ENPH - Enphase: Short-Term Pain With Long-Term Resiliency

2023-05-02 09:34:06 ET

Summary

- ENPH management guided flat sequential revenue growth, might be time to value company on fundamentals over growth.

- NEM 3.0 may cause challenges in microinverter sales but benefit battery sales in California.

- High valuation isn't supported by the macroeconomic landscape. We may see further pressure on the share price.

Enphase ( ENPH ) develops and sells an all-in-one solution for the generation, utilization, and storage of solar power. Through their capital-light business model, Enphase has been able to achieve a 30% free cashflow flowthrough while growing the topline by nearly 70% for FY22. Through the end of FY22, I would say Enphase has been a no-brainer success story. Despite their recent success, ENPH is valued at an extraordinary premium with a company value of 49x FY22 EBITDA. Despite their large free cashflow flowthrough, FCF only yields 3%. Though ENPH isn’t valued as a “value” play and more of a growth story, I believe the economics are changing that may bring ENPH shares back to Earth where valuations do matter. ENPH shares have already experienced a -26% drop in price, wiping out nearly $9b in marketcap, in response to the suggestion of softening demand for their microinverters. Despite Enphase having all of the qualities I like in a company: strong growth, margin expansion, and free cashflow growth, I don’t believe the global macroeconomic environment we’re gearing towards in 2H23 is suitable for this high valuation and on this basis, I provide ENPH with a sell rating (just for clarification, I do believe ENPH can be suitable in a portfolio at a better valuation).

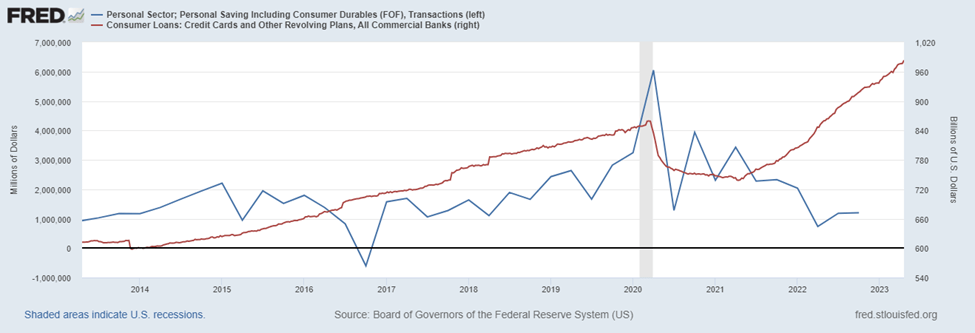

Though Enphase has seen a lot of success in recent years, there are some challenges on the horizon that the solar industry will face that may hinder growth and performance. To state the obvious, there is a global recession looming and the state of the consumer is weakening as spending slows and credit usage rises.

{kind=link}

According to NerdWallet, a solar system installation can range between $16,870-23,170 with an APR as low as 7.74% up to 35.99%, assuming a baseline of 720 credit. According to CNBC, the average American has just over $5,000 in savings. Average amount of money Americans saved in 2022 (cnbc.com) With this assumption along with the growing popularity of capping net metering, new solar implementations may not be the consumer’s top priority for FY23.

There are also rising challenges with NEM 3.0 coming out in California along with other government incentive programs being cut in Europe, potentially disincentivizing consumers from investing in solar panels. Though this may seem harmful to the consumer, it may benefit Enphase by incentivizing consumers to invest in battery storage technology.

The recently released IRA may also create some unintended consequences with the requirement of sourcing materials domestically. Though there doesn’t appear to be any language directed towards home battery systems, batteries intended for electric vehicles must contain 40% of domestically sourced mineral content in order for consumers to receive incentives. Though Enphase currently exclusively sources batteries from China, they are currently in the process of expanding their manufacturing footprint (contract manufacturing) domestically. Whether or not batteries are a part of this expansion is a challenge that may need to be addressed if the IRA were to create a hinderance on consumer incentives. Nonetheless, the IRA will provide a 30% tax credit to consumers buying the solar power ecosystem, including storage, microgrid controllers, fuel cells, and heat pumps throughout the next 10 years.

