DPZ - Enjoy A Slice Of DGI Courtesy Domino's Pizza But Wait For Better Entry Point

2023-11-14 09:35:23 ET

Summary

- Domino's Pizza has a history of strong shareholder returns that appears likely to continue for years to come.

- This company has a solid business model, is well-managed, and is positioned for continued success even if a recession hits.

- The company's highly leveraged capital structure presents some risk, but I believe the company is well-positioned to manage this risk.

- A conservative DCF model shows that the stock has traded close to fair value within the past month.

- I rate DPZ a "Hold" after its current run to $378.51 but would rate it a "Buy" under $340 which I expect to see again given recent volatility.

Editor's note: Seeking Alpha is proud to welcome Quality Dividend Growth as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

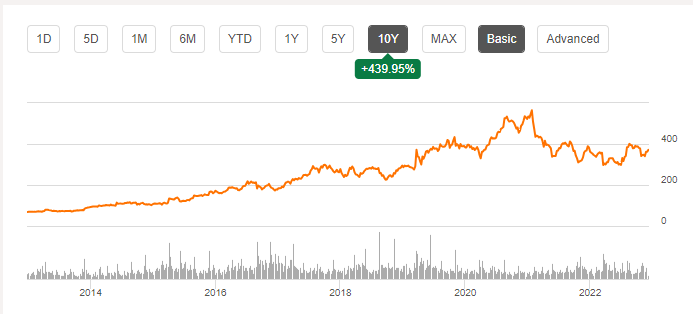

Domino's Pizza (DPZ), the world's largest pizza company, has rewarded investors very handsomely since its IPO in 2004. Excluding dividends, the share price has grown 439.95% or at a CAGR of 18.52% over the past 10 years as shown below. The company's efficient, growing, franchised business model requires relatively low CapEx which has allowed the company to return as much as 70% of its operating cash flow to investors in the form of dividends and share buybacks. In the past decade, Domino's has increased its dividend at a 19.72% CAGR while reducing its outstanding share count by an impressive 38%. Notably, the latter was aided strongly by several recapitalizations where the company issued billions of dollars' worth of long-term debt and used the proceeds to repurchase shares, which is why the company's equity is negative. The most recent recapitalization was in 2021 .

10 Year Outstanding Share Reduction (Company Financials)

{kind=link}

In this article, I will explain why I expect Domino's to continue to reward shareholders (and customers) going forward. I will examine some of the key risks that the business faces, especially its high long term debt as well as the highly competitive market that it competes in, and I will argue why the company is well-positioned to navigate these risks successfully even if a recession hits. I will also explain my DCF analysis which suggests that the stock has traded within a price range that is close to fair value over the past month although the price has recently run approximately 10% higher, meaning that DGI investors should have an opportunity to buy a wonderful business for a fair value if they are patient and wait for a probable dip.

Background

While the stock price has done very well over the past decade, the stock has decreased approximately 32.9% from its all-time highs achieved in late December 2021. Three main concerns have driven this decrease:

- Higher interest rates

- Gross margin pressures

- Weak revenue growth

Let's take a look at each of these concerns to better understand them.

Higher Interest Rates

Domino's capital structure is very highly leveraged: as of September 2023, the company had $5.0 billion in long term debt with a stockholders' deficit of ($4.1) billion and only $283 million in cash, of which $81 million was unrestricted cash and $202 million was restricted cash (primarily for debt covenants) as per its Q3 2023 10-Q . While negative equity can often be a red flag, in this case it was crafted on purpose: Domino's completed several leveraged buyouts over the past 20 years which resulted in massive share buybacks that created a negative equity balance on the balance sheet. These leveraged buybacks happened when interest rates were significantly lower than they are now and where the market now expects rates to be over the next several years. Naturally, the market is concerned that higher interest expenses could reduce what Domino's is able to return to shareholders via dividends and buybacks while investing in its continued growth. Additionally, there is risk of the company losing its investment-grade credit rating if credit agencies become concerned that the company will not be able to service its debt obligations.

