CA - Ensign Energy: Another Canadian Oilfield Services Idea

2023-12-06 07:23:21 ET

Summary

- Ensign Energy is set to benefit from the upcoming increase in Canadian oilfield activity, which is in turn driven by the greater offtake capacity coming in 2024.

- The valuation multiples leave considerable safety margin while the street targets imply considerable upside.

- The debt maturities have been pushed out to 2026.

- The upside is 50% based on the most conservative broker covering the stock.

Note: Ensign Energy is a Canadian company; the article distinguishes between Canadian dollars (C$) and US dollars (US$).

Investment thesis

Ensign Energy Services ( ESI:CA ) is an undervalued land drilling contractor that is set to benefit from upcoming activity strength in Canada. My Ensign thesis is similar to the one I laid out recently for its Canadian peer Precision Drilling ( PDS ):

Pr ecision Drilling : Bullish On Canadian Oilfield Service Stock Going Into 2024

The major difference is perhaps that Ensign is more levered than Precision which makes it more risky but also offers greater upside. I am also bullish on Nabors ( NBR ), which isn't present in Canada any longer, but has strong positions internationally.

Together with Helmerich & Payne ( HP ) and Patterson-UTI Energy ( PTEN ), Ensign, Precision and Nabors are the largest providers of land drilling services in the US and Canada and control a majority of the so-called super-spec or premium rigs that are currently in high demand.

The entire peer group has been beaten down lately, but this is particularly true of Ensign which is close to its 52-week lows:

While the sell-off coincided with the latest drop in oil prices, Ensign can thrive with $70 oil, or perhaps even less. International activity remains strong, Canada's oil industry is about to get a major expansion of its offtake capacity, and, even in the US where public shale companies are cautious about capex, premium rigs remain in high demand.

The cheap valuation multiples, which provide safety margin, and the bullish targets from professional street analysts suggest that this recent drop may be a buying opportunity.

The drilling outlook isn't bad

I have already harped on this in a couple of my recent articles, but I will repeat here too that the disappointing (from a services provider's perspective) US rig counts that have been sliding down for most of the year don't show the full picture:

- Canadian rig counts aren't falling and Canada is actually preparing for a record surge in oilfield services activity in 2024 Q1;

- Outside of North America, rig counts are also flat or increasing;

- Within the US, the evolving technical needs of US oil & gas operators ( XOP ) who keep drilling longer lateral wells to improve their own efficiencies also drive a preference for "super-spec" rigs; this gives the advantage to larger players like Ensign.

