MSFT - EXG: Some Improvements But Time Will Tell

Summary

- EXG aims to provide its investors with a high level of income through capital gains and dividends.

- The fund's portfolio consists of a lot of stocks with very low or non-existent dividend yields, making it highly reliant on capital gains.

- The portfolio has improved somewhat since we last looked at the fund but it could be better in the current environment.

- The fund had to cut its distribution in November because of overdistributing. It is uncertain how sustainable the new distribution will be.

- The fund's price is reasonably attractive and provides it with some margin for error.

Without a doubt, one of the biggest problems facing many Americans today is the pervasive inflation that has been ravaging the economy over the past year. This inflation has been causing problems with most people’s budgets and has forced a substantial number of people to take on second jobs or enter into the gig economy. In fact, according to a recent Prudential Pulse survey , roughly 81% of Generation Z members and 77% of Millennials have either entered or are considering entering the gig economy simply to obtain the extra money that they need to keep their bills paid. In fact, as I pointed out myself, the current low unemployment rate and strong job numbers appear to be largely caused by people taking on additional work simply to keep food on their tables.

Fortunately, as investors we do not need to resort to such extremes as we can put our money to work for us in order to earn extra income. One of the best ways to do this is by buying shares of a closed-end fund that is focused on the generation of income. These funds are nice because they provide easy access to a professionally-managed and diversified portfolio of assets that can in most cases boast a higher yield than any of the underlying assets.

In this article, we will discuss the Eaton Vance Tax-Managed Global Diversified Equity Income Fund ( EXG ), which is one closed-end fund that falls into this category. This fund boasts an 8.37% yield at the current price so it certainly has a yield that is reasonably decent for the generation of income. I have discussed this fund before but a few months have passed since that time and a few things have changed. This article will therefore focus specifically on these changes and provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the Eaton Vance Tax-Managed Global Diversified Equity Income Fund has the stated objective of providing its investors with a high level of current income and gains. This is not exactly unusual as most income-focused closed-end funds will have these objectives. This is because equities provide their returns both in the form of capital gains and dividend payments to investors. With that said, some of the most popular common equities in the market over the past several years have had minimal or non-existent dividends. Even those equities that do have dividends generally do not have high ones unless they are in the traditional energy sector. This is evident in the fact that the S&P 500 Index ( SPY ) only yields 1.58% as of the time of writing. That is substantially lower than the 4% yield that is now available in money market funds and it certainly does not provide a return commensurate with the risk of choosing equities over safe money market instruments. With that said, what this fund is essentially doing is trying to get a certain amount of dividends as well as realizing both short- and long-term gains with the goal of distributing the profits to its investors.

The fund has a surprising amount of low-yielding stocks in the portfolio for an income-focused fund. I pointed this out the last time that we looked at it. Here they are:

| Company |

| Portfolio Weighting |

| Dividend Yield |

| Microsoft ( MSFT ) |

| 4.29% |

| 1.12% |

| Alphabet Class C ( GOOG ) |

| 3.24% |

| 0.00% |

| Apple ( AAPL ) |

| 2.85% |

| 0.65% |

| Coca-Cola ( KO ) |

| 2.46% |

| 2.92% |

| ConocoPhillips ( COP ) |

| 2.43% |

| 1.70% |

| Nestle S.A. ( NSRGY ) |

| 2.40% |

| 2.42% |

| Amazon.com ( AMZN ) |

| 2.21% |

| 0.00% |

| EOG Resources ( EOG ) |

| 2.20% |

| 2.46% |

| Compass Diversified ( CODI ) |

| 2.01% |

| 4.66% |

| Boston Scientific Corp. ( BSX ) |

| 1.91% |

| 0.00% |

With the notable exception of Compass Group, there is nothing here that has a yield above 3.00%. That is surprising, particularly considering that the fund could easily include something like Devon Energy ( DVN ) which has a 9.06% trailing dividend yield. There are quite a few other shale energy companies with similar yields, which have delivered both capital appreciation and high yields over the past year. That would both boost the fund’s income and give it more gains than any of the mega-cap technology stocks that all fell over the past year by quite a lot.

