CA - Exchange Income: New Long-Term Contracts And Record Backlog Imply Undervaluation

2023-09-04 11:00:42 ET

Summary

- Exchange Income Corporation expects passenger growth and earnings improvements from a long-term contract with the Province of Manitoba.

- The Multi-Storey Window Solutions division has a record CAD1 billion backlog, which could lead to future FCF growth.

- Labor shortages and supply chain disruptions pose risks, but I believe the company is undervalued and is part of an industry with low EV/EBITDA levels.

Exchange Income Corporation ( OTCPK:EIFZF ) recently delivered an optimistic outlook that included passenger growth and all-time record CAD1 billion backlog of the Multi-Storey Window Solutions division. I expect a beneficial effect from the long-term contract by the Province of Manitoba, which is expected to improve 2024 and 2025 earnings. I also see risks from labor shortages or supply chain disruptions; however, I believe that EIFZF could trade at a higher price mark.

Company Overview

With a diversified investment portfolio of opportunities in the aviation, aerospace, and manufacturing markets, Exchange Income is a corporation oriented towards the acquisition of consolidated businesses with decent capital flows in specific market niches. The named investment areas are reported as a segment of operations: aviation and aerospace on the one hand and the manufacturing industry on the other hand.

In the first of these areas, some of the companies acquired by the company are Calm Air, Keewatin, Carson, Regional One , and Crew Training International. This diversification of businesses allows Exchange Income to be present in all the areas of the industry, such as airline scheduling, parts distribution, repair services, cargo services and charter, training services for pilots, and industry workers among others.

The manufacturing segment includes Quest, Northern Mat, WesTower, Overlanders, Ben Machine, and Alberta Operations, to name a few of the companies owned by the company. In the same way, the function and services are highly diversified, with production for communications infrastructures and networks, windows for family homes, precision parts for different markets, manufacturing of steel tanks, production of integrated systems for the agro-industrial area, and systems for waste management industries.

Balance Sheet

In the last quarter , Exchange Income reported a meaningful increase in the total amount of assets driven by increases in accounts receivable, inventories, capital assets, and goodwill. Even considering that the total amount of cash decreased, the balance sheet is definitely expanding, which most investors may appreciate.

As of June 30, 2023, the company reported CAD50 million in cash, accounts receivable of CAD519 million, and inventories close to CAD384 million. The current assets/current liabilities ratio stands at close to 2x, so in my view liquidity does not seem to be an issue at the moment.

Source: Quarterly Report

The total amount of liabilities includes accounts payable of CAD413 million, with deferred revenue of CAD71 million, current portion of right of use lease liability of CAD33 million, and total current liabilities of CAD579 million. Finally, with long-term debt close to CAD1.26 million and convertible debentures of CAD132 million, total assets stood at CAD2.594 billion.

Source: Quarterly Report

Valuation

My Base Case Scenario

I believe that the recent outlook provides room to be optimistic about the future. In a recent quarterly report, the company noted that the company will most likely benefit from passenger growth at the airlines and growth in the rotary wing sector. Besides, the company appears to be dealing well with labor shortages and other risks that were highlighted in the past. Under my financial model, the flow of passengers will continue to trend north. Here is a related excerpt from the latest quarterly report.

So far this year, Essential Air Services has been buoyed by the return to more normal passenger volumes at the airlines and by growth in the rotary wing sector across all customer segments. We expect that these conditions will continue to have a positive influence on results for the foreseeable future. Challenges related to labour shortages, amplified by the introduction of new pilot fatigue and duty regulations, and rising costs remain but the companies continue to implement measures to mitigate their impacts. Source: Quarterly Report

It is also worth noting that we can expect sales growth thanks to the long-term contract by the Province of Manitoba and a beneficial impact on earnings from 2024 and 2025. In this regard, the company provided a full explanation in the recent quarterly report.

Keewatin Air was awarded a long-term contract by the Province of Manitoba to provide critical care fixed wing medevac coverage for the whole province. In fact, the medevac contracts in particular will have only a minimal impact in 2024, with the first meaningful contribution to earnings beginning in 2025. Until then, the major impacts will be the investment in aircraft and facilities to execute on the contracts. Source: Quarterly Report

Besides, I am quite optimistic about the Multi-Storey Window Solutions division, which continues to improve. In my view, if the backlog continues to remain at record high levels of close to CAD1 billion (as stated by the company in the earnings call, see quote below), I believe that more investors may have a look at the company. The demand for the stock could push the stock price north.

