ENVX - Enovix: A Dangerous Game

2023-08-31 06:46:19 ET

Summary

- Enovix's valuation is aggressive, and investors are playing a dangerous game.

- The battery industry operates on commodity economics, favoring low-cost producers, which will make it difficult for Enovix to scale and compete.

- Even if everything goes right, the capital intensive, low margin, and fiercely competitive nature of the battery industry will limit the upside for profitability.

- We find the current risk/reward to be terrible and find it unlikely that Enovix can justify their current valuation.

- The most likely scenario is that Enovix either is unable to become a threat or gets crushed by the well capitalized incumbents.

Thesis

There have been many articles written about Enovix (ENVX) that cover the technology, potential demand and use cases, and management's projections. Since the company is essentially pre-revenue, this appears to be all that we can go off of. Rather than focus on the projected quantitative aspects as many authors have done before, the purpose of this writeup is to go over some of the more qualitative aspects. We believe that the valuation is aggressive and investors are playing a dangerous game.

The Dynamics of the Battery Industry

The battery industry operates similar to the solar industry in that there is a tremendous focus on keeping costs low. While there may be variations between producers, cost is ultimately the most important factor. Investors can look to the dynamics between First Solar ( FSLR ) and their Canadian and Chinese peers. Even though First Solar has a differentiated product based on thin film Cadmium Telluride, for most of the past decade they have been losing to their lower cost peers that rely on a crystalline silicon technology. Only with government support has the business of First Solar had a chance of becoming cost competitive. Even then investors should go and check out the valuations granted to solar panel companies, they are quite low. This is because the industry is ultimately one based on commodity economics. The same is true about the battery industry.

While many Enovix bulls will argue that their technology is superior and that it can demand a premium, this dynamic has not mattered in other markets such as solar panels. The lowest cost producers are the ones who win because they end up flooding the market with low cost products, sometimes even selling at or below cost. This has the effect of sucking demand away from their lesser-capitalized peers and makes it difficult for them to actually scale their differentiated product to become cost competitive with the conventional solution.

