GRBK - Even After An Impressive Rally Green Brick Partners Is Still Cheap

Summary

- Green Brick Partners continues to trade for less than 5x earnings, despite impressive growth and resiliency in a tough market.

- Shares could face stagnation in the near term as 2023 presents headwinds for homebuilders, but expansion into Austin, Texas gives me confidence that the company can continue to grow long term.

- With a substantial support level around $20 per share, the technical picture looks attractive and valuation metrics indicate that even after a nice rally, the stock is still quite cheap.

- Mortgage demand is starting to perk up in the new year, but interest rates and inflation are major issues especially for millennial homebuyers.

- In this article, I will also touch on past articles and offer insight into when buying Green Brick Partners stock may be most advantageous for investors.

Investment Thesis

Green Brick Partners ( GRBK ) was one of the first new stocks I added to my portfolio in 2022, after rising interest rates spooked the market and caused homebuilders to crash. Along with many other companies, mortgage REITs took an especially hard hit due to collapsing book values and strong selling pressure combined with negative sentiment in the market. As it often goes, buying when there is blood in the streets is the best way to make money for an investor with a long-term mindset.

In my first article on this subject, "Playing The U.S. Housing Market: Green Brick Partners For Growth and AGNC For Income", I noted that GRBK was trading at a remarkably cheap valuation. This still rings true, as the company has managed to grow earnings and revenues in 2022, but the earnings multiple has actually contracted from 5.9 to 4.7. Book value has barely changed, having gone from 1.2x to 1.3x in the last year, and the price-to-sales ratio having stayed pretty much exactly the same at 0.7x. On an EV-to-sales metric, the stock has also become cheaper compared with last year.

While the share price has gone up nearly 25% since my initial article on the company, the market has not rewarded the stock with higher multiples on earnings or revenues. 2023 could present with some headwinds, however, and the market is continuing to price in risks. Additionally, with fundamentals continuing to improve, this shows that the market is still underestimating Green Brick Partners and the company's ability to deliver outsized returns to shareholders over the long-term.

Introduction

Investing in the housing market was somewhat scary for many market participants last year, but the proof is in the pudding, as both of my picks (AGNC Investment (AGNC) and GRBK) have beaten the market over the short term timeframe. It may not seem so, but AGNC has indeed also outperformed, producing a total return of -1.59% since March 18th, 2022, compared with a return of -10.37% for the S&P 500. While it has not been a full year since my initial article on this subject, it appears as though my strategy of splitting the risk between Green Brick Partners and AGNC for both growth and income has worked. While GRBK has outperformed the market handily, the good news is that this trade is not over yet, as I plan to continue investing in both companies over the long-term.

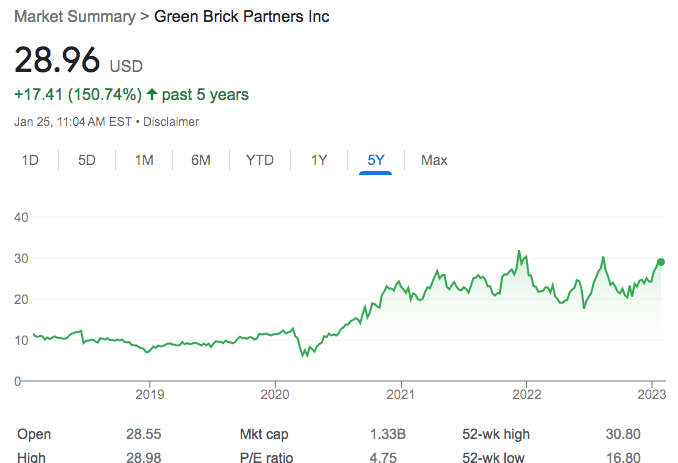

Green Brick Partners provided many opportunities for investment in 2022, especially after an analyst downgrade in mid June which pushed the price below liquidation value and set up for an impressive 75% rally over the next several months. After another price correction which saw the stock test the important $20 technical level in October, the stock has rallied approximately 45% to within just a few dollars of a new 52-week high.

{kind=link}

As we can see from the above chart, the stock is nearing a long-term technical breakout and has managed to hold above the $20 price level since reaching a new trading range in late 2020. While the $30 price level has acted as resistance in the past, it will be telling to see if, or when this new trading range between $30 and $40 could occur.

With fundamentals improving and the market still valuing GRBK under 5x earnings, I do not see much of a reason that the stock would falter and begin to trade back towards $20 or below. It would take much more negative sentiment from analysts, or perhaps some drastic earnings and profit misses in a deteriorating housing market to see that type of decline in share price. With an uncertain and rapidly changing macro environment for equities still in play, there are however substantial risks for the company related to inflation, higher interest rates, and more headwinds in 2023. Despite these headwinds, many analysts are beginning to turn bullish in the new year.

