CA - Enghouse Systems FY2023 Results: Emerging As An Unexpected AI Player

2023-12-20 15:10:59 ET

Summary

- On December 14, Enghouse Systems released its annual report corresponding to the fiscal year 2023. Top line growth has returned after two years of normalization. Additionally, we can observe margin improvement.

- Services now represent 84% of total revenues, indicating that the transition to a SaaS business is being successful.

- For the first time in its history, Enghouse shared the company's initiatives regarding the use of artificial intelligence in its products and services.

- Valuation remains attractive despite the modest 5% rise since the release of the annual report.

Investment Thesis

Last week, on December 14, Enghouse Systems released its annual report corresponding to the fiscal year 2023.

Enghouse Systems Limited ( ENGH:CA), ( EGHSF ) is a Canadian software and services company that provides a range of technology solutions, including communication software, contact center solutions, and network infrastructure products. Previously, the company offered these products through perpetual licenses; however, it is currently transitioning to a Software as a Service (SaaS) model.

For more details, you can refer to my previous analysis , where I delve into this transition in greater depth. In this article, I will analyze the annual report to check the development of the transition towards SaaS. We will also delve into the intriguing role that the company plays as a provider of artificial intelligence, and I will update the valuation to give us an idea of what performance we could expect if we bought at the current price.

FY2023 Results

The company presented results that, in my opinion, were very good and encouraging. Top-line growth has returned after two years of normalization following the revenue 'boom' in 2020 driven by COVID-19. Additionally, we can observe an improvement in margins, attributed to the increased share of services in the revenue mix.

Here are the reported numbers:

- Revenue: It grew only 6% year over year, but annual growth in the fourth quarter was 14%. Additionally, this growth was affected by the 'blessed problem' of transitioning from selling perpetual licenses to gaining customers through subscriptions. Later, we will delve into the growth of each segment of the Revenue Mix.

This positive momentum was somewhat offset by declining software license revenue as we see increasing customer preference for SaaS solutions aligned with our commitment to provide our customers with choice.

-Management comments during the last conference call.

- EBITDA: It grew 14.5% year over year, reaching $127M, equivalent to an EBITDA margin of 28% compared to 26% the previous year.

- Free Cash Flow: It grew 12.6% and reached $114M, equivalent to a margin of 25% compared to 24% the previous year.