I am not too concerned about the debt for a few reasons. First, as shown in the company's 2022 10-K , the company's existing long term notes are fixed rate notes averaging 3.8%, so the increased cost of borrowing has not impacted Domino's yet. The company also owes very little in payments until 2025 and beyond:

{kind=link}

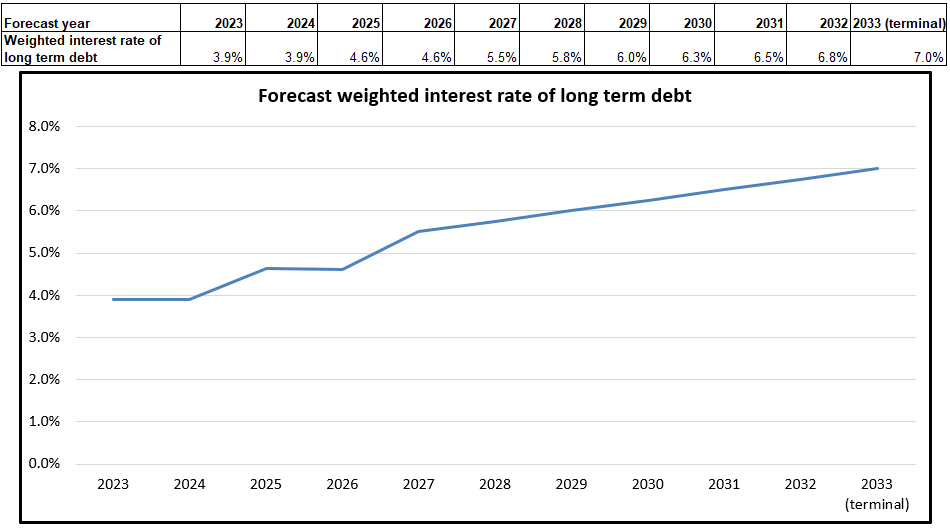

I do think it is most probable that Domino's will issue new debt by 2025 to cover this obligation and that the new debt will likely be significantly higher than a 3.8% interest rate. I have factored this into my DCF model: I forecast that 20% of the long term debt will be reissued in 2025 at an 8% interest rate (which I believe is conservative), bringing the weighted average up to 4.6%. I then forecast that another 20% is reissued in 2027, bringing the weighted average to 5.5%. From there, I forecast the company's weighted average interest rate to gradually increase to 7% by the terminal year (2033). I believe that the actual rates will likely be lower, but I wanted to use numbers that would provide some margin of safety.

{kind=link}

If this scenario plays out, then the company's interest expense as a percentage of operating cash flow (currently an approximate 10%) will gradually close to double over time which will reduce the growth of the amount of cash that can be returned to shareholders, but I believe that actual interest rates will not be quite so high and that the company will still generate plenty of levered FCF to return to shareholders.

The company's cash balance is relatively low, but at this time it really doesn't need to any higher. The company has very efficient working capital: receivables and inventory turn faster than what is due for current liabilities as explained in the 2022 10-K:

Historically, our receivable collection periods and inventory turn rates are faster than the normal payment terms on our current liabilities resulting in efficient deployment of working capital. We generally collect our receivables within three weeks from the date of the related sale and we generally experience multiple inventory turns per month. In addition, our sales are not typically seasonal, which further limits variations in our working capital requirements. These factors allow us to manage our working capital and our ongoing cash flows from operations to invest in our business and other strategic opportunities, pay dividends and repurchase and retire shares of our common stock.

Net Working Capital Turnover in 2022 was an impressive 14.3, suggesting very strong liquidity to cover current obligations. Thus if the company was to hold more cash it would not be a wise use of capital.

Gross Margin Pressures

Domino's has not been immune to the challenges of high inflation and tight labor supply caused by the Covid-19 pandemic. According to the 2022 10-K and the Q3 2023 10-Q, higher food prices, especially cheese, significantly increased the Cost of Goods Sold from 61.3% of sales in 2021 to 63.7% of sales in 2022. However, this has already decreased back to 61.4% through the first three quarters of 2023 thanks to supply chain efficiencies that Domino's has implemented.

Many investors are concerned that revenue has decreased in 2023 thus far by 2.2%. However, much of this revenue decrease was driven by the Supply Chain segment, which contributes more than 60% of the company's total revenue but only 25% of the company's income as of Q3 2023. The average pricing of Supply Chain's sales to stores has dropped by 1.7% Y/Y due to a combination of lower food costs and new efficiencies implemented, but this is more than offset by the reduction in Cost of Goods Sold of the Supply Chain business and hence not harmful to the company's gross margin. Additionally, lower pricing of the Supply Chain's sales to stores will help the stores to be more profitable and generate more royalty income for Domino's which in turn helps the company's margins.

