CA - Equinox Gold: Margins Up But Output Tracking To Low End Of Guidance

2023-11-01 17:29:25 ET

Summary

- Equinox Gold Corp. reported a 4% increase in production year-over-year but will see production come in well below its guidance mid-point for a second consecutive year.

- On a positive note, the company has ample liquidity to complete Greenstone even in a lower gold price scenario, and the project remains on schedule/budget.

- In this update, we'll dig into Equinox Gold Corp.'s Q3 results, what the outlook is for 2024, and where the stock's updated low-risk buy zone sits heading into a transformative year.

The Q3 Earnings Season for the Gold Miners Index ( GDX ) began last week, and one of the most recent companies to report its results is Equinox Gold Corp. ( EQX ). Overall, the company had a better quarter with a 7% decline in all-in sustaining costs [AISC] and a 4% increase in overall production. However, this was largely because of being up against easy year-over-year comparisons. On a positive note, Greenstone remains on budget and schedule against all odds with its first gold pour expected in H1 of next year. However, sales from this asset will be lower than initially anticipated with a recent deal to sell the greater of 500 ounces per month or 1.8% of monthly gold production from Greenstone to help improve its balance sheet at 20% of the gold price (subject to partial buy down option). Let's take a closer look at the recent results below:

{kind=link}

Q3 Production & Sales

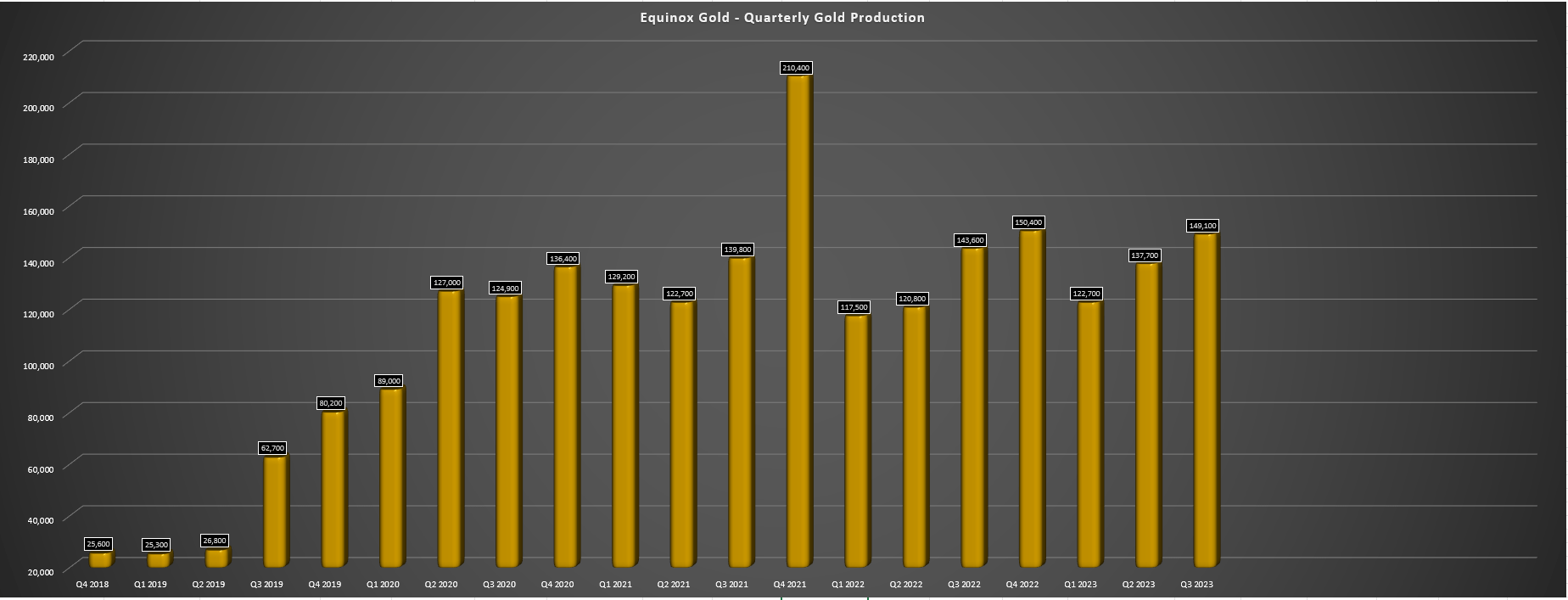

