CA - Enterprise Products Partners: It Still Makes Sense To Be Bullish

2023-11-02 12:02:23 ET

Summary

- Enterprise Products Partners' financial performance continues to be solid despite volatility in the market.

- The company's stock has performed well, with only a 0.5% downside compared to a 6.8% drop in the S&P 500 since last writing about it.

- Despite not being the cheapest option in the midstream/pipeline space, Enterprise Products Partners still offers upside potential for investors.

On October 31st, the management team at midstream/pipeline company Enterprise Products Partners ( EPD ) announced financial results covering the third quarter of its 2023 fiscal year. While the company did experience some weakness in some areas, its overall financial performance was positive compared to what management reported the same time last year. In the past, I have been bullish about the company. Even though I downgraded it back in early August from a ‘strong buy’ to a ‘buy’, that rating still reflects my view that shares should outperform the broader market for the foreseeable future. That assessment was based on how shares were priced and overall fundamental performance, particularly when it came to cash flows.

Since the publication of that article , the stock has continued to deliver as I anticipated. Shares have seen downside of only 0.5% after factoring in distributions. While not as good as upside, it does beat the 6.8% drop that the S&P 500 endured during the same window of time. The data released regarding the third quarter makes me feel even more confident in that assessment. Though shares of the company are not the cheapest in the space and it is not my favorite prospect, it does still seem to offer upside potential that investors would be wise to take into consideration.

Still a solid opportunity

The midstream/pipeline space is very peculiar and requires very domain specific knowledge in order to do well in from an investment perspective. There are certain aspects of the space, for instance, that are different from most anything else in the investing ecosystem. For instance, when you see a company with revenue that is significantly lower or higher than what it was one year earlier and that change in revenue is not attributable to asset sales or purchases, it can often be a sign of something big happening, either for better or for worse. But that is not the case in this market. What really matters is the spread between the resources that the companies in question deal with between the price paid and the price sold.

