SPY - ETJ: Outperformed S&P 500 Last Year But Still Failed To Cover The Distribution

2023-03-24 05:35:54 ET

Summary

- Investors are desperate for income to maintain their standard of living against inflation, which makes funds like ETJ appealing.

- The fund's portfolio is very strange given its incredibly low yield and limited potential for capital gains due to the options strategy.

- The fund's options strategy allowed it to outperform the market in 2022 but it still delivered a loss.

- The fund failed to cover its distribution last year and was forced to cut.

- The fund is now trading at a reasonable valuation, an improvement from the premium that it had back in 2021.

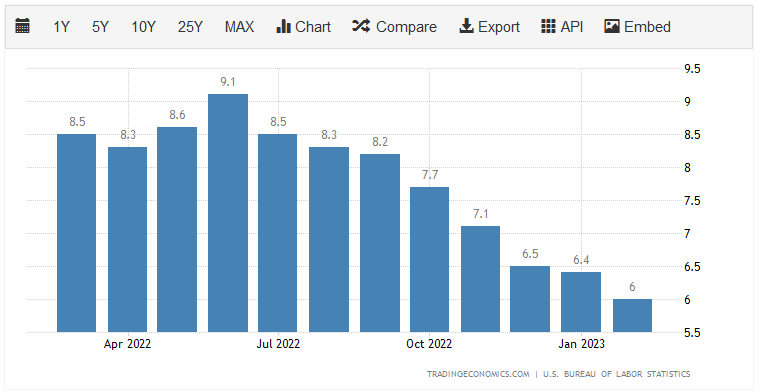

It almost goes without saying that the biggest problem facing most Americans today is the incredibly high level of inflation that has been dominating the economy. Over the past year, there has not been a single month in which the consumer price index went up by less than 6% year-over-year:

{kind=link}

For the most part, wages have not kept up with this level of price increases. Real wage growth in the United States has been negative for two years now, so people can generally afford much less than they could back in 2020. This has caused a surge in people seeking second jobs or gig work simply to get the extra income that is needed to maintain their lifestyles, which I discussed in two recent blog posts (see here and here ).

Fortunately, as investors, we do not have to resort to such methods in order to increase our incomes and maintain our lifestyles. This is because we are able to put out money to work for us. One of the best ways to do this is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are not followed particularly often by the investment media or by most market participants, but they are one of the best vehicles for income investors. This is because they provide an easy way to obtain a portfolio of assets that can usually produce a higher yield than any of the underlying assets or pretty much anything else in the market generally.

In this article, we will discuss the Eaton Vance Risk-Managed Diversified Equity Income Fund ( ETJ ), which is one fund that can be used to earn an income. This is evident in the fact that the fund yields a respectable 9.23% as of the time of writing. I have discussed this fund before, but several months have passed since that time so a great many things have changed. This article will focus specifically on those changes as well as provide an updated analysis of the fund's financial performance.

About The Fund

According to the fund's webpage, the Eaton Vance Risk-Managed Diversified Equity Income Fund has the stated objective of providing its investors with a high level of current income and gains. This is a fairly typical objective for a closed-end fund, although we usually see it applied to fixed-income funds. This fund is certainly not a fixed-income fund, though. In fact, the fund is invested entirely in common equity, although it does have a small amount of cash available:

CEF Connect

In the case of common stock funds, the objective is usually the generation of total return. This is because a common stock is by its nature a total return vehicle. After all, investors purchase common equities for the dividends that they pay out as well as the potential for long-term capital gains. Then again, this fund includes both dividends (current income) and short-term capital gains, so it does include a few of the components of total return, although long-term gains are only a secondary objective.

