TER - Enphase Energy Could Have A Long Runway Of Future Growth Ahead

2023-04-14 09:00:00 ET

Summary

- Enphase is a profitable growth company that could become a great investment if you have a long-term approach.

- Enphase has a 41.81% gross profit margin, grew its top line by 68.61% to $2.33 billion in 2023, and drove 17.05% of every dollar to the bottom line.

- Renewables have a long runway of growth ahead of them and will continue to increase their position in the global energy mix which will provide tailwinds for Enphase.

I have been hearing more and more about Enphase Energy (ENPH) over the previous months. While I have focused on traditional energy companies in the oil & gas industry, that doesn't mean I don't recognize the opportunity in renewable energy companies. The reality is that oil and gas will continue to play a significant role in the global energy mix for decades to come. Just because many industries will still rely on hydrocarbons, that doesn't mean tremendous growth won't occur in the renewable energy sector. I have done a significant amount of research which includes reading the International Energy Agency (IEA) World Energy Outlook, the U.S. Energy Information Administration Annual Energy Outlooks, and the Statistical Review of World Energy from BP p.l.c. (BP). Instead of picking a winner in the solar panel or wind turbine space, I would rather invest in the company that is making the internal components and advancing the space.

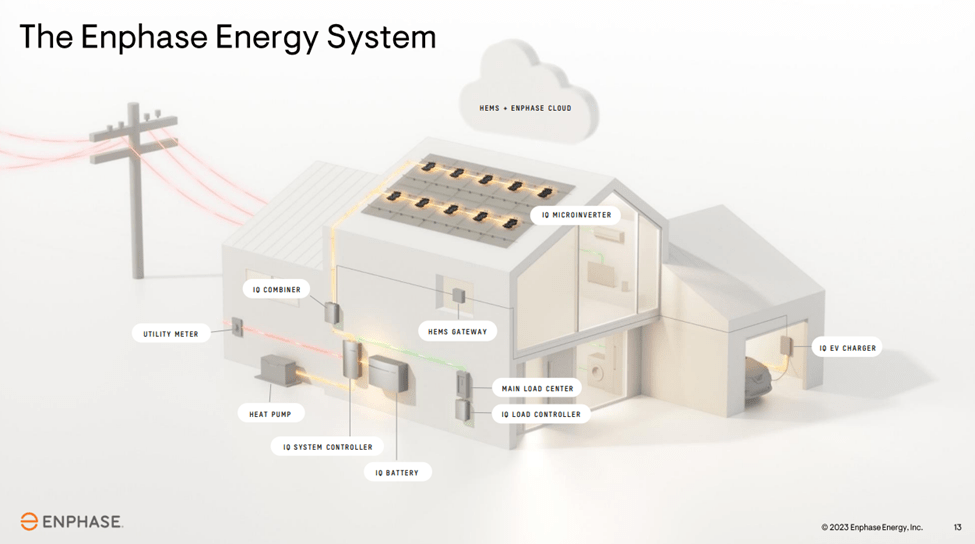

ENPH designs, develops, manufactures, and sells home energy solutions that manage energy generation, energy storage and control and communications on one platform. ENPH had advanced the solar industry as a whole by pioneering a semiconductor-based microinverter that converts energy at the individual solar module level. ENPH is developing into a renewable juggernaut as it generated over $2 billion in revenue throughout 2022, has turned a profit annually since 2019, and is increasing its free cash flow ((FCF)) growth rate. While the valuation may look a bit rich today, I feel it's justifiable due to the combination of growth rates in profitability and decades-long tailwinds from worldwide growth in renewables. I think ENPH could present a strong opportunity for long-term investors.

{kind=link}

What Enphase Energy does, and why I like their business from a numbers perspective

ENPH is a full 360-degree renewable energy company that develops, manufactures, and sells home energy solutions and provides the software to manage the system on a single platform. Unlike other companies, ENPH has taken a systems-based approach to solar technology by pioneering a semiconductor-based microinverter that converts energy at the individual solar module level. ENPH has shipped approximately 58 million microinverters, and over 3.0 million Enphase residential and commercial systems have been deployed in more than 145 countries. The system has an integrated approach to energy solutions that maximizes a home's energy potential while providing advanced monitoring and remote maintenance capabilities.