{kind=link}

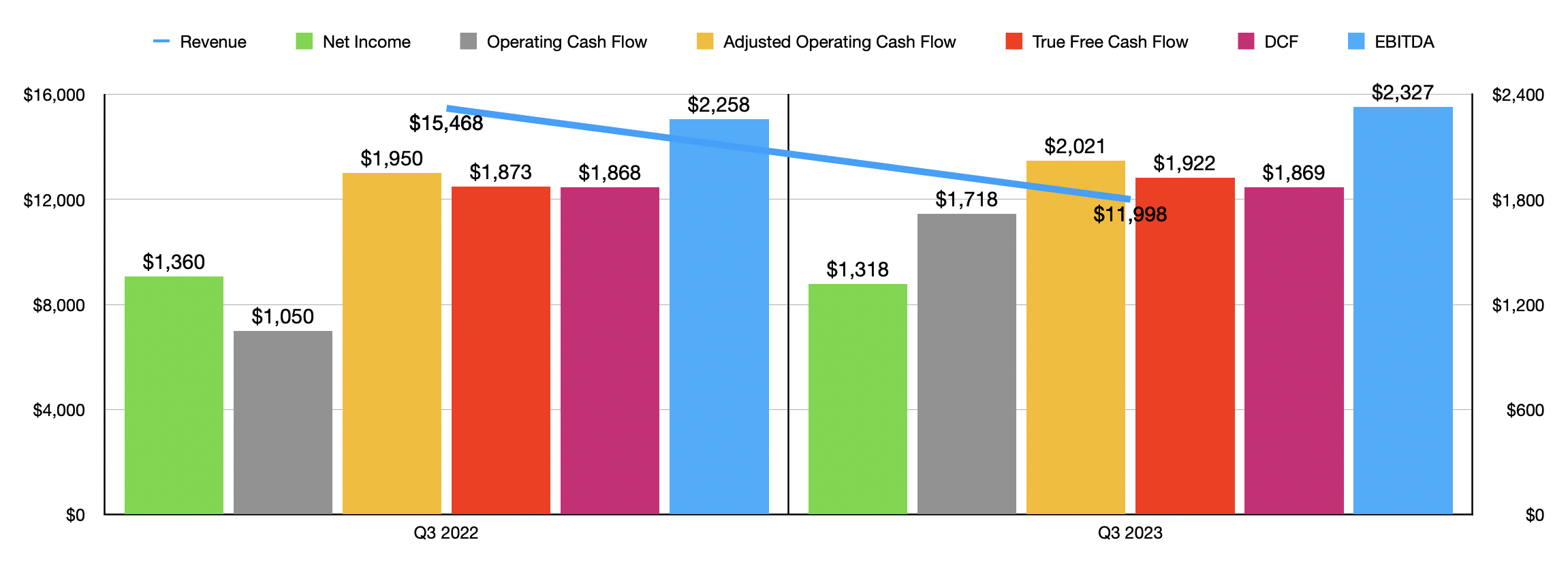

As an example, during the third quarter of the 2023 fiscal year, Enterprise Products Partners reported revenue of just under $12 billion. That is a substantial decline compared to the $15.47 billion in revenue generated the same time last year. But as you can see in the chart above, cash flows were not, in all but one instance, materially different from one year to the next. But before we get into the cash flow data, it would be helpful to touch some on the volumes of goods transported.

{kind=link}

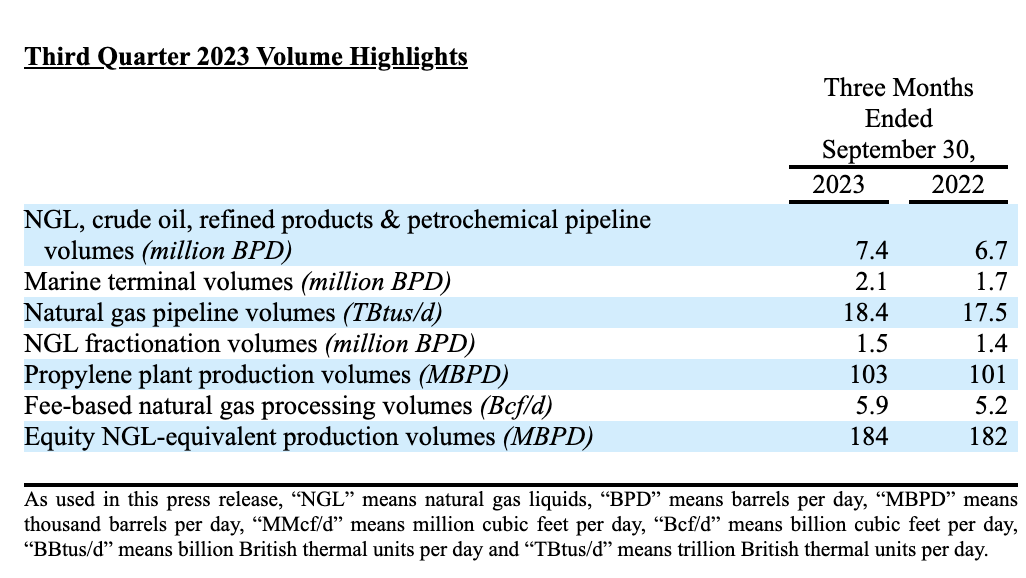

The company has a vast network of pipelines and other assets that it transports natural resources through. For instance, in its NGL, crude oil, refined products, and petrochemical pipelines, it transported an average of 7.4 million barrels per day during the quarter. That's up nicely from the 6.7 million barrels per day reported one year earlier. The company also saw volumes at its marine terminals average 2.1 million barrels per day. That's up from the 1.7 million barrels per day reported the same time last year. Year over year, natural gas pipeline volumes grew by 5.1%, while NGL fractionation volumes managed to climb by 7.1%. The company saw propylene plant production volumes grow from 101,000 barrels per day to 103,000 barrels per day, while fee-based natural gas processing volumes jumped 13.5% from 5.2 Bcf per day to 5.9 Bcf per day. And lastly, equity NGL-equivalent production volumes grew by two million barrels per day from 182,000 to 184,000.

