounted cash flow analysis. Key risks including the high proportion of goodwill and the risk that revenue growth doesn't materialize should be considered before purchasing Enghouse but in my opinion, it's clear that the bull case is more compelling for Enghouse. For investors looking for stable cash flows and a sustainable dividend, look no further.

For further details see:

Enghouse Systems: A Compelling Undervalued Opportunity