Equinox Gold released its Q3 results this week, reporting quarterly gold production of ~149,100 ounces, a 4% increase from the year-ago period. The increase in production was related to a better quarter at Los Filos (~39,500 ounces) which was up against very easy comparisons, a better quarter at Aurizona (higher grades and throughput), and a better quarter at RDM which was also lapping easy comparisons (processing of low-grade stockpiles which pit was de-watered). Unfortunately, the improvement in production at these assets was offset by a weaker quarter at Mesquite with Equinox noting that it had temporary issues with leach pad chemistry and lower production from its new Santa Luz Mine (lower grades and recoveries offsetting higher throughput of ~618,000 tonnes). This led to all-in sustaining costs at Santa Luz of $1,834/oz in the period ($1,682/oz year-to-date), a disappointing start for this asset that just went into commercial production.

Equinox Gold - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

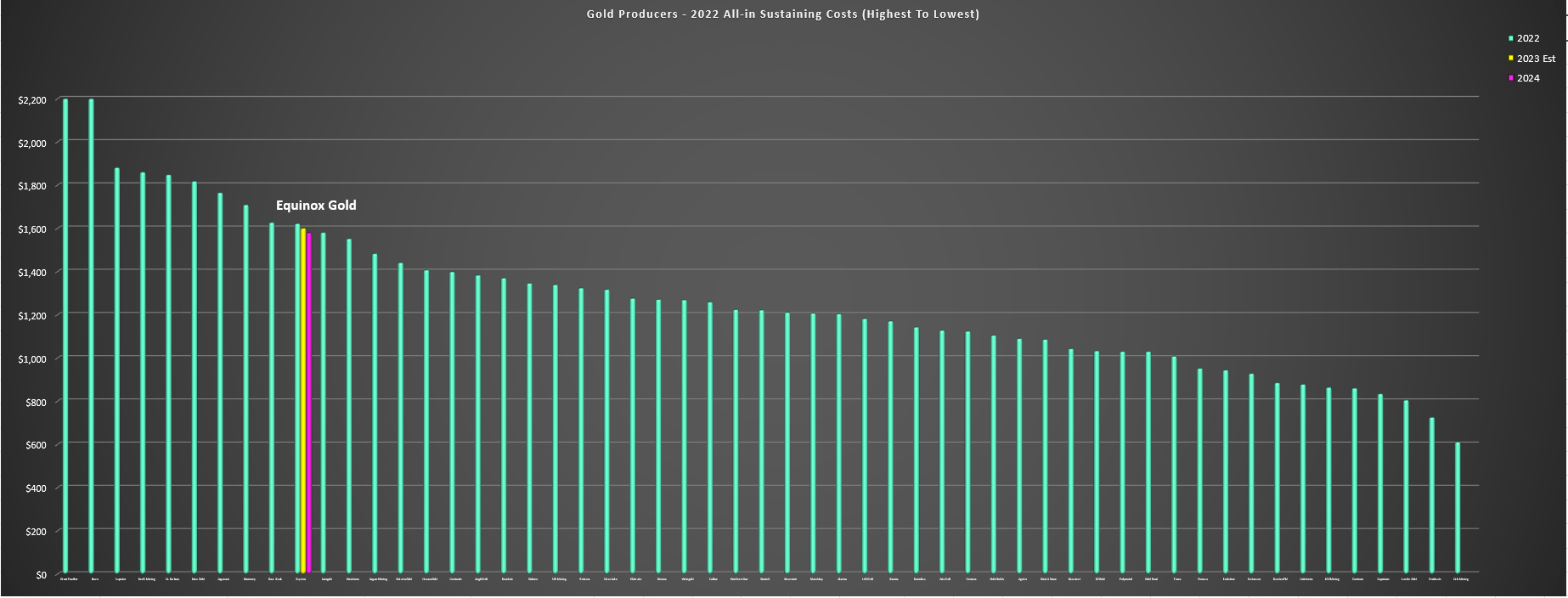

Looking at how Equinox is tracking in relation to guidance, the company has produced just ~409,500 ounces year-to-date, suggesting that it will come in well below its guidance mid-point for a second consecutive year and with production down on a two-year basis. This is because even if the company produces ~155,000 ounces of gold in Q4, this would still place production over 4% below its guidance mid-point of 590,000 ounces of gold. And while AISC is on track to improve year-over-year, this isn't saying much when Equinox was one of the top-10 highest-cost producers in 2022, and the highest-cost producer of its peer group from a scale standpoint (500,000+ ounces) except for Harmony Gold ( HMY ).