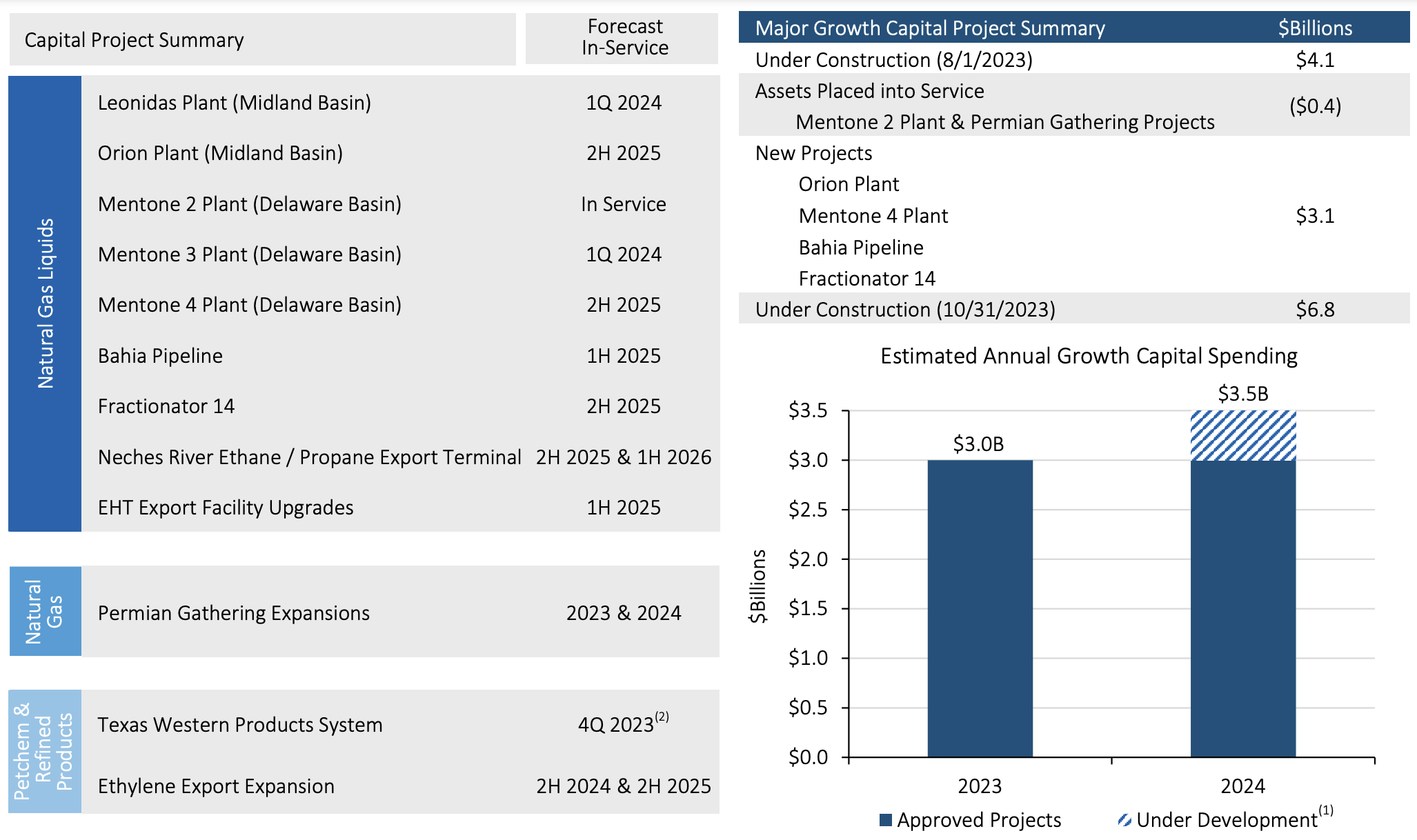

Strong demand for the company's services was instrumental in seeing this kind of growth. But growth would not have been possible had it not been for significant investments that the company continues to make. For instance, from the start of the third quarter of this year until the end of it, the company completed construction and placed into service around $2.7 billion worth of capital projects. That included its 12 th NGL fractionator in Texas and its second PDH unit at its Chambers County facility. It also counts its Poseidon cryogenic natural gas processing plant located in the Midland Basin. And what's really great is that management intends to invest even more moving forward. Along with its third quarter earnings release, the company announced $3.1 billion of new growth capital projects in its largest business, which is the NGL Pipelines & Services segment. That brings the company up to $6.8 billion of organic growth projects that are now under construction.

{kind=link}

Even though revenue fell, the combination of market dynamics and additional projects that are now running allowed some of the firm's profitability metrics to improve year over year. Not all of them, however, managed to increase. Net profits, for instance, dropped from $1.36 billion to $1.32 billion. On the other hand, operating cash flow skyrocketed from $1.05 billion to $1.72 billion. If we adjust for changes in working capital, we get a much more modest improvement from $1.95 billion to $2.02 billion. When analyzing companies like this, I also like to look at what I refer to as ‘true free cash flow’. This strips out from adjusted operating cash flow only the capital expenditures that are dedicated to keeping operations running as is. That means that we aren't punishing the company for its growth investments. This metric came in at $1.92 billion for the quarter. That's up from the $1.87 billion reported last year. A similar metric to this is DCF, also known as distributable cash flow. It remained virtually flat at $1.87 billion. And finally, EBITDA for the enterprise grew from $2.26 billion to $2.33 billion.