Looking further out, the backlog remains constant at record high levels of approximately $1 billion. Inquiry activity has continued to be brisk but conversion to committed contracts is mixed, particularly in the US, largely due to uncertainty over the future direction and impact of interest rates. Source: Quarterly Report

Exchange Income's strategy is based on inorganic growth. The company looks for acquisition opportunities for niche markets, which will most likely lead to FCF margin growth. The businesses acquired have an autonomous operation, and the strategies in this case belong to the board of directors of each company based on the conditions of the market in which they participate. Under my DCF model, I assumed that this strategy will continue to be successful in the coming years. It is also worth noting that Exchange could receive more debt financing as the leverage ratio currently stands at 2.39x, but could go up to 4x.

As at June 30, 2023, the Corporation’s key financial covenant for its credit facility is its senior leverage ratio, and its facility allows for a maximum of 4.0x. The Corporation’s current leverage ratio is 2.39x. Source: Quarterly Report

I believe that management knows well how to buy and integrate new businesses. To give a few examples of previous acquisitions, during 2022, the company acquired a small business that is a leader in the provision of ground and air emergency medical services in Northern Alberta as well as achieved the integration of Northern Mat, a company that provides access solutions for the timber market within Canada. In this sense, Exchange Income has shown successful statistics on its growth strategy.

Source: YCharts

Assumptions

I included a growth rate close to 17% with an EBIT margin of 11%, tax rate close to 25%, working capital/sales of 5%, and capex/sales of 0.16%. Besides, I also assumed a WACC of 4.4% and depreciation/sales of 16%.

For the calculation of the cost of capital, my CAPM model included a risk free rate close to 2.8%, a beta of 0.59, market risk premium of 5.9%, and an implied WACC of 4.4%. I believe that my numbers are conservative.

