CA - Enghouse Systems Reports Revenue Growth As Customers Value Choice

2023-06-15 19:30:46 ET

Summary

- Enghouse Systems Limited reported FQ2 2023 financial results on June 12, 2023.

- The firm provides solutions in the online customer communications and asset management industries.

- Enghouse reported revenue growth, but operating profit fell sequentially.

- The company has the potential to take market share from weaker competitors but faces slowing macroeconomic conditions and higher short-term expenses on transit projects.

- While I'm on Hold for Enghouse in the near term, the stock is worth putting on a watch list for future consideration.

A Quick Take On Enghouse Systems

Enghouse Systems ( ENGH:CA ) reported its FQ2 2023 financial results on June 12, 2023, producing revenue growth of 6.7% year-over-year.

The firm provides a range of software products in the online customer communications and asset management industries.

While valuation appears stretched at current levels, if Enghouse can execute better than its rivals, some of which may be struggling, the stock may have further upside potential later in 2023 or in 2024.

For the time being, I’m on Hold for Enghouse Systems, but I suggest putting it on a watchlist for future consideration.

Enghouse Systems Overview

Markham, Canada-based Enghouse Systems was founded in 1984 to provide customer interaction software for companies in all industries and various asset management solutions for telecom, utility and transportation & safety organizations.

The firm is headed by Chairman and Chief Executive Officer, Stephen Sadler, who was the Vice-Chairman and CEO of Geac Computer Corporation prior to joining Enghouse. He was also Chairman of Helix Investments.

The company’s primary offerings include the following:

-

Contact center software

-

Video conferencing software

-

Public transportation and safety software

-

Telecom service provider software

-

Network virtualization software

The firm acquires customers through its direct sales and marketing efforts, through partner referrals, and by acquisition.

Enghouse Systems’ Market & Competition

According to a 2023 market research report by Grand View Research, the global contact center software market was estimated at USD $28.1 billion in 2022 and is forecast to reach USD $156 billion by 2030.

This represents a very strong forecast CAGR of 23.9% from 2023 to 2030.

The main driver for this expected growth is increasing adoption of cloud-based and virtual contact center solutions to achieve better business continuity.

Also, the chart below shows the historical and projected future growth trajectory of the U.S. contact center software market, by solution, through 2030:

U.S. Contact Center Software Market (Grand View Research)

Major competitive or other industry participants include:

-

8X8

-

Ameyo

-

Amtelco

-

Aspect Software

-

AVOXI

-

Cisco Systems

-

LiveVox

-

Five9

-

Genesys

-

Microsoft

-

NEC

-

Nice

-

SAP SE

-

Talkdesk

-

Twilio

-

UiPath

-

Unify

-

VCC Live

Enghouse is active in several other major software markets worldwide, including business and operations support systems, virtualized network functions, and transportation and public safety.

Enghouse’s Recent Financial Trends

-

Total revenue by quarter has risen recently after falling in 2022; Operating income by quarter has dropped in recent quarters:

Total Revenue and Operating Income (Seeking Alpha)

-

Gross profit margin by quarter has decreased recently; Selling, G&A expenses as a percentage of total revenue by quarter rose in the most recent quarter:

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

Earnings per share (Diluted) have trended lower year-over-year:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP, CAD $)