{kind=link}

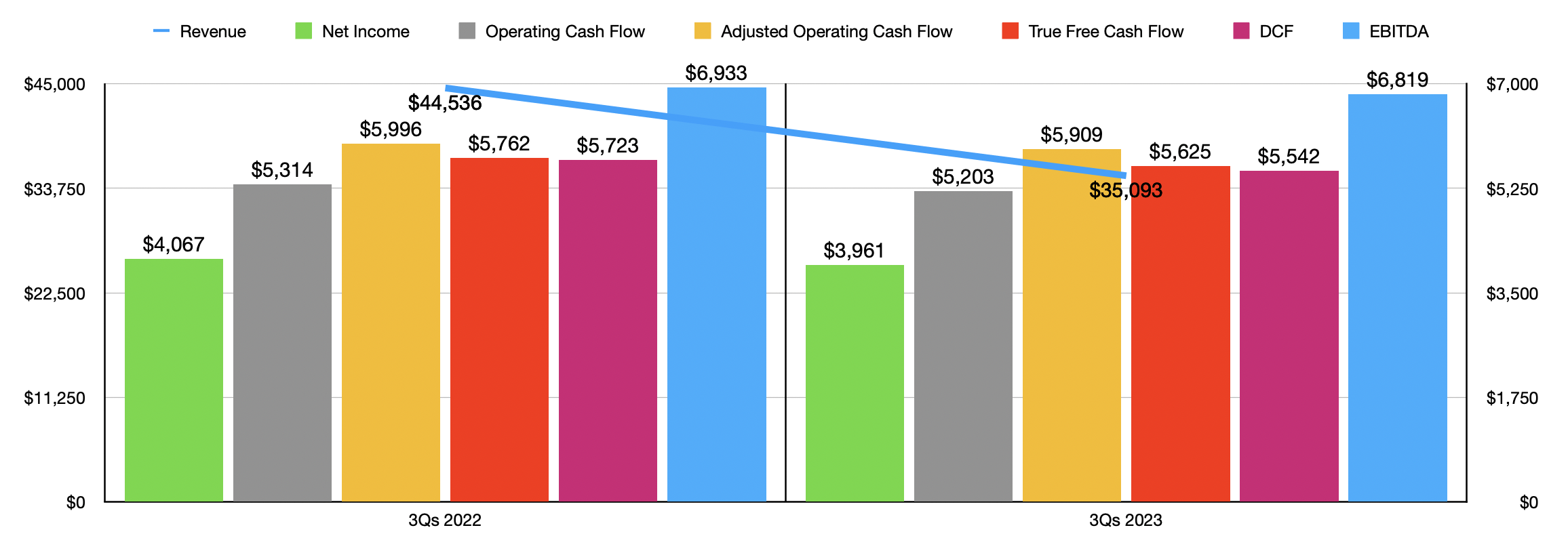

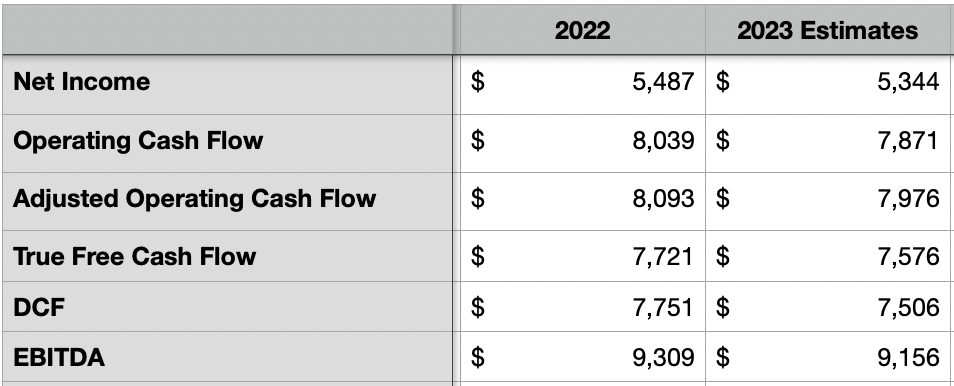

As shown in the chart above, financial performance for the first nine months of this year has been largely weaker than it was for the same time of last year. So it is nice to see so many of the cash flow metrics improve year over year in the third quarter. Unfortunately, management does not do well when it comes to providing much in the way of guidance. But if we annualize the results seen so far, we would expect cash flows for this year as shown in the table below. That table also shows results for the 2022 fiscal year.