{kind=link}

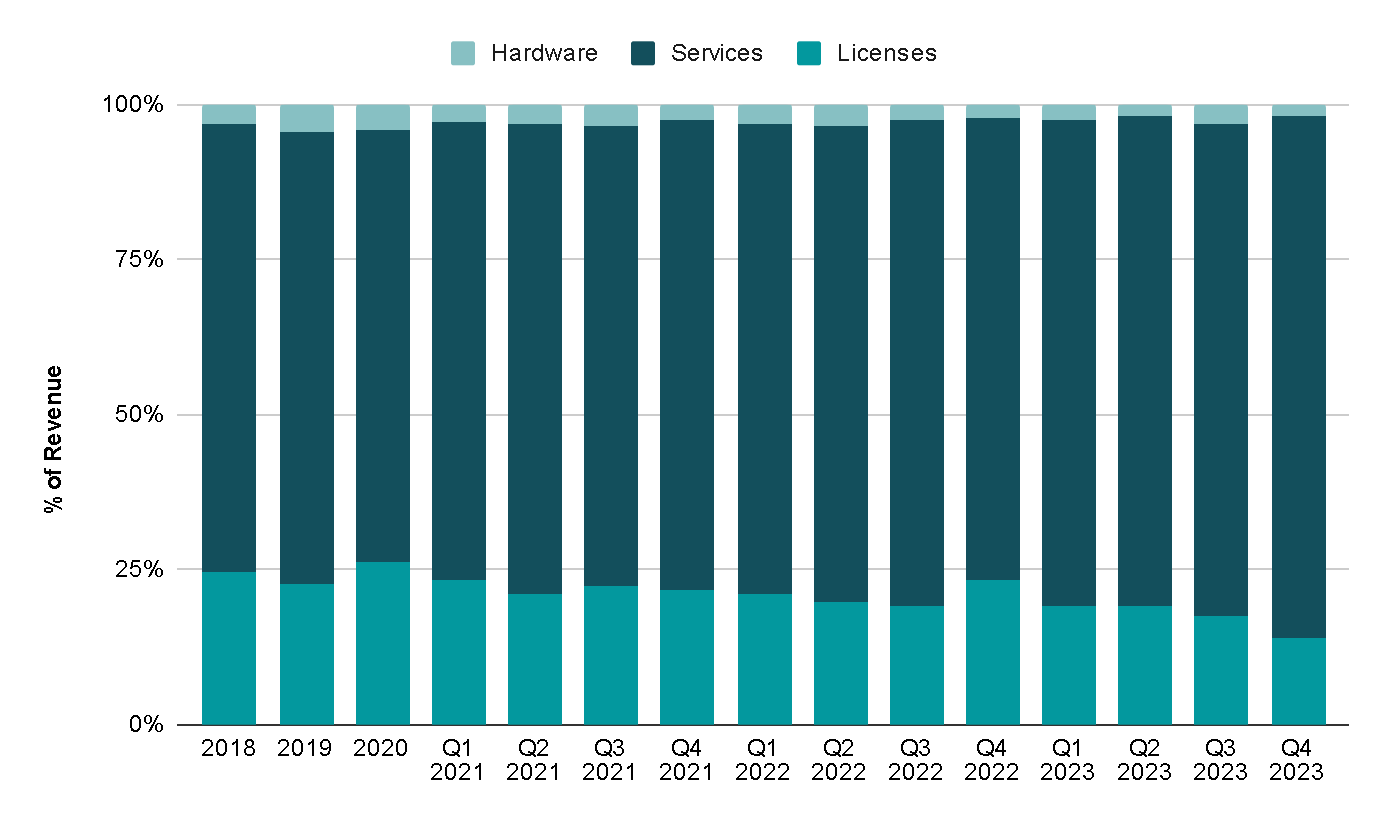

One of the most important metrics to monitor in each report is the weight of Services in the Revenue Mix. This is crucial because Services are characterized by their predictable and recurring nature.

In this regard, the company has shown consistent improvement every year. During the last quarter, Services represented 84% of Revenue, compared to 71% in FY2018. This is a highly positive development, indicating an enhancement in the company's fundamentals as it increasingly focuses on revenue streams with a more sustainable and recurring nature, moving away from one-off revenues such as perpetual licenses and hardware sales.

{kind=link}

Regarding the Gross Margin by segment, it is noticeable how the Hardware segment experienced the lowest margins in the last two years, which, albeit very slight, had an impact on the overall Gross Profit.

On the other hand, during the fourth quarter, the margins of the Services segment improved after a challenging Q2 that weighed on the final margin for FY2023. The Gross Margin of this segment was 62%. However, it's important to note that the Services segment comprises both SaaS revenue and Professional Services. It would be beneficial if the company could provide a more detailed breakdown of the margins for this segment, offering a clearer idea of the potential margin it could achieve once SaaS revenue has a greater weight in sales.

{kind=link}

The conservative policy in debt management persists, a characteristic that has defined Enghouse throughout its history. The net debt is -$228M, that is, with the cash on balance the company could pay all its debt.