{kind=link}

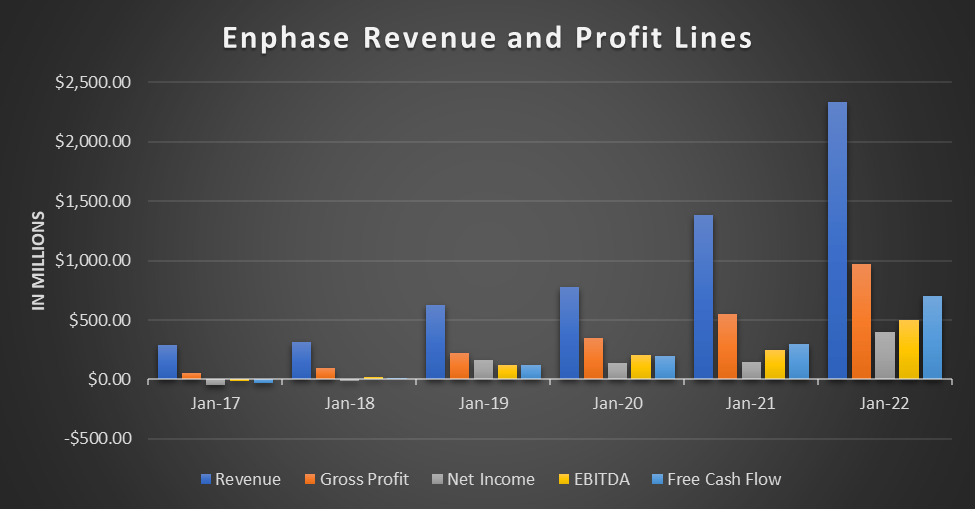

After looking through the financials, I am becoming a real fan of ENPH. This is a company that is generating solid revenue, and profits, with exceptional growth and impressive margins. In the 2022 fiscal year, ENPH generated $2.33 billion in revenue, $698.4 million in FCF, and $397 million in net income. Below is a chart showing the growth over the previous five fiscal years.

{kind=link}

Here is what I like about ENPH, it's not sacrificing profits for growth, and its growth is occurring at a rapid pace. Over the past five years, ENPH has increased its revenue by 714.43% ($2.04 billion) from $286.2 million at the close of 2017 to $2.33 billion at the close of 2022. Their revenue has grown at an average annual rate of 142.89%. This is something that people often forget, it's much harder to sustain elevated growth rates when companies get larger in size. If you look at the revenue growth in 2021 and 2022, it's remarkable. In 2021, ENPH generated 78.46% ($607.6 million) in YoY revenue growth. In 2022, ENPH generated YoY revenue growth of 68.66%, and while growth declined a bit, they added an additional $341.3 million in revenue compared to the dollar amount added in 2021. I fully expect revenue to decline on a percentage basis at a certain point. The key here is that while revenue is slightly declining on a percentage basis, their growth is growing on a dollar basis YoY. In 2021, ENPH added $607.6 million YoY, generating $1.38 billion in revenue then in 2022, they added $948.90 million, generating $2.33 billion in revenue, which is an additional 56.17% ($341.30 million) in YoY revenue growth.