FY2022 production came in at ~532,000 ounces, which was 20% below its FY2022 guidance mid-point of ~667,000 ounces of gold.

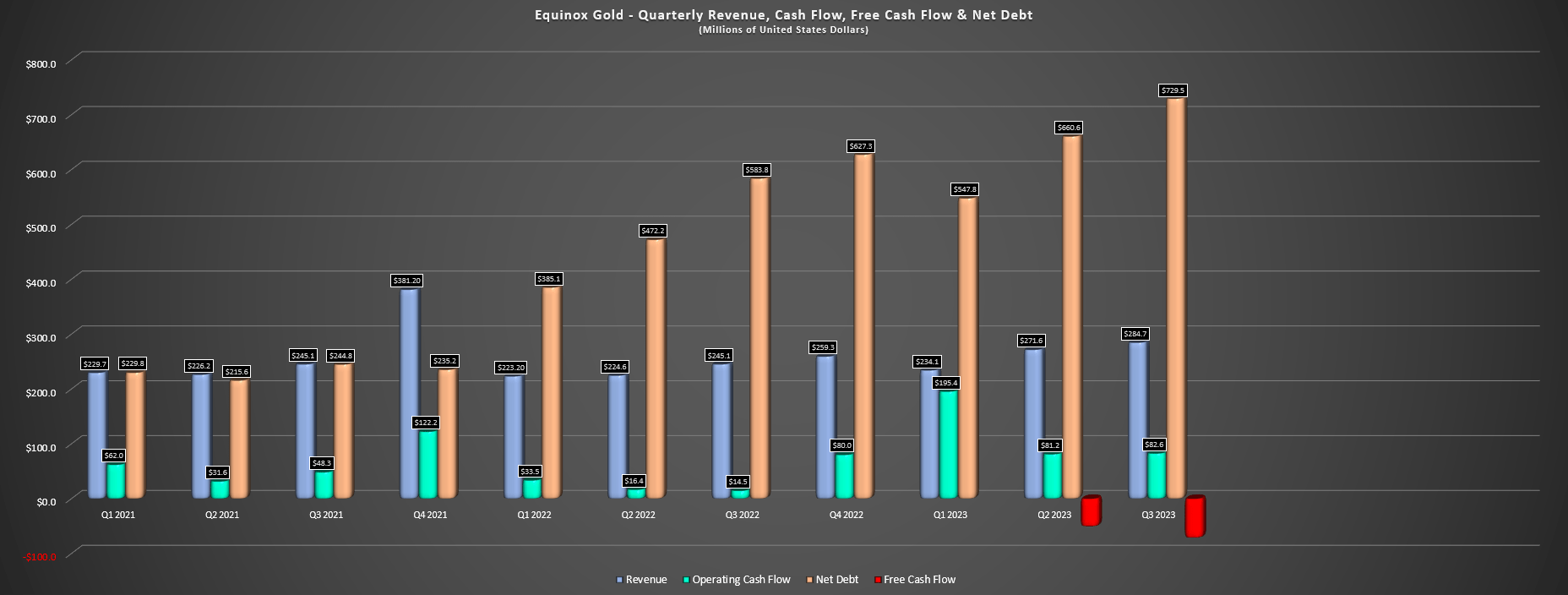

Digging into Equinox's operations a little closer, there wasn't much to write home about despite the benefit of lower consumables costs vs. peak costs last year, with Castle Mountain producing ~4,200 ounces at $1,648/oz, Los Filos producing ~39,500 ounces at $2,082/oz despite lower sustaining capital, and arguably its best mine Aurizona producing ~32,200 ounces at costs still well above the industry average at $1,492/oz. Fortunately, Equinox benefited from a higher average realized gold price of $1,917/oz, which aided in increasing its revenue to $284.7 million, and cash flow before working capital changes improved to $82.6 million. Still, the company still saw a significant cash outflow given the higher capital expenditures at Greenstone, and net debt has risen to $730 million before the Sandbox transaction subsequent to quarter-end, meaning that a successful ramp-up at Greenstone will be critical so the company can start paying down debt.