Weak Revenue Growth

Much of the decrease in Q1-Q3 2023 revenues was driven by the Supply Chain segment as already discussed above.

2023 Q3 same store sales decreased modestly by 0.6% in the US as a result of the company's fortressing strategy . The goal of the fortressing strategy is to improve its service to customers and drive overall sales growth by purposely opening new stores that overlap a portion of the territory of some existing stores. This will clearly cannibalize some existing stores' sales, but the company believes it will drive overall transaction growth via quicker service to customers. Thus, it should not be a surprise if most of Domino's future revenue growth comes from new stores and not existing stores.

Global retail sales actually increased 4.9% in 2023 Q3 adjusted for foreign currency impacts. Domino's expects a strong Q4 with close to 6% growth in global retail sales. It's 2-3 year outlook is 4-8% growth as per its 2023 Q3 press release. Thus, while overall 2023 revenue has not been worthy of a growth stock, the growth picture looks much better going forward. Based on the average estimate of $1.42B Q4 revenue , Domino's total 2023 revenue should be down 0.9% Y/Y.

The CAGR of the Quick Service Restaurant [QSR] industry is forecast to grow anywhere between 3.65% to 11.2% through 2031 according to a variety of market research forecasts including Market Research Future , Proficient Market Insights , and Fortune Business Insights - quite a wide range in forecasts and only a sample of what various market experts predict. I decided to base my revenue forecast on the midpoint of Domino's 2-3 year outlook (6%) which I believe is fair given the opportunities that Domino's has to open new stores in both the US and internationally while increasing transactions at existing stores. Starting in 2024 I assume a 6% growth rate through 2029 and then taper down to a terminal rate of 3% by 2033 in my DCF model.

{kind=link}

Domino's Competitive Advantage and Why It Will Succeed

I have covered the most pressing concerns that many investors have regarding Domino's and why I am not concerned. However, Domino's still belongs to an intensely competitive industry. Why should investors choose DPZ as opposed to any of its competitors, or any other investment option for that matter? Especially DGI investors when the stock currently yields only 1.31%?

It is important to invest in businesses that have a sustainable competitive advantage and generate high levels of free cash flow. For Domino's, its competitive advantages are its highly efficient, well-scaled business model and its customer-centric focus and innovation, both of which it should be able to sustain in the future.

Highly Effective and Efficient Business Model

Most Domino's stores are independently-owned and operated franchises. According to the company's website , 95% of franchisees started their Domino's careers as part-time pizza makers or delivery drivers. Currently, only internal candidates are considered for franchising opportunities, and these candidates must have been a general manager or supervisor of a store for at least a year. Consequently, the people running the stores are familiar with business operations and are heavily vested in the success of their stores.

CapEx costs mostly fall on the franchisees, keeping Domino's overall CapEx costs relatively low. Domino's spends the majority of its CapEx on supply chain equipment and on software innovation. Its Levered FCF/Cash from Operations is 70% which is comparatively high (this will be discussed more later), allowing the company to return the majority of the operating cash that it generates back to shareholders.

Domino's has created a world-class supply chain system that supplies its stores with fresh, prepared, low-cost ingredients. The stores just have to focus on making pizzas and other menu items; most of the preparatory work is already done for them. The key difference between Domino's supply chain vs. its competitors is that most of Domino's supply chain is internally managed while many QSR's have outsourced their supply chains, and the highly effective and efficient supply chain that Domino's manages gives it a competitive advantage for controlling costs without compromising quality or consistency. As the world's largest pizza company, it benefits from economies of scale that help to keep costs low compared to competitors. Additionally, the company has designed menus that are simple for store operations yet flexible for providing customers with ample options.

Altogether, this business model allows Domino's to offer very competitive prices while still offering customers much value compared to competitors. I believe the company is well-positioned to utilize its scale, its supply chain system and its knack for innovation to sustain this competitive business model.

Customer-Centric Focus and Innovation

Domino's has a proven history of delivering value to the customer's entire experience beyond the food itself. In addition to providing quality food at excellent prices, the company has developed several innovations over time to make the customer experience more convenient and rewarding. Examples include the famous Domino's Heatwave Hot Bags to keep pizzas hot during deliveries, the Order Tracker and Pizza Builder system, and its new Pinpoint Delivery system where a customer can have pizza delivered to a non-street address such as a park or a beach amongst many other innovations. While its competitors have copied many of these innovations to some extent, Domino's is usually a step ahead and releasing its next innovation while competitors are busy copying the prior one. I expect that Domino's will continue to innovate and find ways to appeal to the customer's overall experience.