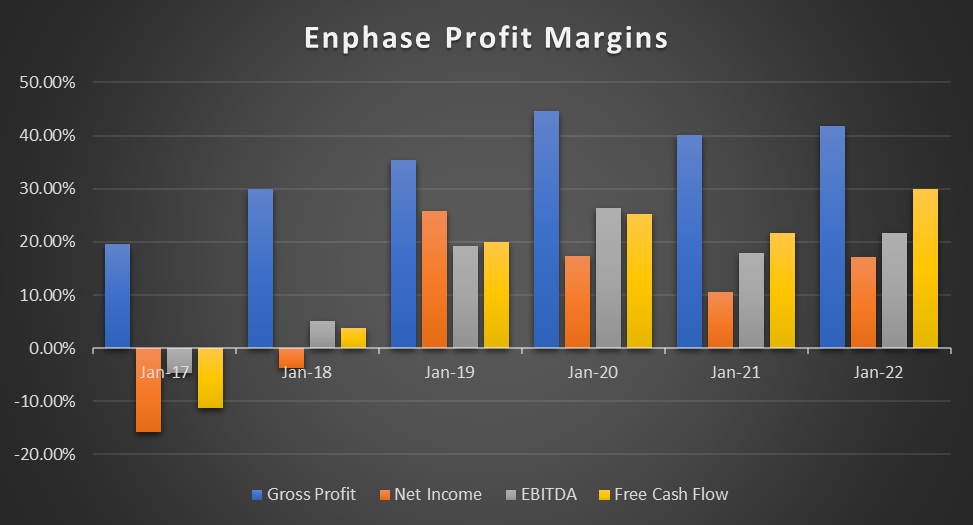

Unlike many of the unprofitable tech companies, ENPH has had no trouble turning a profit. Its gross profit has increased by 1,640.36%, adding $918.60 million over the past five years. In 2022, ENPH generated $974.6 million in gross profit, placing their gross profit margin at 41.81% above Mr. Buffett's 40% threshold for having a moat around their business. ENPH has grown its EBITDA by $517.20 million over the past five years, which means out of every dollar in revenue generated, they are driving 21.61% to its EBITDA line. ENPH delivered $698.4 million of FCF, placing their FCF yield at 29.96%, which is a strong metric as almost 1/3rd of revenue drops down to FCF. After all the taxes are paid, and interest expenses are accrued, ENPH has been GAAP profitable for the previous four years and, in 2022, delivered $397.40 million of net income to their bottom line. This placed their profit margin at 17.05%. This is also a strong metric because ENPH increased its profit margin by 6.53% and generated an additional 173.31% ($252 million) in pure profit YoY.

{kind=link}

In addition to ENPH having strong growth metrics, it has a fortress of a balance sheet. In current assets, ENPH has $1.61 billion of liquidity on hand, consisting of $473.2 million in cash and $1.13 billion in short-term investments. On the liabilities side, ENPH has $1.2 billion in long-term debt, of which $90.9 million is due in 2023. ENPH has enough cash to not only eliminate 100% of its long-term debt but it can also eliminate 100% of its total debt on the balance sheet, which sits at $1.31 billion. I also look at the debt-to-EBITDA ratio because banks often include a certain debt/EBITDA target in the covenants for business loans, and it helps show me an important leverage ratio. ENPH has a total debt-to-EBITDA ratio of 2.61x which is excellent, in my opinion, as ENPH should have no problem servicing its debt obligations without touching its cash on hand.

Where the renewable sector is heading and why ENPH will benefit

ENPH has a tremendous runway of growth as renewables will outpace every other source of energy over the next three decades as it becomes a larger part of the global energy mix. While oil and gas aren't disappearing and will remain important components of the global energy mix, nobody can deny that renewables will continue to increase their relevance on the global stage when it comes to fueling energy consumption.