Equinox Quarterly Revenue, Cash Flow, Free Cash Flow & Net Debt - Company Filings, Author's Chart

{kind=link}

Costs & Margins

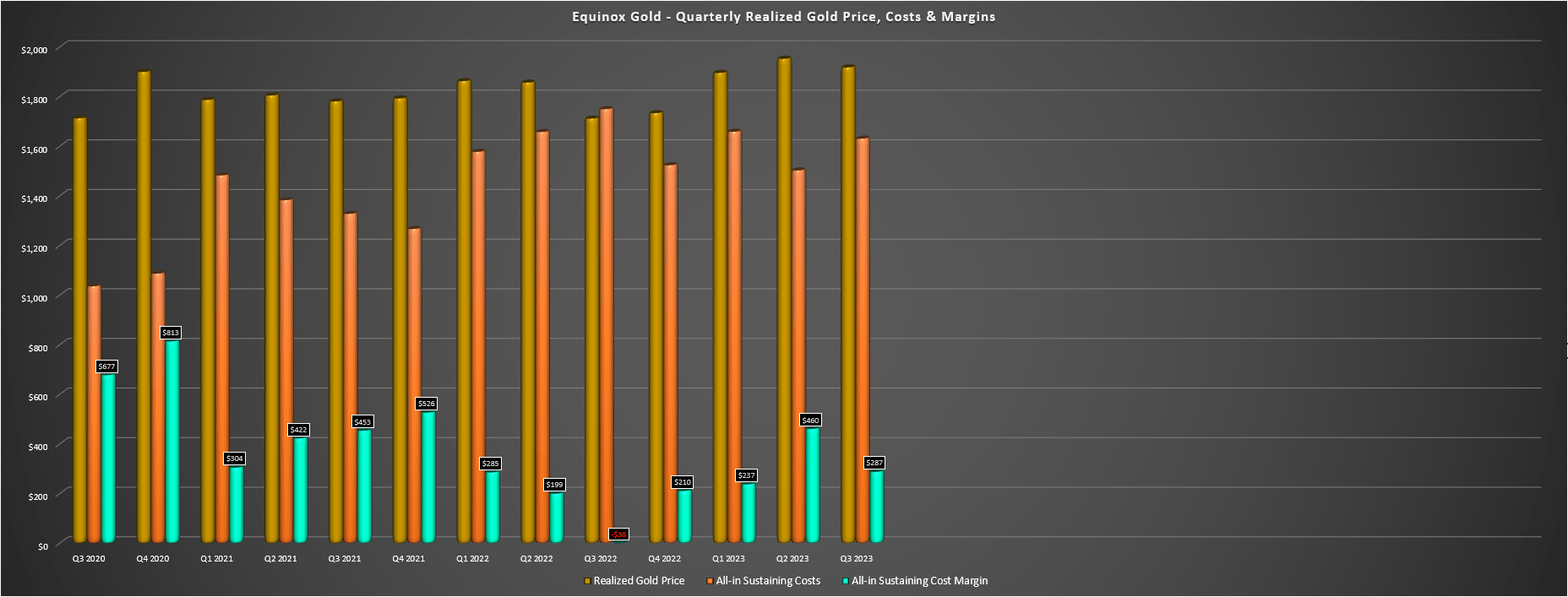

Moving over to costs and margins, we saw a meaningful improvement here, but once again, this was largely a function of being up against some of the easiest comps of any producer sector-wide given that Equinox's Q3 2022 costs were the highest on record and among the highest sector-wide. As shown below, Equinox's cash costs and AISC were down 2% and 7% year-over-year respectively, to $1,363/oz and $1,630/oz, and this resulted in a meaningful improvement in AISC margins which jumped to $287/oz vs. negative levels last year. Equinox noted that this was partially to lower costs of key consumables, but another significant benefit was the lower sustaining capital in the period which was deferred into Q4 that resulted in much better AISC figures in the current quarter. And if sustaining capital was closer to full-year planned levels and closer to $43 million, AISC would have come in above $1,700/oz and over 25% above the industry average (Q3 2023 estimates: ~$1,350/oz).