2023 Breathes New Life Into Housing, But Risks Remain

Many analysts were resoundingly negative on housing in 2022, but some are starting to turn more bullish now that mortgage rates have been on a decline. As of January 25th, 2023, it was reported that weekly mortgage demand had jumped 7% as rates dropped to mirror levels seen from last September.

Even though rates are still much higher than in previous years, demand has been fairly steady and the recent uptick has made homebuilders look even more enticing for the year 2023. Inventory is still low, but companies are stepping up to fill the void in housing. Green Brick Partners is just now getting their foot in the door in the new market of Austin, Texas, with sales expected in the Spring. This is one of the many reasons that I chose to invest in Green Brick, and higher average home prices in this area should bring even higher margins and revenues for the company over the coming quarters. Number of homes sold may be less, but the company is prioritizing earnings over sheer revenue growth this time around.

Risks remain however, as the housing market is in a tug-of-war with affordability, inflation, and the direction of future interest rates causing many buyers to be cautious.

A recent survey found that over 92% of millennials say inflation has impacted their homebuying plans, but surprisingly, many are not letting this stop them from entering the market altogether. While most younger home buyers are rethinking their plans, this usually includes purchasing a slightly smaller home, or buying a "fixer-upper" instead of abstaining from the housing market entirely. In the survey, around 36% of participants answered that they were simply "spending more than expected," which shows that over a third of millennials know how expensive buying a home is, but they are willing to buy anyway, assuming that the days of mortgage rates at 3% are a thing of the past.

The interest rates could absolutely fall more over the coming 12 months, but I tend to agree that a normalized rate of between 5 and 6% is likely, and higher rates for longer seem to be the consensus. While it is debatable if the broad market also sees this to be the reality, I am in the camp of rising interest rates and a potentially ugly downturn for the economy in general. While I do not expect a recession to be catastrophic, for inflation to get back to a 2% rate by January 2024, we would need to see quite a bit of demand destruction. With this demand destruction, homebuilders would, in theory, begin to trade at dirt cheap valuations once more, and I would be adding to my positions aggressively. We are not at this crossroads yet, so holding off on buying more shares in stocks such as Green Brick Partners is likely advantageous.

Substantial Inventory Levels, Changing Dynamics

Green Brick Partners has very substantial inventory levels, with developed land and houses ready to sell over the next full year. Historically, Green Brick was a company in which shareholders essentially got paid in land, as the stock does not pay a dividend and earnings are used primarily to acquire more land for development. This process of acquire land, develop, and sell homes for profit, then repeat has worked increasingly well for the company over the years. Growth has been impressive, but growth at all costs cannot last forever.

As of recently, Green Brick's management has shown a change in the dynamics of the business, as they do not currently have a need to buy land to grow, and they don't plan to buy much land until later on in 2023. This means that with substantial enough inventory levels, shareholders might begin to see earnings paid out in the form of dividends or special dividends, rather than just extra cash sitting on the balance sheet. This potential change in dynamics is something to keep in mind, however, as risks of rapidly falling housing prices could mean that Green Brick would have to liquidate homes for much less than they were originally planning for. In my opinion, a significant downturn in housing prices is not very likely, and any change in sentiment would likely bring about another long-term buying opportunity for the stock.

While the company paying out a dividend or special dividend could also be unlikely, a change in dynamics for shareholders is one thing that is important to note as a possibility here. As a shareholder in Green Brick Partners, I am perfectly fine with getting 'paid in land,' and I think this is a good and constructive way to think about an investment in the company. While growth may not last forever, sustainable growth is something that I look for in many companies that I own, as unsustainable growth can have disastrous consequences for shareholders. I believe that over the long-term, Green Brick Partners can manage the changing market environment well, and reward shareholders accordingly.

Conclusion

Even after a nice rally, Green Brick Partners remains a remarkably cheap stock. With a P/E ratio of 4.7, a price-to-book ratio of 1.3, and an EV-to-sales ratio of 0.9, the stock seems even cheaper than last year, despite a roughly 45% rally since April 1st, 2022. With an average price on that date of around $20, the stock has shown a bounce off of the important technical level, and has rallied impressively every time the stock trades for below liquidation value. The new year has breathed new life into homebuilders, and the stock is setting up for a technical long-term breakout above $30 per share. I believe that in the near term, this resistance level may prove to be sticky and the shares are due for a period of stagnation. However, Green Brick Partners remains a great company that is beginning to show signs of changing dynamics for shareholders. I currently rate GRBK as a Hold, but would be a buyer on the next large pullback in the shares under $25.

For further details see:

Even After An Impressive Rally, Green Brick Partners Is Still Cheap