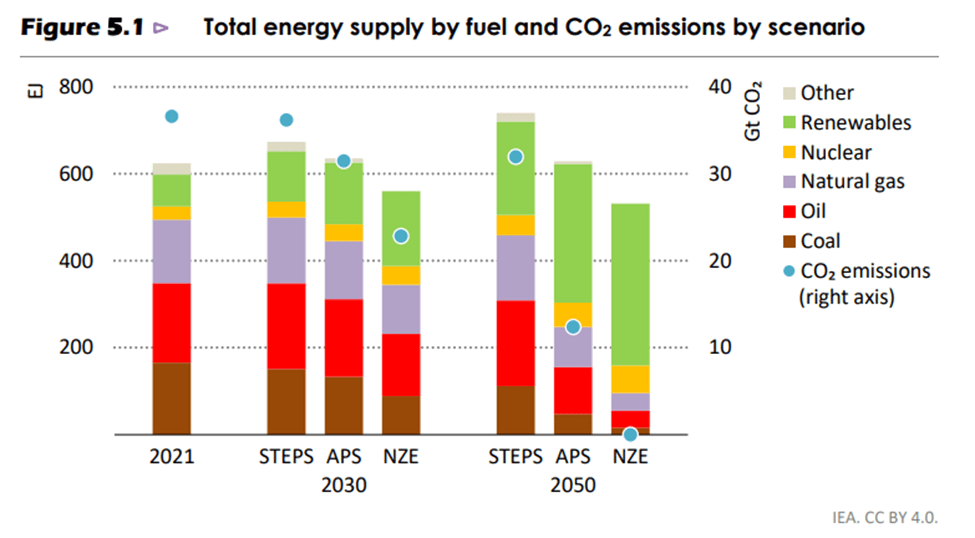

There are several reports I look at to formulate my opinion about where the global energy mix will be in 2050. I don't take a biased approach, and I go by the information government agencies and oil supermajors provide. The IEA released its revised version of the World Energy Outlook 2022 in November of 2022. The IEA has 31 member countries and 11 association countries that examine a full spectrum of energy issues, including oil, gas and coal supply and demand, renewable energy technologies, electricity markets, and energy efficiency. In its stated policies scenario, which is their baseline, renewable energy expands quicker than any source of energy through 2050. Based on the graph below, in the baseline scenario, renewables will triple their position in the global energy mix in 2050, compared to where they were in 2030, and in the net zero emission scenario they increase their position by 5-6x.