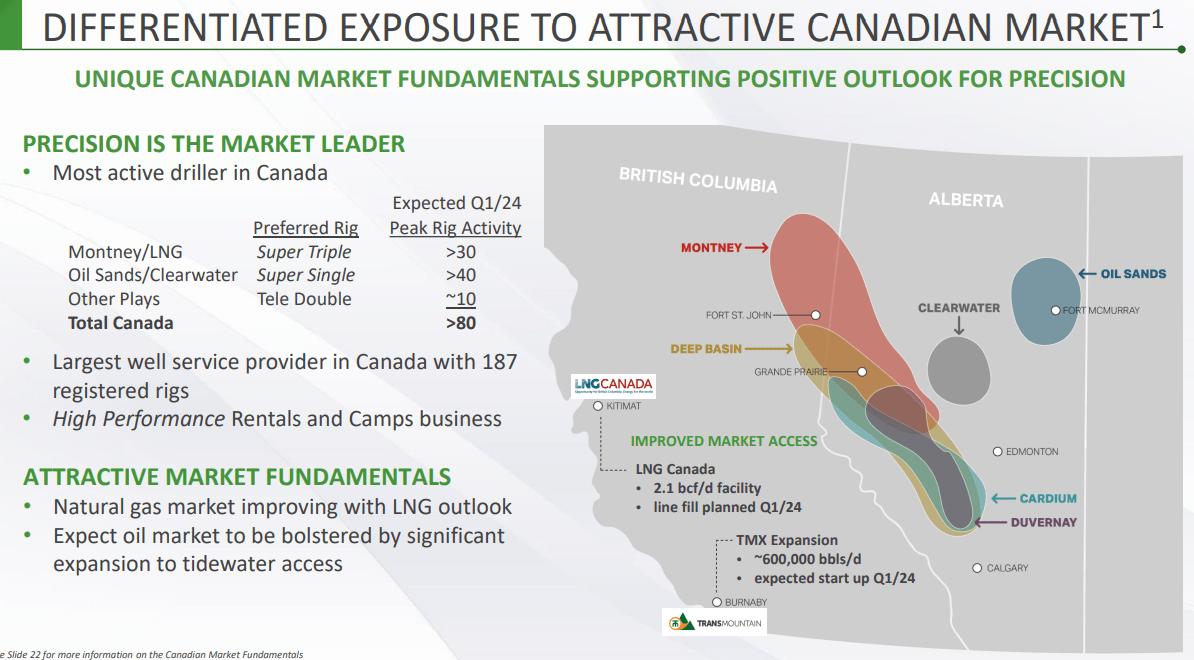

I like this slide from Precision which illustrates nicely the Canadian dynamics:

Precision Drilling Presentation

{kind=link}

A big event in Canada is the TMX pipeline expansion which will increase its capacity from 300,000 to 890,000 bpd. Given Canada produces give or take 5 million bpd which exceeds the capacity of existing pipelines, adding another half a million is a big deal and will make marketable oil that is now limited by expensive railway transportation to the US Gulf Coast.

Canada's offtake issues drive a big discount for Canadian oil relative to WTI that can easily get above $20 per barrel. As Canada's market access improves, the realizations for Canadian oil may even go up even as WTI declines if the differential shrinks enough. This, in turn, explains why Canadian E&Ps are planning to increase their investment in production in 2024.

In the words of STEP Energy ( STEP:CA ), a Canadian provider of completion services (the completion work comes after the drilling, but the demand drivers are basically the same):

STEP will use the moderating of activity in Q4 2023 to complete more intensive maintenance on equipment to prepare it for the extremely intensive utilization anticipated for Q1 2024 ... Activity in 2024 is expected to increase, with multiple clients signaling that their 2024 capital budgets will be higher than 2023 . The discipline in global oil markets and anticipated completion of the Trans Mountain pipeline project and the Coastal Gas Link pipeline/LNG Canada projects are creating an opportunity for Canada to materially increase production in 2024.

The Coast Gas Link project mentioned by STEP is an additional tailwind as it will provide greater market access for Canada's natural gas through the forthcoming Shell ( SHEL ) LNG Canada export facility; that is a bit further down the road than TMX though.

Ensign Energy is well positioned in Canada:

{kind=link}

As its other large peers, Ensign is not limited to North America either. The company also has rigs internationally in Australia, the Middle East, Argentina and Venezuela. International capex has been holding up much better because it is driven by long-cycle projects and much of it is funded by national oil companies.

A recent presentation by oilfield services research firm Spears & Associates me ntioned they expect 9% capex growth internationally and 5% for Canada in 2024.

Lastly, even in the US not all rigs are equal. The annual rig census study from NOV Inc. ( NOV ) showed that even as active rigs in the US decreased , utilizations still went up as more idle rigs were retired. At the same time, the proportion of more powerful rigs keeps growing:

Author

Ensign Energy nicely fits into the changing requirements of the US market as more than 70% of its marketed rigs are the coveted high-spec rigs:

{kind=link}

In my view, in 2024 Ensign can at minimum hold its ground in the US while capturing the upside from Canada and internationally (perhaps Venezuela).

Highlights from the quarterly earnings

Ensign's quarterly report wasn't disappointing. Both revenue and EBIDTA are up year-on-year and 2022 Q3 was a strong benchmark:

Ensign Energy Quarterly Report

{kind=link}

About a week ago, the company also confirmed the redemption of its 2024 notes which completes for now its refinancing and extends maturities until 2026, with projected very manageable 8-9% interest cost.

During the earnings call management expressed some cautious optimism on Canada:

Analyst:

And lastly for me given we're getting optimistic comments from a number of the E&P companies about activity that they see for the second half of 2024 and then 2025 on the natural gas side because of LNG Canada and then potentially the announcement of a second train. Are you starting to see conversations about locking up more equipment in that Northwest, Alberta Northeast BC side?