Despite these domestic challenges, there is still a large market that Enphase is currently addressing in developing countries that don’t necessarily have reliable power grids. Other challenges that may benefit Enphase is the current geopolitical tension and the suppression of natural gas exports (higher natural gas prices can make PVs appear more appealing). Though the US has done a good job at picking up the slack for transporting LNG across Europe and APAC, there may be continued stress on gas prices in the future, leading to sourcing challenges, higher prices, and potential outages. Please read my report on AGX for a deeper discussion on power transmission and utilization .

Value Proposition

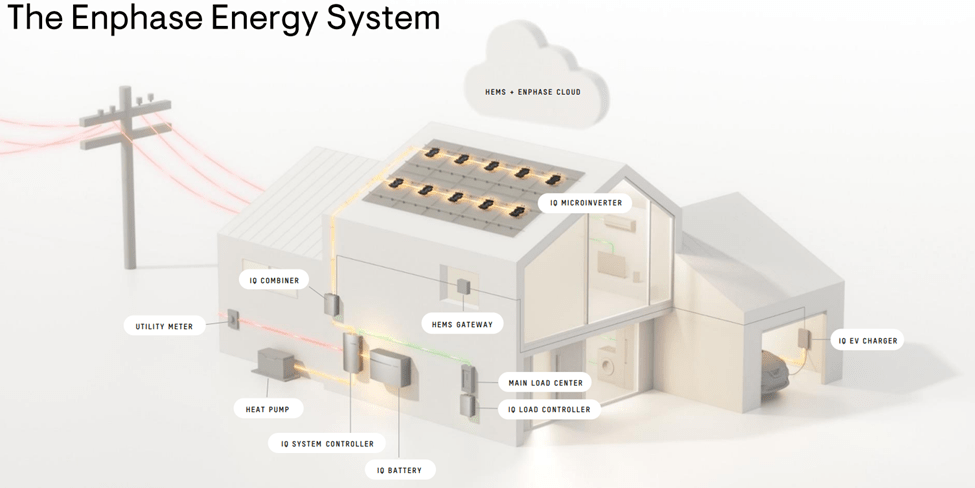

Enphase has also made it easier for the consumer to purchase their suite of products by creating a complete solar installation and management ecosystem from generating design proposals, sourcing financing, permitting, installation, and monitoring through their cloud-based application. Though this may seem rudimentary, Enphase has successfully streamlined the process and positioned itself as the go-to source for solar installation and power management.

Enphase’s greatest strength is their ability to control the entire home ecosystem through their hardware and cloud-based software. With their latest release of IQ8, a home can essentially run autonomously without being connected to the grid. Their technology also allows the homeowner to control how and where the electricity is distributed throughout the home, allowing the homeowner to preserve power during grid outages.

{kind=link}

Enphase has been very strategic in their acquisition targets. Their most recent acquisition of GreenCom completed the ecosystem for connectivity of devices and power monitoring. This acquisition will allow Enphase customers to selectively distribute power throughout their home, a benefit that’s most visible during natural disasters or intermittent power generation.