Equinox Gold - Quarterly Gold Price, AISC & AISC Margins - Company Filings, Author's Chart

{kind=link}

On a positive note, Equinox's 60% ownership of Greenstone (~90% complete with pre-commissioning activities underway) will have a significant positive effect on its consolidated all-in sustaining costs, especially if the company can optimize its portfolio (focus on margins vs. absolute ounces). This is because Greenstone is expected to translate to attributable production for Equinox of 240,000 ounces per annum in its first five years at sub $875/oz AISC even being conservative and accounting for inflationary pressures. This would make it the lowest-cost asset in its portfolio by a wide margin and certainly help to drag down costs after a tough two-year stretch. That said, these margin benefits will not show up immediately given the ramp-up period for a mine of this size. Hence, even with Greenstone set to pour first gold pour in H1-2024, I would expect limited free cash flow generation next year for Equinox and all-in sustaining costs to come in at or above $1,550/oz before costs finally start to come down closer to the sector average in 2025.

Recent Developments

Finally, looking at recent developments, Equinox issued $172.5 million in convertible notes in September at 4.75% with an initial conversion price of $6.30 per share. This allowed the company to repay $116 million on its RCF, and the company has since continued to make progress at Greenstone with ~89% of the approved budget (~$1.20 billion on 100% basis) spent to date. However, following quarter-end, the company chose to sell 1.80% of monthly production (or 500 ounces, whichever is greater) at Greenstone (100% basis) to Sandbox Royalties for $75 million. The deal will result in an average of 600 ounces going out the door per quarter in the first five years of production for Equinox or ~$1.0 million less in sales per quarter at spot prices. And while there is a buyback option for 75%, the two deals will result in lower sales than anticipated and a higher fully diluted share count.

On a positive note, the company now has liquidity of ~$600 million following the Sandbox deal vs. operating and capital commitments of $580 million in the next twelve months. This gives it breathing room to complete construction at Greenstone and survive the lengthy ramp-up phase without additional share dilution if we were to see a correction in the gold price that impacted its near-term cash flow (current operations). That being said, while Greenstone being so close to completion and navigating the tough environment on budget is undoubtedly positive, Greenstone is one world-class asset among several average assets, and it's difficult to see a path to sub $1,350/oz AISC on a sustainable basis without some portfolio optimization even with Greenstone in the portfolio.

Valuation

Based on ~394 million fully diluted shares and a share price of US$4.50, Equinox trades at a market cap of ~$1.77 billion and an enterprise value of ~$2.03 billion. This makes Equinox one of the lowest capitalization names in the sector among those producers with the potential to produce upwards of 800,000 ounces of gold by 2025, with its enterprise value being significantly below that of SSR Mining ( SSRM ) and Alamos Gold ( AGI ).