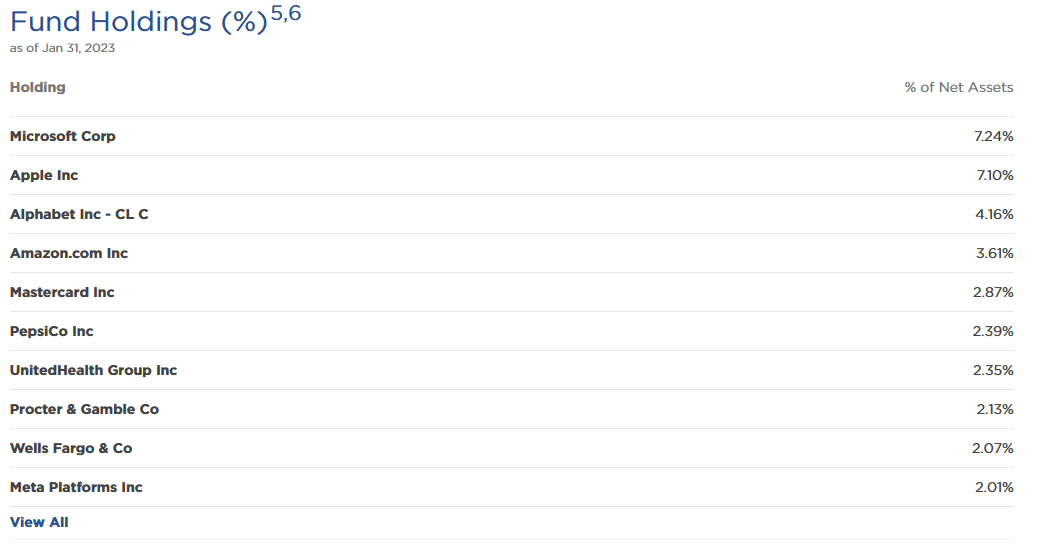

Despite the fund's stated objective of achieving current income, it does not invest specifically in dividend stocks. We can see this quite easily by looking at the largest positions in the fund's portfolio. Here they are:

{kind=link}

As I have pointed out in numerous past articles on this fund, this is a very strange portfolio for any fund that claims to have current income as an objective. This is because every stock on this list either has no dividend or has such a small yield that it hardly matters. Here are the yields of these stocks:

| Company |

| Current Dividend Yield |

| Microsoft ( MSFT ) |

| 1.00% |

| Apple ( AAPL ) |

| 0.58% |

| Alphabet ( GOOG ) |

| NA |

| Amazon ( AMZN ) |

| NA |

| Mastercard ( MA ) |

| 0.65% |

| PepsiCo ( PEP ) |

| 2.61% |

| UnitedHealth Group ( UNH ) |

| 1.39% |

| Procter & Gamble ( PG ) |

| 2.54% |

| Wells Fargo & Co. ( WFC ) |

| 3.23% |

| Meta Platforms ( META ) |

| NA |

As we can see, the only one of these companies that has a dividend yield of over 3% is Wells Fargo & Co. and even that one is well below what can easily be obtained by putting cash into a money market fund. Thus, none of these companies is at all useful for earning dividend income.

That leaves us with capital gains, and admittedly some of these did very well at that. Or at least, they did prior to 2022. As I pointed out in my last article on the Eaton Vance Risk-Managed Diversified Equity Income Fund, the Federal Reserve's monetary tightening campaign has had a much more negative impact on the technology sector than it did on any other sector of the economy. This is important because five of the ten companies on this list are mega-cap technology companies. However, now that money is no longer free, many investors have become much more discerning about where they put their money. We are not seeing things such as non-fungible tokens being sold for millions of dollars as we did at the height of the second technology bubble two years ago. The same applies to these technology companies as the market is no longer willing to assign large multiples to growth that may not occur for decades if it ever will. As a result, the stock prices of the mega-cap technology companies that are represented here have come crashing to a level that at least better reflects their intrinsic value. I discussed this in my previous article on this fund, so here is how these stocks have performed in the six months since we last discussed the fund:

| Company |

| 6-Mo. Trailing Return |

| Microsoft |

| 16.83% |

| Apple |

| 6.71% |

| Alphabet |

| 7.49% |

| Amazon |

| -12.63% |

| Meta Platforms |

| 46.37% |

This is much better than what any of these companies delivered since the start of 2022 and indeed all of them have had negative returns over the past twelve months. It is questionable where the technology industry is going since this sector continues to experience massive layoffs. According to layoffs.fyi, which is a website that has been tracking technology sector layoffs since the start of 2022, so far in 2023 517 technology companies have laid off 152,858 employees. Earlier today, Amazon's Twitch streaming unit announced that it is going to lay off 36% of its workforce. So, the layoffs continue and while that will probably be good for the near-term profits and cash flows for many of these companies (which might explain why all of them except Amazon are actually performing acceptably since we last looked at this fund), it is also a sign that the technology sector as a whole will not return to its bubble valuation levels anytime soon.

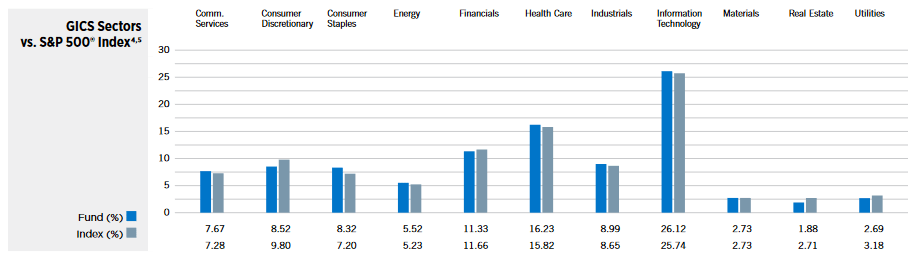

The reason that I am discussing the technology sector in an article about the Eaton Vance Risk-Managed Diversified Equity Income Fund is the incredibly high weighting that this fund has for the technology sector and for these five companies in particular. As of December 31, 2022, the technology sector accounted for 26.12% of the fund's portfolio, which is a higher weighting than the S&P 500 Index had to the sector as of that date:

{kind=link}

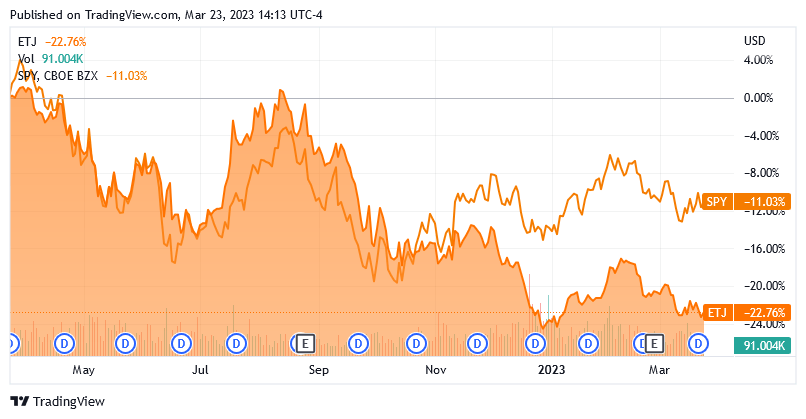

As my long-term readers on the topic of closed-end funds are no doubt well aware, I do not like to see any individual position in a fund account for more than 5% of the fund's assets. This is because that is approximately the level at which an asset begins to expose a portfolio to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the fund, then this risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market as a whole does not, and if that asset accounts for too much of the fund, then it may end up dragging the entire portfolio down with it. As we see above, Microsoft and Apple are well above that 5% level, although none of the other technology companies are anymore (Alphabet and Amazon both also were back in 2021). This is likely a reason why this fund has substantially underperformed the S&P 500 Index ( SPY ) over the past year:

{kind=link}

Admittedly, the Eaton Vance Risk-Managed Diversified Equity Income Fund does have a substantially higher yield than the index and so in terms of total return, it did not compare nearly as poorly. The fund's portfolio itself delivered a -14.93% total return in 2022 compared to -18.11% for the S&P 500 Index. However, the Eaton Vance Risk-Managed Diversified Equity Income Fund's share price delivered a total return of -22.46% during 2022 assuming all distributions were reinvested:

Fund Fact Sheet

This just goes to show you that a closed-end fund can sometimes deliver substantially different performance from the portfolio than the market price reflects. In addition, as I pointed out back in 2021 , this fund was substantially overvalued at that time, which is not the case today.

One of the interesting things about this fund is the way that it uses options in its investment strategy. In addition to its portfolio, the fund has an options collar on the S&P 500 Index. A collar is an options strategy in which a fund buys put options on the index and obtains the money for those put options by selling call options. In effect, this provides the fund with a great deal of downside protection since it is able to exercise the put option during falling markets to lose less money than it would have lost without the put option. However, this strategy also works in reverse as the fund will not gain as much as the index does during bull runs. This strategy served it well in 2022 as is evidenced by the fact that the portfolio delivered a better total return than the index, although the fund still lost money. It will also likely provide it with downside protection in case the technology sector has further problems, although at the moment it seems that the job losses are the direct result of the industry shedding its bubble-level excesses.