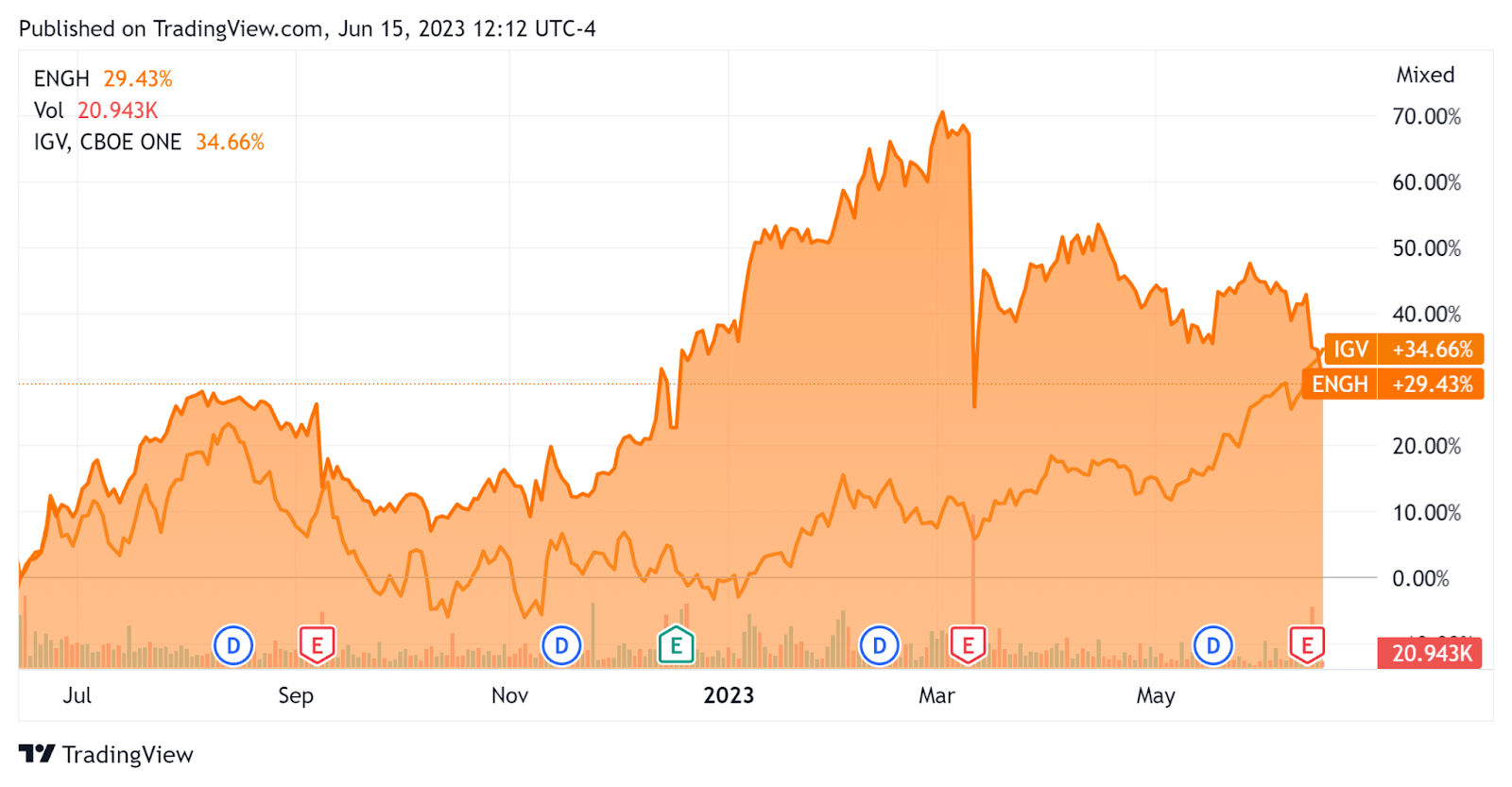

In the past 12 months, Enghouse’s stock price has risen 29.43% vs. that of the iShares Expanded Technology-Software ETF’s ( IGV ) growth of 34.66%, as the chart indicates below:

{kind=link}

For the balance sheet, the firm ended the quarter with CAD $234.5 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash flow was CAD $95.0 million, during which capital expenditures were only CAD $0.7 million. The company paid only CAD $1.9 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Enghouse

Below is a table of relevant capitalization and valuation figures for the company:

| Measure ((TTM)) |

| Amount |

| Enterprise Value/Sales |

| 4.0 |

| Enterprise Value/EBITDA |

| 17.0 |

| Price/Sales |

| 4.5 |

| Revenue Growth Rate |

| -4.0% |

| Net Income Margin |

| 19.7% |

| EBITDA % |

| 23.6% |

| Net Debt To Annual EBITDA |

| -2.3 |

| Market Capitalization |

| $1,940,000,000 |

| Enterprise Value |

| $1,720,000,000 |

| Operating Cash Flow |

| $95,660,000 |

| Earnings Per Share (Fully Diluted) |

| $1.54 |

(Source - Seeking Alpha, CAD $)