Furthermore, Domino's recently revised their customer rewards program so that customers receive rewards points for orders of at least $5 (formerly $10) and also have more redemption options than before, starting at 20 points (formerly 40).

{kind=link}

This is a strong value proposition when many competitors are raising prices due to inflation and shrinking the number of options on their value menus. (Domino's has opted more for "shrinkflation" than for raising prices - for example, it's signature $7.99 carryout deal for a large pizza in the US now offers only one topping instead of three toppings, but the pizza is still $7.99.)

{kind=link}

Several analysts on the Q3 earnings call voiced concerns regarding the revised rewards program and coupon deals and how both of these will affect margins, but Domino's is confident that these moves will help to drive transaction growth and boost the company's overall sales, income and also customer loyalty. This is because customers are becoming more price conscious due to high inflation costs that has pinched their discretionary spend - Domino's believes that it can use its scale and efficiency to appeal to price-conscious consumers while still generating profit. This gives it an advantage over its competitors during pricing wars.

What About a Possible Recession?

If a recession does hit, I believe that Domino's efforts to appeal to price-conscious consumers will pay off because consumers will still need to eat and don't always have time or want to cook. A recession would likely cause more consumers to become price-conscious and seek value in their eating choices. Customers love to feel like they are getting a great deal, and redeeming free appetizers or side items more often feels even better when budgets are tight.

I think the biggest concern for Domino's during a recession would be that fewer franchisees would want to open new stores, and this could temporarily slow Domino's growth ambitions.

Comparison to Competitors

Domino's has many competitors, both direct and indirect (grocery stores that serve prepared meals, mail service meal kits, etc.). These companies compete with Domino's not only for customers and employees but also for investors as well. I looked at both Yum! Brands ( YUM ) and McDonald's ( MCD ) to see how some of their key metrics compare to DPZ:

Author's table using Seeking Alpha data

Liquidity

Compared to these direct competitors, Domino's has the highest Current Ratio but the lowest Quick Ratio. However, recall from earlier the company's Net Working Capital Turnover of 14.3 which means that it can operate safely with a lower Quick Ratio compared to most companies. Thus, I am not concerned about Domino's liquidity.