Source: Author's Calculations

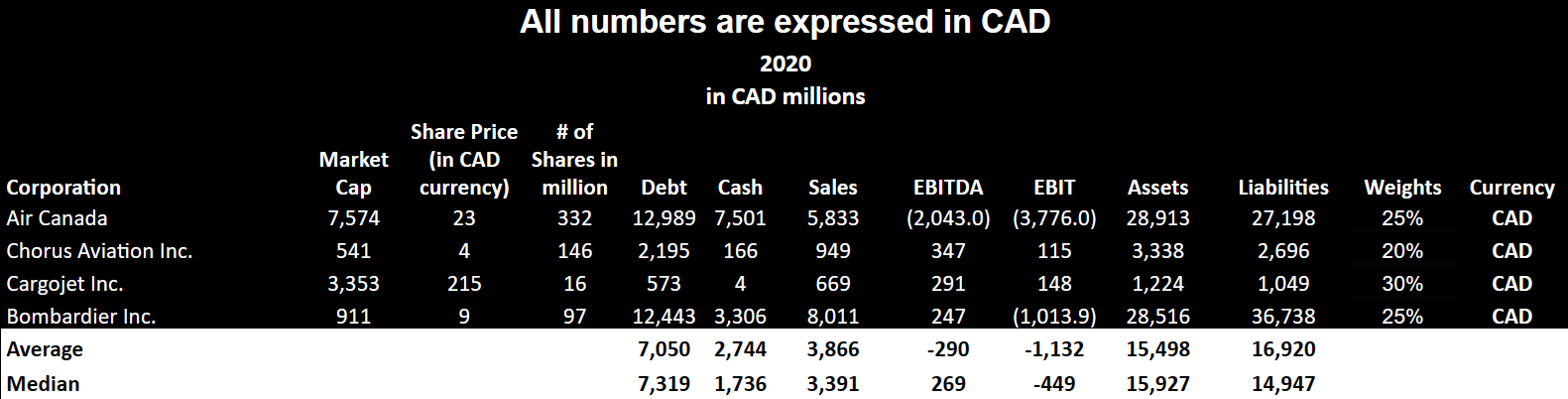

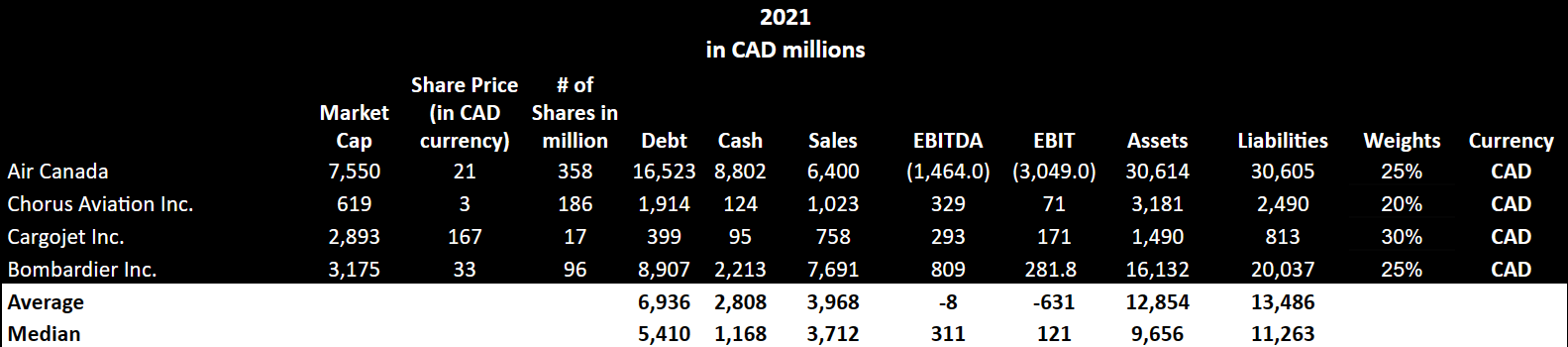

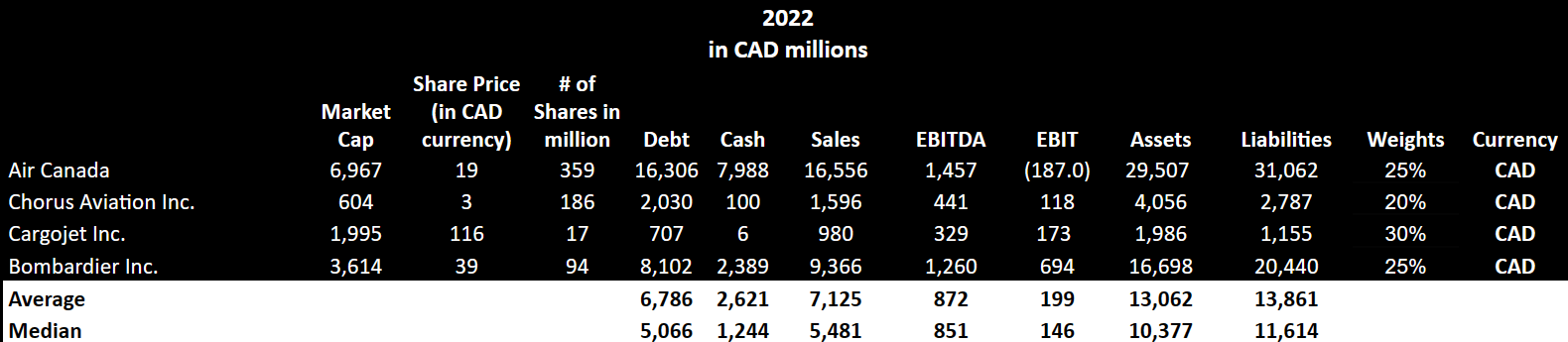

For the calculations of such assumptions, I studied carefully the figures reported in 2020, 2021, and 2022, so my figures are not really far from what the company reported in the past.

Source: Author's Calculations

Source: Author's Calculations

The results of the previous assumptions include 2027 sales of CAD4514 million, EBIT close to CAD496 million, adjusted operating profit worth CAD372 million, and depreciation of about CAD733 million. Finally, with changes in working capital close to CAD225 million and capital expenditures of CAD733 million, the implied FCF would be $147 million.

Source: Author's Calculations

With a WACC close to 4.4%, I obtained an implied enterprise value close to CAD4.764 billion. Subtracting net debt close to CAD1.62 billion, the implied equity would be CAD3.144 billion, and the fair price would be close to $74 per share.

Source: Author's Calculations

Bearish Case Scenario (with an increase in cost of capital: WACC Of 5.1%)

Some investors out there may have a look at the interest included in the convertible debentures. They may be willing to have another case scenario with a cost of capital close to 5%-5.75%. With the recent increase in the risk-free rate and the recent volatility in the interest rates, I cannot blame them.

Source: Quarterly Report

With the previous table in mind, I made another case scenario, in which the company suffers a period of stock volatility, or sudden increases in the interest rate push the cost of capital to around 5.4%. Note that all the other variables that I included in the previous case scenario remain the same. Sales growth, EBIT margin, tax rate, working capital/sales, capex, and depreciation remain approximately the same.

Source: Author's Calculations

Under these conditions, I obtained an equity valuation of close to $2.2 billion and an implied fair price of close to CAD52 per share.

Source: Author's Calculations

Peers

Due to the diversification of the business, it is difficult to synthesize a single market in which competition factors exist for this company. In the aerospace market and its niches, the appearance of new competitors or infrastructure changes in the original manufacturers that serve them could change the current logic in the regions of Canada, where the company actively operates. For Regional One, the largest of the companies owned by Exchange Income in this sector, competition is high at a domestic and international level, with greater production capacities that allow them to offer aircraft parts at significantly lower prices.