{kind=link}

*$ in Millions

{kind=link}

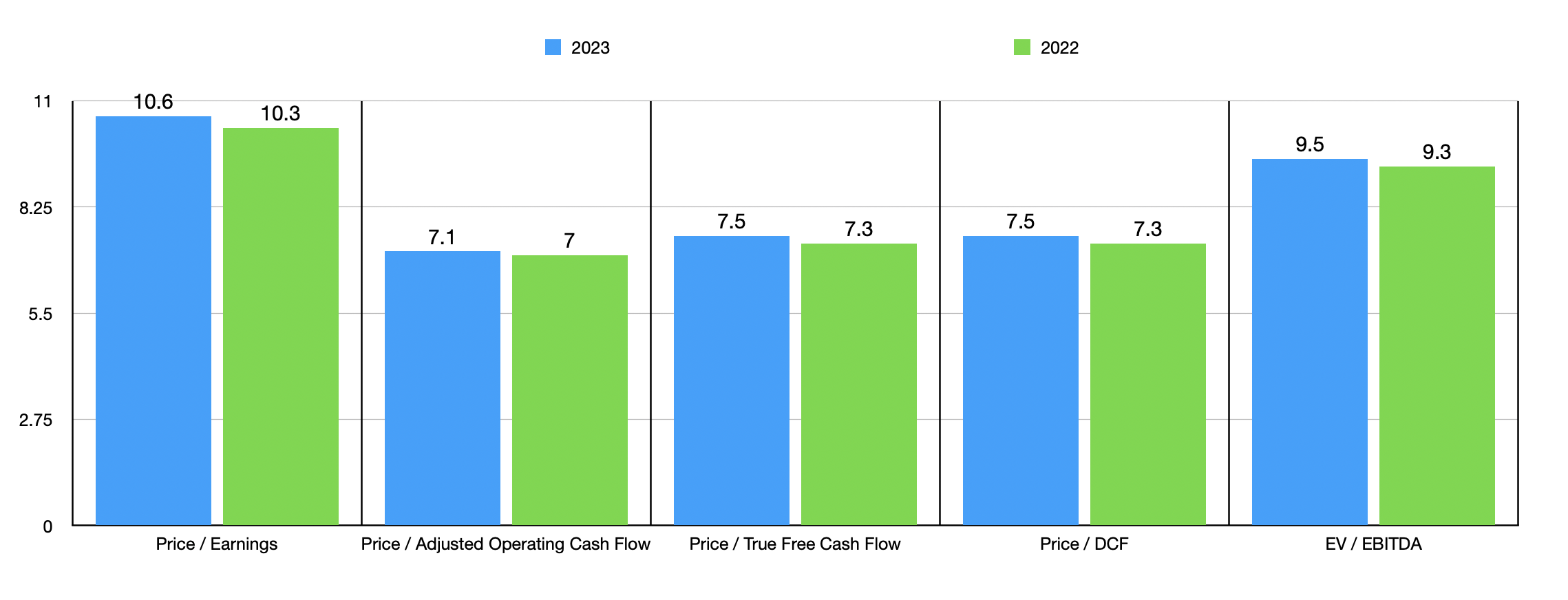

Taking that data, I then was able to create the chart above. In it, you can see how shares are priced both on a forward basis and using data from 2022. Naturally, the stock does look a bit more expensive. But given that all of these metrics, except the price to earnings multiple, are in the single digits, I would still consider the stock cheap on an absolute basis. The next question, however, is how cheap shares might be compared to similar firms. In the table below, I priced the company next to five similar enterprises. I did so using only two of the profitability metrics. These are the two that I believe are most vital for determining the relative valuation of the enterprise. Using the price to operating cash flow approach, I found that four of the five companies ended up being cheaper than Enterprise Products Partners. And when it comes to the EV to EBITDA approach, only two of the five firms were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Enterprise Products Partners |

| 7.1 |

| 9.5 |

| TC Energy ( TRP ) |

| 6.4 |

| 15.9 |

| Kinder Morgan ( KMI ) |

| 6.5 |

| 10.5 |

| The Williams Companies ( WMB ) |

| 7.5 |

| 9.9 |

| Cheniere Energy ( LNG ) |

| 4.0 |

| 4.2 |

| Energy Transfer ( ET ) |

| 4.0 |

| 7.8 |

Takeaway

All things considered, I would argue that Enterprise Products Partners is still a solid player in the midstream/pipeline market. While not everything's perfect, the overall picture is impressive and shares of the business look cheap on an absolute basis. They are also more or less fairly valued relative to similar enterprises. What's important though is that, in addition to being cheap, the company continues to invest in growth initiatives. It also is rewarding shareholders directly at the same time. In the last nine months, for instance, the company repurchased $92 million worth of shares while continuing to boast a distribution that gives it a yield of 7.56%. This does not mean that the company is at the top of my list, however. The top prospect, which is a company that I own shares of, is Energy Transfer. In addition to being cheaper, Energy Transfer has a higher yield of 9.51% at this time. But for those who do believe that Enterprise Products Partners is a good opportunity, my sentiment would be that it's far from being a bad one.

For further details see:

Enterprise Products Partners: It Still Makes Sense To Be Bullish