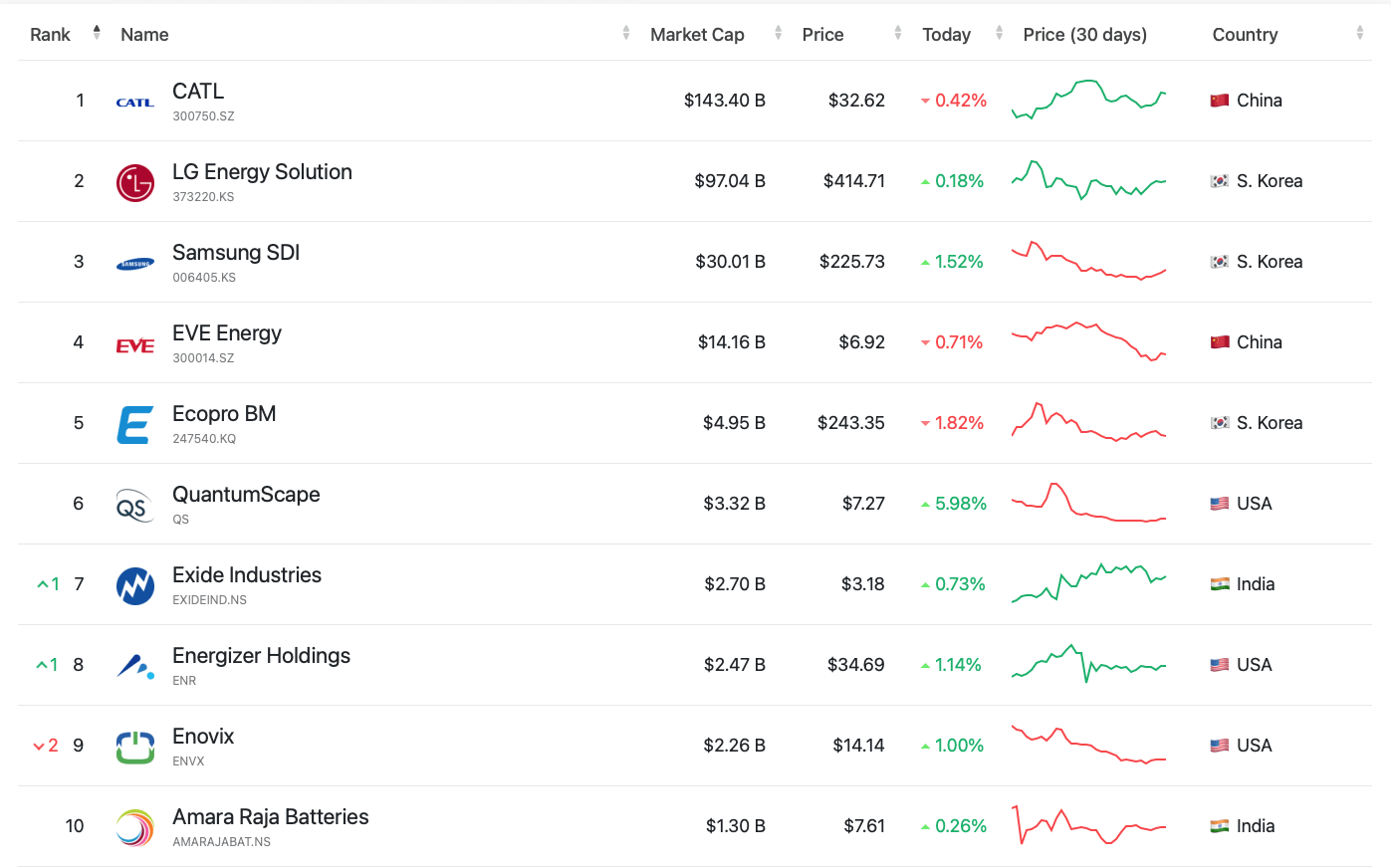

Below we can see a list of the largest publicly traded battery companies by market cap. CATL, LG, Samsung, and EVE essentially dominate this market.

Public Battery Manufacturers (Companies by Market Cap)

{kind=link}

Even in a scenario where Enovix develops a superior battery and is able to begin scaling it, who's to say that these other manufacturers won't integrate the technology into their own products? The other manufacturers would then have a scale advantage and technological parity, making Enovix's chances of justifying their current valuation slim. For those who believe that IP laws would stop this from happening you would be mistaken. Even if their competitors honored IP laws they would just reverse engineer Enovix's batteries and put their own spin on it to make their product "unique" and therefore avoid breaching IP protections.

The capital intensive nature of the battery industry means that scale wins. Enovix is currently staring up at a mountain that will be difficult to climb, especially when they are being attacked at every turn by far better capitalized and more experienced peers. Even if everything goes well for the company it's still unlikely that investors would see spectacular returns over the long-term due to the capital intensive nature of the industry limiting free cash flow to equity holders and by extension intrinsic value.

A perfect illustration of this limited upside is a comparison between Enovix and Canadian Solar ( CSIQ ). While yes, they are not in exactly the same industry, both the solar panel and battery industries operate with commodity economics. Canadian Solar is a North American based manufacturer of a commodity product and is not the dominant force in their market. This is what Enovix will realistically become in an optimistic scenario, which is why this comparison is being made.

We can see that Enovix currently has a larger market cap than Canadian Solar.

This is despite Canadian Solar having nearly $8 billion in TTM revenue compared to Enovix being essentially pre-revenue.

Enovix is lighting cash on fire and needs to continue spending to ramp production, while Canadian Solar is highly profitable.

Lastly, Canadian Solar is trading below book value while Enovix is trading at above 9x.

