SPY - EWJ: Japan Will Need More Than Just Ultra-Loose Monetary Policy And Corporate Reforms

2023-08-17 10:17:01 ET

Summary

- Investors are hopeful that ultra-loose monetary policy and corporate reforms will revive Japan's stagnant economy.

- Investors may believe that even if Japanese equities were to produce mediocre returns, the potential for substantial FX gains would justify taking the risk.

- However, we warn that investors ought to be more conservative with their expectations when assessing the potential impact of ambitious reforms in Japan.

- Without bold policies to reverse Japan's deteriorating demographics, piecemeal attempts to stimulate growth and reform corporate governance will likely fall short of investor expectations.

For decades, policymakers have explored and implemented a variety of economic policies in an attempt to revive growth in Japan. However, these policies have either failed to generate sufficient momentum to jump-start growth or have been unable to sustain growth beyond the initial burst of activity. Hence, it is surprising to see an increasing number of investors who are feeling hopeful that ultra-loose monetary policy and the promise of corporate reforms will finally cure Japan of economic stagnation.

In this article, we re-evaluate Japan's economic outlook by examining key factors that have recently reignited investor interest in Japanese equities. We also revisit some of the structural macroeconomic challenges that continue to impede the country's recovery. Finally, we address the critical question of whether investors should invest in Japanese equities today or whether they would be better off waiting on the sidelines.

Ultra-Loose Monetary Policy Is Looking Promising

The adage "desperate times call for desperate measures" certainly rings true in the context of economic policy. History has shown that piecemeal reforms and half-hearted measures are rarely effective in engineering major macroeconomic shifts. Many prominent economists have also highlighted the need for quick and bold policy action in order to tame animal spirits before they spiral out of control.

In Japan's case, the policies implemented to revive growth after the asset bubble burst in the early 1990s were not only implemented too late but also inadequate in many areas. This is why economists argue that Japan will need to implement much bolder measures today, given how economic stagnation has become so deeply entrenched in the psychology of its citizens and corporate leaders. Behaviours, including excess savings at extremely low interest rates, high risk aversion, disillusionment to growth, as well as the puzzling phenomenon of businesses ' reluctance to raise prices and wages, highlight the need for bold policy action.

For the first time in decades, Japan's economic revival is starting to look promising for investors. The weak Japanese yen has boosted exports and tourism, and inflation is finally encouraging companies to raise prices and wages. The cheap yen, coupled with expectations that the Bank of Japan (BoJ) will soon unwind its ultra-loose monetary policy, has attracted foreign investors seeking to capitalize on the potential for yen appreciation and Japan's renewed growth story. In recent months, major investors such as Singapore's sovereign wealth fund GIC, Blackstone, and Warren Buffett's Berkshire Hathaway have all announced fresh investments in Japan.

The chart above shows how the yield spread between U.S. Treasuries and Japanese government bonds has widened since 2021, and how closely correlated the yield spread is with JPY weakness. Therefore there are good reasons to believe that as both the Fed and BoJ unwind monetary policy, we should see the yield spread narrow and JPY appreciating against the dollar. We think this is one of the main reasons why Japanese equities have become so compelling for investors. Indeed, even if Japanese equities produce mediocre returns, the potential for substantial FX gains may justify taking the risk.