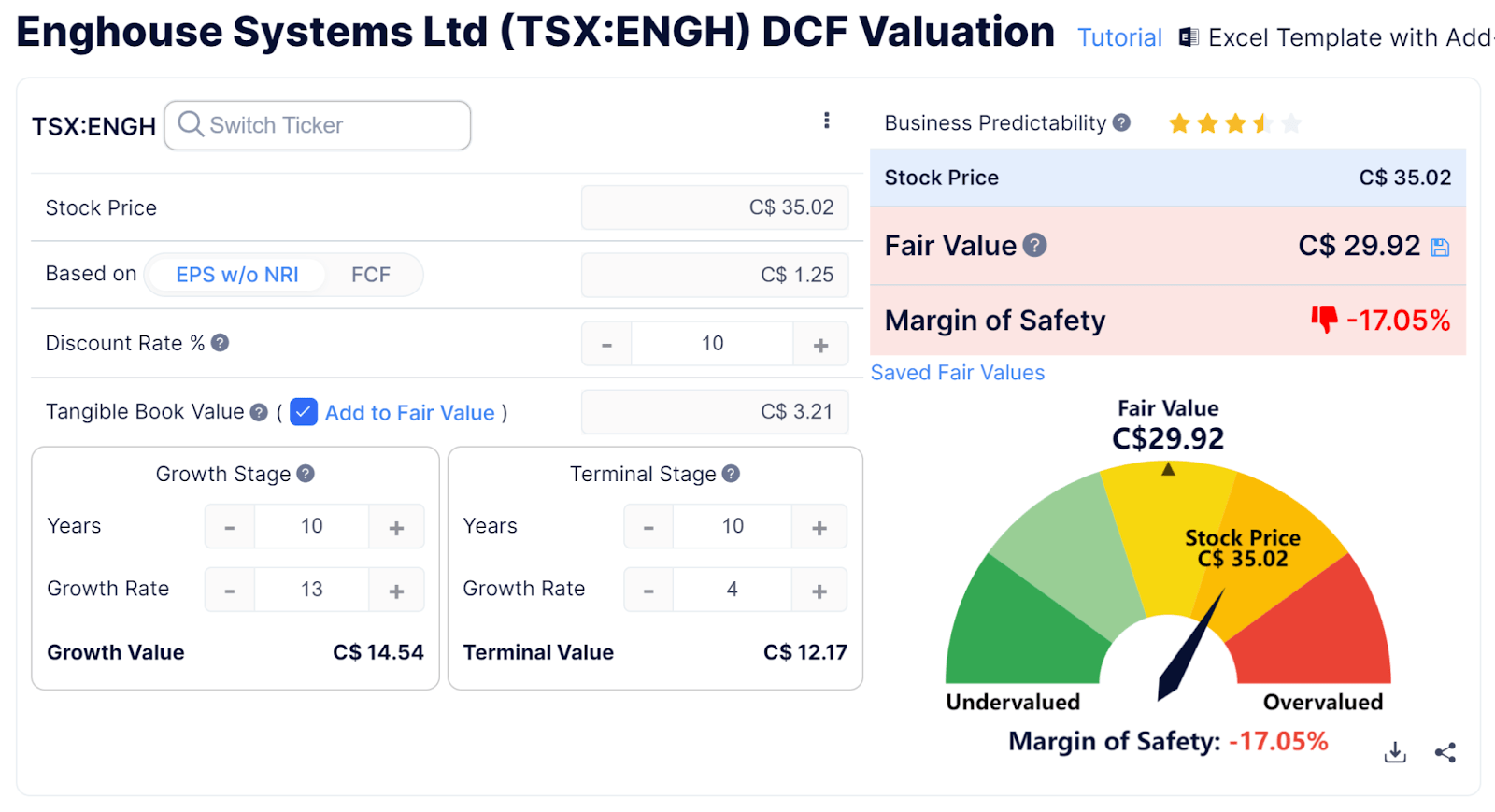

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

{kind=link}

Assuming generous DCF parameters, the firm’s shares would be valued at approximately CAD $29.92 versus the current price of CAD $35.02, indicating they are potentially currently overvalued, with the given earnings, growth, and discount rate assumptions of the DCF.

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

Enghouse’ most recent Rule of 40 calculation was 19.6% as of FQ2 2023’s results, so the firm is in need of improvement in this regard, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| -4.0% |

| EBITDA % |

| 23.6% |

| Total |

| 19.6% |

(Source - Seeking Alpha, CAD $)

Commentary On Enghouse

In its last earnings call (Source - Seeking Alpha), covering FQ2 2023’s results, management highlighted the completion of two acquisitions. One for its video creation, management and delivery offerings and the other for its mobile asset management and telecom and IT expense management offerings.

The company's gross margins were negatively impacted by higher-than-usual implementation costs, which management expects to be reduced as these large public safety projects advance.

Leadership also spoke to its workaround employing AI and ML to improve efficiencies internally, as well as to support its product portfolio through potential automation capabilities at scale.

Management did not disclose any company, customer or dollar retention rate metrics.

Total revenue for FQ2 2023 grew by 6.8% YoY, while gross profit margin dropped by two percentage points.

Selling, G&A expenses as a percentage of revenue increased by 2.3%, a negative signal, and operating income fell 18.7% YoY.

Management did not provide any forward financial guidance.

The company's financial position is strong, with substantial liquidity and no debt; free cash flow was strong in the trailing twelve months.

Enghouse’s Rule of 40 performance has been subpar recently, with a lack of revenue growth, the primary culprit of its disappointing performance.

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

Earnings Transcript Key Terms Frequency (Seeking Alpha)

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited ‘Recession’ once and ‘Challeng[es][ing]’ two times.

The negative terms refer to a potential recession ahead that may lead to greater acquisition opportunities for the company.

Analysts questioned management about the drop in gross margins, with management highlighting both the large transit projects that are coming online and the fact that SaaS revenue models tend to have lower gross margins than on-premise revenue models.

Regarding valuation, my discounted cash flow calculation suggests that the company's stock is potentially overvalued at current levels.

A potential upside catalyst to the stock could include a higher margin trajectory as its large transit projects come online and move to maintenance fee revenue, but that will probably take some time to materialize.

A risk to the company is a downturn ahead, slowing sales cycles and increasing customer churn.

The firm appears to differentiate itself from competitors in its ability to provide a range of choices to customers, from multi-tenant SaaS to private cloud or on-premises solutions.

While valuation appears stretched at current levels, if Enghouse can execute better than its rivals, some of which may be struggling, the stock may have further upside potential later in 2023 or in 2024.

For the time being, I’m on Hold for Enghouse Systems, but I suggest putting it on a watchlist for future consideration.

For further details see:

Enghouse Systems Reports Revenue Growth As Customers Value Choice