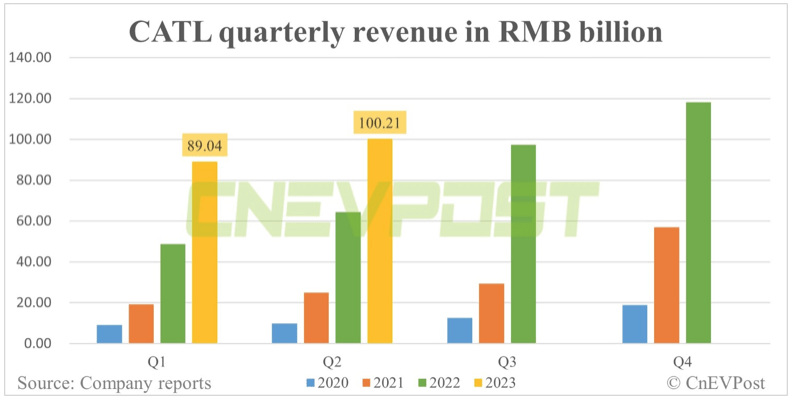

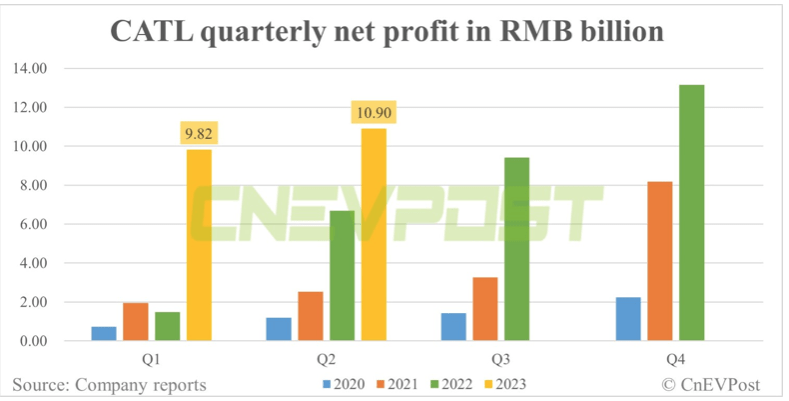

For a more direct comparison within the same industry we can look at CATL. CATL achieved revenue of RMB $100.21 billion ($14 billion) in the second quarter of 2023. This represents a 55.87% increase from the same period last year and a 12.54% increase from the first quarter. Refer back to the market cap of CATL that we looked at earlier: $143.40 billion. CATL is given a low multiple of roughly 2.5x sales when they are growing at a blistering clip on an already massive revenue base. CATL reported a net profit of RMB $10.9 billion in the second quarter, up 63.13% year-on-year and up 10.97% from the first quarter. This values CATL at a PE of around 24.

CATL quarterly revenue in RMB Billion (CnEVPost) CATL quarterly net profit in RMB Billion (CnEVPost)

{kind=link}

{kind=link}

CATL is operating at massive scale, growing like a weed, and is valued at just 2.5x sales and a PE of 24. Enovix is pre-revenue and is deeply unprofitable while they scale production. If Enovix ever presented a viable threat to CATL, wouldn't CATL just utilize the dynamics of commodity economics to crush Enovix before they could achieve scale? If CATL (or any other battery maker) would be unable to "copy" Enovix's design, they would instead just flood the market with supply at such a low price that Enovix would have to sell below cost to be competitive. Since many of these battery manufacturers are already profitable and at scale they can afford the margin hit, while Enovix cannot.

The easiest battery markets for Enovix to enter are the phone and IOT/wearables markets. These are some of the lowest margin segments of the battery industry. Samsung and others would likely use aggressive pricing tactics in order to make sure that Enovix could never truly gain a foothold. For those who claim that they would gladly pay an extra $100 for a battery that lasts longer, this is not the majority of phone/IOT/wearables users, especially ex-North America and Europe. Batteries are a volume business, and even in a scenario where a phone manufacturer uses Enovix's batteries the margins would be razor thin because Enovix has zero leverage.

All the optimism about "production ramping" misses the point that batteries (especially in the phone and IOT markets) aren't particularly profitable and there are gigantic competitors that would seek to crush Enovix if they ever became a threat. In a capital intensive, highly competitive, and thin margin industry many lions get killed when they are merely cubs, before they have a chance to grow big enough to fight back. Even in a bullish scenario where everything goes right think about the reality of the battery industry: capital intensive, highly competitive, and thin margins. These are not traits that investors generally gravitate towards and it seems highly unlikely that Enovix can justify their current valuation given the reality of the situation.

Risk Factors

A risk to the bearish case for Enovix is if the company can gain advance contracts and funding from device manufacturers such as Apple. This would help them build capacity and ensure that there would be an end buyer of that capacity at an economically viable price. Enovix could also get acquired by one of the large battery companies for their technology. Either of these events would weaken the bear case.

We view the risk/reward as being very unattractive. We can envision a scenario where the company is able to justify their current valuation but don't think it's likely. Short-term traders could make money off of the volatility, but long-term investors would be better off staying on the sidelines and seeing how this develops.

Key Takeaway

The valuation of Enovix appears to be pricing in far too optimistic of a scenario. Even if everything goes smoothly the economics of the battery industry limit the potential for profitability. The likeliest scenario is that Enovix gets crushed by competition. At best the company will be stuck in a low margin, high capital intensity, and fiercely competitive industry where they lack the scale of their peers.

For further details see:

Enovix: A Dangerous Game