SPY - EOS: Portfolio Concerns And Declining NAV Are Reasons To Avoid

Summary

- Eaton Vance Enhanced Equity Income Fund II seeks to provide investors with a high level of income through a covered call options strategy.

- The closed-end fund is very heavily weighted towards the FAAMG stocks, which have delivered a very disappointing performance as the Federal Reserve tightens policy.

- The EOS fund's portfolio appears to be poorly configured with the impending recession.

- The fund is failing to cover its distributions and had to cut its payout back in November.

- The fund is overvalued right now and best avoided until the price declines.

Without a doubt, one of the biggest problems plaguing most Americans today is the pervasive inflation that has driven up the costs of nearly everything that we consume in our daily lives. This inflation has been most heavily centered on food and energy, which are both necessities. Unfortunately, this has had an outsized impact on the most vulnerable members of society. This is likely one reason why credit card debt is currently at an all-time high and the savings rate has hit the lowest level that it had in seventeen years. It is also why a recent Prudential Pulse survey revealed that roughly 81% of Generation Z members and 77% of Millennials have entered or are considering entering the gig economy just to obtain extra money to make ends meet.

Fortunately, as investors, we do not need to resort to such measures in order to get the extra income that we need to maintain our standard of living in today’s economic climate. This is because we can put our money to work for us. One of the best ways to do this is to purchase shares of a closed-end fund ("CEF") that specializes in the generation of income. These funds are quite nice because they provide easy access to a professionally-managed portfolio of assets that can usually generate a higher yield than any of the individual assets possesses.

In this article, we will discuss the Eaton Vance Enhanced Equity Income Fund II ( EOS ), which is one closed-end fund that investors can use for the purpose of generating income. As of the time of writing, this fund pays an 8.12% yield, which is certainly enough to turn most heads. Unfortunately, the fund looks to be expensive today but that does not mean that it is not worth following as there is a possibility that a more attractive price will present itself at some point in the future. Let us investigate and see if this fund could be a worthwhile addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Eaton Vance Enhanced Equity Income Fund II has the stated objective of providing its investors with a high level of current income. The fund has a secondary objective of capital appreciation. This is not exactly surprising considering that the fund specifically states that it aims for income in its name. However, equity funds are generally more interested in total return than in income. After all, equity is by its nature a total return instrument since investors that purchase common stock are typically seeking both income and capital gains. This fund is certainly an equity fund as currently all of its assets are invested in common stock:

CEF Connect

This is one thing that differentiates the Eaton Vance Enhanced Equity Income Fund from other equity income closed-end funds. We commonly see that many of these funds also include preferred stock and debt in their portfolios. That makes a great deal of sense since preferred stock typically has a higher yield than the common stock of the same company. In fact, outside of the traditional energy sector, debt also typically has a higher yield than common equity issued by the same company. Thus, this fund must be doing something other than purchasing high-yielding fixed-income securities to boost its yield to an acceptable level for an income investor.

We can see quite clearly what the fund is doing differently than many other equity income funds by looking at its fact sheet . The Eaton Vance Enhanced Equity Income Fund is not only investing in common stocks that are expected to deliver an appealing total return but is then writing call options against these stocks. This is called a “covered call strategy,” and it is one of the best ways to generate income from a common stock portfolio. Basically, what you are doing is creating the option out of thin air and then selling it for an upfront payment. The buyer of the option then has the right to purchase the stock from you at a price that is specified in the option, but the buyer must exercise this right by a specified date. In exchange for this, you get to keep the upfront payment regardless of whether the option is exercised or not. The premium paid by the buyer is thus how the strategy generates income. Naturally, the goal is for the buyer to not exercise the option by the expiration date, allowing you to keep the upfront premium and then write another option to repeat the process and thus generate a steady source of income.

The fact that this fund is using an options strategy might concern some risk-averse investors, however. After all, we have all heard about how risky option strategies can be. However, the covered call option is quite safe. This is because the worst possible outcome is that you have to sell stocks that you already own. The only real downside is that you will not get as large of a capital gain as you would have had the option not been exercised. If the strike price of the option is greater than the price that the fund paid for the stock, then it is effectively guaranteed to generate a capital gain even in the worst-case scenario. If the stock goes down, then the upfront premium that was received helps to offset the capital loss from the declining stock price. Thus, in many ways, this fund’s strategy is actually less risky than a similar fund that does not use the options strategy and it generates a higher level of income. That is something that any risk-averse investor should appreciate.