Distribution Analysis

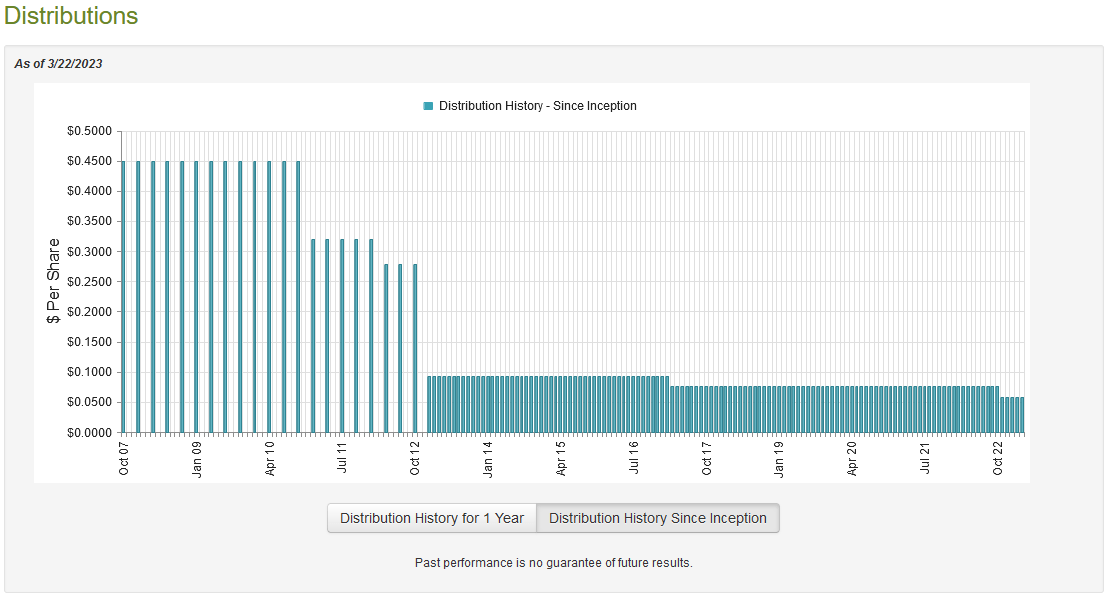

As stated earlier in this article, the primary objective of the Eaton Vance Risk-Managed Diversified Equity Income Fund is to provide its investors with a high level of current income and gains. The fund pays both of these things out to its investors via its distributions. Admittedly, the companies in the fund's portfolio do not have especially high yields and many of them delivered rather disappointing performances in 2022, but properly executed options strategies can be quite profitable in flat to declining markets. This is perhaps less true for collar strategies like the one used by this fund because of the fact that some of the premiums received are spent on buying a protective put, but it still delivers some additional potential for income. In short, this fund can generally be expected to pay out a reasonable distribution from all of these different sources of incoming money. That is certainly true as this fund pays out a monthly distribution of $0.0579 per share ($0.6948 per share annually), which gives it a 9.23% yield at the current price. Unfortunately, the fund recently broke its long track record of consistency and cut its distribution back in November:

{kind=link}

The fact that the fund recently cut its distribution may serve as a bit of a turn-off for those investors that are looking for a stable and secure source of income. Its track record prior to that was respectable though as the fund had maintained its distribution for several years. The incredibly poor performance of the mega-cap technology companies that dominated its portfolio last year probably had something to do with this cut, which is one of the reasons why that portfolio has concerned me for quite some time. Fortunately, though, anyone buying the fund today does not have to worry too much about the fund's past performance. This is because someone buying today will receive the current distribution at the current yield. As such, the most important thing is the fund's ability to sustain its distribution at the current level.

Fortunately, we have a fairly recent document that we can consult for this purpose. The fund's most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, it will give us a pretty good idea of how well the fund navigated one of the most turbulent years in the past decade. In addition, this report is much newer than the one that we had the last time that we looked at the fund so I am sure that the updated analysis will be welcome. During the full-year period, the Eaton Vance Risk-Managed Diversified Equity Income Fund received a total of $8,875,014 in dividend income and surprisingly no interest from its portfolio. It paid its expenses out of that amount, which left it with $2,307,547 available for shareholders. As might be guessed, that was nowhere close to enough to cover the $58,495,689 that the fund paid out in distributions during the year. At first glance, this may be concerning as the fund's net investment income was nowhere near sufficient to cover the distribution that it pays out.

However, the fund does have other means through which it can obtain the money that it needs to pay for its distribution. For example, it might have had capital gains that it can pay out. It also might have income from its options strategy, which is considered either capital gains or return of capital depending on the situation. The fund failed miserably at this over the course of 2022, which is admittedly not surprising considering its technology-heavy portfolio and the weak market for such companies that year. The fund did manage to realize net gains of $34,275,880 but this was more than offset by $137,486,081 net unrealized losses. Overall, the fund's assets declined by $139,572,619 after accounting for all inflows and outflows. That is a clear sign that it failed to cover its distribution over the course of the year, which certainly explains the distribution cut. The fund may be able to maintain the new one, but we will have to wait and see how it performs this year. So far though, things are looking better due to the strong performance of a few of the fund's largest holdings so far this year.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Risk-Managed Diversified Equity Income Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of March 22, 2023 (the most recent date for which data is currently available as of the time of writing), the fund had a net asset value of $7.95 per share. However, the shares currently trade at $7.58 per share. This gives the fund's shares a 4.65% discount to net asset value at the current price. This is a better price than the 3.35% discount that the shares have traded at on average over the past month, although it is still not an especially large discount. However, the price is not unreasonable here.

Conclusion

In conclusion, the Eaton Vance Risk-Managed Diversified Equity Income Fund is one of the more interesting funds in the market due to its collared options strategy. I know of no other fund that uses such a strategy. However, its portfolio continues to look incredibly strange for a fund that is ostensibly targeting income since it is heavily invested in technology, and that options strategy limits its capital gains potential! The fund's portfolio did manage to outperform the S&P 500 last year though, so the collar strategy did work to protect it from the worst of the carnage. The fund is trading at a reasonably attractive price right now, but it failed to cover its distribution last year. It remains to be seen how well the fund will cover its new reduced distribution this year.

For further details see:

ETJ: Outperformed S&P 500 Last Year But Still Failed To Cover The Distribution