{kind=link}

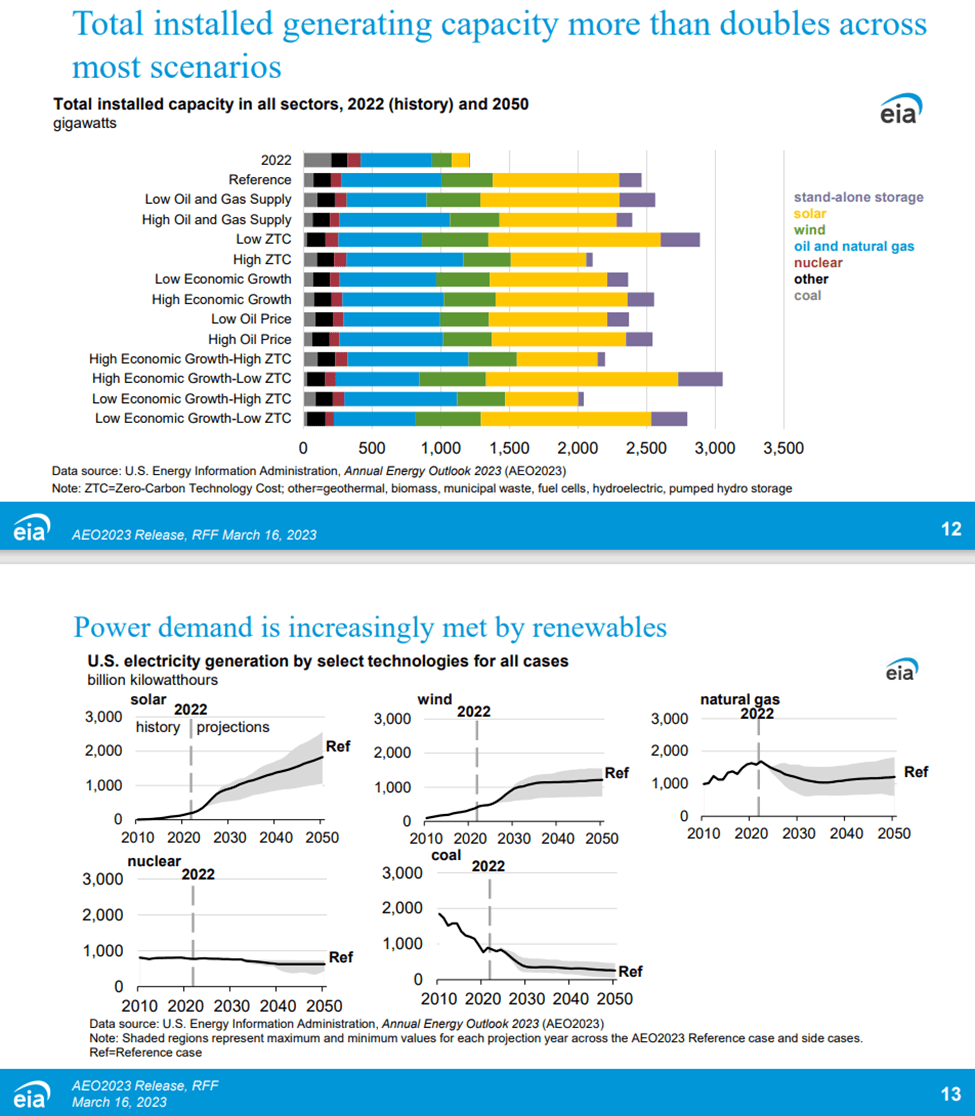

In the EIA Annual Energy Outlook 2023, which looks at the domestic energy landscape, they have renewables, specifically solar, benefiting a great deal. Solar, in just the reference case, will increase by roughly 5x in its installed generating capacity by 2050. In its most aggressive scenario, solar increases by roughly 7-8x its generating capacity by 2050. Looking at solar's share of the U.S. electricity generation, it will increase by roughly 9x through 2050. In all cases, solar increases the most in installed capacity over the next three decades.

{kind=link}

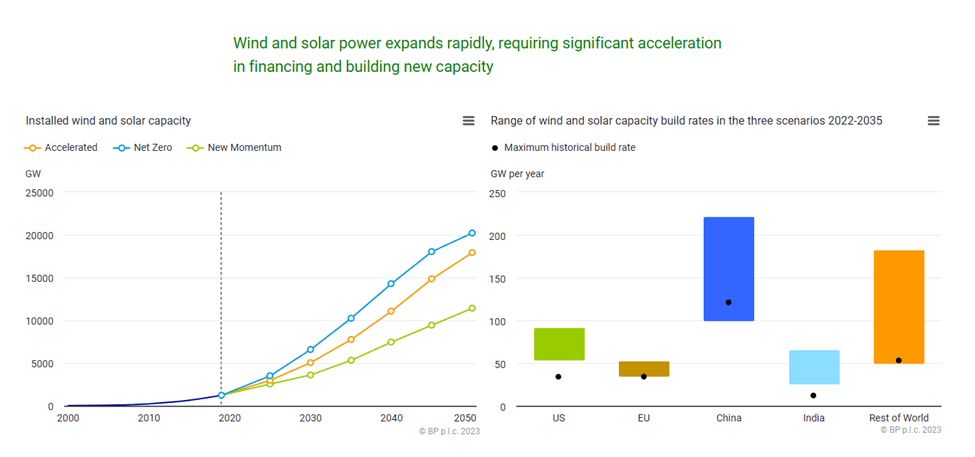

BP provides some of the most in-depth independent research in the energy industry. In their 2023 Energy Outlook, BP has installed wind and solar capacity increasing by 827.70% from 1,231 GW in 2019 to 11,420 GW in 2050. In an accelerated adoption case, this increases to 17,936 GW.

{kind=link}

No matter how you look at the data, oil and gas will still play a significant role in the global energy mix in 2050, but the most growth will come from renewables. Solar will see the largest growth by the projections I have read, and it will provide a huge runway of growth for companies focused specifically on renewable energy. ENPH is in a great position to capitalize on the inevitable as solar continues to become a larger piece of the global energy mix each year for decades to come.