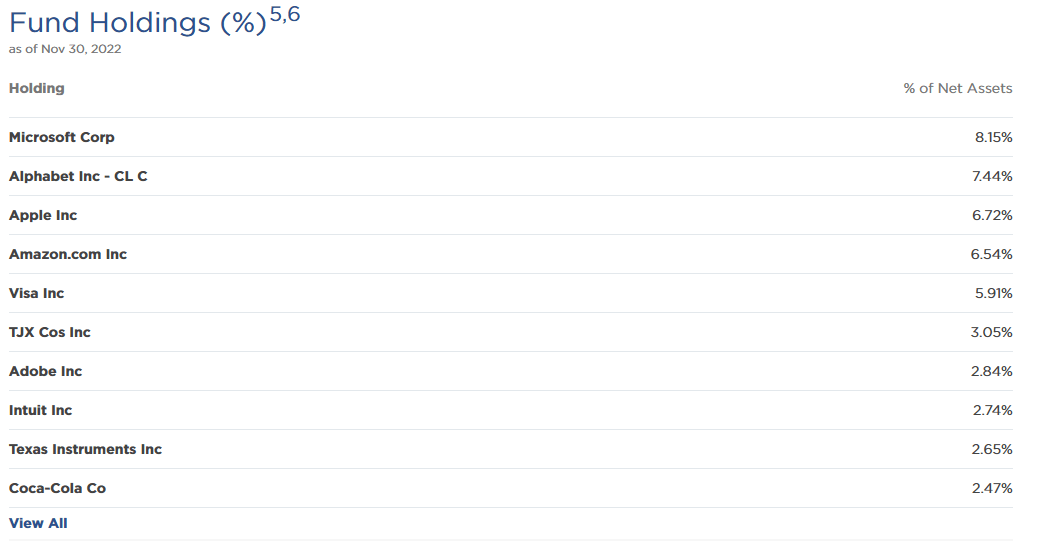

In various previous articles, I have criticized a number of Eaton Vance’s closed-end funds for not having an especially good portfolio for the conditions that have prevailed in the market over the past year. This one suffers from that same problem, which we can clearly see by looking at the largest positions in the fund:

{kind=link}

The big problem here is the sheer number of technology companies that account for the fund’s largest positions. These stocks were darlings of the market back during the Federal Reserve’s loose money days but they have performed very poorly now that inflation has set in and the central bank has begun raising interest rates:

{kind=link}

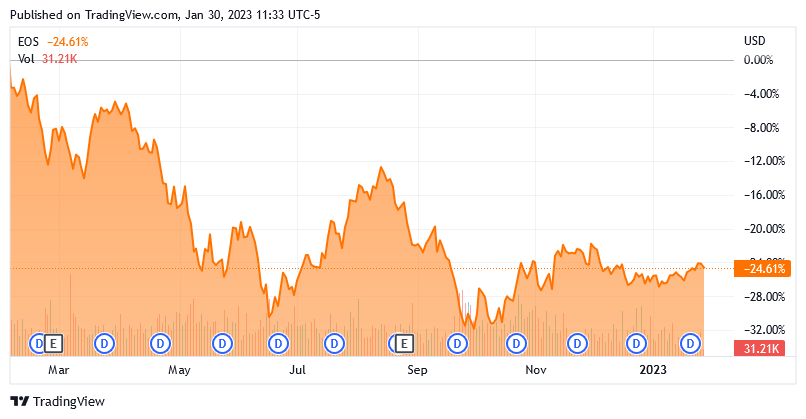

As we can see, all of these stocks are down at least 20% over the past twelve months, except for Apple Inc. ( AAPL ). However, even Apple has lost 17.38% of its former value. This is a big reason why the fund itself is down 24.61% over the same period:

{kind=link}

The fund’s heavy exposure to these poorly performing technology stocks is quite evident by looking at its high weighting to them. As my regular readers on the topic of closed-end funds are likely well aware, I do not like to see any single position in a fund account for more than 5% of the fund’s total assets. This is because that is approximately the point at which a given asset begins to expose the portfolio to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if the asset accounts for too much of the portfolio, then it will not be completely diversified away. Thus, the concern is that some event will occur that causes the price of a given asset to decline when the market does not, and if it accounts for too much of the portfolio, it will end up dragging the entire fund down with it. As we can see above, all four of the mega-cap technology stocks have a weighting that is well above 5% so they all exerted significant downward pressure on the fund’s portfolio over the past year. This is exactly what we see with its disappointing performance.