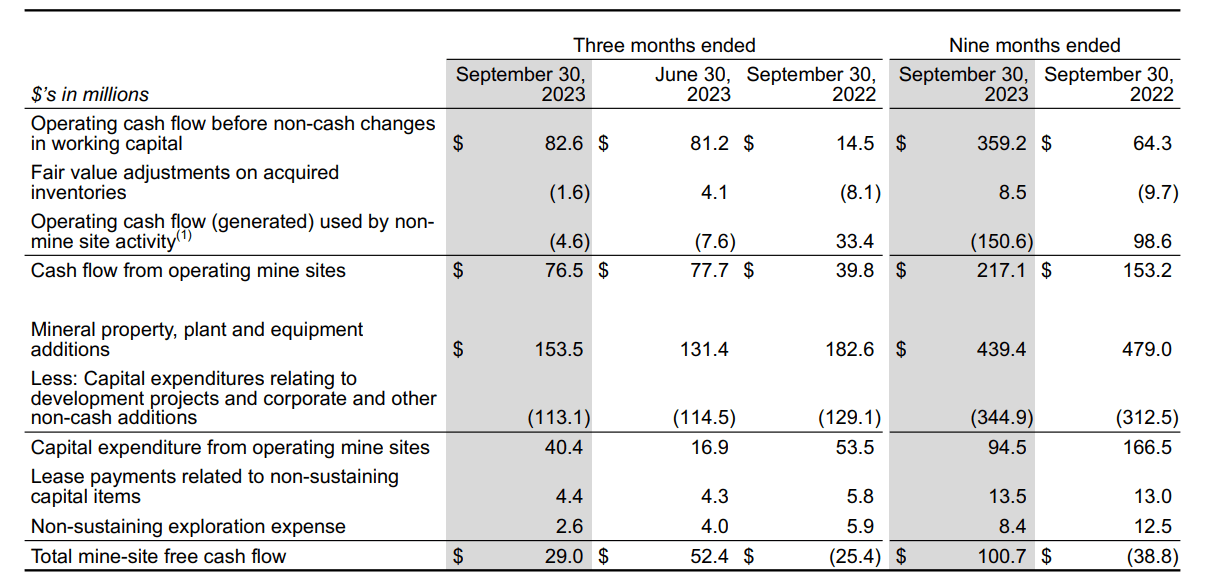

That said, the company has a much weaker balance sheet than both companies, with over $600 million in debt (excludes convertible notes), and lower quality assets on balance, with significant concentration to Tier-2 ranked jurisdictions (Mexico, Brazil), and higher cost assets (FY2022 AISC: $1,622/oz). In fact, the only real standout assets are Aurizona and Greenstone, with its portfolio generating barely $100 million in free cash flow across its seven mines year-to-date, which is less than one of Alamos' mines in the same period (Mulatos Complex: ~$115 million).

Equinox - Year-to-Date Mine Site Free Cash Flow - Company Filings

{kind=link}

However, while Equinox may deserve to trade at a discount to AGI and SSRM given that it has a high-cost and lower-quality portfolio, the stock is still very reasonably valued. This is because EQX trades at less than 0.70x P/NAV based on an estimated net asset value of ~$2.65 billion, a valuation that is typically reserved for a producer with its assets in Tier-3 ranked jurisdictions and or a single-asset producer that's more sensitive to the gold price (higher costs). And while there's no question that Equinox is sensitive to the gold price with FY2024 AISC likely to come in above $1,550/oz during the ramp-up phase at Greenstone, we should see company-wide AISC improve to $1,400/oz on lower in FY2025 which should help with a re-rating.

So, even if we use a conservative multiple of 0.90x P/NAV given the multiple compression we've seen sector-wide, Equinox could command a valuation closer to US$6.00 per share (assuming no additional share dilution).

2022 Producers All-in Sustaining Costs vs. EQX 2022 & 2023/2024 Estimates - Company Filings, Author's Chart & Estimates

{kind=link}

All that being said, I prefer to buy producers with stronger balance sheets, lower-cost assets (less sensitive to gold price), and ideally those generating meaningful free cash flow. And while Equinox will be in this position in 2025, I wouldn't expect to see a much better year in 2024 given that it will take time to push Greenstone to commercial production and its other high-cost assets continue to be a drag on margins. In addition, I prefer a minimum 40% discount to fair value when it comes to small-cap producers to ensure a margin of safety.

Hence, if we apply this 40% discount to fair value to the stock's 18-month target price (0.90x P/NAV on ~395 million fully diluted shares), the ideal buy zone for the stock comes in at US$3.65 or lower. To summarize, I still don't see a low-risk buying opportunity yet, and I continue to see more attractive bets elsewhere in the sector.

Summary

Equinox Gold Corp. has done an impressive job of keeping Greenstone on schedule and budget and the heavy lifted is in the rear-view mirror with project progress at ~90% completion and the company avoiding asset sales or heavy share dilution thus far. This is certainly a better outcome than the significant asset sales and dilution following capex blowouts that we saw from Iamgold ( IAG ) and Argonaut ( ARNGF ), respectively, and while Equinox sold one asset, the Mercedes sale turned out to the right move.

However, while Equinox Gold Corp. is cheap and its 60% share of Greenstone is transformative, I don't expect a significant improvement in its all-in sustaining cost profile for at least six quarters (Q1 2025), and I continue to favor other names given EQX's outperformance year-to-date. To summarize, while I strongly consider Equinox Gold Corp. stock below US$3.65, I remain on the sidelines for now.

For further details see:

Equinox Gold: Margins Up But Output Tracking To Low End Of Guidance