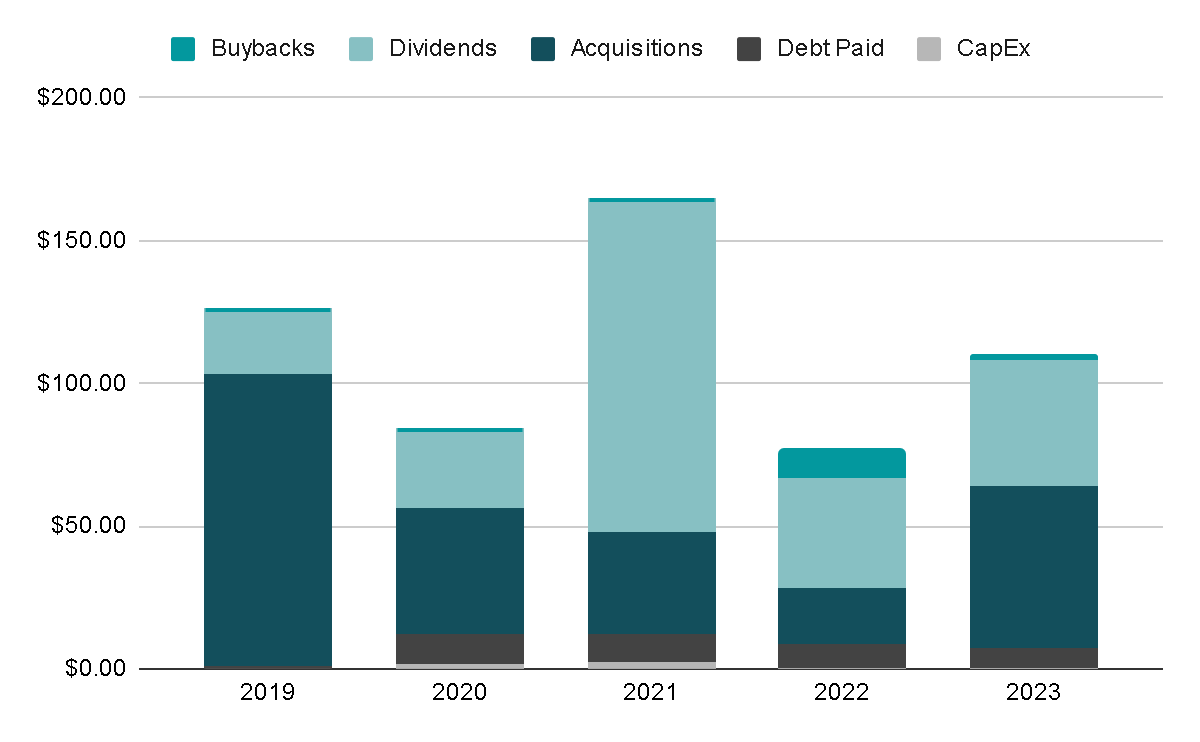

At the end of the year, the company increased Cash and Equivalents by $173M, compared to $167M the previous year. This is significant because the company typically utilizes cash for activities such as share buybacks, dividend payments, and acquisitions. Notably, in 2021, they even issued a special dividend.

We continue to actively pursue opportunities to strategically deploy our cash reserves on acquisitions and return cash to our shareholders in the form of dividends. Yesterday, the Board of Directors approved a quarterly dividend of $0.22 per common share.

-Management comments during the last conference call.

{kind=link}

If we annualize the $0.22 dividends per share that they plan to distribute in February 2024, it would amount to $0.88 Canadian dollars per year in dividends. At the current price of $34.85, this would represent a dividend yield of 2.52%. While dividends may not be the primary focus for the company, they serve as a positive factor, especially considering the low debt and strong cash generation. And at the end of the day, as the Spanish saying goes, no one is bitter about a candy .

As evident in the graph below, the capital allocation policy is very clear. Over the last five years, more than 80% of the cash has been allocated to both returning capital to shareholders through dividends and buybacks and making acquisitions with cash without issuing shares or taking on debt. In the specific FY2023 under consideration, three acquisitions were made, which we will discuss in more detail below.

{kind=link}

Acquisitions

Enghouse has a track record of generating value through its acquisitions. It typically pursues small, cost-effective acquisitions, integrates them to enhance profitability, and ultimately makes the initial investment appear even more favorable once the acquired company significantly improves its performance. This year was no exception, as management highlighted during the conference call:

In 2023, all three acquisitions that were completed were effectively integrated, transforming these companies from historical losses into profitability in the immediate quarter following each acquisition.

-Management comments during the last conference call.

Throughout this year, the company completed the acquisitions of Qumu , Navita , and Lifesize , all of which were successfully integrated into fiscal 2023. Based on my estimates, they collectively contributed around $130M pro forma in Revenue.

- Qumu: This company closely aligns with Enghouse, providing tools to create, manage, and measure live and on-demand video content for enterprises. Similar to Enghouse, it also generates revenue from maintenance and SaaS. Previously listed on the stock exchange, Qumu is estimated to have generated around $20M in revenue during the year, according to information from Investing.com.

- Navita: A Brazil-based provider, Navita offers a suite of products focused on managing and controlling critical mobile assets, as well as overseeing telecommunications and IT expenses. Its business model is purely Software as a Service, and Enghouse reported that it generated $7.5M in revenue in the last year.

- Lifesize: The final acquisition of the year, completed in August, Lifesize offers cloud software for the efficient management of hybrid workforces. Once again, it's evident what type of companies Enghouse is seeking. The purchase price for Lifesize was around $20M, a particularly intriguing figure considering my findings indicate that the company generated revenue ranging between $100M and $280M . This suggests that Enghouse managed to acquire Lifesize at a quite attractive price.

To analyze the efficiency of these acquisitions, we can examine the Free Cash Flow Return on Capital Employed (FCF ROCE). The following graph displays this standard metric alongside the goodwill-adjusted metric, as goodwill is typically generated on the balance sheet when making acquisitions. This year's ROCE improved slightly from the previous year, reaching 19.5%, though it still falls below the decade-long average of 21%. Meanwhile, the goodwill-adjusted ROCE stands at 29.7%. In both metrics, a clear value generation is evident with the acquisitions, particularly noteworthy considering they are conducted entirely in cash, further enhancing the contribution.