Dividend Yield, Payout and Growth

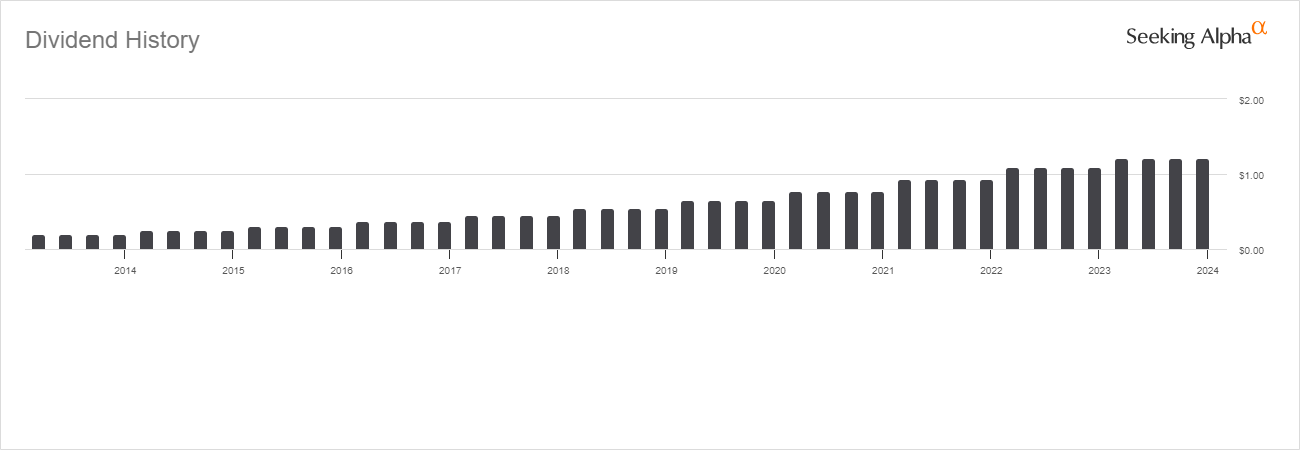

Of the three companies, Domino's currently has the lowest dividend yield but also the lowest payout ratio and the highest five-year dividend growth CAGR. The relatively low 32.4% payout ratio provides a margin of safety for the company's ability to continue growing the dividend at a high rate. At the current 17.52% CAGR the dividend is nearly doubling every four years. It is worth noting that most of the company's remaining Levered FCF not paid out in dividends is being used to buy back shares which is also a form of shareholder return, and as the table shows Domino's does boast the highest reduction of outstanding shares over the past decade at an impressive 38%. Furthermore, because the company allocates most of its Levered FCF to share buybacks, it always has the option to reduce buybacks and allocate a higher percentage to dividend payouts. DPZ currently has an 11 year streak of dividend growth which I expect to continue: I don't see why this company shouldn't become a Dividend Aristocrat down the road.

{kind=link}

Operating Efficiency and Margins

Additionally, Domino's boasts a higher Levered FCF/Cash from Operations of 70% thanks to its efficient, low CapEx business model. This means that as the business grows, a higher portion of its increased Cash from Operations will be available to reward shareholders through dividend increases and share buybacks. Because of this, I am not concerned that Domino's has lower Gross, EBIT and Net Margins than its competitors - this makes sense given the way its Supply Chain business segment operates (which lowers gross margin but makes its stores more competitive). However, I would expect to see margins improve steadily over time as the company continues to scale, especially its EBIT and Net Margins as a result of decreased SG&A as a percentage of sales.

Valuation

Forward PE is quite comparable for all three stocks, with DPZ the highest by a slight amount. However, it also has the highest FCF Yield, suggesting that it is attractively valued compared to its competitors. I will analyze the stock's valuation much further in the next section as I dive further into my DCF analysis.

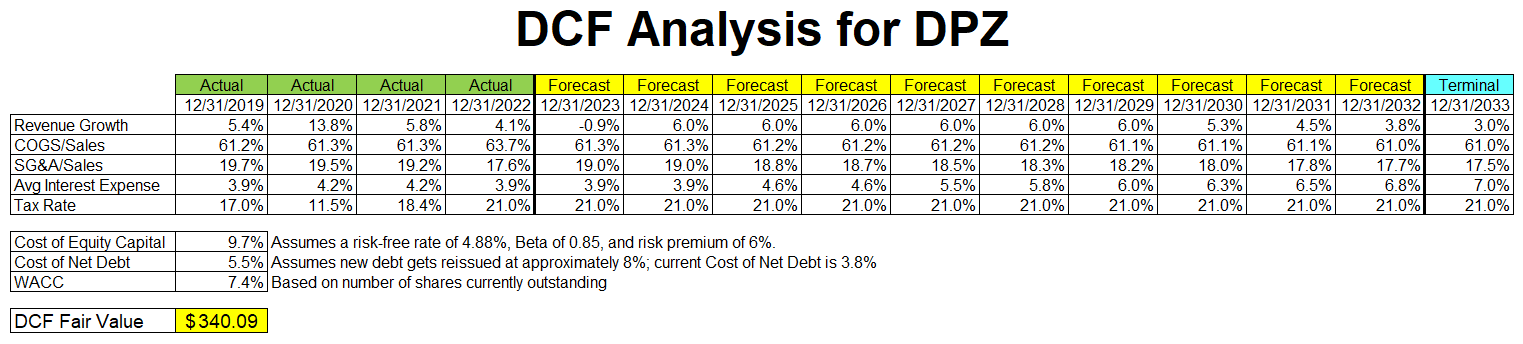

My DCF Analysis

Ultimately, the intrinsic value of this stock is the Net Present Value of its discounted future cash flows, particularly its FCF to Common Equity. Of course, everyone's DCF model looks different because we all make different assumptions about the company's growth and margins. Here are my own assumptions based on my research and analysis:

{kind=link}

My calculated fair value using conservative assumptions is $340 per share, which is 10.1% lower than the market price $378.51 as of the time of this writing, but within the range of $333 to $379 that the stock has traded over the past month.

Revenue

As discussed earlier in this article, 2023 Revenue should be 0.9% lower than 2022 if Q4 estimates of $1.42B materialize, and I then forecast average revenue growth of 6% based on the company's own 2-3 year outlook (4-8%) and market forecasts for the QSR industry. I used a 3% terminal rate in year 2033. If a recession does hit in 2024 then growth could be lower: each incremental decrease of 1% to my forecasted 2024 growth rate lowers the fair value by approximately $4, so a flat 2024 would result in a fair value of $316. However, as discussed earlier I expect Domino's to be well positioned in a recession due to the efforts it is already making to offer low-price value to customers.