Ensign CEO:

Yes, yes. We have. It started this summer notionally, and I think it's starting to pick up ever so slightly. It's -- once you get over 80% utilization in any rig category, things go a little crazy, all of a sudden everyone goes we should have started this conversation three months ago. But operators, have been a little spoiled with the ability to pick and choose over the last few years. I think that may change into 2024.

On the US outlook management commented:

With US production starting to come off, rig efficiency plateaued, DUCs at their lowest levels in a decade and with the onset of more Tier 2 inventory, this will certainly manifest itself into more rig demand moving forward. It's a nice construct for the future. We think that we will see a disciplined uptick in demand for our rigs and other services generally starting in early 2024, which will be followed with stronger pricing support manifesting in the back half of 2024.

Ensign's management's comments weren't as bullish as what we heard from Precision, but ultimately both companies are exposed to the same drivers.

Valuation and risks

Based on the analyst consensus estimates, Ensign is now trading at 3.4x EV to 2024 EBITDA and 5.1x price to 2024 earnings. This looks cheap considering EBITDA is forecasted to grow slightly through 2025 and debt isn't any longer an issue until 2026. The price to 2025 earnings ratio sits even lower at 3.7x; I think that leaves considerable "safety margin" for anyone who buys now.

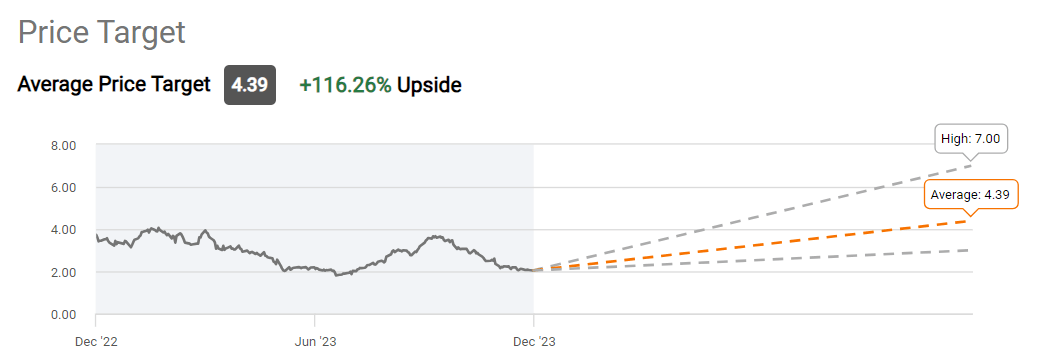

The average street target on Ensign is C$4.39 which implies 116% upside:

{kind=link}

One of the recent calls included in Seeking Alpha's average is a "hold" from Stifel. The Stifel report (behind paywall) assigns a C$3 PT based on a 3.5x EV multiple on estimated 2024 EBITDA. Stifel cautions on the debt load but is optimistic that U.S. rig count has likely bottomed and notes potential upside from rig adds in Venezuela. As Ensign has fallen further since this report was issued, it now has 50% upside even to Stifel's "hold" target.

Another broker included in the average is TD Cowen with "buy" call and C$4.75 PT which implies more than 100% upside. What I find interesting about the TD report (behind paywall) is that they arrive at their target based on a modest $70 price forecast for the WTI oil ( CL1:COM ) benchmark in 2024. In other words, the target isn't contingent on higher oil prices.

TD also assumes that the Canadian rig count will average 185 in 2024. As of last week , the metric stands at 192, so, again, this isn't an aggressive projection by any means. So the TD Cowen target should be seen more as due to Ensign repricing given its undervaluation than the industry conditions greatly improving - although I believe the latter will happen too.

In terms of risks, Ensign is a small-cap energy stock, so the volatility shouldn't surprise anyone. What I would rather like to flag though is the annoying thin daily volume on the US over-the-counter ticker ESVIF. So liquidity risk is very important to mind, especially if you don't trade directly the Toronto listing (use limit orders).

Takeaway

The US drilling rig market has likely bottomed and Canada is about to start a new year with robust oilfield services demand. As Ensign Energy is already profitable in the current environment, the compressed valuation provides quite a bit of safety margin even if things don't improve. That is why I see it as a limited downside / considerable upside asymmetric bet.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Ensign Energy: Another Canadian Oilfield Services Idea