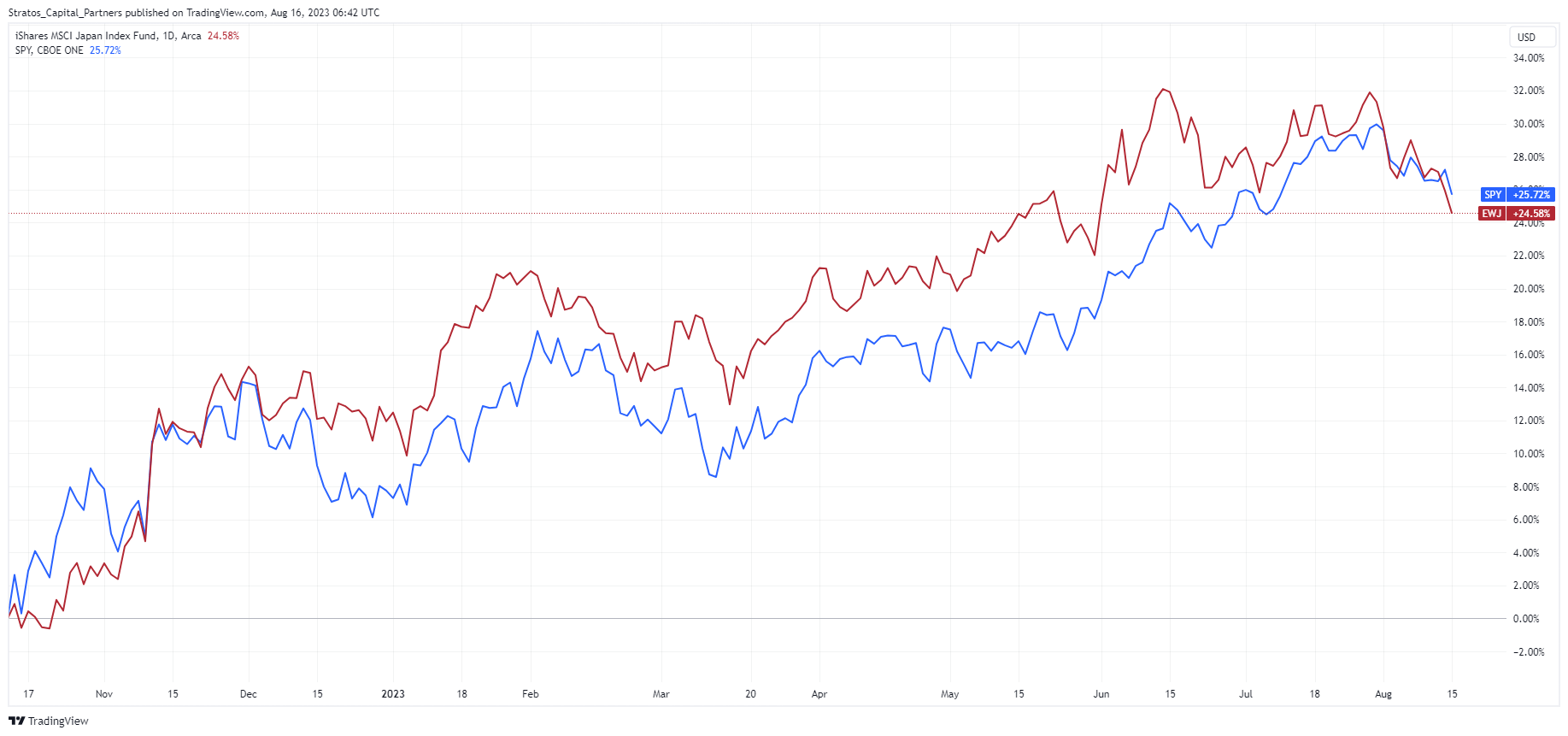

Thus, it is no wonder why the iShares MSCI Japan ETF (EWJ) has performed equally well compared to the SPDR S&P 500 ETF Trust (SPY) since the equity market bottomed in October 2022. Despite Japanese equities having persistently underperformed U.S. equities in terms of returns on equity ((ROE)) over the years, investors are still willing to invest. Presumably for potential FX gains.

{kind=link}

Corporate Reforms An Added Boost To Japan's Revival

Efforts to revive Japan's economy are also accompanied by concrete policies aimed at driving corporate reforms and raising ROEs for Japanese listed companies. This is a crucial element in our opinion as foreign investment in Japan will be helpful in providing an added boost to the country's efforts to sustain long-term growth.

The Tokyo Stock Exchange ((TSE)) which operates Japan's core financial exchange markets and administers the country's corporate governance standards, has recently introduced meaningful changes to its market restructuring initiative. One of the key measures implemented will require listed companies that are trading at extremely low price-to-book ratios (P/B) to provide adequate reasons justifying their inability to comply with TSE's guidelines to improve capital efficiency and profitability.