With that said, there were a few improvements to this portfolio since the last time that we looked at it in November. In particular, the weightings allocated to the big technology names except for Microsoft decreased a bit. We also see that Walt Disney Company ( DIS ) was replaced with Boston Scientific among the fund’s largest holdings. It is questionable how much these changes were actually driven by the fund consciously changing its portfolio or by the fact that some of these stocks delivered better performance than others over the past three months. The fund only has a 27.00% annual turnover so I am inclined to believe the latter scenario and chalk this up to the technology companies continuing to underperform value names in the market. That is something that will probably be the case for a while since financially strapped consumers will not be buying expensive iPhones or shopping at Amazon as much as they once did. As such, it is nice to see value stocks having a bit higher weighting in the fund than they did, but it obviously still has quite a way to go.

The fact that the fund does have a low turnover is quite nice to see, though. As I just mentioned, the fund’s annual turnover sits at 27.00%, which is a pretty low figure for an equity fund. The reason that this is nice to see is that trading stocks or other assets costs money, which is ultimately billed to the shareholders. This creates a drag on the portfolio that makes management’s job harder because they have to cover these extra costs and still deliver a return that satisfies the shareholders. This is a task that few management teams can perform on a consistent basis and it is one of the reasons why passive index funds tend to outperform most actively-managed funds. This one, for its part, did outperform the S&P 500 Index in 2022 as it only lost 15.62% versus the 19.40% loss of the index. However, that is not exactly the best index to use for a global fund.

A look at the fund’s holdings will almost certainly make one thing that the fund’s “global” classification is a misnomer. After all, the only company in the largest positions list that is not American is Nestle. However, a look at the broader portfolio does tell a different story. In fact, only 54.18% of the fund is invested in American companies:

CEF Connect

The United States only accounts for a bit less than a quarter of the global gross domestic product so the fund is still overallocated to the nation relative to its actual representation in the global economy. With that said though, most global funds have a 60%+ weighting to the United States so this one is doing a bit better than most when it comes to achieving international diversification. The reason that this is important is because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will take an action that has an adverse impact on a company in which we are invested. The only real way to protect ourselves against this is by ensuring that only a small proportion of our portfolios is invested in any individual country. This fund is certainly doing that to a certain degree, which is nice to see.

Distribution Analysis

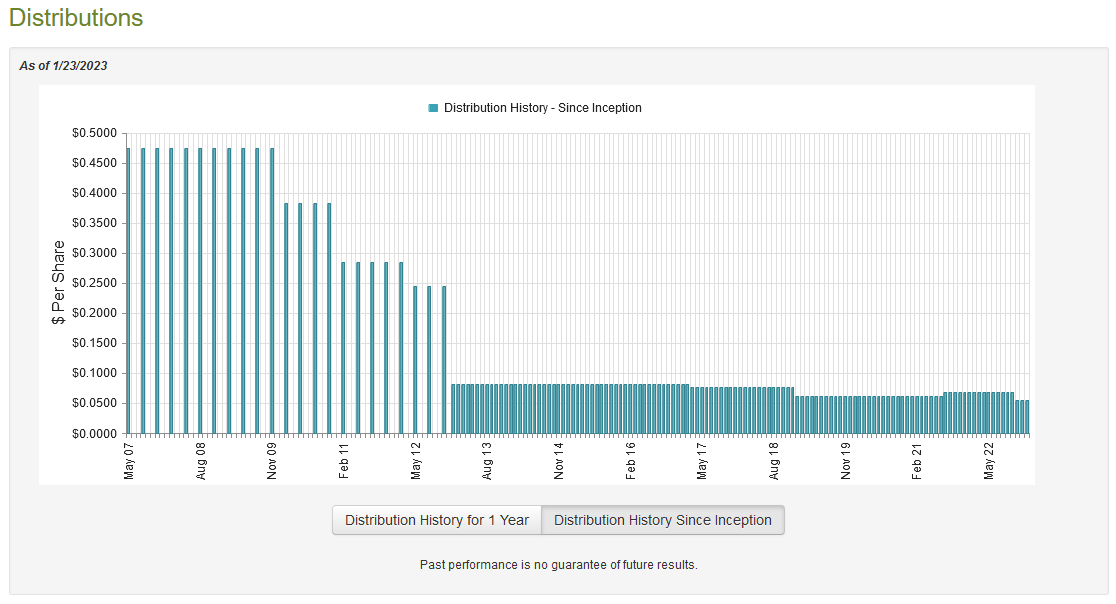

As stated earlier in this article, the primary objective of the Eaton Vance Tax-Managed Global Diversified Equity Income Fund is to provide its investors with current income and gains through the distributions that it pays out. The fund is certainly good at achieving this goal at first glance. It pays out a monthly distribution of $0.0553 per share ($0.6636 per share annually), which gives it an 8.37% yield at the current price. The fund’s distribution history leaves something to be desired as it has generally declined over the years with the most recent cut coming in November:

{kind=link}

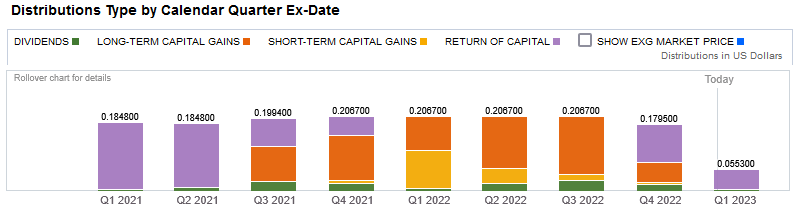

The fact that the distribution is now at its lowest level in history is likely to give potential investors pause. It also reinforces the comments that I made both in this article and in my previous one that the fund’s portfolio is not particularly well-structured for the objective that it is attempting to achieve. Another thing that will likely give more conservative investors cause for concern is the fact that the fund makes a significant number of return of capital distributions, although it did mostly pay out capital gains over the course of 2022:

{kind=link}

The reason why this may be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital, such as the distribution of unrealized capital gains. The fact that the fund was distributing capital gains may cast some concern on its ability to sustain the distribution since the fund has to actually generate sufficient capital gains to maintain the distribution and this is not always possible. We certainly saw this with the recent payout cut. As such, we will want to investigate the fund’s finances in order to determine exactly how it is financing these distributions and how sustainable they are likely to be.

Fortunately, we do have a very recent document to consult for that purpose. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. This is a much more recent report than we had available the last time that we looked at the fund and it should cast some light on the circumstances that resulted in the distribution cut. It may also tell us how sustainable the new distribution is likely to be. During the full-year period, the Eaton Vance Tax-Managed Global Diversified Equity Income Fund received a total of $50,148,221 in dividends and surprisingly nothing in interest. It did receive a small amount of income from lending out the securities in its portfolio though and reported a total income of $50,148,342 during the period. The fund paid its expenses out of this amount, which left it with $20,486,954 available for the shareholders. This was nowhere close to enough to cover the $248,779,255 that it paid out in distributions over the course of the year, however. This will undoubtedly be somewhat concerning at first glance.

However, the fund does have other methods that it can employ to obtain the money that is needed to cover the distribution. One of these is through capital gains but as might be expected, the fund failed miserably at this over the period. It did achieve net realized gains of $213,778,636 but this was more than offset by $759,647,383 net unrealized losses. Overall, the fund’s assets declined by $761,361,124 after accounting for all inflows and outflows. Thus, the fund clearly failed to cover the distribution. In fact, this performance was so bad that even its net realized gains plus net investment income was not sufficient to cover the distribution. That explains the distribution cut and the return of capital distributions. Time will tell if it can generate sufficient returns to maintain the distribution at the new level as it definitely will not be able to through dividends alone. Fortunately, January has been proving to be fairly strong in terms of market performance so hopefully, that will help somewhat.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Eaton Vance Tax-Managed Global Diversified Equity Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debts. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. That is fortunately the case here today. As of January 23, 2023 (the most recent date for which data is available as of the time of writing), the Eaton Vance Tax-Managed Global Diversified Equity Income Fund had a net asset value of $8.49 per share but the shares trade for $7.89 per share. This gives the shares a 7.07% discount to net asset value at the current price. This is a reasonable price to pay for the fund and it is better than the 5.86% discount that the shares have had on average over the past month. Overall, the price is fine today.

Conclusion

In conclusion, the Eaton Vance Tax-Managed Global Diversified Equity Income Fund is showing some improvements since the last time that we looked at it, although the worst-case scenario did generally play out. The fund’s high allocation to the mega-cap technology stocks caused it to have a poor enough performance that it had to cut the distribution. We saw the same thing happen to several other Eaton Vance closed-end funds recently. The fund appears to be more reasonable in terms of its portfolio now, although it does have some room for improvement. We will have to wait and see if it can generate sufficient capital gains to maintain the distribution at the current level but fortunately, the price is good enough to give it some margin for error.

For further details see:

EXG: Some Improvements But Time Will Tell