The fund’s holdings by sector are also somewhat disappointing. Here they are:

CEF Connect

One thing that we quickly note here is that the technology sector accounts for 36.44% of the fund’s assets. This is substantially above the 26.67% weighting to the technology sector in the S&P 500 Index (SP500). We also see significant exposure to consumer cyclical in the fund, which may not be the best idea. As I noted in the introduction, the raging inflation that we have seen in the United States over the past year has stressed consumers to the point that the savings rate is at a seventeen-year low, and credit card debt is at an all-time high. This is a clear sign that consumers are at their breaking point and are unlikely to be engaging in much discretionary spending. Thus, a more defensive portfolio may be in order, as would adding some exposure to energy (the highest-performing sector in 2022).

With all that said though, the Eaton Vance Enhanced Equity Income Fund II does have an incredibly low annual turnover for an equity closed-end fund. The fund’s turnover of 18.00% is much lower than that of nearly all equity funds and even most fixed-income funds. This is something that is fairly attractive since a high annual turnover can be a drag on a fund’s performance. This is because it costs money to trade stocks and other assets, which is billed directly to the fund’s shareholders. This creates a drag on the fund’s performance because management needs to generate sufficient returns to cover these expenses and still deliver a high enough return to satisfy the investors. This is a task that few management teams are able to achieve consistently, which is one reason why actively-managed funds tend to underperform their relevant indices. The Eaton Vance Enhanced Equity Income Fund II does not have an official benchmark index, but it did underperform the S&P 500 Index substantially in 2022.

Distribution Analysis

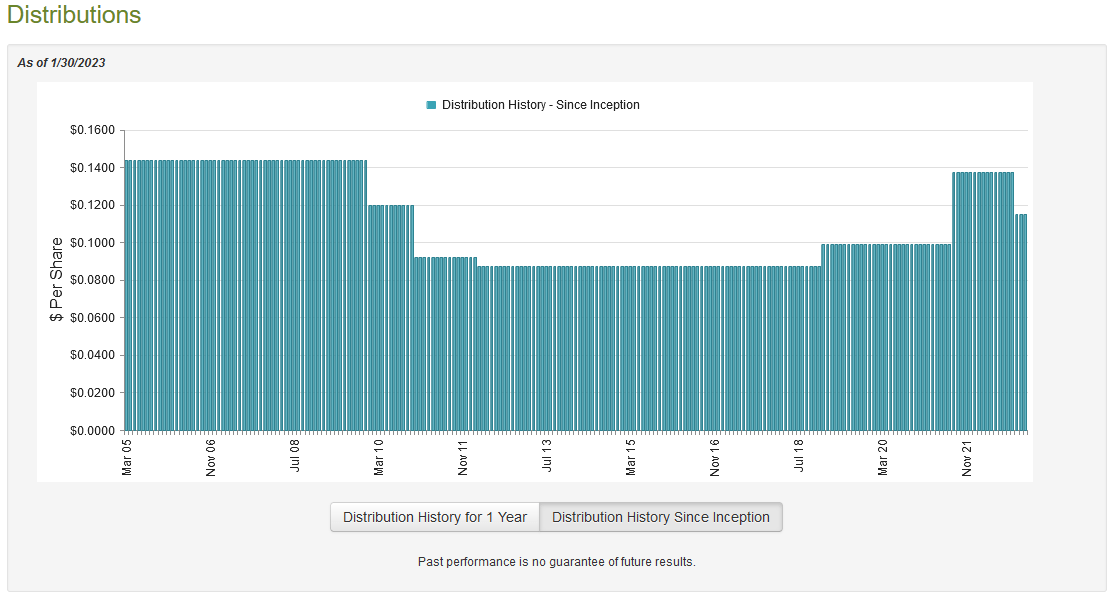

As stated earlier in this article, the primary objective of the Eaton Vance Enhanced Equity Income Fund II is to provide its investors with a high level of current income. It does this mostly through a covered call strategy, which does tend to produce a great deal of income when properly executed. As such, we might assume that the fund itself pays a fairly high yield. This is certainly the case as the fund currently pays a monthly distribution of $0.1152 per share ($1.3824 per share annually), which gives it an 8.12% yield at the current price. The fund’s distribution has varied quite a bit over the years and it, unfortunately, cut back in November:

{kind=link}

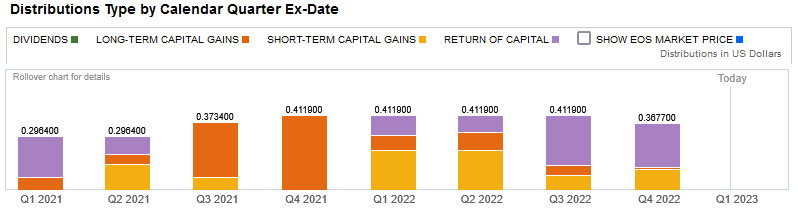

This distribution cut was probably due to the portfolio not being very well positioned for the Federal Reserve’s abandonment of the easy money policy that dominated in the fourteen years since the last financial crisis. The fact that its distribution has varied quite a lot over the years though could be a turn-off for those investors that are looking for a secure and consistent distribution to use to pay their bills and finance their lifestyle. These same investors might also be concerned about the fact that the fund has been making a number of return of capital distributions recently:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital distribution, such as the distribution of money received through option strategies under certain conditions. We also see that the fund has been making some substantial capital gains distributions. These may not be sustainable either since the fund actually has to have capital gains and sufficient capital gains consistently in order to maintain its distribution. That may not always be possible as we saw with the fall of the mega-cap technology stocks in 2022. As such, we want to have a look at the fund’s finances to determine exactly how it is financing its distributions and how sustainable they are likely to be.

Unfortunately, we do not have an especially recent document to consult for this purpose. The fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2022. As such, the report will not include details about the fund’s performance during the third and fourth quarters of 2022, which is when the fund made numerous return of capital distributions. However, the Federal Reserve began its tight money policy in March of 2022 so this report should still give us a good idea of how well the fund navigated that and the market turbulence that accompanied it. During the six-month period, the Eaton Vance Enhanced Equity Income Fund II received a total of $4,597,821 in dividends and, surprisingly, no interest from the investments in its portfolio. This gives it a total income of $4,597,821 during the period. The fund paid its expenses out of this amount, leaving it with a negative $848,155 available to pay the shareholders. In other words, the fund’s dividend income was not sufficient to cover its expenses. This is probably because of the fund’s technology-heavy portfolio that results in a substantial number of its assets having either no or a very low yield.

However, the fund’s reported income does not include the amount that it receives from the options premiums. This is because that money is classified as either capital gains or return of capital, depending on the situation. In addition, the fund can generate money through capital gains to pay its distributions. As might be expected though, it did not have much success at this during the first half of 2022. The fund did manage to realize net gains of $37,659,794 but this was more than offset by $362,257,078 net unrealized losses. The fund paid out $42,268,199 in distributions so clearly it failed to cover them. Overall, the fund’s assets fell by $361,292,182 during the period. Perhaps even more disappointingly, the fund’s assets at the end of June 2022 were lower than its assets at the start of 2021:

| June 30, 2022 |

| January 1, 2021 |

| Net Assets as of Date |

| $850,732,178 |

| $1,055,566,592 |

This certainly explains the distribution cut and it also very clearly illustrates my earlier point about the fund’s portfolio being poorly positioned for the current market environment. Unfortunately, we will have to wait and see if the fund managed to improve its situation in the second half of 2022 by reducing its outflows with the distribution reduction. The next two semi-annual reports will tell this story.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Enhanced Equity Income Fund II, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is unfortunately not the case with this fund today. As of January 27, 2023 (the most recent date for which data is currently available), the Eaton Vance Enhanced Equity Income Fund II had a net asset value of $16.73 per share but the shares actually trade for $16.94 per share. This gives the fund’s shares a 1.26% premium to the net asset value at the current price. This is a much more attractive price than the 5.08% premium that the shares have had on average over the past month. However, the fund’s disappointing performance is hardly deserving of a premium and it is generally not a great idea to pay a premium for any fund. Thus, the fund looks overvalued today and it would make sense to wait until the price comes down before purchasing shares.

Conclusion

In conclusion, the Eaton Vance Enhanced Equity Income Fund II has a very good strategy as covered calls are a great way to both reduce risk and generate income from a common stock portfolio. However, this particular fund is far too heavily invested in a handful of mega-cap technology stocks that have delivered very disappointing performances over the past year. The fund is also overly exposed to consumer discretionary stocks at a time in which the budgets of many consumers do not allow for much in the way of discretionary purchases. Thus, it may be a good idea to avoid this fund until economic conditions improve significantly or it alters its portfolio. The fact that it is trading at a premium valuation and cannot cover its distributions only increases the strength of this conviction. I want to like Eaton Vance Enhanced Equity Income Fund II because it is one of the few covered call closed-end funds in the market, but its problems are too great to ignore.

For further details see:

EOS: Portfolio Concerns And Declining NAV Are Reasons To Avoid