Cost of Goods/Sales

As noted earlier this has already returned to 2021 levels of 61.3%. I forecast a very gradual decrease in this metric (which is favorable) due to efficiencies of scale, but I expect that Domino's will do better than what I forecast so there should be some margin of safety in this forecast.

SG&A/Sales

This metric is also running close to 2021 levels due to high inflation, but I do expect it to start decreasing again as the company continues to scale while inflation moderates.

Average Interest Expense

As previously discussed, I expect this to rise as the company refinances its current long term notes over the next several years starting in 2025. I think 7% is on the high side for a terminal rate given long-term average interest rates and the company's investment-grade credit rating, but I wanted to be conservative.

Tax Rate

I assumed a continued rate of 21%, matching 2022.

WACC

For Cost of Equity I assumed a risk-free rate of 4.88%, 24-month Beta of 0.85, and a Risk Premium of 6% which I felt was on the conservative side and is higher than most published estimates. I used the number of shares outstanding for weighting purposes because the company has negative equity. I also assumed a Net Cost of Debt at 5.5% which is higher than the current 3.8% given that I expect this to rise over the next several years.

Fair Value

If I had to give a range for estimated fair value, I would argue that fair value is $325 in the pessimistic scenario, $355 in the optimistic scenario, and $340 in the base scenario.

Thus, at the time of this writing the stock is trading at a premium, but given the stock's volatility and trading range over the past month I think that opportunities to "buy the dip" will present themselves. I recently added some shares when the price was under $340 and would gladly add more if the price drops near that level again. I am a firm believer in Warren Buffet's famous proverb that it is better to buy wonderful businesses at fair prices than to buy fair businesses at wonderful prices. As a long-term DGI investor, I do believe that Domino's is a wonderful business that will generate Alpha over the next decade or more, and I don't fret much about short-term volatility.

Other Risks

Domino's faces other significant business risks as well, including:

- Consumer health focus

- Use of single source suppliers

- Advertising funds are tied to store sales

Consumer Health Focus

Domino's is not known for serving healthful food options. Any consumer trends that favor more healthful eating and avoidance of fast food would be a headwind for the QSR industry, including Domino's.

Single Source Suppliers

According to its 2022 10-K, Domino's purchases all of its cheese from a single supplier, and it also purchases most of its meat from a single supplier. While the company does maintain sourcing agreements with its major suppliers, this still presents significant supply chain risks if these single suppliers run into operational problems (including foodborne illness) or supply issues of their own. While Domino's could likely work to procure these materials from other sources, the quality or availability of supply and the pricing might not be favorable if an extended disruption were to occur. With ongoing labor shortages this is a valid risk.

Advertising Funds are Tied to Sales

Domino's collects a royalty from its stores, typically around 6%, specifically allocated to an "U.S. franchise advertising" reserve which acts as a non-profit passthrough to fund corporate advertising spend. This means that if revenue growth continues to be weak or even declines, then advertising spend would also decline unless the company contributes money at the corporate level which would reduce the cash available to return to shareholders.

Conclusion

While I consider DPZ more of a "Hold" at its current price of $378.51, I consider it a "Buy" under $340 and given recent volatility believe that we could likely see that price again in the near future. I recently added shares in the past month when the price was under $340 and plan to hold shares for at least a decade while collecting a high-growth dividend each year. I look forward to seeing Q4 results and whether the company will show a strong return to growth, which I am confident that it will. The business faces several challenges primarily related to higher interest rates and fierce competition, but I believe that the company is well-positioned to navigate these challenges and continue to deliver for shareholders and customers alike. The company is well-managed, has a highly competitive business model, and operates in a market that should allow for solid revenue growth for years to come. While the dividend yield is only 1.31%, I expect it to continue to grow the dividend at a high CAGR of at least 10% (likely higher) and for the company to continue to reduce its number of outstanding shares, although it will likely back off the leveraged buyouts now that interest rates are much higher than they were over the past decade. I believe that the dividend is safe, will continue to grow at a high rate, and will not hold back the company's growth plans. As a long-term DGI investor I like DPZ for both its dividend growth and expected capital appreciation which I believe will beat the SP500 over the next decade.

For further details see:

Enjoy A Slice Of DGI Courtesy Domino's Pizza, But Wait For Better Entry Point