{kind=link}

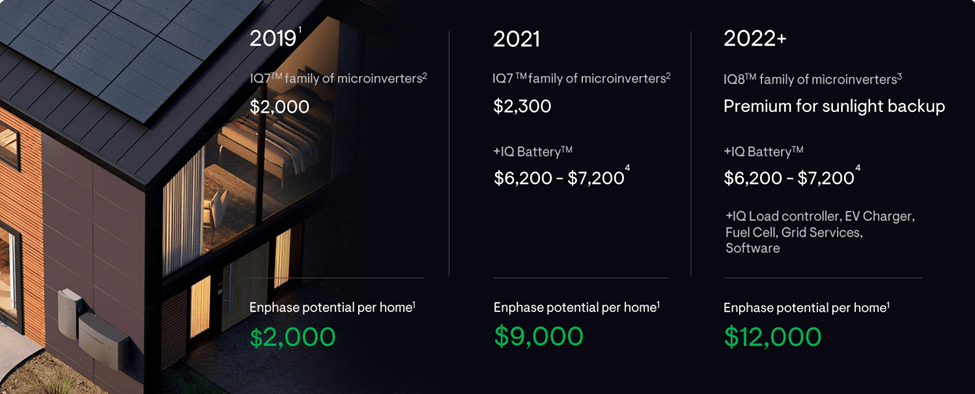

Though Enphase doesn’t exactly break out exact sales figures, they do break out general incremental numbers. Holding constant their numbers, we can expect the microinverter to generate $2,000 per sale, the IQ Battery to generate $7,000, and the rest of the ensemble to produce ~$7,000 in additional revenue.

{kind=link}

Despite the high economies of scale potential the solar industry can experience, there are some very real challenges faced in the industry. NEM 3.0 was voted on in California on December 2022 and implemented mid-April 2023, resulting in the reduction of compensation for selling energy to the grid from $0.25-0.35 down to $0.05-0.08 and increasing the breakeven timeframe from 5-6 years to roughly 10 years. This may have varying effects on sales between microinverters and batteries. Existing customers will be more likely to buy Enphase’s power storage systems and new potential customers may be more hesitant to buy microinverters.

{kind=link}

Financials & Valuation

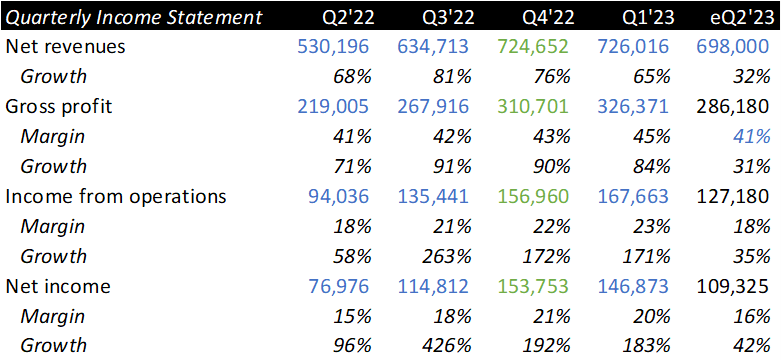

Q1’23 continued to hold strong for Enphase for both top- and bottom-line growth while bringing margins back to 2020 levels. Despite this quarter’s success, management had some lackluster guidance for q2’23, with revenue coming in anywhere between $700-750mm for a baseline of 32% growth.

{kind=link}

Assuming growth remains relatively flat throughout FY23 and a slower taper for 2H23, we can expect revenue to ballpark 24-30% and a slight pull on margins as we work down the income statement. I’m expecting net margin to contract to 15%, below their FY22 margin of 17%. In this instance, maintaining the same 48x earnings multiple, ENPH shares should be priced at $145/share, assuming a 1% growth rate in the float. Despite this lower price, ENPH is a growth tech company and I believe the preferred multiple will be price to sales. Using the average of ENPH peers of 4.34x, a more appropriate share price will be $85.66/share.

SeekingAlpha

Despite these notes, ENPH is one of the few companies in the industry that is profitable and generates free cash flow, deeming the stock worthy of a higher multiple than its peers. Though from a value perspective ENPH is still priced to perfection, their capital-light business model may prove beneficial through a downturn. Though solar power generation is a lot less efficient than traditional sources, ENPH isn’t in the business of selling electricity. As long as there’s a consumer demand for PV and off-the-grid connectivity, Enphase should continue to succeed in growing their business and breaking into new markets. The rationale behind my sell position depends almost entirely on the macro environment and the resiliency of consumer spending; otherwise, I believe Enphase is a strong candidate for a long-term long position.

For further details see:

Enphase: Short-Term Pain With Long-Term Resiliency