According to documents published by TSE, around 50% of some 1,800 companies listed on the prime market are generating ROEs of under 8% and trading below book value. A low ROE generally reflects low profitability, usually as a result of inefficient management of capital or a lack of growth. Crucially, TSE has warned that companies that fail to comply with the new corporate governance standards and guidelines could potentially be delisted by 2026 .

Policy Is One Thing, Implementation Another

Sound economic principles and well-designed policies aside, successful reforms also often have to wrestle with the harsh realities of implementation. Governments in democratic and capitalist nations typically have limited powers to directly intervene in the affairs and management of private sector companies. As a result, policies aimed at driving corporate reform are often subjected to intense lobbying, extensive revisions, and long delays in implementation.

Policymakers also prefer to make multiple small adjustments when imposing new rules and requirements on companies instead of making bold sweeping policy changes. This is because reforms are often costly to companies and would require committing additional resources to adapt to changes. So it is understandable that policymakers are careful not to place unnecessary administrative burdens on companies. Additionally, company executives tend to be more receptive to small and manageable regulatory demands that are spread out over time instead of drastic changes.

This presents a serious dilemma for policymakers: bold policies risk facing heavy resistance from various stakeholders, but piecemeal policies would fail to make a meaningful impact. Hence, investors ought to be more conservative with their expectations when assessing the potential impact of ambitious reforms in Japan.

While we appreciate the Japanese government's efforts to drive corporate reform, we suspect that much more will be needed to achieve meaningful change in Japan's corporate culture. While the government's guidelines are a step in the right direction, they are unlikely to achieve immediate results in boosting ROEs. We argue that the problems associated with the lack of growth and profitability in Japan are much more structural in nature.

For example, large Japanese companies have demonstrated a reluctance to take risks or adopt new ideas to drive growth in the past. Japanese companies also tend to be more focused on maintaining long-lasting relationships with their customers and business partners, even at the expense of sacrificing profits. This sort of corporate culture is deeply ingrained and may prove difficult to change with piecemeal reforms.

Demographics, Demographics, And Demographics

Any discussion of long-term economic prospects would be rather pointless without an adequate view of a country's demographics. We recently published a critical assessment of China's economic prospects, highlighting the country's rapidly deteriorating demographics and how it is sliding into a period of stagnant economic growth. Japan too is struggling due to deteriorating demographics. And we believe that is why repeated attempts to reignite economic growth in the past have failed to pull Japan out of stagnation.

Below is a series of charts comparing the expected evolution of Japan's population pyramid to that of China and the U.S. Notice how Japan and China's population pyramids are projected to form a widening top and a narrowing bottom, reflecting an ageing population being supported by a shrinking working-age population. This is likely to drag on disposable incomes and domestic demand, while potentially adding inflationary pressures due to reduced productivity.

U.S. Census Bureau, Bloomberg

Since labour is a core factor of production in long-term economic growth models, deteriorating demographics are usually a death sentence for growth. Even though we are of the view that Japan is in a better position to address its demographic challenges compared to China, the Japanese government has so far failed to demonstrate the political will to be bold on immigration reforms.

Make no mistake, Japan's major cities such as Tokyo and Osaka have regularly been featured among rankings of the most liveable cities over the years. Japan is also among the top tourist destinations in Asia, attracting millions of visitors from around the world each year. Thus, attracting skilled migrants should not be too much of a problem. Many foreign expatriates would also jump at the opportunity to work and live in the country if only immigration rules were much less stringent.

EIU Global Liveability Index 2023, Statista

From our standpoint, policies that would ease immigration to Japan remain the most unexploited but also the most powerful lever that Japanese policymakers could pull to ignite growth. Without bold policies to reverse Japan's deteriorating demographics, however, we are afraid that piecemeal attempts to stimulate growth and reform corporate governance will likely fall short of investor expectations.

Hopes for a lasting economic revival in Japan are certainly brewing for some major investors. Perhaps these investors know more than us. But judging from the many false dawns we have repeatedly witnessed for Japan in the past, we still think we are better off waiting on the sidelines.

For further details see:

EWJ: Japan Will Need More Than Just Ultra-Loose Monetary Policy And Corporate Reforms