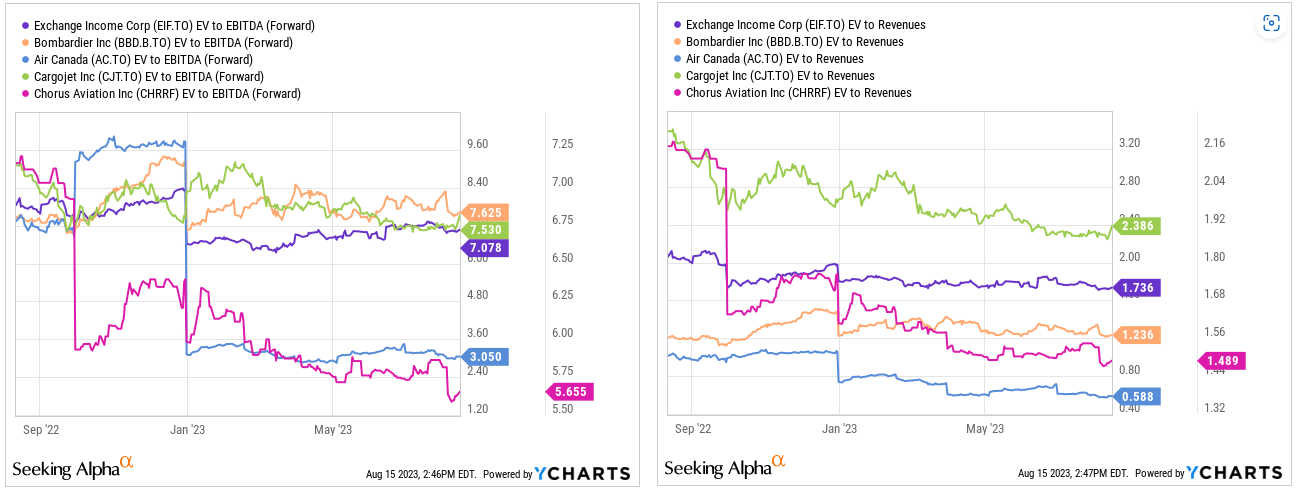

The peer group that I designed included Air Canada ( OTCQX:ACDVF ), Chorus Aviation ( OTCPK:CHRRF ), Cargojet ( OTCPK:CGJTF ), and Bombardier ( OTCQX:BDRBF ). Many of these companies are larger than Exchange Income, so they could be trading at larger EV/EBITDA and EV/Sales.

{kind=link}

{kind=link}

{kind=link}

With that about the information of the peer group, I believe that Exchange Income is still not the most expensive company in the group. If we look at the valuation of peers, there is room for improvement in terms of market capitalization. It is also worth noting that I do not believe that the peer group is trading at expensive valuations. Most competitors are trading at 7x-3x, which does not seem at all as expensive as other companies in different industries.

{kind=link}

Source: YCharts

In the manufacturing segment, although competition is high, it is less and relative to specific product markets. So, in this sense, the company's participants maintain a differential on the added value of their products and a positive competitiveness margin at regional level.

Major Risks

Despite the high diversification, the company's operations are concentrated on the North American market, generating a direct dependence on its economic conditions. In addition, with regard to its aerospace segment, any decrease in demand, disruption in the appearance of new competitors, and exceptional situations could affect the operations of its subsidiaries, consequently the financial results of Exchange Income.

In the same way, the concentration of its clients for each segment is high, and a cut in relations with these represents a latent risk factor. Of course, due to the nature of the company, the risk about acquisition strategies, both in their selection and future integrations, and their operation is the general framework of day-to-day operations.

Emphasizing the positive financial results that the company has shown, Exchange Income presents itself as a good low-risk investment opportunity, both for short-term and long-term investments, although a high return is not to be expected in none of these cases.

Takeaway

Exchange Income expects to continue to benefit from passenger growth, and may see earnings improvements from 2024 and 2025 thanks to the long-term contract by the Province of Manitoba. The CAD1 billion backlog of the Multi-Storey Window Solutions division is also worth noting, which appears to be at record levels, and may improve future FCF growth. Labor shortages, supply chain disruptions, and other risks could bring some FCF volatility; however, I believe that the company is quite undervalued. Besides, it appears to be part of an industry that does trade at low EV/EBITDA levels.

For further details see:

Exchange Income: New Long-Term Contracts And Record Backlog Imply Undervaluation