{kind=link}

AI Strategies

While artificial intelligence ((AI)) is currently in vogue among the market and investors, Enghouse has a longstanding history in this field. For the first time, the company has provided detailed insights into how they are leveraging AI, signaling promising opportunities for cost optimization within their products, benefiting both Enghouse and its clients.

Enghouse has been developing and integrating AI technologies since 2019, which commenced with the acquisition of Eptica and our approach involves integrating leading AI technologies with our own proprietary AI innovations.

-Management comments during the last conference call.

Here are some of Enghouse's AI initiatives and offerings:

- AI in Video Software: Enghouse's transcription engine is a pivotal software component that automatically translates phone calls and video recordings into text. This technology holds the potential for significant advancements in cost optimization.

- AI in Contact Centers: The company has introduced an AI-powered quality assurance product for contact centers. This tool automates the evaluation of agent performance by analyzing recorded interactions, scoring agent effectiveness, and providing recommendations. This not only enhances efficiency but also saves supervisors considerable time by reducing the need to manually review recordings.

- AI on Critical Services: Enghouse incorporates AI in its video healthcare solutions. The video fall detection technology is integrated into a virtual sitter application, allowing healthcare professionals to monitor multiple patients simultaneously. The system triggers alarms when a patient is falling or at risk of falling, whether in a home or hospital setting. Moreover, in emergency safety technology, AI is utilized to optimize the fastest route for emergency vehicles such as fire trucks, police cars, or ambulances. This involves considering various variables like vehicle size, traffic conditions, and traffic lights. The goal is to enhance efficiency and, ultimately, save lives.

In summary, Enghouse serves as a conduit through which its clients can implement AI in their custom software, enhancing the value of products and services and providing additional benefits.

Updated Valuation

To assess the potential return on investment at the current price, I will project revenue and margins, applying an exit multiple later on.

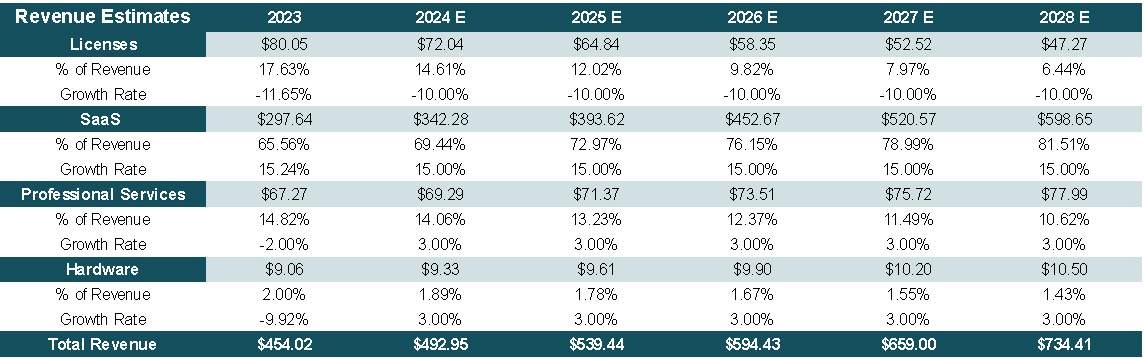

Over the next five years, I anticipate a 10% annual decline in License Revenue, while SaaS is expected to increase by 15% annually. This projection appears feasible given the 15% growth observed in the SaaS segment in the last year and a 10% growth over the past five years.

This would represent a compound annual top-line growth of 10.5% over the next five years.

{kind=link}

In the short term, this may result in somewhat subdued revenue growth, but as the Perpetual License segment decreases in weight, growth is expected to become more significant. Additionally, I foresee a gradual improvement in the EBITDA margin.