The current valuation may be a bit rich but the growth rates could make the price justifiable

I am big on paying a great price for a company so I wanted to see how ENPH is valued compared to its peers, which Seeking Alpha lists as:

• SolarEdge Technologies ( SEDG )

• Teradyne ( TER )

• Entegris Inc ( ENTG )

• Amkor Technology ( AMKR )

• MKS Instruments ( MKSI )

There isn't a one size fits all approach to valuing companies, and different metrics are more important to different investors. My preference is to base my valuation model on FCF as the profitability measure because, unlike net income, it can't be manipulated through write-offs, write-downs, and other GAAP accounting practices. FCF is simply deducting capital expenditures from the cash generated from operating activities. How much cash a company generates from its operations is much harder to manipulate than net income because $1 of cash from ops should always equal $1 of cash from ops. To determine what I believe the fair market value is, I start with the total equity of a company. Total equity is simply total assets minus total liabilities. This is my baseline because if a company was to dissolve itself, theoretically, the total equity is what would be left for the shareholders to chop up among themselves after all liabilities are zeroed out. After the baseline for total equity is established, I look toward profitability. I can't predict what companies will do in the future, so I take the average price to FCF multiple that the largest companies in the market trade at, then assign that multiple to each company's FCF and add that figure to its total equity. This gives me a baseline valuation because I am taking the equity of the company and an average multiple on profits to determine its value. Then I look at the company's market cap and see if it's currently trading at a discount or premium to what Mr. Market has determined.

{kind=link}

ENPH has a market cap of $26.96 billion which is the largest in its peer group, and it trades at a 38.61x multiple on its FCF. I actually don't mind the multiple due to its growth in profitability. There are two companies, SEDG and ENTG, which I have excluded from my valuation model because they generate negative FCF. ENPH, TER, AMKR, and MKSI trade at an average price to FCF (P/FCF) of 26.51x. If I multiply each of these companies 2022 FCF by the 26.51x multiple and add the equity on the balance sheet to find what I would consider a fair market value, TER, AMKR, and MKSI trade at a discount and ENPH trades at a premium. I also added P/E, and the P/E range is 10.86 to 35.32, with ENPH trading at the high end with the 35.32 P/E.

Yes, ENPH trades at a higher P/FCF multiple and a higher P/E ratio than its peers, but I could argue that the premium is warranted due to its growth not just in revenue but profitability. Their P/FCF isn't egregious, and this is a multiple that could significantly improve going forward. I am actually going to do some research on TER and MKSI, as they look very interesting. As far as ENPH, the valuation could be looked at as a bit rich today, but this is a company that is in a sector that is projected to explode with growth, and ENPH has demonstrated that it can capitalize on the trend.

Here is the real question I am asking myself right now, hypothetically, could ENPH get to $2 billion of annual FCF by 2030? ENPH grew its FCF by $398.70 million (133.03%) YoY to $698.4 million. If ENPH was to grow its FCF by $250 million YoY for the next seven years, it would add $1.75 billion of annual FCF, placing its 2029 FCF 2029 at $2.45 billion. Based on my methodology, this would place my fair market value at $65.72 billion for ENPH, which would indicate there is 143.73% upside which is an average annual return of 20.53%. Please remember this is hypothetical, and I don't have a crystal ball, ENPH could grow their business significantly more or they may underperform my estimates. It is also entirely possible that ENPH finishes 2029, generating $4 billion in FCF, which would place its fair market value at $106.87 billion based on my methodology. This would mean that there is 296.31% upside and an average annual rate of return of 42.33%. While the current valuation is higher than its peers, it may be for a good reason, and based on its current trends, ENPH could certainly generate some handsome returns for long-term investors.

Conclusion

If you have read some of my other articles where I have gone through valuations, you may be shocked at what I am about to say. If you're looking at ENPH as a long-term investment, out to 2030, I think it's a buy all day, and if it happens to decline to around $150, it would be an opportunity to dollar cost average. ENPH has great top-line growth, strong profitability, strong margins, and a great balance sheet. ENPH isn't sacrificing growth for profits and is driving 17.05% of each dollar to the bottom line while having a 29.96% FCF yield. If ENPH was in a different sector, I probably would be saying it's overvalued, but there is no question that the growth in renewables should provide excellent tailwinds for ENPH over the next several decades. I am not an investor in ENPH, but after doing my due diligence, I think there is a strong opportunity in ENPH, and I plan on starting a position in the coming weeks.

For further details see:

Enphase Energy Could Have A Long Runway Of Future Growth Ahead