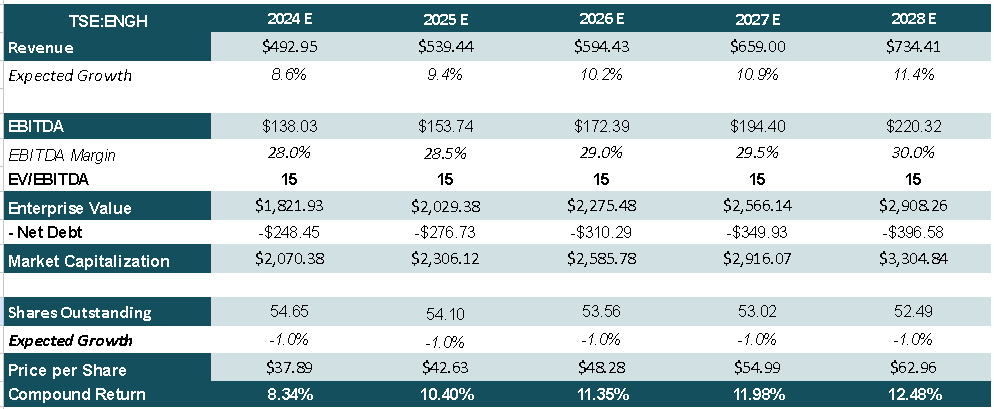

Applying an exit multiple of 15x EV/EBITDA and assuming the company continues to repurchase shares at a rate of 1% per year, the anticipated return would be around 12.5%, plus the current dividend yield of 2.5% per year.

{kind=link}

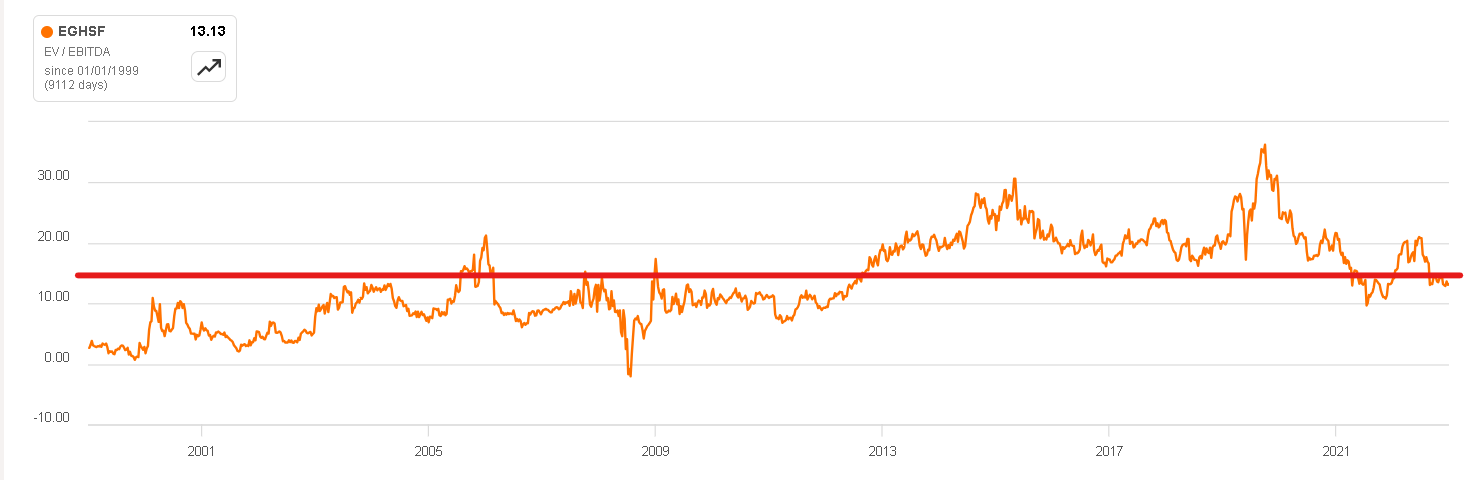

The choice of the EV/EBITDA multiple is based on the company's historical performance since 1999. Although the multiple has been around 20x in the last ten years, there is potential for upside if the market becomes more optimistic about Enghouse.

{kind=link}

Final Thoughts

This report paints a positive picture, and shareholders have reason to be pleased with the company's performance and future prospects.

Top-line growth has returned, profitability has improved, and the company has successfully executed cost-effective acquisitions. The Services segment is gaining more significance in revenue, the company maintains a debt-free status, and its ventures into artificial intelligence initiatives appear promising. Despite a valuation that could be more favorable, the current Free Cash Flow Yield of 6% and an EV/EBITDA multiple of 13x make it seem like a reasonable opportunity to initiate a position. With the confirmation that the transition is progressing smoothly, Enghouse, in my view, is a 'buy'.

On the other hand, risks remain the same. Essentially, everything revolves around the fact that Enghouse is a technology company, making competition inherently challenging, particularly for a Small Cap with a $2 billion Market Cap. Additionally, the technology industry is dynamic, and swift technological changes could influence the relevance of Enghouse's solutions. Failure to adapt to emerging technologies or industry disruptions could significantly impact the company's revenue and profitability.

For further details see:

Enghouse Systems FY2023 Results: Emerging As An Unexpected AI Player